Is Fiserv at $47 a Value Trap or a Deep-Value Opportunity?

3 hrs ago

Netflix posted revenue of approximately $12.25 billion in Q1 2026, growing 16% year-over-year. Diluted earnings per share came in at $1.23, above consensus. Operating margins sit above 30%, with guidance pointing higher still.

Shares have shed more than 40% of their value from the company’s all-time peak.

That gap between a business compounding earnings at double-digit rates and a share price that has nearly halved since June 2025 is not a reporting lag or a market glitch. It reflects a fundamental repricing of what Netflix is worth, driven by four distinct forces operating simultaneously: growth deceleration, a founder’s departure, a failed mega-acquisition that revealed management’s risk appetite, and a macro rotation away from steady compounders toward AI-linked names. Some of those forces are grounded in genuine business reality. Others are sentiment artefacts that have historically reversed.

Here is what the data actually tells you about each driver, which ones are durable, and which ones the market is likely overweighting at today’s price.

Start with the numbers, because they frame the right question.

| Metric | Q1 2026 Result |

|---|---|

| Revenue | ~$12.25 billion |

| Revenue growth (YoY) | ~16% |

| Diluted EPS | $1.23 (above consensus) |

| Operating margin | >30% (Q2 guidance ~32.6%) |

| Stock decline from peak | ~45% from June 2025 high of ~$134 |

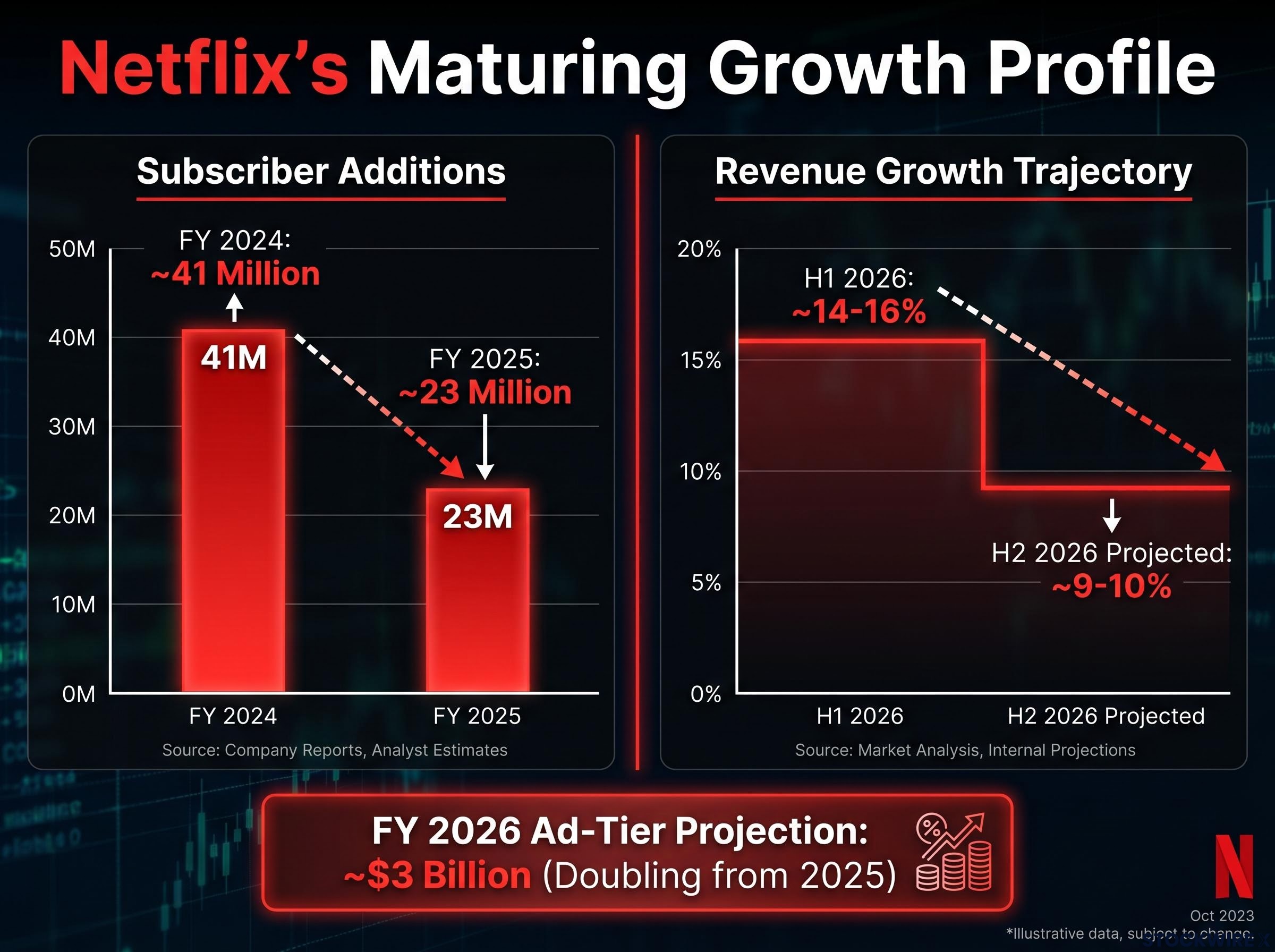

Netflix hit an all-time high near $134 in June 2025. As of late June 2026, the stock trades in the low $70s, a drawdown of roughly 45%. Operating income grew approximately 18% year-over-year in the most recently reported quarter. Management’s full-year 2026 revenue growth guidance is approximately 11-13% on a currency-neutral basis, rising to around 12-14% once favourable exchange rate tailwinds are included.

The question is not whether earnings are falling. They are not. The question is why investors are now less willing to pay a premium for those earnings, and whether that repricing reflects a permanent shift in what this business is worth or a temporary overshoot driven by sentiment. That distinction is the entire analytical task.

The mechanics of growth deceleration repricing are not unique to Netflix; Zscaler shed approximately 30% in a similar episode where every reported metric beat guidance yet forward ARR growth guided sharply lower, illustrating how markets price the trajectory of growth rather than any single quarter’s result.

