Why Tokyo’s $72bn Yen Defence Keeps Failing

5 mins ago

SpaceX is about to join the Nasdaq-100 on 7 July, and if you own QQQ, you are already buying it whether you decided to or not.

The mechanics behind that automatic purchase, and what they mean for SPCX’s price action over the next week, are widely misunderstood by retail investors. This is not a fundamental event. It is a flow event, arriving in the middle of the hottest US share issuance environment on record, and the distinction matters enormously before anyone considers trading around it.

Here is a clear framework for understanding exactly what index inclusion triggers, what the record IPO environment signals about current market conditions, and where the real risk sits for investors heading into 7 July.

Every fund that tracks the Nasdaq-100 is required by its mandate to purchase SpaceX shares in proportion to the company’s new index weight once the 7 July change takes effect. That includes the Invesco QQQ Trust, the primary vehicle underlying the NDX and one of the most widely held ETFs in the world.

This buying is not discretionary. Passive funds are not making a judgement about SpaceX’s business. They are following index rules.

The non-discretionary nature of this buying is rooted in how passive index mandates are structured: fund managers tracking the Nasdaq-100 are contractually obligated to mirror the index composition, which explains why trillions of dollars now sit in funds that must buy whatever the index dictates.

The core principle: Passive funds are not choosing SpaceX; they are following index rules. If you own a Nasdaq-100 tracker, you will own SpaceX automatically once the rebalance is effective.

The timing follows a well-established sequence:

Any price move in SPCX this week reflects positioning and mandate-driven demand, not a new read on SpaceX’s business prospects. If the stock surges into the inclusion date, that is the sound of forced buying, not a fundamental signal, and you should interpret it accordingly.

A listing this large exposed a gap in the existing index methodology, and Nasdaq closed it in real time. That tells you something about SpaceX’s market weight before you even look at the share price.

Nasdaq introduced a fast-entry framework specifically designed for mega-cap newcomers. Under the old rules, a newly listed company would wait through a traditional seasoning period before becoming eligible for the Nasdaq-100. The revised methodology compresses that timeline to just 15 trading days for companies that qualify.

The Nasdaq-100 fast-entry rule that accelerated SpaceX’s inclusion also creates a structural asymmetry with the S&P 500, which imposes a minimum 12-month seasoning period and simultaneous profitability gates that would independently block most newly listed technology companies regardless of their market capitalisation.

| Criteria | Standard entry | Fast-track entry | Weighting treatment |

|---|---|---|---|

| Eligibility threshold | Annual reconstitution review | Top 40 by market cap | Standard float-adjusted |

| Seasoning period | Multiple months | 15 trading days post-listing | Low-float multiplier applied |

| SpaceX effective date | N/A | 7 July 2026 | 3x multiplier until float reaches 33.3% |

SpaceX debuted on Nasdaq on 12 June 2026 at an approximate valuation of $1.75 trillion, raising roughly $75 billion in one of the largest IPOs ever by proceeds. It cleared the top-40 market-cap threshold on day one.

The low-float weighting multiplier is the mechanical lever most investors will not have heard of, and it is the one that determines the actual size of the passive buying wave.

Here is what it means in plain terms: because only a small portion of SpaceX’s total shares are freely traded (the public float), the index applies a 3x multiplier to the company’s weight until its float reaches 33.3%. The index treats SpaceX as if it has a larger weight than its freely traded shares alone would justify.

That correction exists to avoid under-representing a massive company just because most of its stock is still locked up. But it also concentrates passive demand into a tighter buying window, meaning funds must buy more SpaceX than raw market cap weight alone would require. The price impact becomes harder to predict than a standard index addition because more capital is chasing fewer available shares.

The front-running is not a theory. It is already visible in the data.

