How to Read Clinical Milestones in ASX Biotech Stocks

5 hrs ago

Most of the world’s cell therapy capital sits in the United States and Europe. The clinical infrastructure, the regulatory precedent, the institutional investor base fluent in pre-revenue biotech risk: all of it is concentrated offshore. If you are an Australian investor looking for direct exposure to this category, you are not choosing between equivalent options. You are navigating a genuine access problem.

That problem matters now because the global cell therapy pipeline is advancing quickly. Several ASX-listed companies are conducting clinical programmes that hold their own against global peers, generating milestone data, engaging the FDA, and presenting at international oncology conferences. Yet the analytical tools most investors instinctively reach for, earnings, margins, dividend yield, do not apply here. The gap between standard equity analysis and what this asset class actually requires is where most positioning errors begin.

This piece gives you a concrete framework for reading clinical-stage ASX biotech stocks in the cell therapy category. It uses a live programme as a worked example, walks through the milestone signals that replace financial metrics, and names the structural risks precisely enough that you can track them. After this, you will know what actually matters when there are no earnings to analyse.

Global cell and gene therapy investment is concentrated where the supporting architecture already exists: major US academic medical centres, dedicated manufacturing facilities in the US and Europe, and a deep institutional investor base that has been pricing clinical-stage risk for decades. The capital, the clinical infrastructure, and the regulatory precedent all sit predominantly offshore.

Alliance for Regenerative Medicine investment data from Q4 2025 confirms that cell and gene therapy capital remains concentrated in the United States and Europe, with clinical trial activity following the same geographic distribution, which explains the structural access gap facing Australian investors seeking direct programme-level exposure.

Large-cap global pharmaceutical companies offer one route into this category. Pfizer, Novartis, and Bristol Myers Squibb all hold cell therapy assets. But those pipeline programmes typically represent small fractions of enterprise value. Diversified revenue bases, established commercial operations, and earnings-driven valuations dominate. What you get is indirect, diluted exposure to the innovation layer where cell therapy is actually being advanced.

ASX-listed clinical-stage biotechs offer a structurally distinct access point. There is no commercial revenue, no dividend, and no earnings metric to anchor valuation. Instead, you are exposed directly to programme-level information: trial progression, regulatory designations, and scientific conference outcomes. That exposure is concentrated rather than diluted, and it demands a different analytical posture from the start.

| Attribute | Large-cap global pharma | ASX clinical-stage biotech |

|---|---|---|

| Revenue profile | Diversified commercial revenue | Pre-revenue |

| Primary value signals | Earnings, margins, dividends | Clinical milestones, regulatory designations |

| Analytical framework | Financial metrics, product cycle analysis | Programme advancement, regulatory pathway clarity |

| Investor exposure type | Indirect; pipeline is a fraction of enterprise value | Direct; programme progression drives valuation |

If you want direct exposure to cell therapy at the clinical development stage, large-cap pharma is limited by design. The ASX route requires a different toolkit, and understanding that toolkit is what the rest of this analysis provides.

