Is Fiserv at $47 a Value Trap or a Deep-Value Opportunity?

1 hr ago

UBS just moved 20 percentage points out of its AI chip overweight and into defensive infrastructure plays in a single month. That kind of repositioning from one of the world’s largest wealth managers deserves more than a headline.

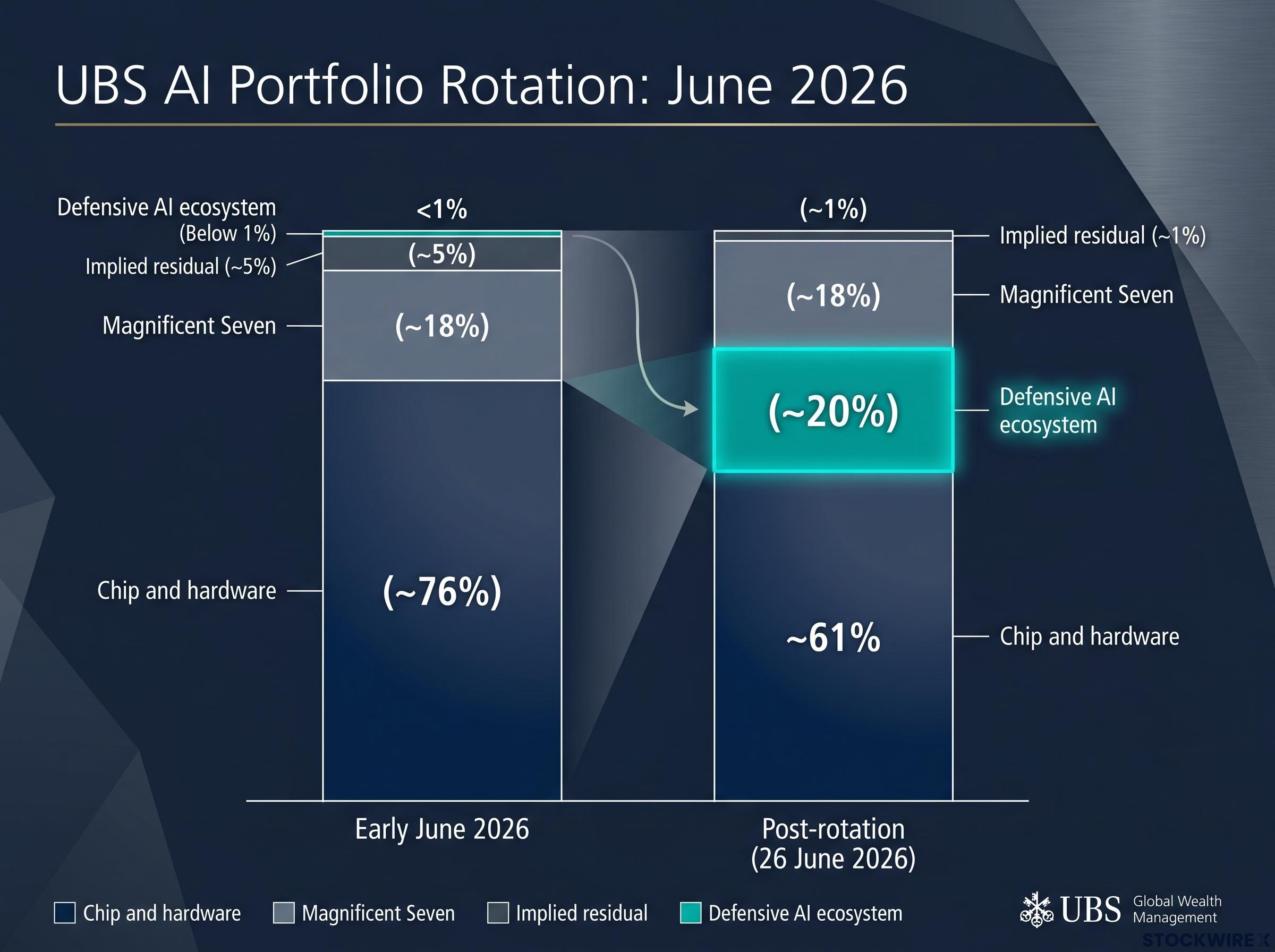

The June 2026 semiconductor rally, led by Micron, handed institutional investors a natural exit point from an extended concentration trade. UBS took it. The shift from below 1% to roughly 20% in defensive AI ecosystem holdings is not a minor trim; it signals a deliberate rethink of how the AI trade should be structured at this stage of the cycle. For investors whose portfolios still reflect the chip-heavy positioning that worked in 2024 and 2025, the logic behind that shift matters more than the move itself.

