Is Fiserv at $47 a Value Trap or a Deep-Value Opportunity?

8 mins ago

Pfizer is trading near levels it has not seen in years, its forward earnings multiple compressed to around 8x, and at least one board insider has deployed nearly $500,000 of personal capital into the stock at prices close to where it trades today. That combination has drawn real attention from value-oriented investors. It has also attracted some claims that do not hold up.

This piece works through both sides of the signal: what the verified insider data actually shows, where the circulating narrative overstates the evidence, and how the valuation framework holds up when stress-tested against Pfizer’s genuine risk profile. The stock’s decline is not a mystery. The question is whether current pricing already reflects those risks or whether the market has overshot.

Here is a concrete framework for evaluating insider activity as a contrarian indicator, using Pfizer’s current situation as the live case study, including where the data supports the bullish thesis and where it requires more scepticism.

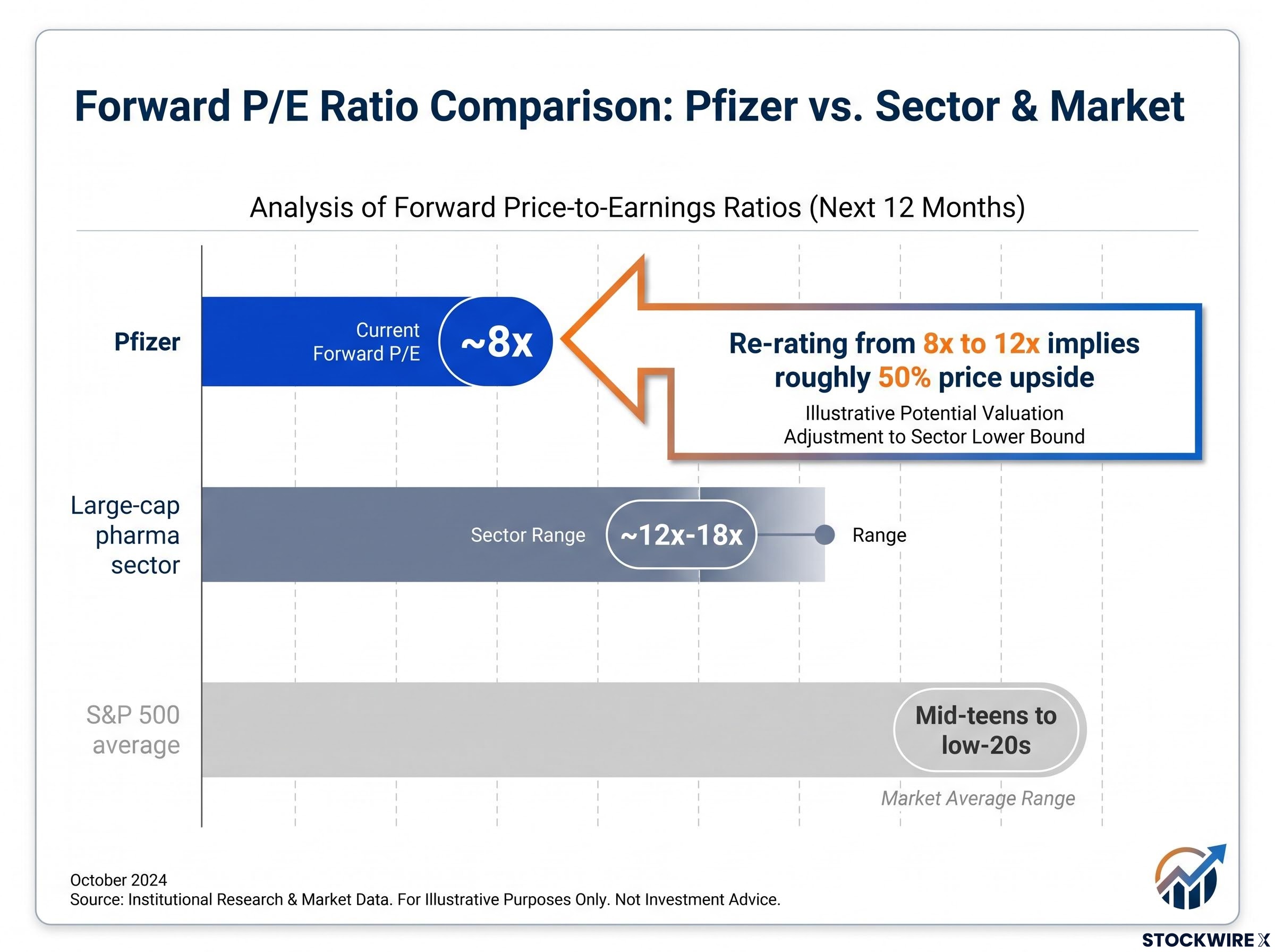

At $24-$25 as of mid-2026, Pfizer trades near multi-year lows. The forward price-to-earnings ratio (P/E), the stock price divided by expected earnings over the next twelve months, sits at approximately 8x. That is deeply compressed relative to almost any reasonable comparison.

