Morningstar vs Markets: a 125-Point Gap in the US Rate Outlook

8 mins ago

Barclays published a twelve-month forecast on 25 June 2026 projecting U.S. 10-year Treasury yields at 4.65%. That number is not a rate call. It is the headline output of a structural argument that the rules governing how government bonds are priced, owned, and traded have changed for years to come.

The forecast sits inside a broader research note identifying two reinforcing forces reshaping fixed income markets simultaneously: a sovereign bond supply shock that central banks can no longer absorb, and a Federal Reserve that has deliberately become harder to predict. Neither force is temporary. Together, they amount to what Barclays calls a “multi-year reset in how sovereign debt is priced and owned,” and the implications reach anyone holding bond allocations, not just professional rate traders.

Here is what the analysis tells you about whether the bond position you currently hold is sized for the market that actually exists now, rather than the low-rate, low-volatility environment that ended three years ago and is not coming back.

The distinction matters. A cyclical rate spike argues for patience: sit tight, wait for the reversal, collect the coupon. A structural reset argues for repositioning, because the old equilibrium is gone and the new one has not finished forming.

Barclays frames this explicitly as the latter. The bank’s recommendation targets long-duration sovereign bonds specifically, not fixed income broadly, which is a precise and important distinction. Short-dated credit and intermediate maturities sit in a different category. The risk concentration is in the long end of government curves.

Barclays’ twelve-month forecast: U.S. 10-year Treasury yields at 4.65%, published 25 June 2026, anchored to a structural thesis rather than a tactical rate view.

The thesis rests on two structurally independent pillars that happen to reinforce each other. The first is a supply-demand imbalance in sovereign debt markets. The second is a Federal Reserve that has become deliberately less predictable. Each one would matter on its own. Together, they reset the maths for anyone holding long-duration government bonds as a core allocation.

OECD sovereign bond issuance is on course for a new annual record in 2026. The drivers are persistent and well understood: post-COVID debt loads, expanded defence spending across NATO members, energy transition costs, and structurally loose fiscal policy in the United States, Europe, and the United Kingdom. None of these spending programmes have an end date.

That is the supply side. What has changed is who is available to buy it.

