Where BofA Says European Equity Risk Is Most Concentrated

3 hrs ago

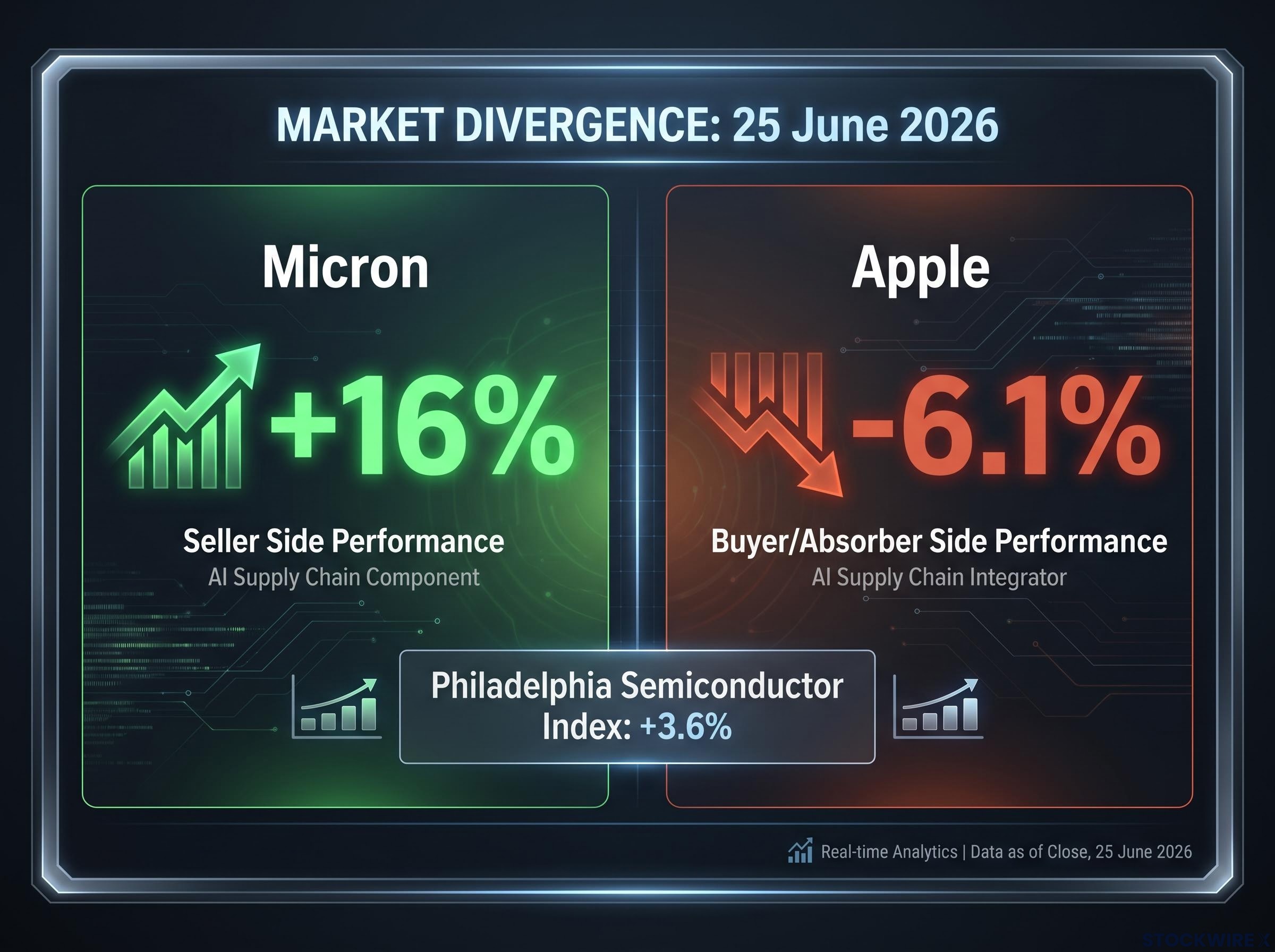

Micron surged 16% on 25 June 2026. Apple fell 6.1% on the same day. The Philadelphia Semiconductor Index climbed 3.6% while the Nasdaq Composite headed for its worst week in months.

Technology did not move as one sector on Thursday. It moved as two, and the split tells you something specific about where AI capital is actually flowing through the supply chain right now, and which companies are collecting it versus which ones are paying for it.