| Benchmark | Forward P/E range | Context |

|---|---|---|

| Pfizer | ~8x | Near multi-year lows |

| S&P 500 average | Mid-teens to low-20s | Recent historical range |

| Large-cap pharma sector | ~12x-18x | Across market cycles |

The market has specific concerns embedded in that discount:

The re-rating arithmetic is straightforward. If Pfizer’s forward earnings base is genuinely normalised (meaning COVID distortions have already washed through), a re-rating from 8x to 12x would imply roughly 50% price upside. That is a structural framework, not a forecast. Its entire validity rests on one assumption: that the current earnings denominator is real and sustainable, not still inflated by residual COVID effects. If it is inflated, the true forward multiple is higher than 8x, and the apparent discount is smaller than it looks.

The re-rating arithmetic here relies on three screening metrics working in combination: a compressed forward P/E as the entry signal, free cash flow yield as the earnings-quality check, and debt-to-equity as the balance-sheet risk filter, because any one of them in isolation can produce a misleading picture of whether a stock is genuinely cheap or simply impaired.

That assumption is exactly what the market is debating.

The insider activity picture that has circulated around Pfizer is materially different from what public filings actually confirm. The distinction matters, because investors making allocation decisions on unverified claims are building on a foundation that may not exist.

One transaction stands out clearly in the verified record.

