Barclays Flags Structural Bond Reset With 4.65% Yield Call

49 mins ago

Two semiconductor earnings releases landed on 24 June 2026, and by the following morning Micron shares were up roughly 20% in premarket trading while a broad chip rally was spreading across the sector. The question worth asking is not whether the numbers were good but what kind of good they were.

Micron and Qualcomm are not telling the same story, but together they reinforce the same underlying conclusion: AI infrastructure spending is running ahead of consensus expectations, and the hardware ecosystem built around it is repricing in real time. For investors holding technology exposure or weighing entry points in semiconductors, these two data points landed on the same day and pointed in the same direction.

Here is what the specific numbers behind each company’s results actually signal about the AI spending cycle, and which variables will determine whether this semiconductor stock rally marks a new leg up or a late-cycle spike.

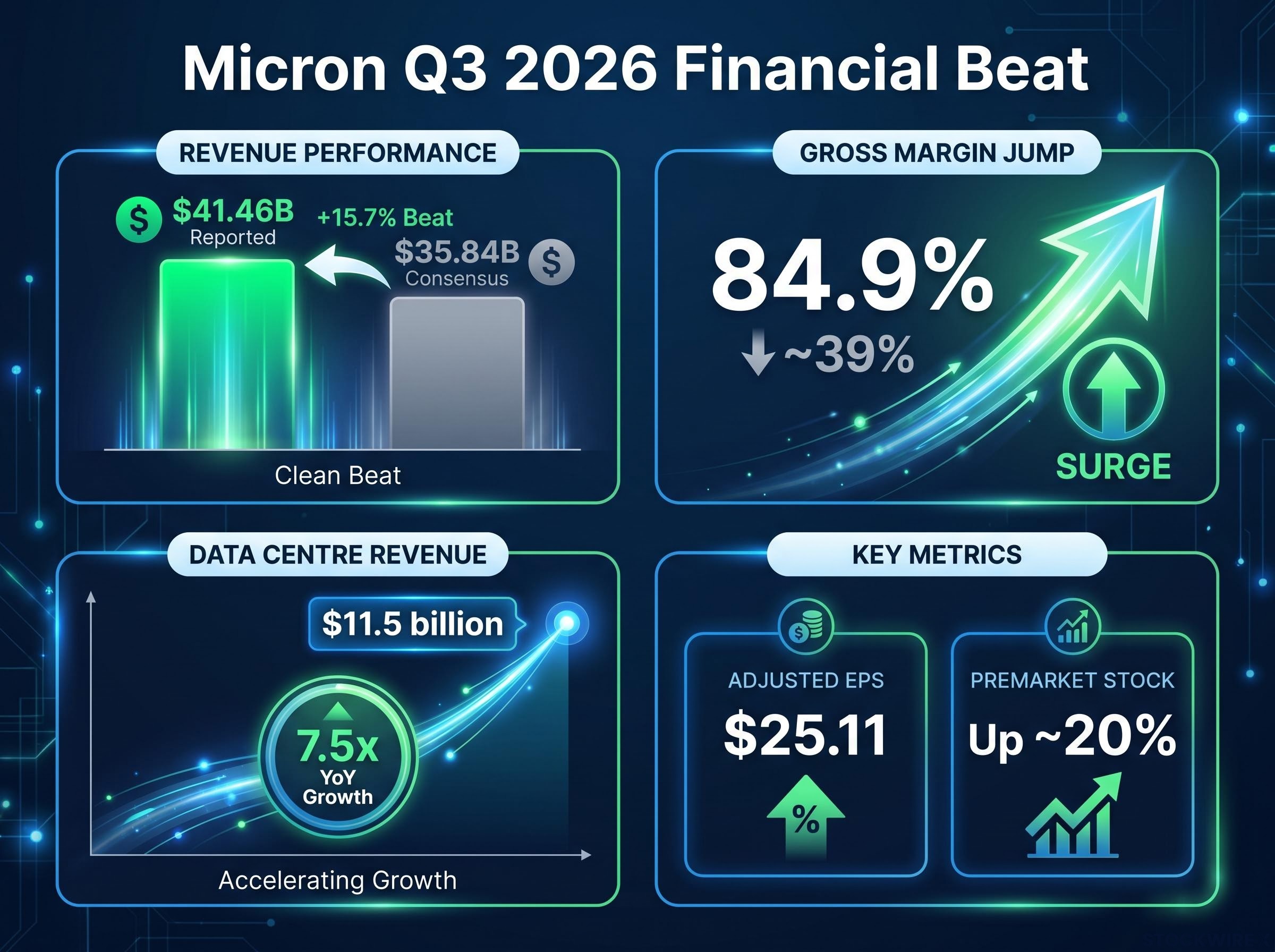

Start with the headline: Micron delivered fiscal Q3 2026 revenue of $41.46 billion, clearing Wall Street’s consensus estimate of $35.84 billion by a substantial margin. Adjusted earnings per share of $25.11 topped analyst forecasts with room to spare. Data centre segment revenue reached $11.5 billion, representing growth of more than seven times compared with the prior year period, and total data centre and cloud storage revenue exceeded $25 billion.

Those are the raw numbers. Here are the ones that matter more:

| Metric | Reported | Comparison point |

|---|---|---|

| Revenue | $41.46B | $35.84B consensus |

| Adjusted EPS | $25.11 | Analyst consensus (beat) |

| Gross margin | 84.9% | ~39% in Q3 FY25 |

The structural signal: Gross margins moving from 39% to 84.9% in a single year do not happen in a normal pricing upcycle.