Here is what UBS actually did, why hyperscaler capital expenditure is the variable driving the most institutional caution right now, and how you can apply the same rebalancing logic to your own AI exposure. The data is specific, the implications are direct, and the framework travels well beyond UBS‘s own book.

Start with the numbers, because the scale speaks for itself.

According to disclosures reported by Investing.com on 26 June 2026, UBS‘s equity strategy team brought its combined semiconductor and hardware weighting down from around 76% to roughly 61% across June, following a period of profit-taking. Separately, the firm’s allocation to more defensive corners of the AI ecosystem climbed from under 1% at the start of the month to close to 20% by late June. The Magnificent Seven combined weight sits at roughly 18%, which UBS is running as a deliberate underweight position relative to the broader index.

The catalyst was specific. The SOXX semiconductor ETF advanced around 10% across June, with Micron‘s results alone responsible for a jump of roughly 4% in a single session. That rally gave UBS the liquidity and momentum to reposition without selling into weakness.

| Portfolio segment | Early June 2026 | Post-rotation (26 June 2026) |

|---|---|---|

| Chip and hardware | ~76% | ~61% |

| Defensive AI ecosystem | Below 1% | ~20% |

| Magnificent Seven (combined) | ~18% | ~18% |

| Implied residual | ~5% | ~1% |

Despite the trim, the position UBS retains still sits roughly 20-25 percentage points above what the Nasdaq 100‘s estimated 42% AI chip and hardware allocation would imply.

That overweight tells you UBS has not abandoned chips. It has repositioned within them while building a defensive layer that barely existed in its portfolio four weeks ago.

The speed of this defensive rotation, from near-zero to 20% in a single month, tells you UBS viewed the Micron rally not as confirmation of the chip trade but as an opportunity to take the other side of it while momentum was still running.

The trim targeted a specific subset of the semiconductor universe. UBS kept its core structural positions intact and channelled profit-taking into smaller and mid-sized names across the AI supply chain, including components and materials businesses in optics, packaging substrates, heat dissipation, advanced interconnect, and analog chips.

What stayed, and what UBS calls “attractive risk-reward,” tells a clearer story than what was sold.

Retained and preferred sub-sectors:

Trimmed and momentum-driven sub-sectors:

The distinction is not subtle. TSMC, Applied Materials, and SK Hynix are picks-and-shovels businesses with long-cycle order visibility and structural roles in AI hardware manufacturing. Their demand is tied to the multi-year buildout of AI capacity across product cycles, not to a single wave of sentiment.

The smaller names UBS trimmed had rallied on proximity to the AI theme rather than on confirmed, durable order books. After a 10% SOXX advance in a single month, those were the positions where the risk-reward had shifted most.

Semiconductor cycle timing adds another dimension to the near-term risk calculus: TSMC’s locked-in 2026 capital budget of $52-56 billion and Samsung’s estimated $70-80 billion annual outlay confirm a 2027-2029 supply wave is already in motion, with the double-hit mechanism (earnings disappointment and multiple compression arriving simultaneously) making late exits structurally costly.

What this distinction tells you is that maturity and structural positioning within semiconductors now matter more than sector-level exposure. Owning TSMC is a fundamentally different risk proposition from owning a small thermal management supplier that tripled on AI enthusiasm. If your portfolio treats all chip exposure as equivalent, UBS‘s differentiation is worth examining.

To understand why UBS rotated into defensive AI plays, you need the framework it is using to think about AI investing. UBS‘s CIO team splits the AI ecosystem into three layers:

UBS‘s message is direct:

Enterprise AI adoption at the infrastructure level is the commercial foundation UBS’s application-layer rotation depends on: only an estimated 12-20% of enterprises currently achieve meaningful operational AI embedding, and agentic AI deployment sits at 17% as of April 2026, leaving a large adoption gap that validates the medium-term case for intelligence and application layer equities even as hardware multiples face compression pressure.

“It is time to diversify beyond the enabling stack and move into the application and intelligence layers where adoption and monetisation are accelerating.”

The “defensive AI ecosystem” plays UBS rotated into span data-centre operators, telecoms, and selected payments businesses. These holdings share a profile of robust balance sheets and reliable dividend payments, giving investors a route into AI themes with less volatility than concentrated chip positions.

UBS‘s Year Ahead 2026 research flagged AI and technology as key equity market drivers while explicitly warning about bubble risk and overinvestment as reasons to diversify. Their Global Family Office Report 2026 found that 65% of family offices are already invested across the AI value chain, including data-centre infrastructure, software platforms, and semiconductor producers, suggesting that sophisticated capital has been broadening its AI exposure for some time.

For investors who have been treating AI as a pure semiconductor story, this framework signals that the institutional playbook has moved on. Staying chip-concentrated is increasingly a choice to underweight the parts of the stack where adoption and monetisation are now accelerating.