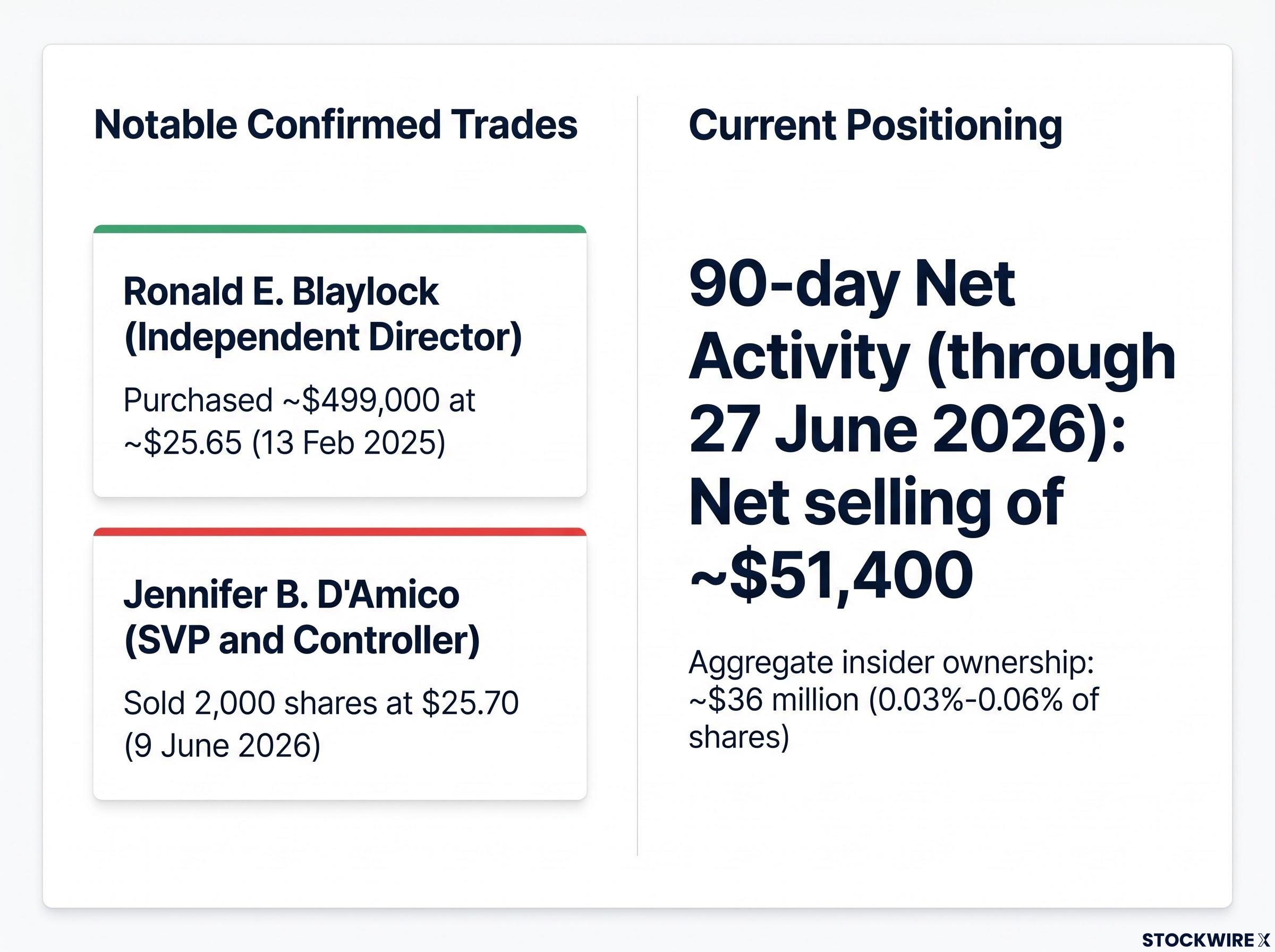

Ronald E. Blaylock, Independent Director, purchased approximately $499,000 of Pfizer shares at roughly $25.65 per share on 13 February 2025. The purchase increased his holding by approximately 150%, bringing his total to 27,707 shares held directly plus 4,750 shares held indirectly through a trust.

That is a legitimate contrarian data point. A board director deploying nearly half a million dollars of personal capital at prices similar to today’s trading range is a meaningful signal of personal conviction.

What the verified data confirms:

What is not confirmed by public Form 4 filings:

Form 4 filings, cross-referenced across Insider Screener, Yahoo Finance, SECForm4, and Simply Wall St, do not support the broader insider buying narrative that some platforms have circulated. If additional transactions exist that aggregators have not yet captured, they would need independent verification against EDGAR filings before being treated as fact.

The Blaylock purchase is worth taking seriously. But working from a single director-level data point is fundamentally different from working with the clustered high-conviction buying pattern that generates the strongest insider signals.

Insider purchases are not all created equal. The academic and practitioner literature on insider trading signals identifies four variables that determine whether a purchase is genuinely informative or just noise. Applying those variables to Pfizer’s verified record shows where the signal is strong and where it falls short.

The academic research on insider trading signals consistently identifies clustering, executive seniority, and transaction size as the variables that most reliably distinguish informative purchases from noise, a framework that maps directly onto the four-criterion analysis applied to the Blaylock transaction here.

Three of four primary criteria are met. The absence of a buying cluster among operating executives is a meaningful gap that weakens the overall conviction picture. One director buying, however large the transaction, is not the same signal as the CFO, General Counsel, and multiple directors all buying within a 30-day window.

The fifth variable is purchase size relative to the buyer’s estimated compensation. At approximately $499,000, Blaylock’s purchase is large enough in absolute terms to represent a material personal commitment for most individuals, regardless of director-level compensation. While exact compensation figures for board directors are not always public, the dollar size places this well above token or symbolic buying.

Aggregate insider ownership across Pfizer totals approximately $36 million, representing roughly 0.03%-0.06% of shares outstanding. That is moderate alignment, not exceptional. It provides some skin-in-the-game comfort but falls well short of the kind of concentrated insider ownership that characterises founder-led businesses.

A stock trading at a sub-10x forward P/E with a $24-$25 price tag and a large-cap pharma profile is exactly the kind of situation that attracts Graham-and-Dodd-style value investors. Historical 13F filings, the quarterly disclosures that institutional managers with over $100 million in assets are required to file, have shown value-oriented interest in Pfizer, including references to option positions in prior quarters.

What those filings cannot tell you is what those investors are doing today.

How 13F filings work: Institutional investors file 13F disclosures 45 days after each quarter ends. That means the most recent public data is always at least several weeks stale by the time you see it. A position reported in a Q1 filing could have been modified or exited entirely before the disclosure date.

Any claim of current institutional accumulation by a named investor must be tied to a specific, dated 13F filing, and should note whether subsequent filings show the position was maintained. Implying that a well-known investor is accumulating at today’s prices, without referencing a specific recent filing, is not something the available data supports.

