How Comcast’s Split Ends a Decade of Conglomerate Discount

18 mins ago

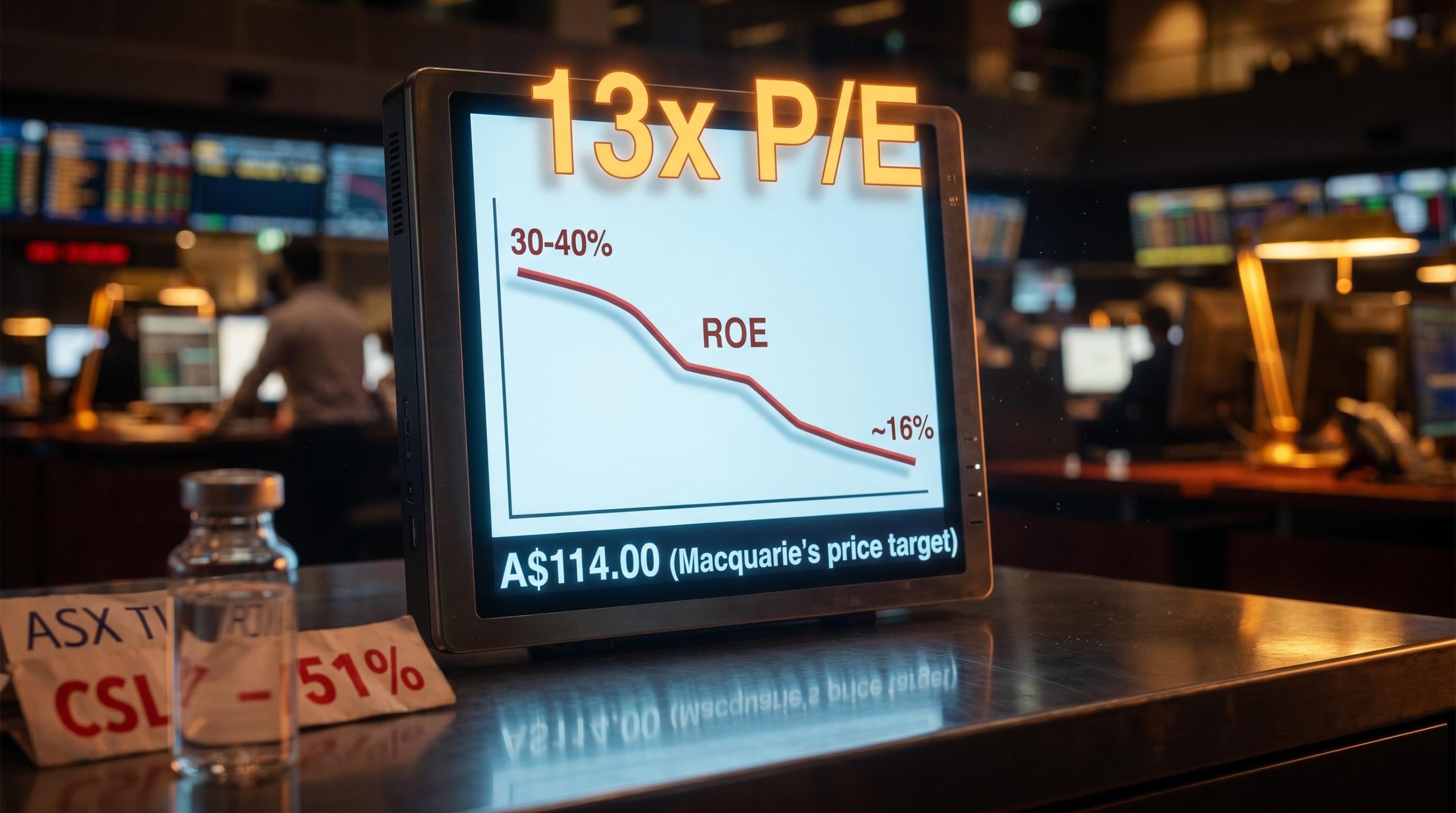

CSL is trading at roughly 13x earnings, a price-to-earnings multiple the stock has not worn since around 2010. It has fallen approximately 51% from where it stood twelve months ago. And yet Macquarie, one of the most closely followed institutional brokers on the ASX, will not call it a buy.