Here is the framework for determining which side of that divide your current tech holdings sit on, and whether the macro backdrop is accelerating or cushioning the pressure.

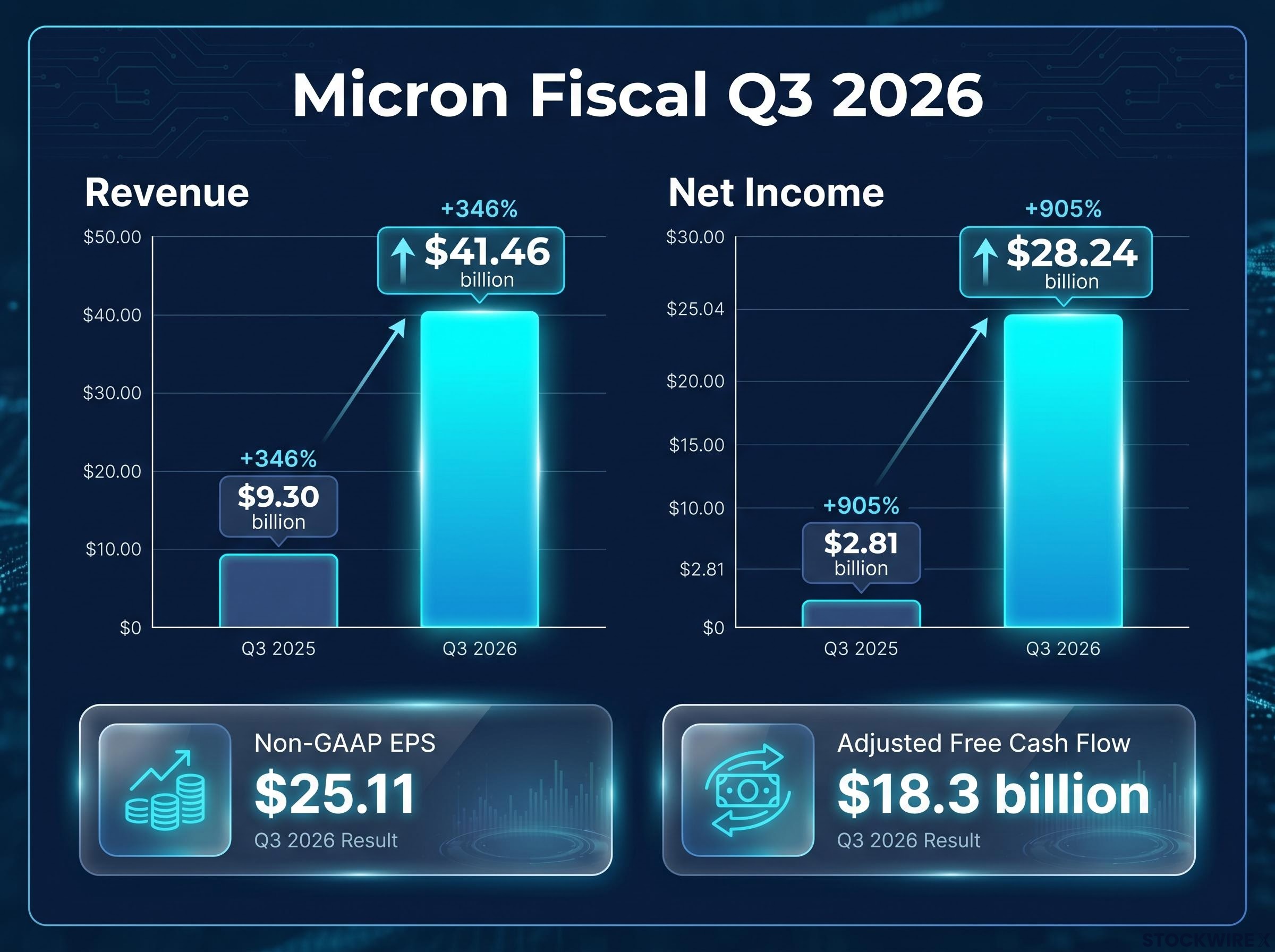

Micron Technology’s (NASDAQ: MU) fiscal Q3 2026 results were not a beat. They were a structural signal.