For readers wanting to verify institutional positions independently, WhaleWisdom, 13F.info, and related aggregators are the appropriate primary sources. The institutional interest dimension adds useful context for understanding the investor base forming around these price levels, but it should sharpen your due diligence instincts, not substitute for them.

A stock can look cheap on paper and stay cheap for years, or decline further, if the conditions driving the discount are structural rather than temporary. Here are the four specific conditions under which Pfizer’s 8x forward P/E would represent a value trap rather than genuine undervaluation:

The four conditions listed above map directly onto the value trap risks that practitioners have documented across decades of large-cap underperformance: a business that looks cheap on a forward multiple but faces structural rather than cyclical earnings impairment will stay cheap, or cheapen further, regardless of how compressed its P/E appears.

The pharmaceutical tariff structure introduced under Section 232 adds a compounding layer to this uncertainty, with a tiered rate schedule that carries a 100% default rate for non-qualifying companies and a formal reassessment of generic drug exemptions projected around April 2027, creating a policy timeline that runs parallel to the period when Pfizer’s normalised earnings base is most in question.

The central analytical uncertainty runs through all four conditions: distinguishing temporary COVID normalisation from permanent structural earnings impairment. That distinction is what determines whether the 8x denominator is real or inflated, and it is genuinely uncertain even for sophisticated analysts.

Value realisation in large-cap pharma turnarounds typically plays out over multiple years, not quarters. Investors entering with a short time horizon are exposed to mark-to-market losses even if the long-term thesis ultimately proves correct.

Insider buying does not establish a price floor. Insiders have been wrong before, and a stock can decline further even when a long-term value thesis is eventually validated. The time horizon you are actually working with is as important as the analytical framework you apply.

The verified record is enough to make Pfizer a stock worth serious analytical attention. Whether it is enough to constitute a buy signal depends on judgements only you can make.

| What the verified record supports | What requires independent verification |

|---|---|

| Stock trading at historically compressed multiples (~8x forward P/E) | Clustered C-suite buying among operating executives (not confirmed by public Form 4 filings) |

| One confirmed large director-level insider purchase ($499,000, February 2025, near current prices) | Current institutional accumulation by named value investors (requires specific dated 13F reference) |

| Structurally coherent re-rating thesis (8x to 12x, ~50% implied upside, conditional on stable normalised earnings) | Whether the normalised earnings base is genuinely sustainable or still COVID-elevated |

| Well-documented risk profile with specific failure conditions identified | Seagen integration progress and pipeline execution trajectory |

Before treating Pfizer’s current valuation as an actionable signal, you should be able to answer four questions with specificity: Is the earnings base genuinely normalised? Is Seagen integration on track? Has the drug-pricing risk been priced in or not? And what time horizon are you actually working with?

The Blaylock purchase tells you that at least one informed insider was willing to deploy meaningful personal capital at roughly today’s prices. The verified data does not tell you that the C-suite agrees. That gap is where your own analysis begins.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Insider buying occurs when a company director or executive purchases shares on the open market using personal capital, signalling personal conviction that the stock is undervalued. For Pfizer, the most significant confirmed transaction is Independent Director Ronald E. Blaylock's $499,000 open-market purchase at $25.65 per share in February 2025, near current trading prices.

No. Public Form 4 filings cross-referenced across multiple sources do not confirm any recent open-market purchases by Pfizer's CFO, Chief Administrative Officer, or Chief Legal Officer. The only verified large insider purchase in the record is the $499,000 buy by Independent Director Ronald E. Blaylock in February 2025.

Pfizer's compressed ~8x forward P/E reflects four specific concerns priced in by the market: a sharp decline in Paxlovid and Comirnaty revenues from peak COVID levels, balance sheet leverage from the Seagen acquisition, pipeline execution uncertainty, and drug-pricing headwinds from the Inflation Reduction Act's Medicare negotiation provisions.

A re-rating from 8x to 12x forward P/E would imply roughly 50% price upside, but only if the current earnings denominator is genuinely normalised. If COVID-era revenues have not yet fully washed through the earnings base, the true forward multiple is higher than 8x and the apparent discount is smaller than it looks.

The four variables that determine signal strength are: seniority and information access, open-market purchase type (rather than option exercises or 10b5-1 plan sales), clustering of multiple insiders buying within a tight time window, and the purchase price relative to the stock's historical range. Pfizer's verified record satisfies three of the four criteria but lacks the clustering of multiple operating executives that generates the strongest insider signals.