That margin expansion tells you customers are paying for performance and time-to-deployment rather than cost per bit. It means Micron holds genuine pricing power right now, and the scale of the beat forces analysts to revise near-term earnings models upward, which mechanically pushes valuations higher even on flat multiples.

The scale of the current AI investment cycle, with US IT spending reaching 4.9% of GDP in Q1 2026 and surpassing every prior technology investment peak including the dot-com era, provides the macro context for why a memory supplier can post 84.9% gross margins without triggering immediate demand destruction.

To understand why Micron’s margins are this wide, you need to understand the product at the centre of the demand surge: high-bandwidth memory, or HBM.

Micron has indicated it is supply-constrained in HBM and advanced DRAM. That distinction matters. Being supply-constrained means demand is so strong that the company cannot make enough product to satisfy it. That is a structurally different situation from a typical inventory cycle where a company builds stock and waits for orders.

Advanced packaging complexity is the bottleneck. Stacking dies, sourcing specialised substrates, and qualifying new production lines takes 12-18 months at minimum. Equipment lead times compound the delay. The practical result is that supply additions cannot keep pace with the current demand curve, which reinforces the durability of Micron’s current pricing power.

Investors wanting to model the specific supply mechanics behind Micron’s capacity constraints will find our full explainer on the global DRAM shortage, which details why SK Hynix projects tightness through 2030 and why $200 billion in committed capex cannot deliver meaningful new HBM output before 2027-2028.

For investors, a supply-constrained Micron signals that AI training clusters are still being built aggressively and that inference infrastructure is adding to demand rather than substituting for it. That changes the runway calculation for anyone trying to time this cycle.