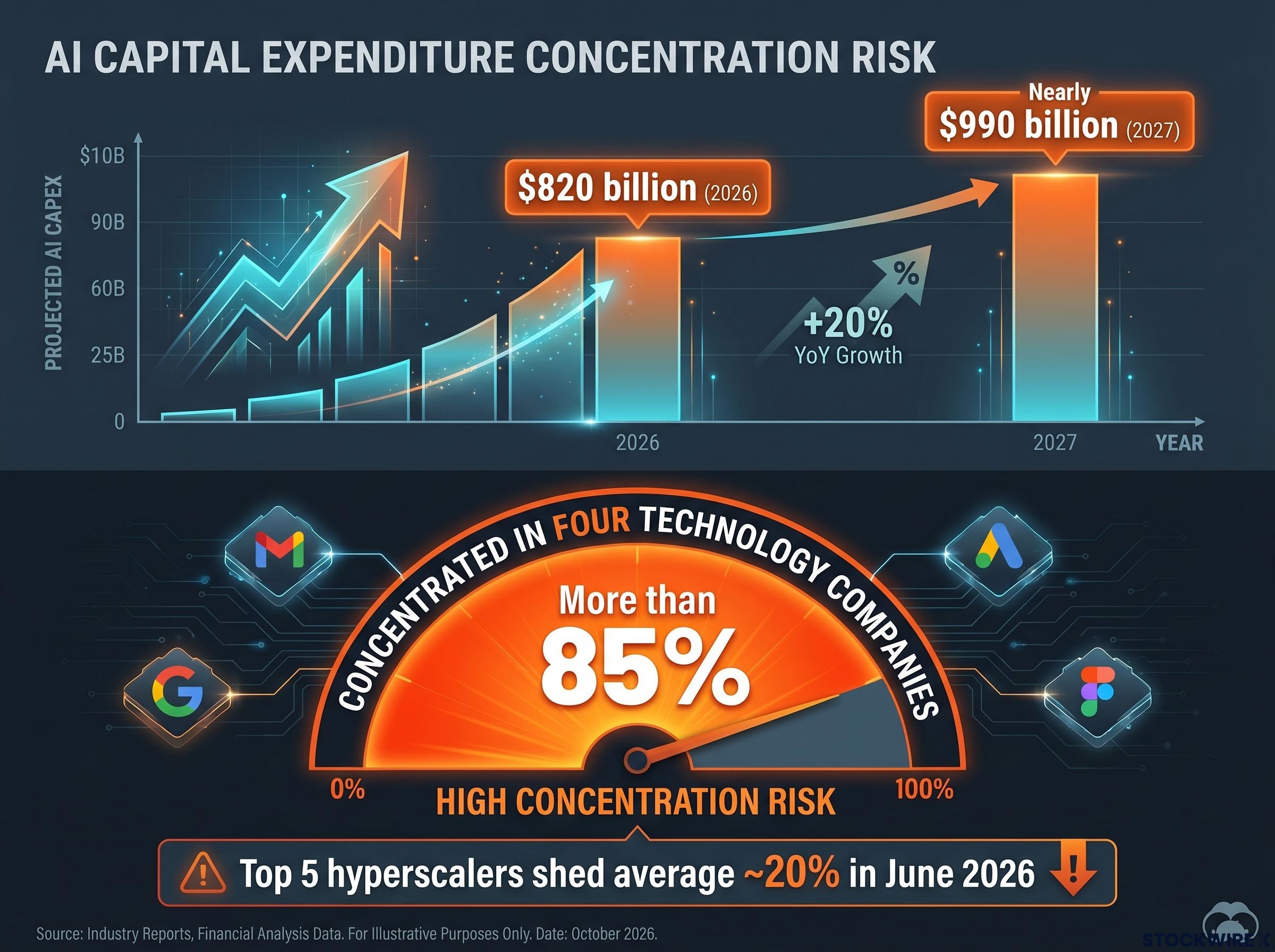

Shares in the top five hyperscalers shed an average of around 20% across June 2026. That is not an abstract macro data point. It is the variable that connects directly to every semiconductor and infrastructure holding in an AI portfolio.

Here is why. Hyperscaler capital expenditure is the funding mechanism for the entire AI hardware buildout. UBS projects AI-related capex will reach $820 billion in 2026, rising to nearly $990 billion in 2027. More than 85% of that spending is driven by four companies.

The hyperscaler capex trajectory heading into mid-2026 is already established in Q1 disclosures: Amazon, Microsoft, Alphabet, and Meta collectively spent $130 billion in Q1 2026 alone, with Microsoft reporting an annualised AI revenue run rate above $37 billion, the commercial justification that has kept boardroom spending commitments intact through the first half of the year.