When a company’s expected growth rate drops from 15-20% or higher into the high single digits or low double digits, the market does not simply shave a few points off the share price. It compresses the valuation multiple, the amount investors are willing to pay per dollar of earnings. That compression can be severe even when current results look strong, because the multiple reflects expectations about years of future compounding, not last quarter’s print.

Netflix is living through exactly that transition. Revenue growth is still coming from three sources:

The composition matters. Subscriber growth, the engine that powered the premium multiple, is decelerating. Price increases and advertising monetisation are partially offsetting the slowdown, but they carry lower growth ceilings and signal a more mature business profile.

The number making investors uncomfortable is not the Q1 headline. It is what comes next.

With growth running at roughly 14-16% in the opening six months of 2026, full-year guidance pointing to around 12% implies a marked step-down in the back half of the year, with second-half 2026 expansion potentially settling somewhere in the 9-10% range.

If that trajectory holds, Netflix is no longer a premium growth compounder. It is a mature, highly profitable media business growing at roughly the rate of the broader market. That is not a bad business. But it is a different category, and different categories carry different multiples. The lower price is not irrational pessimism; it is the market recalibrating the multiple to match the growth profile. The question for you is whether today’s price has already captured that downshift, or overshot it.

Reed Hastings, Netflix’s co-founder and board chair, announced during the April 2026 earnings release that he will not stand for re-election when his current term expires at the June 2026 annual meeting.

The market reaction to that earnings report was driven less by the quarter itself, which beat expectations, and more by the combination of softer forward guidance and the surprise of the departure. Hastings is specifically associated with three strategic pivots that built the company investors own today:

Each of those decisions required a willingness to sacrifice short-term comfort for long-term strategic positioning. That is what the market fears losing, not a name on a letterhead, but a decision-making framework that has historically favoured bold bets over incremental optimisation.