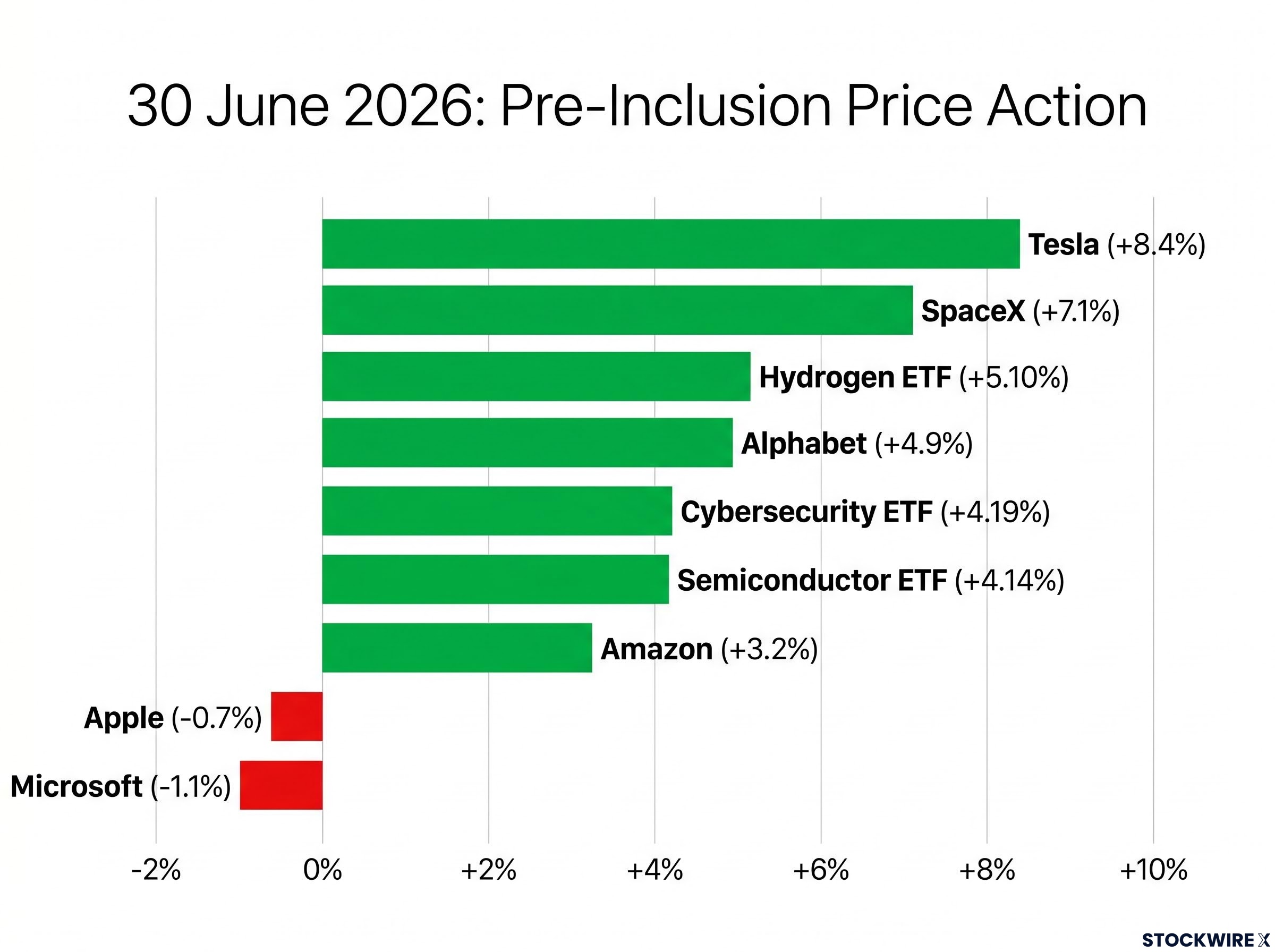

On 30 June 2026, SpaceX gained 7.1% in a single session. That was not a broad market tide lifting everything. Look at who else moved that day, and who did not:

Outperformers:

Underperformers:

Sector ETFs confirmed the selective nature of the rally. The Semiconductor ETF closed the session 4.14% higher, the Cybersecurity ETF added 4.19%, and the Hydrogen ETF was the standout, finishing up 5.10%. But the two largest companies in the index, Apple and Microsoft, declined.

SpaceX’s 7.1% gain against that backdrop is a pre-inclusion positioning signal. Sophisticated traders buy ahead of anticipated passive flows, banking on the knowledge that index funds will be forced buyers after the 6 July close. By the time those funds actually purchase, a significant portion of the expected passive-flow premium may already be priced in.

Index inclusion flow mechanics produced a near-identical pattern in the Honeywell Aerospace spinoff on 29 June 2026, where when-issued shares surged over 9% after hours on confirmation of dual S&P 500 and S&P 100 inclusion, with the spinoff’s constrained float compressing the same forced-buying dynamic into an even tighter window than SpaceX faces.