That tension sits at the centre of the current CSL debate. The stock has bounced roughly 23% from its 3 June 2026 low, but even after that recovery it remains approximately 38% below its 200-day moving average. The question is whether this collapse from premium-growth compounder to low-teens earnings multiple represents a genuine buying opportunity, or a fair price for a business whose quality has structurally changed.

Here is the analytical framework for making that call yourself, grounded in what Macquarie’s current numbers actually show: the valuation mechanics behind the derating, the three structural headwinds that drove it, what the forward earnings path looks like, and what a credible recovery would actually require before this stock deserves a higher multiple again.

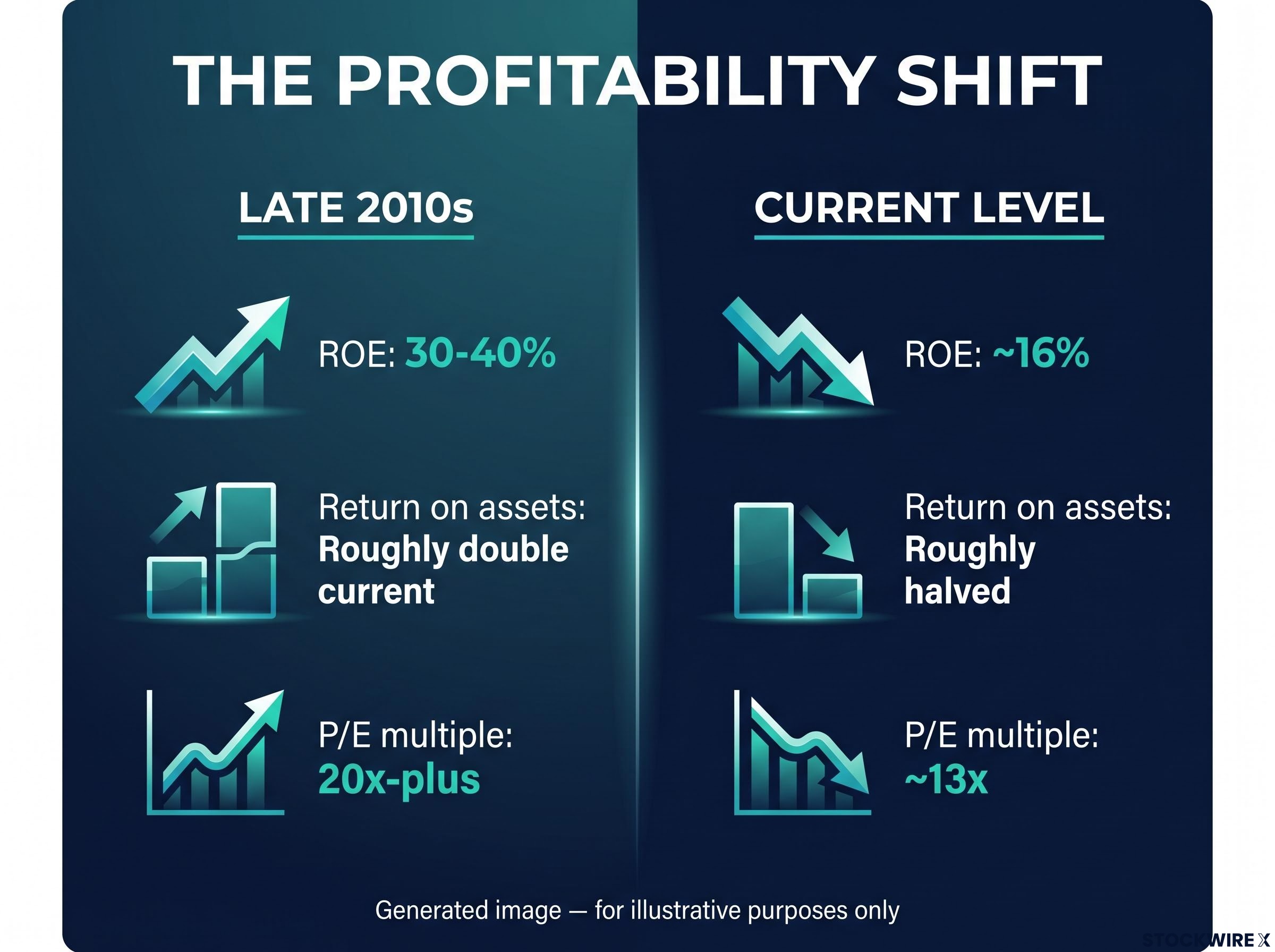

CSL at 13x earnings is not the same company that last traded at this multiple. In 2010, CSL was a simpler, faster-growing plasma business with a return on equity (ROE, the percentage of profit a company generates relative to shareholder capital) in the 30-40% range. That profitability profile justified a premium multiple north of 20x for most of the following decade.

The profitability shift in one number: CSL’s ROE has fallen from 30-40% in the late 2010s to approximately 16% currently, according to Macquarie-sourced data. Return on assets has declined by approximately half over the same period.

Premium multiples are not gifts from the market. They reflect investor confidence that a company will compound returns at an exceptional rate for years to come. When that confidence erodes, the multiple follows.

What happened to CSL is not a sentiment swing. The stock is down 51% over twelve months and sits 38% below its 200-day moving average because the earnings quality and capital efficiency that once justified a 20x-plus valuation have materially deteriorated. Buying at 13x is not automatically buying cheap if the return profile that warranted twice that multiple is genuinely gone.