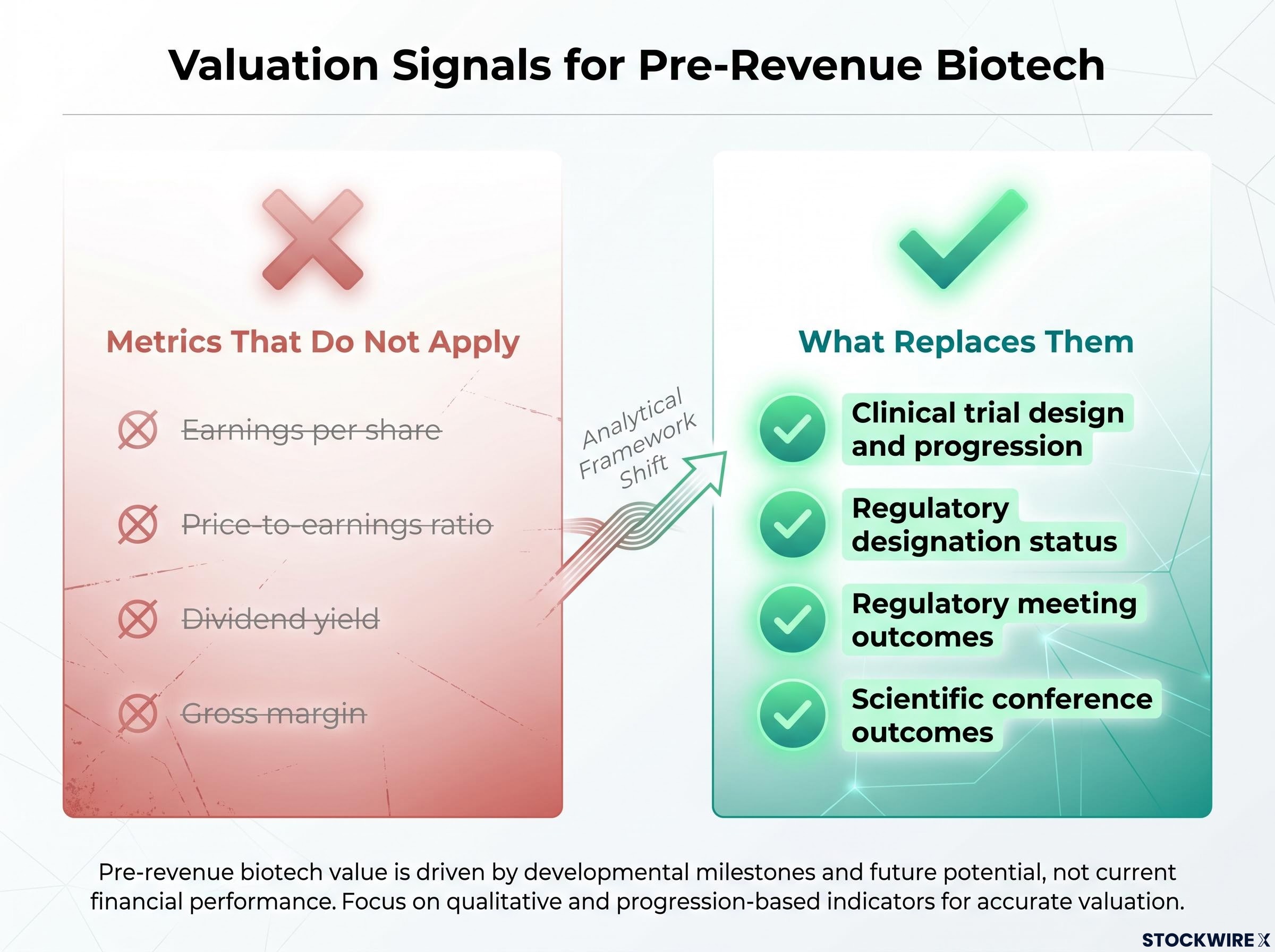

“Pre-revenue clinical-stage” means exactly what it sounds like: no commercial product on the market, no earnings metrics, no dividends, and valuation driven entirely by programme-level information. Conventional financial analysis, earnings per share, price-to-earnings ratios, gross margins, has limited relevance in this context. These metrics will matter if a programme reaches commercialisation, but at the clinical stage, they tell you almost nothing about value progression.

So what replaces them? Four categories of observable information carry the analytical weight:

And the metrics that do not carry weight here:

One important structural point: an ASX listing is a capital markets mechanism, not a constraint on where programmes operate. An ASX-listed company can run US trials, engage the FDA, and target global oncology markets. The domestic listing is the access point. The innovation cycle is international. For investors trained on financial statements, the shift to milestone-based analysis is not a downgrade in rigour. It is a different set of rigorous tools applied to a different type of information.

The shift from earnings-based to milestone-based analysis sits within a broader ASX stock evaluation framework that covers how to read continuous disclosure filings, identify upgrade and downgrade cycles, and distinguish business quality from valuation, skills that apply across the ASX regardless of sector.