By the time index funds actually buy, sophisticated traders are often already selling into the flow. The largest price gains from inclusion mechanics may have already occurred, making chasing the stock into the event date a higher-risk proposition.

SpaceX is not entering the Nasdaq-100 in a vacuum. It is arriving in the middle of the most active US share issuance environment ever recorded.

Cumulative US share sales through 30 June 2026 hit a record $251 billion for the first half of the year, eclipsing the previous H1 high set back in 2021. That figure captures IPOs, follow-on offerings, and secondary sales across the market. The scale is historically unusual.

What does record issuance tell you? Three things:

The bullish interpretation of $251 billion in H1 issuance is straightforward: capital markets are open and functioning. The cautionary interpretation is structural.

Heavy issuance periods have historically sometimes been followed by phases where investors become more selective about where they deploy capital. More new stock means more competition for the same pool of investor dollars. When appetite eventually softens, the most recently listed and most richly valued names tend to feel the adjustment first. That is not a prediction. It is a structural consideration worth holding alongside the headline data.

After the mechanics, the price action, and the macro backdrop, here is the reset: none of this changes SpaceX’s business.

Index inclusion improves visibility and can increase liquidity. It does not alter revenue, margins, execution risk, or long-term competitive dynamics. The low-float 3x weighting multiplier is a temporary mechanical adjustment, not a permanent elevation of SpaceX’s index importance.

The well-documented post-inclusion pattern tells a consistent story: pre-announcement rally, heavy end-of-window flow, then mixed post-event behaviour as the marginal buyer shifts back to discretionary investors making fundamental judgements. Once that happens, any gap between SpaceX’s price and its underlying business value becomes the investor’s risk, not the index’s.

Index inclusion boosts visibility, not revenue.

Here are the five practical takeaways before 7 July:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Two threads run through this event. The first is mechanical: forced passive buying concentrated into a narrow window, amplified by a low-float multiplier, in a stock less than a month old as a public company. That thread resolves quickly. By mid-July, the rebalance is done, and the marginal buyer shifts back to investors making discretionary judgements about SpaceX’s earnings power, competitive position, and valuation.

The second thread is structural: record $251 billion in H1 share sales, an IPO pipeline that shows no sign of slowing, and a market environment where both issuers and investors are acting as if favourable conditions will persist. The question worth watching is whether the current megacap tech cycle has durable legs or is borrowing returns from the future.

Treat the 7 July window as a flow event, not a valuation signal. Keep your attention on portfolio construction, diversification, and whether the risk in SpaceX and other megacap tech names is justified by their long-term earnings power. That is the question that will still matter in September; the index mechanics will not.

For investors wanting to understand how lock-up expiry, investor base composition, and expectations gaps shape returns in the months after the index rebalancing window closes, our dedicated guide to IPO post-listing mechanics walks through each structural factor with data on how they interact once forced buying dissipates.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

SpaceX's Nasdaq-100 inclusion takes effect on 7 July 2026, meaning every fund that tracks the index, including the Invesco QQQ Trust, is contractually required to purchase SpaceX shares in proportion to its new index weight. QQQ holders gain automatic SpaceX exposure without taking any action.

Nasdaq introduced a fast-entry framework that compresses the traditional seasoning period to just 15 trading days for companies that rank in the top 40 by market capitalisation. SpaceX debuted on 12 June 2026 at roughly $1.75 trillion and cleared that threshold on day one, making it eligible for the 7 July effective date.

Because only a small portion of SpaceX shares trade freely, Nasdaq applies a 3x multiplier to the company's index weight until its public float reaches 33.3%, treating SpaceX as if it carries greater weight than its freely traded shares alone would justify. This concentrates passive buying demand into a tighter window, making the price impact harder to predict than a standard index addition.

Yes. SpaceX gained 7.1% in a single session on 30 June 2026, outperforming most megacaps while Apple fell 0.7% and Microsoft dropped 1.1%, which is consistent with sophisticated traders front-running the anticipated passive buying wave ahead of the 6 July rebalance execution.

Cumulative US share sales through 30 June 2026 reached a record $251 billion for the first half of the year, surpassing the previous H1 high set in 2021. While this reflects strong risk appetite and open capital markets, it also means more new stock competing for the same pool of investor capital, which can become a headwind if appetite softens.