Nothing in the current financials demonstrates deterioration attributable to this change. It is a governance and culture concern, not an operational one. The market is rationally pricing some extra uncertainty until the post-Hastings leadership team is tested by several major strategic decisions. Historically, founder departures from high-profile growth companies carry an uncertainty premium that fades as new management accumulates a track record over subsequent quarters.

Markets typically assign a founder succession premium to the uncertainty period between departure and demonstrated continuity, a dynamic playing out in real time at Berkshire Hathaway, where Greg Abel’s first quarters as CEO are being watched for evidence that the capital allocation discipline built under Buffett will hold.

What this tells you is that the Hastings risk is real but time-bound. It raises a specific question, whether the next leadership team will show the same strategic ambition, and that question will be answered by observable decisions over the next year or two, not by headlines this week.

In December 2025, Netflix pursued a potential acquisition of Warner Bros. Discovery at an enterprise value of approximately $82.7 billion. The deal was not completed; Warner Bros. Discovery was ultimately taken by Paramount. No disastrous acquisition closed. But the episode changed how sophisticated investors think about Netflix’s capital allocation, and that change has not fully reversed.

Two specific moves alarmed the market. First, Netflix paused its share buyback programme to preserve cash during the pursuit, signalling that management was willing to redirect capital from shareholder returns toward deal-making. Second, had the acquisition closed, the resulting leverage would have been substantial.

Analysts estimated the combined entity would have approached approximately 4x net debt to EBITDA, a ratio that would have placed significant strain on the balance sheet and left the business with far less room to manoeuvre through any economic downturn.

The deal not closing resolved the immediate threat. It did not resolve the underlying concern: that management now has a demonstrated appetite for transformative, heavily leveraged acquisitions. Market commentary has pointed to Lionsgate as a name that could surface in future deal speculation, which keeps capital allocation concerns active among investors.

Netflix walking away from the Warner Bros. Discovery deal after Warner’s board accepted a rival bid resolved the immediate capital risk but left a lasting imprint on how the market assesses management’s acquisition ambitions, with the $83 billion enterprise value of the original pursuit now serving as a reference point for any future deal speculation.

This is the most durable of the non-fundamental concerns. Capital allocation decisions compound over years and directly determine whether free cash flow gets returned to shareholders or consumed by integration costs. The market is not pricing the WBD outcome specifically; it is pricing the capital allocation framework the pursuit revealed. For you, the distinction matters: this risk factor is not resolved by the deal falling through. It remains a live input to valuation until management demonstrates a sustained period of disciplined capital return.

The share price decline at Netflix has not unfolded in a vacuum. It has tracked a wider institutional shift in which capital has moved away from businesses with dependable free cash flow generation and into names tied to AI development and enabling infrastructure, a trend that gathered pace through late 2025 and carried into 2026.

This is a portfolio allocation shift, not evidence that AI competitors have eroded Netflix’s streaming competitive position. Netflix has not lost its core competitive advantages. It still commands the largest global subscriber base, the deepest content library, and the most sophisticated recommendation engine in streaming. The rotation is about where institutional capital is flowing, not about what has changed inside the business.

Institutional capital flows in 2026 have moved decisively away from AI and mega-cap technology toward energy, industrials, and defensive sectors, with energy gaining more than 22% year-to-date against a broad market return of under 1%, a divergence that contextualises why quality compounders like Netflix face pricing headwinds that have little to do with their underlying business performance.

The effect is real, though. When large institutions reduce their allocations to a name, marginal demand drops, and price declines triggered by company-specific concerns get amplified beyond what the fundamental picture alone would justify. The rotation makes every other negative catalyst land harder.