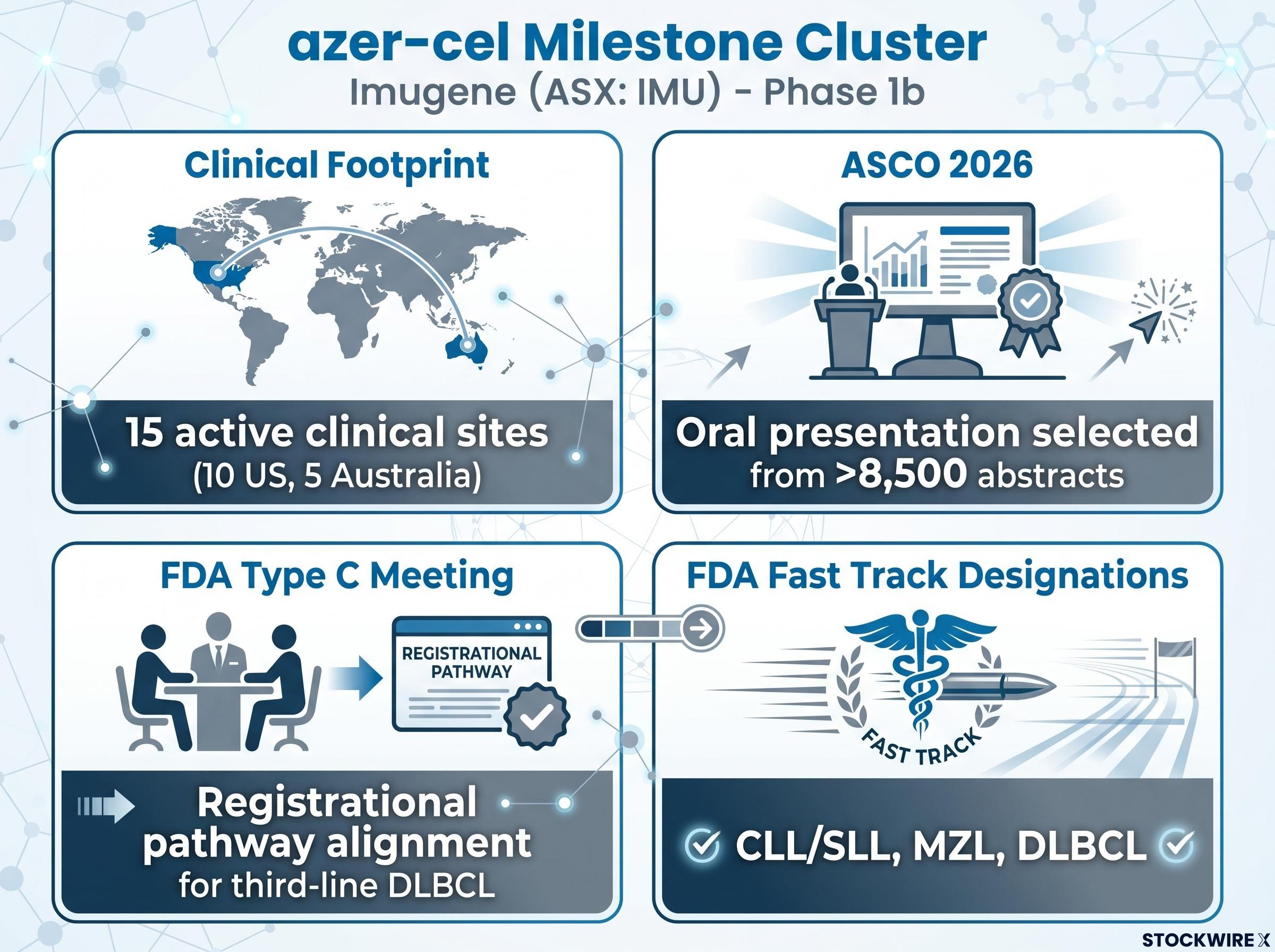

Among ASX-listed companies advancing clinical-stage cell therapy, Imugene (ASX: IMU) provides a concrete reference point for how this structure operates. Imugene is a clinical-stage oncology company with no commercial revenue. Its pipeline includes azer-cel (azercabtagene zapreleucel), an allogeneic CAR T-cell therapy candidate in a Phase 1b programme for B-cell haematological malignancies. Allogeneic CAR T uses donor-derived, pre-manufactured cells aiming for off-the-shelf scalability, as opposed to autologous CAR T, which uses each patient’s own cells and carries more complex manufacturing logistics.

The programme spans multiple countries, with sites distributed across 10 US and 5 Australian locations, bringing the total to 15 active clinical sites. That matters because it signals access to broader patient populations, engagement with US-based investigators embedded in the global oncology ecosystem, and orientation toward FDA-defined regulatory and commercial outcomes.

Here is how the current milestone cluster reads when you apply the framework from the previous section:

The azer-cel Phase 1b results reported in March 2026 provided the underlying efficacy data behind these milestone signals, with 100% overall response rates in CLL/SLL and 80% in MZL cohorts across a patient population with a median of two or more prior lines of therapy.

The FDA Fast Track Designation criteria require that a therapy address a serious condition and demonstrate the potential to fill an unmet medical need, which is why designation signals elevated regulatory engagement rather than any presumption of eventual approval.

At ASCO 2026, azer-cel programme data earned a place among oral presentations, selected through competitive abstract review of a field totalling more than 8,500 submissions, an independent, competitive scientific review that places the programme’s early data among the most visible in global oncology this year.

These indications sit within therapeutic categories shaped by BTK inhibitor therapies such as ibrutinib and zanubrutinib, a segment whose 2025 global market size has been estimated at around US$12.0 billion (though sources conflict; research data cites closer to US$10.4 billion). That figure is market context, not a revenue projection for azer-cel. It tells you these are large, clinically active disease areas with established diagnostic pathways and significant unmet need among patients who progress on or are intolerant to current therapies.

Viewed as a cluster rather than individually, these milestones indicate a programme that is actively executing at multicentre scale, has cleared competitive scientific review, and has concrete regulatory pathway guidance.