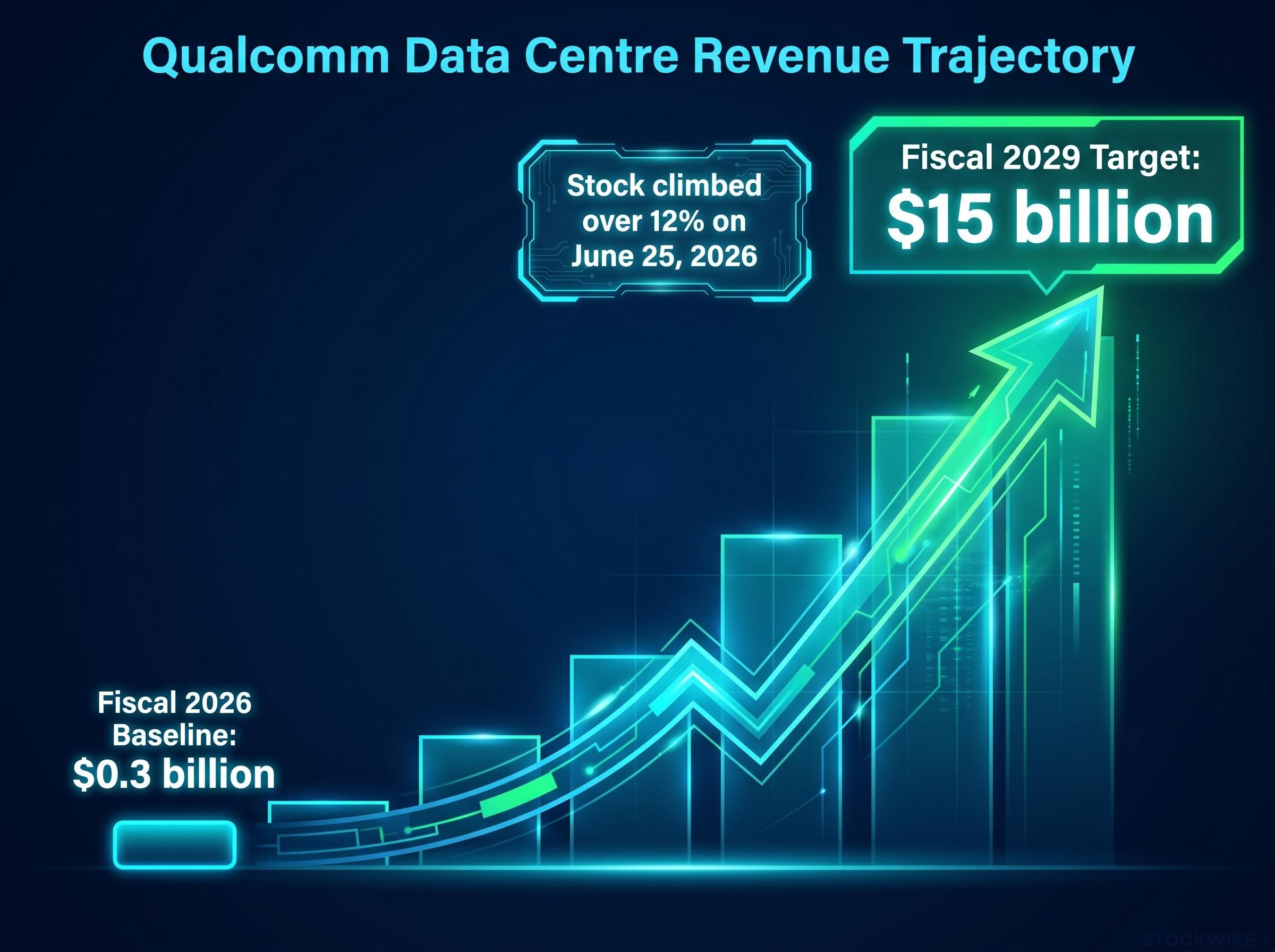

Qualcomm used its Investor Day on 24 June 2026 to project annual data centre revenue of $15 billion by fiscal 2029. The current baseline: roughly $0.3 billion in fiscal 2026. Its stock climbed over 12% when markets opened on 25 June 2026.

The scale of the shift: From $0.3 billion today to a $15 billion annual target by fiscal 2029.

A business that has historically been priced as a smartphone chip supplier now requires investors to reconsider its total addressable market and what earnings multiple that warrants. Three strategic implications flow from this:

The $15 billion target is not just a Qualcomm story. It implies AI data centre capex is structurally higher and longer-duration than many prior models assumed, which affects how investors should model the whole sector.

Micron’s close to 20% premarket move and Qualcomm’s gain of more than 12% combined to set off a wide advance across semiconductor equities worldwide. That breadth is the tell.

Together, these two companies delivered two complementary signals: current earnings power is higher than modelled, and the future opportunity is larger and longer than modelled. Each part of the semiconductor value chain benefits from a different piece of that message.