Management explicitly attributed the surge to “heightened demand associated with the artificial intelligence surge,” with data-centre and cloud memory revenues delivering multi-hundred-percent growth year over year.

The scale in context: Micron reported $41.46 billion in quarterly revenue, up from $9.30 billion a year earlier. Net income grew from $2.81 billion to $28.24 billion over the same period.

Revenue quadrupling in a single year at a capital-intensive chipmaker is not a cyclical bounce. It is direct evidence that AI infrastructure buyers are routing enormous capital through memory and semiconductor suppliers right now. The flow has a specific direction, and it matters for how you position within tech.

The AI investment boom has driven US IT spending to 4.9% of GDP in Q1 2026, surpassing both the dot-com era peak and the cloud buildout cycle, with rewards concentrated in the infrastructure and energy layer rather than in application software where monetisation remains contested.

The stock’s 16% single-session gain on 25 June was the market confirming what the income statement already said. The Philadelphia Semiconductor Index’s 3.6% advance on the same day shows the market moved the entire sub-sector, not just one name.

The split inside technology is a supply chain story. AI model training and inference at scale require massive deployments of DRAM, NAND, and specialised logic chips. DRAM is dynamic random-access memory, the short-term working memory that processors rely on; NAND is flash storage, the longer-term memory that holds data. These are the physical components that make AI infrastructure run, and only a handful of companies manufacture them at scale.

Memory prices have soared over the past couple of years, largely because AI chip deployment is consuming all available production capacity from a limited supplier base. That is a seller’s market, and it flows directly into chipmaker margins. Micron’s results are the clearest proof.

The AI chip supply chain concentrates control across just four companies, with Nvidia, TSMC, ASML, and Broadcom each occupying a distinct and non-interchangeable layer, a structure that explains why capital flowing into AI infrastructure lands so heavily on a narrow supplier base.

For software and consumer-facing companies, the economics run in the opposite direction. Hyperscalers ramping AI capex channel that spending primarily to semiconductor and accelerator vendors. SaaS and consumer internet companies integrating AI features pay more for cloud services without yet seeing revenue step-functions that match what semiconductor vendors are capturing.

The diagnostic question you can apply to any tech holding is straightforward: is this company selling into the AI buildout, or paying for it? The answer determines whether AI is a tailwind or a headwind on that company’s income statement.

| Company Type | Supply Chain Position | AI Revenue Impact | AI Cost Impact |

|---|---|---|---|

| Memory/semiconductor makers (e.g., Micron, SK Hynix) | Sellers of AI infrastructure components | Multi-hundred-percent data-centre revenue growth | Capex rises, but funded by strong cash generation |

| Device OEMs (e.g., Apple) | Buyers of memory and components | Minimal direct AI revenue uplift | Higher component costs compress margins or force price increases |

| Software/platform companies | Buyers of cloud and compute infrastructure | AI monetisation still early-stage | Higher cloud and infrastructure bills arrive before revenue |

Apple Inc (NASDAQ: AAPL) dropped 6.1% on Thursday 25 June 2026, after the company lifted prices across its iPad and MacBook ranges to absorb higher memory component costs driven by AI-related demand, according to Investing.com reporting.

The structural logic is clean. Apple sources DRAM and NAND from a concentrated supplier base, primarily Micron, Samsung, and SK Hynix, with limited substitution options. When AI-driven capacity constraints push memory prices higher, Apple faces two options, and neither is attractive:

Both paths carry risk. Both paths reduce the stock’s near-term appeal relative to the chipmakers sitting on the other side of the same transaction.

What Micron captured on 25 June, Apple absorbed. A 16% gain for the memory supplier, a 6.1% decline for the device maker, on the same trading day, from the same underlying dynamic: the price of AI infrastructure.

This is not a one-quarter anomaly. As long as AI deployment keeps consuming available memory capacity, the seller’s market persists, and OEM margins remain under pressure.

The memory chip price forecast through 2028, confirmed by S&P Global Ratings in June 2026, shows memory now accounting for approximately 35% of laptop bill-of-materials costs, up from 15-18% previously, which quantifies precisely the cost pressure Apple and other OEMs are navigating when they raise device prices.

The macro backdrop is not creating a separate headwind. It is amplifying the same divergence.