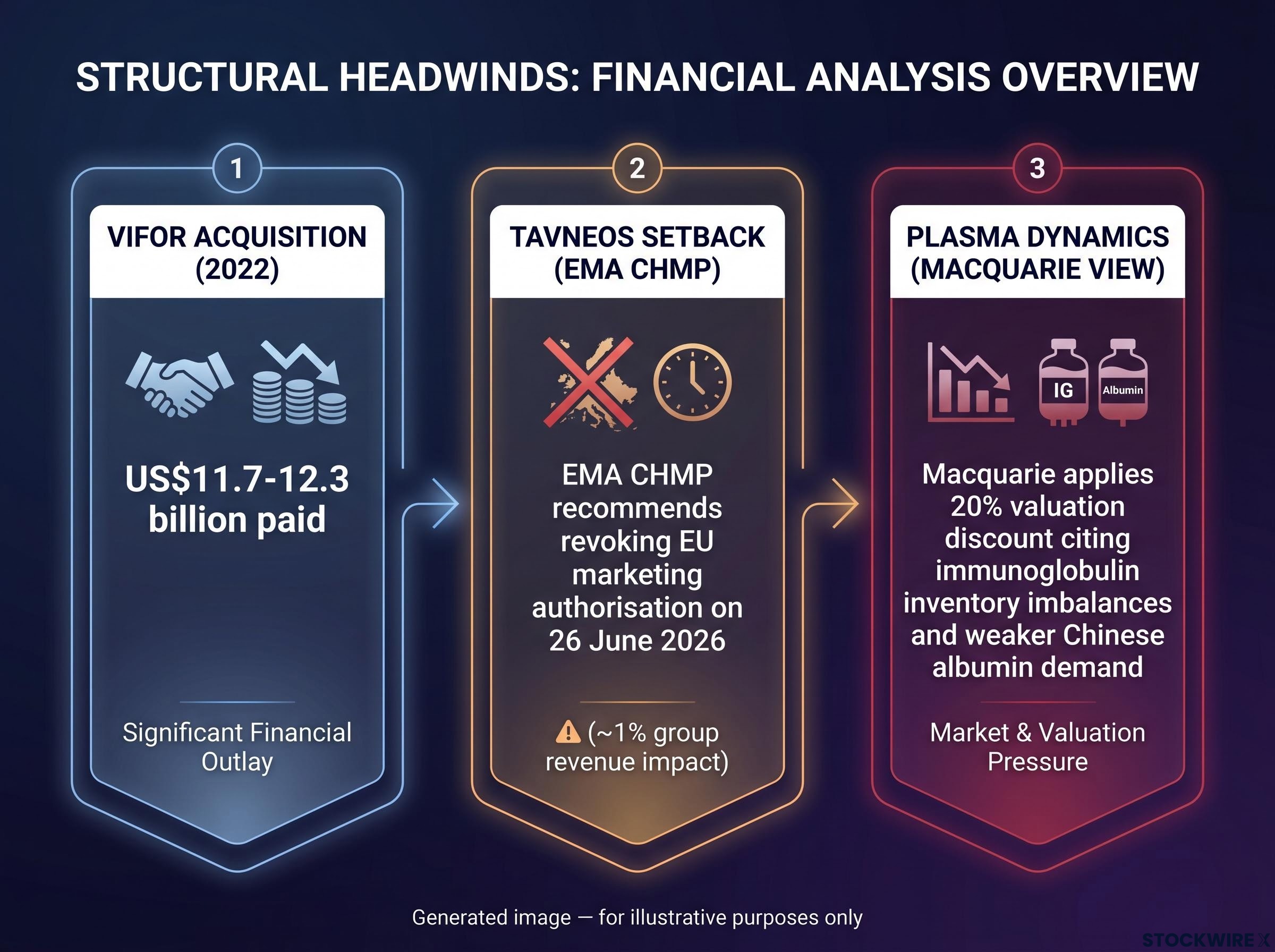

Three problems explain the derating, and they do not operate independently. Each one compounds the damage of the one before it.

Based on Macquarie’s modelling, Tavneos revenue is forecast to drop around 65% from FY27, with that decline feeding through to earnings per share reductions of approximately 3% in FY27 and 4% in FY28.

Macquarie’s position in one number: The broker has applied a 20% valuation discount to CSL, citing inventory imbalances in immunoglobulins, weaker albumin demand from China, and questions around management confidence.

That compounding effect matters. Vifor raised the cost base. Tavneos damaged the strategic story that justified the cost base. And plasma dynamics mean the legacy business cannot paper over the gap. Macquarie’s caution is not excessive conservatism; it is an analytically consistent response to a business facing headwinds on multiple fronts simultaneously.

ROE is the right metric for understanding what has changed at CSL, and understanding why requires more than a textbook definition.

Return on equity measures how effectively management converts shareholder capital into profit. For a capital-intensive, research-and-development-driven healthcare business like CSL, it captures the quality of the entire operation: how well the plasma collection network is monetised, how efficiently acquisitions are integrated, and whether the capital invested in pipelines generates returns that exceed the cost of that capital. When ROE is high and stable, investors pay a premium because they trust the compounding engine. When it falls, the premium falls with it.

Return on equity is the right lens for this analysis because it captures the quality of the entire capital allocation cycle, not just the profit outcome for a single period; a business generating 16% ROE is priced by the market on fundamentally different terms than one generating 30-40%, even if both carry the same ticker.