These allocation shifts tend to feel entrenched while they are underway, yet over subsequent quarters they have often partially unwound as the favoured theme’s valuations become stretched and institutions begin looking for re-entry points in quality businesses that have been de-rated. For you, sector rotation is the least actionable of the four catalysts, precisely because it is the one most disconnected from Netflix’s actual business quality. But it is also the one that can move prices most dramatically in the short term, which is why it warrants being named and correctly weighted rather than dismissed.

Four catalysts. Two categories.

Fundamental and durable:

Sentiment-driven and more likely temporary:

The magnitude question is where the analysis sharpens. A 40-45% drawdown from a business still posting double-digit revenue growth, operating margins above 30%, and ad-tier revenue doubling toward approximately $3 billion in 2026 is on the larger end of what the fundamental picture alone would justify. The sentiment-driven factors account for a meaningful portion of the gap between the business reality and the current price.

The key variable that will determine whether this repricing proves rational or excessive is where the annual revenue growth rate settles: holding in the low double digits would tell a very different story from a sustained drift into high single digit territory over the coming two to three quarters.

Two scenarios follow from that variable. If growth stabilises in the low double digits, the current lower multiple may represent a fair new baseline, and the drawdown partially reflects a dislocation between intrinsic value and sentiment. If growth drifts into sustained high-single-digit territory, further multiple compression could follow, and today’s repricing may prove justified or even insufficient.

This is not a prediction. It is a framework. Tracking reported revenue growth across the next several quarters is the observable discipline that will answer the question, independent of any narrative around departing founders or abandoned deals.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The sell-off is not purely irrational. Growth deceleration and capital allocation risk are real, and both justify a lower multiple than Netflix carried at its June 2025 peak. But a 45% drawdown from a business still compounding earnings at double-digit rates, with margins above 30% and a rapidly scaling advertising business, has likely overshot what the fundamentals alone warrant. Sentiment factors, the Hastings departure and the AI rotation, account for a meaningful share of the gap.

The market has de-rated Netflix to a more mature business. The next several quarters of revenue growth data will either validate that re-rating or reveal it as excessive. That is where the burden of proof now sits: not on the headlines, but on the growth rate.

Sentiment-driven declines and fundamental deterioration look identical in the moment. They have very different trajectories. The discipline to separate them, using observable data rather than narrative, is what distinguishes analysis from reaction. Keep your focus on the reported growth figures, because those numbers carry the signal the headlines cannot.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Netflix shares have fallen roughly 45% from their June 2025 peak due to four simultaneous pressures: decelerating subscriber growth, co-founder Reed Hastings departing the board, the failed Warner Bros. Discovery acquisition attempt that revealed management's appetite for heavily leveraged deals, and a broader institutional rotation away from steady compounders toward AI-linked names.

Growth deceleration occurs when a company's expected revenue expansion rate drops significantly, such as from 15-20% into high single digits, which causes investors to pay less per dollar of earnings because the compounding runway looks shorter. For Netflix, subscriber additions fell from roughly 41 million in 2024 to approximately 23 million in 2025, and full-year 2026 guidance implies second-half growth could settle near 9-10%, pushing the market to reclassify the business as a mature compounder rather than a premium growth stock.

Netflix pursued Warner Bros. Discovery at an enterprise value of approximately $82.7 billion in December 2025, pausing its share buyback programme in the process; analysts estimated the combined entity would have carried roughly 4x net debt to EBITDA. Even though the deal did not close, it demonstrated management's willingness to pursue large, leveraged acquisitions, a capital allocation concern that remains a live valuation input for investors.

Hastings was the architect behind Netflix's three most consequential strategic pivots: the move to streaming, the shift to original content, and international expansion. His departure raises uncertainty about whether the next leadership team will show the same strategic ambition, but the concern is a governance and culture risk rather than an operational one, and it typically fades as new management accumulates a track record over several quarters.

The article identifies the key variable as where annual revenue growth settles over the next two to three quarters: growth stabilising in the low double digits would suggest the drawdown has overshot fundamentals, while a sustained drift into high-single-digit territory would justify further multiple compression and validate the repricing.