Most first-time investors know they should research a stock before buying it. Very few know what to actually look for once they open the annual report. The problem for Australian beginners is not access to information. ASX-listed companies must disclose financial performance every six months, and continuous disclosure rules require them to update the market when circumstances change materially. The real gap is a framework for interpreting what all that information means.

What follows is a practical, step-by-step methodology for evaluating any ASX-listed company, drawing on how professional fund managers at firms like Wilson Asset Management actually approach the task. It covers where to start, what signals to prioritise, what red flags to avoid, and how AI tools can compress research time without replacing judgement.

Start with documents any investor can access for free

The phrase “do your research” stops most beginners cold. It sounds like it requires a Bloomberg terminal and a finance degree. It does not.

Every ASX-listed company maintains an investor relations section on its website. The documents housed there are free, public, and far more readable than most people expect. Three types matter most:

- Annual report: Contains the full financial statements, director commentary, and the CEO’s letter, which is the single most accessible starting point for any new investor.

- Investor presentations: Function like a structured pitch deck, summarising the investment case, recent results, and longer-term financial targets (often extending to 2030 or 2035) in a visual, digestible format.

- Regulatory filings (ASX announcements): The continuous disclosure record required under ASX Listing Rule 3.1, which obliges companies to immediately notify the market of any information that could materially affect the share price.

That disclosure obligation matters. It means the filing record is not marketing spin alone; it carries legal accountability. Under the rule, a company that becomes aware its earnings are likely to differ materially from prior guidance must promptly update or withdraw that guidance.

Missing financial reports sit alongside adverse audit opinions and unexplained board departures as governance warning signs that ASIC now treats as enforcement priorities, with three ASX-listed companies collectively fined $1.17 million in 2026 for multi-year non-lodgement failures that retail investors in small-cap positions had limited time to act on before liquidity dried up.

The ASX Listing Rule 3.1 continuous disclosure obligations set out in ASX Guidance Note 8 require listed entities to immediately notify the market of any information that a reasonable person would expect to have a material effect on the share price, giving retail investors the same legal right to that information as institutional fund managers.

How to read an annual report without getting lost

Start with the CEO’s letter. It provides a plain-language overview of performance, strategic direction, and the forward outlook, written for shareholders rather than analysts. Move to the investor presentation next, which condenses the same themes into slides with charts and targets.

Leave the full financial statements for last. According to Anna Milnes, Deputy Portfolio Manager at Wilson Asset Management, the last five to six years (approximately 2019 to 2025) represent a particularly instructive review window, covering COVID disruption, supply chain stress, rising interest rates, and recovery cycles. Footnotes in the financial statements often contain material detail, and AI tools (covered later in this guide) can help surface that information efficiently.

When big ASX news breaks, our subscribers know first

What a good business actually looks like on paper

Knowing where to find documents is the first step. Knowing what to look for inside them is the step that builds real analytical instinct.

The first and most reliable green flag is a business model simple enough for any layperson to explain in one sentence. Complexity is not a sign of sophistication. It creates information asymmetry, meaning professional investors can exploit what retail investors cannot see. A company whose revenue model is straightforward to describe is a company whose risks are easier to assess.

Beyond business model clarity, the following signals form a practical checklist:

The green flags outlined above gain precision when anchored to quantitative benchmarks, and the fundamental analysis metrics that matter most, including P/E ratio, earnings per share, revenue growth, profit margins, and return on equity, each answer a distinct question about whether a business is performing and whether its price reflects that performance.

- Upgrade cycle: A period of rising earnings expectations from analysts, which tends to correlate with a rising share price because it reflects improving operating momentum.

- Gearing within target range: Many companies disclose a target debt-to-equity ratio in their investor presentations. Some debt is not inherently negative (it can enhance returns on equity), but a company operating within its disclosed gearing range signals disciplined capital management.

- Revenue growth and margin expansion: A growing top line combined with expanding profit margins attracts more buyers than sellers, supporting the share price over time.

- Credible management communication: How a CEO communicates matters. Watch video of results presentations and conference panels where available.

Anna Milnes, Deputy Portfolio Manager at Wilson Asset Management, describes management quality and emotional intelligence as underrated factors in investment assessment. Watching video footage of a CEO presenting, including noting body language and communication style, is a practical technique available to retail investors evaluating larger ASX-listed companies.

Knowing what a green flag looks like prevents beginners from being drawn in by brand familiarity or a recently rising share price rather than the underlying quality of the business.