According to data reported around 25-26 June 2026, the U.S. consumer price index topped the 4% mark for the first time in roughly three years. The CME FedWatch Tool indicated that traders had priced in 64% odds of a 25-basis-point rate rise at the September meeting, as of the reporting date.

Higher rates compress the present value of distant cash flows, which hits long-duration, high price-to-earnings growth names hardest. A price-to-earnings ratio (P/E ratio) measures how much investors pay per dollar of a company’s earnings; the higher it is, the more the stock’s valuation depends on future earnings rather than current ones. That category describes much of large-cap software and consumer tech.

Micron’s current earnings momentum provides a meaningful buffer against that pressure. When a company generates $18.3 billion in free cash flow in a single quarter and reports revenue growth of 4x year over year, its valuation depends far less on distant cash flow projections. The earnings support is here, not five years from now.

The weekly index data shows the macro sort already underway:

| Index | Weekly Return (approx.) | Primary Driver |

|---|---|---|

| Nasdaq Composite | -4.4% | Growth tech sell-off on rate sensitivity and AI cost concerns |

| S&P 500 | -1.9% | Broad tech drag partially offset by defensive sector strength |

| Dow Jones Industrial Average | +0.7% | Defensive rotation into healthcare, utilities, industrials |

Rate sensitivity and AI supply chain position are now working in the same direction, compressing the same set of tech names simultaneously. Companies with strong current earnings are insulated on both fronts. Companies with premium multiples and rising infrastructure costs are exposed on both.

The structural thesis and the macro overlay converge on a practical diagnostic. Run any tech holding through these three questions:

If your tech holding answers favourably on all three, AI and the rate environment are likely working for it. If it stumbles on two or more, the structural and macro headwinds are compounding against it.

The single-session divergence on 25 June 2026 is not a news event to note and move past. It is a visible expression of a structural condition that will continue sorting tech winners from losers as the AI buildout matures.

The Philadelphia Semiconductor Index’s 3.6% advance alongside Micron’s 16% gain shows the market already pricing this as a sub-sector thesis, not a single-stock story. The Nasdaq’s projected 4.4% weekly decline alongside the Dow’s 0.7% gain shows the defensive rotation reinforcing the same split from the macro side.

The hardware and software divergence that Micron and Apple made visible in a single session on 25 June has been building across the full year: semiconductor equipment names gained 47.6% in 2026 while software applications fell 22.7%, a spread of more than 70 percentage points that reflects the same supply chain logic playing out at sector scale.

The variable that would change the calculus is clear: when software and platform companies begin generating AI-driven revenue at a scale comparable to their infrastructure costs, the cost-absorber dynamic weakens. Until that inflection arrives, the semiconductor-beneficiary thesis holds, and the companies sitting on the right side of the AI supply chain, the ones generating $18.3 billion in quarterly free cash flow from it, remain structurally advantaged.

The Micron quarter confirmed what the supply chain economics already implied: the AI buildout is not a rising tide. It is a current flowing in one direction. The investor’s job is to determine which side of that flow their exposure sits on.

When the next AI-related catalyst hits, the first question is no longer “is this good for tech?” It is: which part of the supply chain captures the upside, and which bears the cost?

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Semiconductor stocks are shares in companies that design or manufacture chips, memory, and related hardware components. They sit at the centre of AI investing because every AI model requires massive amounts of memory and processing power, making chipmakers like Micron direct revenue beneficiaries of the AI infrastructure buildout.

Micron reported fiscal Q3 2026 results showing revenue of $41.46 billion, up more than 4x year over year, and net income of $28.24 billion, up approximately 10x, driven by what management described as heightened demand from the AI surge in data-centre and cloud memory.

Apple raised prices across its iPad and MacBook ranges to absorb higher memory component costs driven by AI-related demand, placing it on the cost-absorber side of the supply chain rather than the revenue-beneficiary side, which the market repriced immediately.

Ask three questions: does the company generate direct revenue from AI infrastructure demand, does its earnings growth justify its valuation without relying on distant projections, and does it have strong operating cash flow relative to its capex and debt. Companies that answer favourably on all three sit on the beneficiary side of the AI supply chain.

Higher rates compress the present value of future earnings, hitting companies with premium multiples and limited current earnings hardest. Micron's $18.3 billion in quarterly free cash flow and 4x revenue growth provide insulation that most software and consumer tech names with high price-to-earnings ratios and rising infrastructure costs do not currently have.