ASCO oral selection, Fast Track Designations, and FDA Type C meetings are early-stage signposts, not guarantees. Durability of efficacy across larger patient cohorts, safety signals that may emerge with scale, and comparative positioning against future competitors all remain ahead in the development path. Phase 1b is early. Multiple additional stages and inflection points lie between here and any potential approval.

The milestone cluster above is evidence of programme momentum and external validation. It is not evidence of eventual success. Any realistic framework for this category must account for the structural risks that define it.

Regulatory risk deserves separate emphasis. Designations and pathway guidance do not guarantee positive regulatory decisions. Changing standards, new competitor data, or emerging safety concerns can alter development trajectories at any point.

FDA institutional capacity has deteriorated materially since 2025, with the agency losing more than 1,300 employees, creating unpredictable approval backlogs that fall disproportionately on cell and gene therapy programmes and novel oncology products, the exact categories where ASX-listed clinical-stage biotechs have concentrated their US regulatory strategies.

These are not reasons to avoid the category. They are the terrain on which returns are pursued, and understanding them precisely is what separates informed exposure from uninformed speculation.

For investors wanting to see how these structural risks have played out in practice across recent ASX healthcare history, our deep-dive into ASX healthcare risk mispricing examines how Immutep’s 90% single-session collapse and two major large-cap selloffs reveal the distinct risk profiles concealed behind the broader healthcare label.

The allogeneic CAR T segment sits at an early but maturing phase of global clinical development. Multiple programmes are advancing toward mid-stage trials, and the strategic rationale, off-the-shelf scalability that addresses the manufacturing constraints of autologous approaches, continues to attract development investment. The landscape is still evolving, with no consensus yet on which allogeneic platform will ultimately deliver durable commercial-scale results.

For ASX investors in 2026, the ability to read clinical milestones with calibrated precision is the practical skill that converts awareness of this innovation category into a disciplined investment posture. Knowing how to interpret ASCO abstract selection tiers, FDA designations, and registrational pathway guidance is itself the analytical edge. The frameworks are available even when the outcomes are not.

The analytical framework is the investor’s primary tool in this category. When there are no earnings to model, the quality of your milestone interpretation determines the quality of your positioning.

The BTK inhibitor segment, estimated at roughly US$12.0 billion across the B-cell malignancy settings where azer-cel holds Fast Track Designations, underscores the clinical and commercial importance of these disease areas. Approaching ASX-listed cell therapy exposure means combining awareness of the structural differences between large-cap pharma and clinical-stage listings with a milestone-calibrated reading of programme-level signals. That combination is what makes engagement with this category disciplined rather than speculative.

The access structure (ASX-listed clinical-stage versus large-cap pharma) and the analytical framework (milestone-based versus earnings-based) are the durable tools here, independent of any single programme’s outcome. The azer-cel milestone cluster is a worked example of the framework in action: it shows you what to look for, how to weight each signal, and where the boundaries of early-stage validation sit. It is not an endorsement or recommendation regarding Imugene or any specific company.

Engaging with ASX biotech stocks in this category requires applying the right framework consistently. Earnings-based analysis will not help you here. Milestone-based analysis, applied with calibrated expectations and clear-eyed risk awareness, will.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. These statements are speculative and subject to change based on market developments and company performance.

ASX biotech stocks in the clinical-stage category are pre-revenue companies whose value is driven entirely by programme-level milestones such as trial progression and regulatory designations, not earnings or dividends. Large-cap pharma like Pfizer or Novartis hold cell therapy assets too, but those pipelines represent a small fraction of enterprise value, making ASX clinical-stage listings the more direct route to cell therapy exposure.

FDA Fast Track Designation is granted to therapies addressing serious conditions with the potential to fill an unmet medical need; it enables more frequent FDA interactions and earlier alignment on trial design. It is a process milestone that signals elevated regulatory engagement, not an approval shortcut or guarantee of eventual commercialisation.

The four categories that carry analytical weight are clinical trial design and progression, regulatory designation status, formal regulatory meeting outcomes (such as FDA Type C meetings confirming a registrational pathway), and scientific conference outcomes including whether data earns a competitive oral presentation at a major event like ASCO.

Azer-cel (azercabtagene zapreleucel) is an allogeneic CAR T-cell therapy candidate being developed by Imugene (ASX: IMU) for B-cell haematological malignancies, currently in a Phase 1b programme running across 15 active clinical sites spanning 10 US and 5 Australian locations.

The primary risks are development risk (most candidates do not reach approval), capital dilution from repeated equity raises required to fund pre-revenue operations, milestone dependency where a single negative readout can sharply reprice the stock, thin liquidity on many ASX biotech names, and cyclical compression of valuations during risk-off market environments.