How to spot warning signs before they cost you money

If upgrade cycles are the tailwind, earnings downgrade cycles are the storm. Recognising one early is among the most practical skills a beginner can develop, because the emotional pull to buy a fallen stock is strong and the consequences of acting too early are often severe.

An earnings downgrade cycle occurs when a company issues repeated downward revisions to its guidance. It tends to compound through three mechanisms:

- Guidance reset revealing deeper issues: The first cut often reveals that original assumptions were too optimistic. It signals that management’s forecasting may be weak, increasing the probability of future misses.

- Operational and financial knock-ons: Lower expected earnings can trigger cost-cutting that hurts growth, potential debt covenant pressure, loss of bargaining power with suppliers, and management departures.

- Valuation and sentiment spiral: A falling share price raises the cost of equity capital, making it harder to fund growth. Analysts lower target multiples, meaning the stock can de-rate further even if earnings stabilise.

This is the mechanism behind the concept of “catching a falling knife.” A sharply falling share price can look like a bargain. It is not sufficient justification to invest without evidence of stabilisation.

Cochlear (ASX: COH) illustrates the pattern. The company had previously delivered sustained annual revenue growth of around 10% with high profit margins, yet its share price fell approximately 65% in one year due to funding headwinds in the United States market and increased competitive pressure, compounded by multiple guidance downgrades. Several other ASX names experienced similar dynamics in 2024 to 2025:

| Company | Ticker | Downgrade trigger | Outcome |

|---|---|---|---|

| Cochlear | COH | US funding headwinds, competitive pressure | Share price fell ~65% in one year |

| Lendlease | LLC | Property revaluations, delayed exits, restructuring costs | Multiple consecutive earnings downgrades |

| Domino’s Pizza Enterprises | DMP | Rising costs, weaker same-store sales, failed international expansion | Repeated guidance cuts as management responses hurt volumes |

| Qantas | QAN | Intensified competition, regulatory scrutiny, cost inflation | Series of profit outlook trims after strong post-COVID commentary |

Balance sheet signals that separate manageable debt from dangerous debt

Excessive debt becomes dangerous when a company cannot comfortably service repayments, particularly as interest rates rise. Two measures matter alongside the gearing ratio: the interest cover ratio (how many times operating earnings cover interest payments) and free cash flow (cash generated after capital expenditure, which determines whether a company can actually pay down debt).

Investor presentations almost always include a balance sheet slide, making these figures accessible without needing to parse the full financial statements. Any divergence from a company’s disclosed gearing range warrants close scrutiny.

When a strong company isn’t a strong buy

Understanding green flags and red flags addresses the quality question. It does not address the price question, and the distinction between the two is the single most important conceptual shift a beginner needs to make.

A company’s share price is driven by supply and demand. When strong fundamentals attract buyers, the price rises. That rising price means the future return available to a new investor shrinks, even if the business continues to perform well. This is a valuation premium: the market has already priced in the good news.

A high-quality company is not automatically a sound investment if its share price already reflects an elevated valuation. Business quality and investment value at a given price must be assessed independently.

Cochlear’s recovery makes the lesson concrete. After declining approximately 65%, Cochlear shares recovered strongly, rising approximately 25-30% in the twelve months to mid-2025, according to reports from Livewire Markets (15 April 2025) and Motley Fool Australia (30 May 2025). The company’s long-term quality characteristics (sustained revenue growth, high margins, medical device leadership) remained intact throughout. But entry price still determined investor outcomes: those who bought at the peak before the downgrade cycle experienced a very different result from those who waited for stabilisation.

Australian investors will encounter two broad schools of thought on this question:

- Quality-first signals (emphasised by managers including Magellan, Hyperion, and Wilson Asset Management): management quality, competitive moat, capital allocation discipline.

- Value-oriented signals (emphasised by managers including Perpetual and Platinum): price-to-earnings ratio, price-to-book ratio, free cash flow yield.

Beginners benefit from understanding both lenses rather than committing dogmatically to one. The strongest analysis combines an assessment of business quality with a sober evaluation of whether the current price already reflects that quality.

The practical discipline of identifying undervalued stocks, using price-to-earnings ratio, free cash flow yield, and debt-to-equity ratio as overlapping filters rather than standalone rules, is where the quality-versus-price framework covered here becomes actionable in a real stock screen.

How to use AI tools to research stocks faster without cutting corners

AI tools are not a shortcut that replaces the framework above. They are a research accelerator that lowers the barrier to doing the hard work properly.