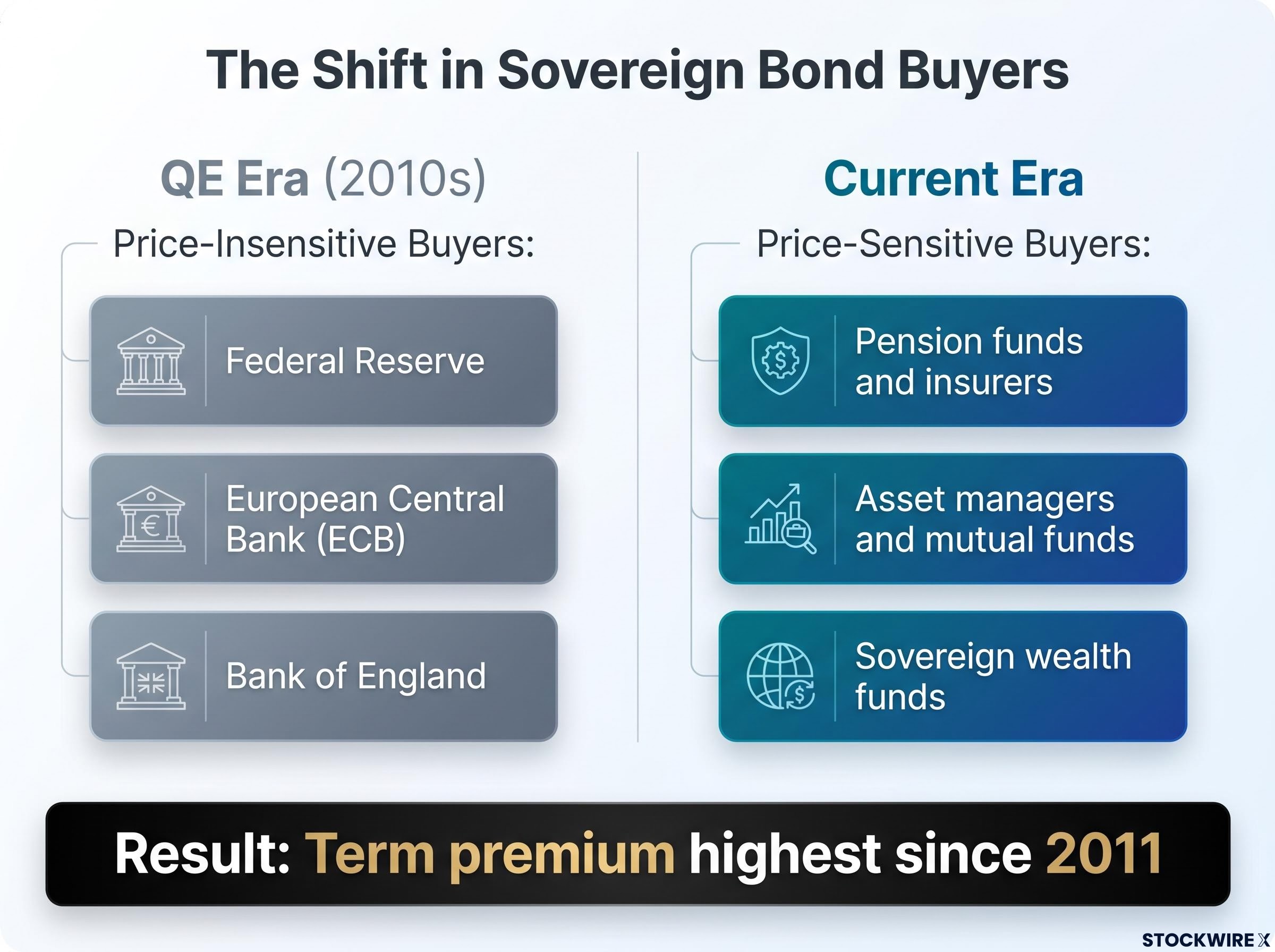

During the decade of quantitative easing (QE), central banks purchased enormous quantities of government bonds regardless of price. That programme, where central banks create money to buy bonds in order to keep yields low, meant the Fed, European Central Bank (ECB), and Bank of England functioned as the marginal, price-insensitive buyers of duration. They compressed yields and absorbed supply risk.

That structural support has been removed. Central banks have shifted to quantitative tightening, allowing bonds to roll off their balance sheets. No new QE programme is on the horizon. The buyer base has shifted to institutions that care very much about what they pay:

Each of these buyer types has a return threshold. None will accept the negative real yields or suppressed term premia that prevailed when central banks were the backstop.

The result is visible in the data. According to Barclays, the additional compensation that investors require for holding long-dated U.S. Treasuries rather than rolling shorter-term debt has reached its highest point in fifteen years. The bank’s view is that this repricing remains incomplete and further adjustment is expected.

The supply-demand imbalance would be significant on its own. The Fed dimension amplifies it.

Barclays characterises the new Fed chair’s approach, observed at the first meeting under the new leadership reported in June 2026, as a deliberate departure from the communication clarity that defined the previous decade. The shift involves greater emphasis on real-time inflation signals, a deliberate scaling back of forward guidance, and a meeting-by-meeting decision framework rather than a mapped-out rate path.

What markets are losing is meaningful. In the 2010s, participants could map the Fed’s likely rate path 12-18 months ahead with reasonable confidence. The dot plot, press conferences, and “path” language gave traders and portfolio managers a stable planning horizon. That clarity has been structurally reduced.

Barclays identifies three specific structural consequences:

Barclays notes that this policy transition has so far been only partially absorbed by markets, with the full repricing still ahead. For anyone holding long-duration positions, less policy predictability means hedging duration risk becomes structurally more expensive and complex, raising the effective cost of those positions beyond what the nominal yield alone suggests.