Memory chip stocks had already repriced sharply before this earnings release: Micron, Sandisk, and SK Hynix combined for gains exceeding 250% in the 30 days ending 12 May 2026, a move driven by the same sold-out HBM capacity and manufacturing complexity that the June quarter results confirmed as durable rather than transient.

| Segment | Immediate benefit | Longer-term driver |

|---|---|---|

| Memory suppliers | Sustained margin and pricing power | Multi-year AI demand curve |

| Logic and accelerator vendors | TAM validation across multiple suppliers | Broadening customer base for AI compute |

| Foundries | Stronger utilisation outlook | Justified advanced-node capex |

| Equipment and materials | Rising order volumes | Extended capacity-addition runway |

A rally built on analyst estimate revisions, forced by actual reported numbers, is more durable than one built on forward narrative alone. Micron’s beat will require consensus EPS forecasts to move meaningfully higher, creating a mechanical floor under the valuation. That is fundamentally different from a momentum-driven spike on optimistic commentary.

When investors buy equipment makers, foundries, and memory peers simultaneously, they are re-rating the AI infrastructure ecosystem as a whole. That kind of move tends to be stickier than single-stock momentum, and it matters for anyone holding broad semiconductor or technology ETF exposure.

The results are strong. The forward risks are real. Distinguishing between the two is what separates a durable position from a cyclical trade.

The single most important forward indicator: Hyperscaler capex guidance. Any shift toward language of capacity digestion or spending slowdowns would be a direct negative for the memory and AI accelerator demand outlook.

Here are the specific variables to watch:

The prior technology sector selloff demonstrated how quickly sentiment can reverse. For investors deciding whether to add semiconductor exposure today, the key question is not whether AI spending is real but whether the current pricing and margin environment will persist long enough to justify current valuations. Hyperscaler capex guidance over the next two quarters is the clearest read on that.

Hardware valuation risks tied to hyperscaler capex concentration are not hypothetical: the four largest cloud providers account for approximately 17% of S&P 500 market capitalisation, and a shift in their spending language toward capacity digestion would mechanically compress consensus earnings models for memory, foundry, and equipment stocks simultaneously.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to change based on market conditions and various risk factors.

25 June 2026 delivered a two-part confirmation. Current AI demand is running well ahead of prior estimates: Micron’s 84.9% gross margin and 7.5x data centre revenue growth proved that. And credible industry players now see a multi-year runway for large, high-margin data centre revenue: Qualcomm’s $15 billion 2029 target from a $0.3 billion base established that.

The debate has shifted. It is no longer “is AI infrastructure spending real?” The question now is how long this cycle lasts and which parts of the value chain capture the most durable margin. The broader earnings cycle reinforces that leading technology firms remain in aggressive build-out mode, not consolidation mode.

Three forward confirmation points will determine whether this rally extends or consolidates:

Investors who understand that the conversation moved from existence to duration on 25 June are better positioned to decide what to own and for how long. The data is now clear enough to frame the decision. What remains is execution, and the next set of earnings will tell you whether the execution is matching the ambition.

—

High-bandwidth memory (HBM) is a type of memory chip stacked directly alongside AI accelerator processors to deliver far faster data throughput than standard DRAM. It sits at the centre of the current semiconductor stock rally because demand is so strong that Micron cannot make enough of it, a supply constraint that takes 12-18 months minimum to address and is keeping pricing power unusually high.

Micron reported fiscal Q3 2026 revenue of $41.46 billion against a consensus estimate of $35.84 billion, with adjusted EPS of $25.11 and a gross margin of 84.9%, up from approximately 39% a year earlier. Data centre segment revenue reached $11.5 billion, representing roughly 7.5x year-over-year growth.

Qualcomm announced at its Investor Day on 24 June 2026 that it targets annual data centre revenue of $15 billion by fiscal 2029, up from roughly $0.3 billion in fiscal 2026. The scale of that projection forced investors to reprice the company's total addressable market and earnings potential well beyond its historical identity as a smartphone chip supplier.

The two earnings prints delivered complementary signals: current earnings power is higher than analysts modelled, and the future data centre opportunity is larger and longer than previously assumed. Each part of the semiconductor value chain, from memory suppliers and foundries to equipment makers, benefits from a different part of that message, which is why the re-rating was broad rather than stock-specific.

The most critical variable is hyperscaler capex guidance: any shift toward capacity digestion language from cloud providers would immediately compress demand forecasts for memory, foundry, and equipment stocks. Additional risks include faster-than-expected HBM supply additions compressing Micron's margins, Qualcomm failing to secure the design wins needed to hit its $15 billion target, and export control restrictions affecting AI infrastructure spending.