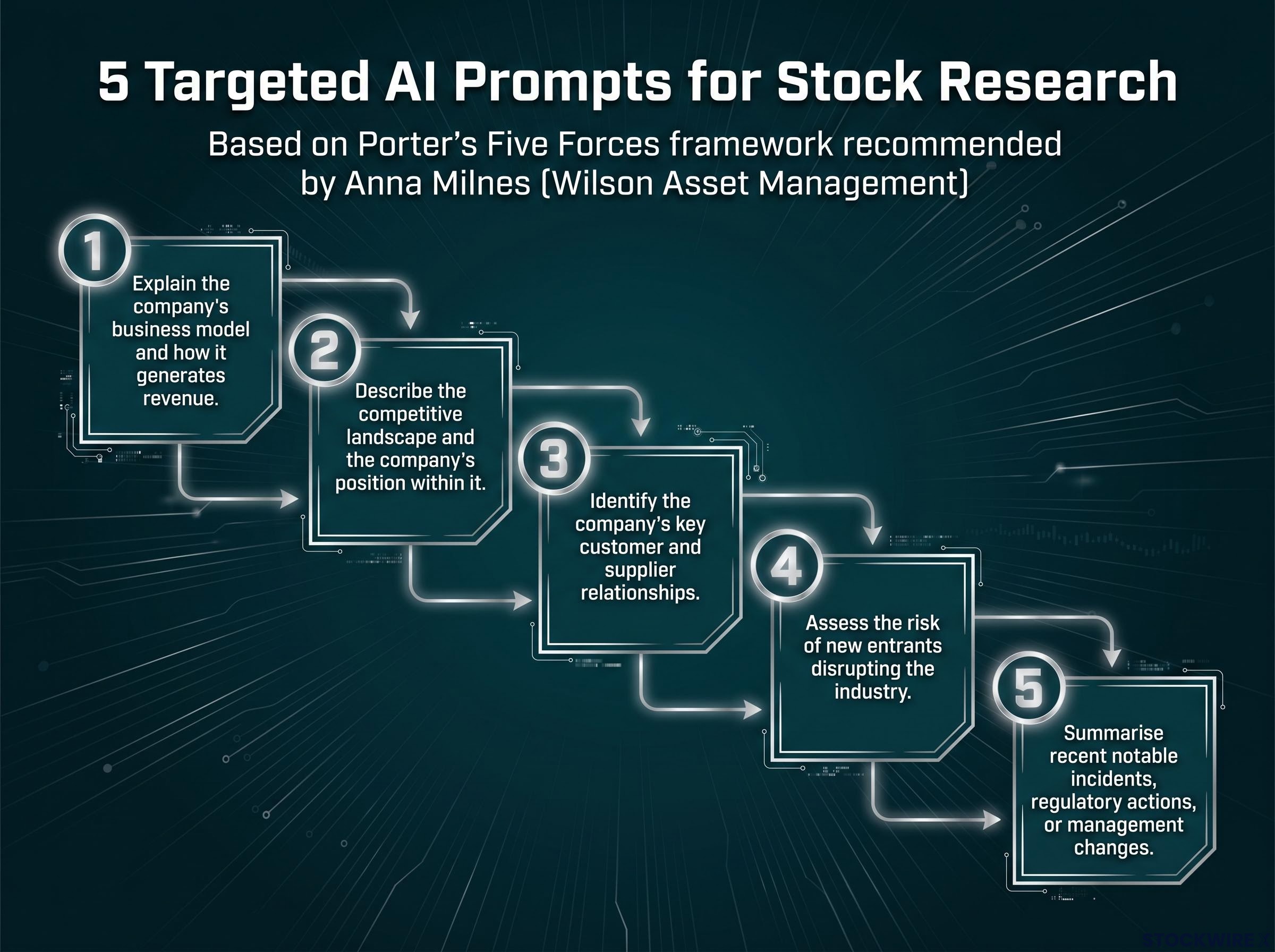

Anna Milnes of Wilson Asset Management advises approaching AI with specific, targeted questions rather than broad requests for stock tips. The recommended prompt framework maps to Porter’s Five Forces methodology and covers five areas:

- Explain the company’s business model and how it generates revenue.

- Describe the competitive landscape and the company’s position within it.

- Identify the company’s key customer and supplier relationships.

- Assess the risk of new entrants disrupting the industry.

- Summarise recent notable incidents, regulatory actions, or management changes.