If long-dated yields are rising faster than short-dated yields, the signal is not random. It reflects a specific component of bond pricing called the term premium, which is the additional yield investors demand for lending money to a government over a long time horizon rather than repeatedly rolling over short-term debt. It compensates for three things: duration risk, inflation uncertainty, and policy unpredictability.

For a decade, QE suppressed term premia by removing risk from the market and placing it onto central bank balance sheets. Central banks bought long-duration bonds in vast quantities, compressing the premium that private buyers would otherwise have demanded. The result was an artificially low equilibrium that made long bonds appear safer and cheaper than they actually were.

| Era | Term premium level | Key driver |

|---|---|---|

| QE era (2010s) | Suppressed, often near zero or negative | Central bank absorption of duration risk |

| Current era (2026) | Highest since 2011 | Price-sensitive buyers replacing central banks |

With QE unwound and sovereign supply rising, the term premium is repricing toward levels that reflect actual supply-demand conditions. Barclays believes this process remains incomplete.

The implication is direct: even if the official policy rate stays flat, long bond prices can continue to fall as the term premium component of yield rises. Rate expectations alone do not capture the full downside risk in long-duration positions. That is the gap many bond investors are not accounting for.

The diagnosis leads to a specific set of positioning recommendations. Barclays characterises passive long-duration sovereign holdings not as a safe core allocation but as something quite different:

“A concentrated risk bet that requires explicit justification.”

The bank’s repositioning logic rests on four considerations:

The practical question this raises is straightforward: if the case for long-duration government bonds as a low-risk core holding has structurally weakened, the fixed income sleeve of a portfolio needs a different logic. Barclays is arguing that logic now centres on shorter duration, active management, and a willingness to hold credit risk where the compensation is adequate.

The two pillars reinforce each other. Record sovereign supply arriving at the same time as a more volatile, less predictable Fed creates a structurally higher equilibrium for both yields and rate volatility. Barclays explicitly does not see a return to the QE-era low-yield environment as a base case, and states that market pricing has not yet fully absorbed the structural shift.

The frame is multi-year, not quarterly. That changes how you monitor it. Three variables will signal whether the regime shift is tracking as Barclays projects or whether conditions are evolving differently:

The burden of proof has shifted. Holding a large long-duration sovereign position now requires an active reason to do so, not simply the absence of a reason to change. That is what a structural reset means in practice.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Term premium is the extra yield investors demand for holding long-dated government bonds instead of rolling over short-term debt, compensating for duration risk, inflation uncertainty, and policy unpredictability. Barclays reports it has reached its highest level since 2011, and argues the repricing is still incomplete, meaning long bond prices can continue falling even if the official policy rate stays flat.

Barclays published a twelve-month forecast on 25 June 2026 projecting U.S. 10-year Treasury yields at 4.65%, framing this not as a tactical rate call but as the output of a structural thesis: record OECD sovereign issuance, the withdrawal of central bank bond buying, and a more unpredictable Federal Reserve have combined to reset how sovereign debt is priced for years ahead.

Barclays characterises the new Fed chair's approach, first observed in June 2026, as a deliberate shift away from the forward guidance and mapped-out rate paths that defined the prior decade. The new framework emphasises real-time inflation signals and meeting-by-meeting decisions, expanding the range of plausible outcomes at each FOMC meeting and making duration hedging structurally more expensive.

Barclays recommends reducing exposure to long-duration sovereign bonds across global markets, favouring short-to-intermediate maturities, reassessing sovereign versus investment-grade credit (which becomes comparatively more attractive as risk-free yields rise), and shifting from passive set-and-forget duration strategies to active duration management calibrated for higher volatility.

Barclays identifies three key signals: OECD sovereign issuance volumes relative to price-sensitive buyer demand, FOMC communication style under the new chair (whether less predictable guidance persists or softens), and term premium movements from their current fifteen-year high. Continued term premium expansion confirms the repricing is ongoing; stabilisation or reversal would signal the structural adjustment is complete.