$820 billion in projected 2026 AI capex, rising to nearly $990 billion in 2027, with more than 85% concentrated in four technology companies.

That concentration creates a fragile transmission mechanism. Sharp falls in hyperscaler share prices create boardroom pressure to revisit the pace and scale of forward spending commitments. A falling stock price does not directly reduce capex budgets, but it changes the boardroom calculus around the pace of investment.

| Hyperscaler action | Downstream impact |

|---|---|

| Reduced or deferred data-centre buildout | Lower GPU and high-bandwidth memory procurement |

| Scaled-back infrastructure projects | Reduced data-centre hardware and cooling orders |

| Slower network expansion | Weaker demand for network infrastructure buildout |

| Re-evaluated AI platform investment | Reduced AI software platform spending |

UBS affirmed that its medium-term outlook for AI investment demand holds firm, with cloud infrastructure expansion and growing agentic AI workloads providing the underlying support. But the near-term vulnerability is clear.

The concentration of more than 85% of projected AI capex in four companies means a single hyperscaler earnings call, a softened guidance phrase, a deferred project, a “re-evaluating our build timeline” comment, can move the entire AI supply chain in hours. If you hold chip and infrastructure names, hyperscaler capex guidance is not background noise. It is your leading indicator.

UBS‘s rebalancing logic is institutional, but the principles are portable. The question it raises for your own allocation is specific: does your AI exposure still match the risk-reward profile at current valuations, or are you carrying the same concentration UBS just reduced?

An investor whose AI allocation is more than 70% chip and hardware exposure is positioned similarly to where UBS was before the June rebalancing.

UBS‘s allocation framework breaks into four components, and each serves a different function:

UBS‘s Year Ahead 2026 guidance was explicit about being “mindful of bubble risks” and the need to diversify beyond megacaps. The June action was a deliberate use of Micron-driven momentum to reposition. The principle generalises: a sharp, sentiment-driven rally is an opportunity to lock in gains and shift toward higher-quality or more defensive AI exposures, not an invitation to chase late momentum.

Cap-weighted index exposure means your AI allocation is more Magnificent Seven-heavy than UBS‘s deliberately managed strategy. Diversifying across the AI value chain, supply chain, infrastructure, applications, reduces the crowding risk inherent in a narrow set of headline names.

UBS‘s overall AI conviction remains intact. The CIO team reportedly expects low-teens percentage upside for the AI theme in 2026, driven by approximately 25% earnings growth from AI-linked companies, though neither figure has been independently verified. The longer-run case for AI demand, built on rising agentic workloads and continued infrastructure scaling, remains broadly unchanged.

What has changed is how that conviction is expressed. It now sits inside a structurally diversified portfolio rather than a concentrated chip bet. Whether this repositioning looks prescient or premature depends on three variables:

BofA’s AI rally warning, published the same week as UBS’s repositioning, identifies AI infrastructure enablers as the highest-risk category, trading at peak multiples on peak earnings expectations simultaneously, a convergence that gives the institutional caution a second, independent data point beyond UBS’s own disclosures.

The strategic tension UBS has made explicit through this rebalancing is the core portfolio decision every AI investor now faces. Staying chip-concentrated is an implicit bet that the hyperscaler capex cycle holds and the rally extends. Following UBS‘s rotation means accepting less upside potential in a continued chip rally in exchange for a more resilient position if capex guidance softens.

The next two hyperscaler earnings seasons will likely determine which side of that trade looks correct. You do not need to predict the outcome. You do need to know which side of the trade your current portfolio is on.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced are subject to market conditions and various risk factors.

The defensive AI ecosystem refers to companies that benefit from AI infrastructure growth but carry less volatility than pure chip plays, including data-centre operators, telecoms, and payments businesses with strong balance sheets and reliable dividends.

UBS used the Micron-driven SOXX rally of approximately 10% in June 2026 as a liquidity opportunity to take profits from momentum-driven chip names and rotate into more defensive AI ecosystem holdings, cutting chip and hardware exposure from roughly 76% to 61%.

Hyperscaler capex is the capital spending by the largest cloud providers on data centres, GPUs, and AI infrastructure; UBS projects this will reach $820 billion in 2026, and because more than 85% is concentrated in four companies, any softening in their spending guidance can move the entire AI supply chain almost immediately.

Investors with more than 70% of their AI allocation in chips and hardware are positioned similarly to where UBS was before its June rebalancing; the framework suggests diversifying across supply-chain picks-and-shovels, infrastructure operators, application-layer software, and defensive AI ecosystem holdings rather than concentrating in a single layer.

UBS divides the AI ecosystem into the enabling layer (chips, hardware, and data-centre infrastructure), the intelligence layer (foundation models, software platforms, and AI development tools), and the application layer (enterprise software, agentic AI, and consumer-facing AI products).