Several AI tools are now accessible to Australian retail investors, each with a distinct use case:

| Tool | Best used for | Key limitation |

|---|---|---|

| Perplexity AI | Aggregating company news and broker commentary quickly | May surface outdated or unverified secondary sources |

| FinChat | Querying ASX financials and filings in natural language | Coverage of smaller ASX-listed companies can be limited |

| Microsoft Copilot (Excel) | Running scenario and sensitivity checks on EPS and debt ratios | Requires manual data input and verification of outputs |

| Simply Wall St | Automated commentary on valuations, dividend safety, and risk flags | AI-generated narratives can oversimplify complex situations |

| GuruFocus | Surfacing red flags such as deteriorating margins or rising leverage | Screening criteria may not reflect Australian regulatory nuances |

ASIC MoneySmart (2024) cautions that AI tools can produce plausible-sounding but inaccurate or out-of-date information, may not comply with Australian regulatory nuances, and are not a substitute for reading primary filings or obtaining licensed financial advice.

Morningstar Australia has separately noted that AI may miss footnote details that are material to valuations. The investor who uses AI well is one who already knows what questions to ask and treats the output as a starting point, not a conclusion.

Investors exploring the specific failure modes of AI tools in the ASX context will find our full explainer on AI limitations in ASX small cap research, which examines why AI can only synthesise publicly available consensus information, how confirmation bias is amplified when investors prompt with a bullish thesis, and what primary research disciplines professional small cap managers use instead.

The biases that will undo good research if you let them

A sound evaluation framework and good AI tools still cannot protect an investor from the biggest risk of all: their own cognitive patterns. Naming these patterns is the first step to countering them.

Five biases are most practically relevant for beginner Australian investors:

- Confirmation bias: Ignoring red flags that contradict an existing thesis. An investor who likes a company’s brand may dismiss a profit downgrade as temporary without investigating the downgrade cycle mechanisms outlined earlier in this guide.

- Recency bias: Chasing stocks that have recently risen, assuming the trend will continue. A beginner sees an ASX small cap up 40% in three months and buys without checking whether the price already reflects an optimistic scenario.

- Anchoring: Refusing to sell because the stock was once at a higher price. An investor who bought at $15 holds at $8, waiting to “get back to breakeven” rather than reassessing the thesis on current information.

- Herd behaviour and FOMO: Following finfluencer stock tips without independent analysis. ASIC has focused enforcement attention on finfluencer-driven pump-and-dump schemes affecting ASX small caps in 2024 and 2025.

- Overconfidence: Concentrating too heavily in a single stock or theme after a few early wins, underestimating how much of that success was market conditions rather than skill.

Practical habits that counteract common investor biases

The countermeasures recommended by Australian financial educators, including Morningstar Australia and ASIC MoneySmart, are consistent and worth committing to habit:

- Slow down: Impose a minimum waiting period before acting on any new stock idea. The urgency is almost never real.

- Diversify: Spread positions across companies and sectors to reduce the cost of any single misjudgement.

- Use primary sources: Annual reports and ASX announcements are the check on any secondary or AI-generated summary.

- Reassess on current facts: Ask whether the stock is worth buying today at its current price, not whether the goal is to recover a previous loss.

Research quality is only as good as the objectivity of the person conducting it. Understanding these biases is what turns a framework into a sustainable investing practice rather than a one-time checklist.

Putting the framework to work on your next stock idea

The methodology covered in this guide compresses into six steps that can be applied to any ASX-listed company this week:

- Find the documents. Go to the company’s investor relations page and download the latest annual report, investor presentation, and recent ASX announcements.

- Read for business clarity. Start with the CEO’s letter and investor presentation. If the business model cannot be explained in one sentence, note it as a risk.

- Check for green flags and red flags. Look for upgrade or downgrade cycles, gearing within the disclosed target range, revenue growth trajectory, and management credibility.

- Assess valuation against quality. Determine whether the current share price already reflects the company’s strengths. A good business at an expensive price may still deliver a poor return.

- Use AI to accelerate the work. Ask the five targeted questions (business model, competitive landscape, customer and supplier relationships, new entrant risk, recent incidents) and verify the outputs against primary filings.

- Audit your own biases before acting. Slow down, check multiple sources, and evaluate the stock on current facts rather than the price at which it was first noticed.

The five-year review window (approximately 2019 to 2025) remains the most instructive starting point for assessing how any ASX company has handled stress and recovery. The goal is not to find a perfect company but to make a well-informed decision with the information available. That process becomes faster with practice.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.