| Metric | Late 2010s | Current level |

|---|---|---|

| Return on equity | 30-40% | ~16% |

| Return on assets (directional) | Roughly double current | Roughly halved |

| P/E multiple | 20x-plus | ~13x |

The deterioration is driven by the Vifor acquisition raising the capital base faster than earnings have grown. A business generating 30-40% ROE deserves a materially higher multiple than one generating 16%. Investors who anchor to CSL’s historical P/E without accounting for the ROE shift are comparing two fundamentally different businesses that happen to share a ticker code.

A CSL trading at 13x with 16% ROE is priced more like a mature industrial than a healthcare compounder. That is not necessarily wrong. It is the market telling you the compounding engine has downshifted, and you need a specific thesis on when and how ROE recovers before treating current prices as a bargain.

The 23% bounce from the 3 June 2026 low has generated optimism. Macquarie’s earnings forecasts suggest that optimism is running ahead of the fundamentals.

| Year | Net profit / EPS growth (approx.) | Tavneos EPS drag |

|---|---|---|

| FY26 | -4% (net profit decline) | Minimal (pre-revocation baseline) |

| FY27 | +4% adjusted EPS growth | ~3% EPS reduction |

| FY28 | +4% adjusted EPS growth | ~4% EPS reduction |

That trajectory tells you something important. FY26 earnings are expected to fall 4%. The subsequent years deliver roughly 4% adjusted EPS growth each, but that is growth off a lower base, not a return to the acceleration pattern that characterised CSL through most of the 2010s. When you net off the Tavneos drag, the organic improvement is even more modest.

Every P/E ratio encodes an implied growth rate, the minimum forward revenue expansion the market is demanding for an investor to earn a satisfactory return, and at 13x with only 4% adjusted EPS growth on the horizon, CSL’s current multiple implies a growth expectation that the earnings trajectory does not yet support.

The Neutral rating in one number: Following the recent rally, Macquarie’s revised price target of A$114.00 (lifted from A$111.00 on 29 June 2026) leaves very little distance between the target and where the stock currently trades.

A price target that barely clears the current share price after a 23% recovery is Macquarie’s way of telling you the easy gains are already priced in. The harder work of fundamental improvement, meaning a genuine earnings inflection rather than low-single-digit growth, is what the market must now wait for, and the data does not yet confirm it is coming.

The conditions for a credible re-rating are identifiable. They are also interdependent, which is why partial progress on one or two is insufficient.

The next test: CSL’s August 2026 full-year results will include the Tavneos intellectual property impairment disclosure. This is not a potential recovery catalyst; it is a baseline credibility test for how management handles setbacks.

None of these conditions is implausible on its own. Their combination, however, implies a timeline measured in years rather than quarters. Macquarie’s FY27-FY28 adjusted EPS growth of approximately 4% each year is the baseline, not an acceleration, that the market must see delivered before confidence can begin rebuilding.

Cochlear, which Macquarie also holds at Neutral with a price target of A$119.00 (increased from A$115.00 on 29 June 2026), has shed approximately 59.5% of its value over the past twelve months. Premium ASX healthcare multiples have compressed across the board as earnings growth visibility has faded. This is not a CSL-specific punishment; it is a sector-wide repricing of businesses that investors previously treated as defensive growth compounders but which have proved more cyclical than assumed.

The genuine analytical tension is this: at 13x with 16% ROE and no earnings inflection yet visible, CSL is a stock for investors who have a specific, time-bound thesis on when and how ROE recovers. It is not for those who simply believe a lower price must mean better value.

For investors who want a systematic framework for drawing that line, our dedicated guide to value investing covers the specific screening metrics, structural warning signs, and analytical tests that distinguish a genuinely mispriced business from one whose low multiple is arithmetically deserved.

Macquarie’s Neutral stance, modest upside, and a price target that leaves almost no margin above the current share price are intellectually consistent with the available evidence. The recovery case is real. The value-trap risk is equally real. The data does not yet resolve the tension, and investors are better served by acknowledging that uncertainty than by reaching for a conviction the numbers cannot support.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Return on equity (ROE) measures how effectively management converts shareholder capital into profit. CSL's ROE has fallen from 30-40% in the late 2010s to approximately 16% currently, which is the primary reason its price-to-earnings multiple has compressed from above 20x to around 13x.

Macquarie has applied a 20% valuation discount to CSL, citing inventory imbalances in immunoglobulins, weaker albumin demand from China, and questions around management confidence. Its revised price target of A$114.00 leaves almost no upside from current prices, meaning the broker sees the recent 23% rally as having already priced in the easy gains.

The European Medicines Agency recommended revoking Tavneos's EU marketing authorisation on 26 June 2026. While Tavneos contributes only around 1% of group revenue, Macquarie's modelling forecasts a roughly 65% drop in Tavneos revenue from FY27, translating to an EPS drag of approximately 3% in FY27 and 4% in FY28.

A credible re-rating requires ROE sustainably recovering toward 18-20% or above, stabilisation and margin improvement in the Vifor unit, normalisation of plasma and immunoglobulin inventory dynamics, recovery in Chinese albumin demand, and positive pipeline news to replace the Tavneos narrative. Macquarie's analysis implies this is a timeline measured in years, not quarters.

CSL has not traded at a 13x earnings multiple since around 2010, when it was a simpler, faster-growing plasma business earning 30-40% ROE. For most of the following decade, the market priced the stock above 20x. The current multiple reflects a business whose capital efficiency and earnings quality have materially deteriorated, not just a sentiment-driven selloff.