Micron Surges 9% After Guiding $6.4 Billion Above Consensus

7 hrs ago

Judo Capital Holdings shares lost nearly half their value in a single ASX session on Thursday 25 June 2026, after the small business lender revealed a profit downgrade and a sharp rise in bad loan provisions that blindsided a market told as recently as April that guidance remained intact.

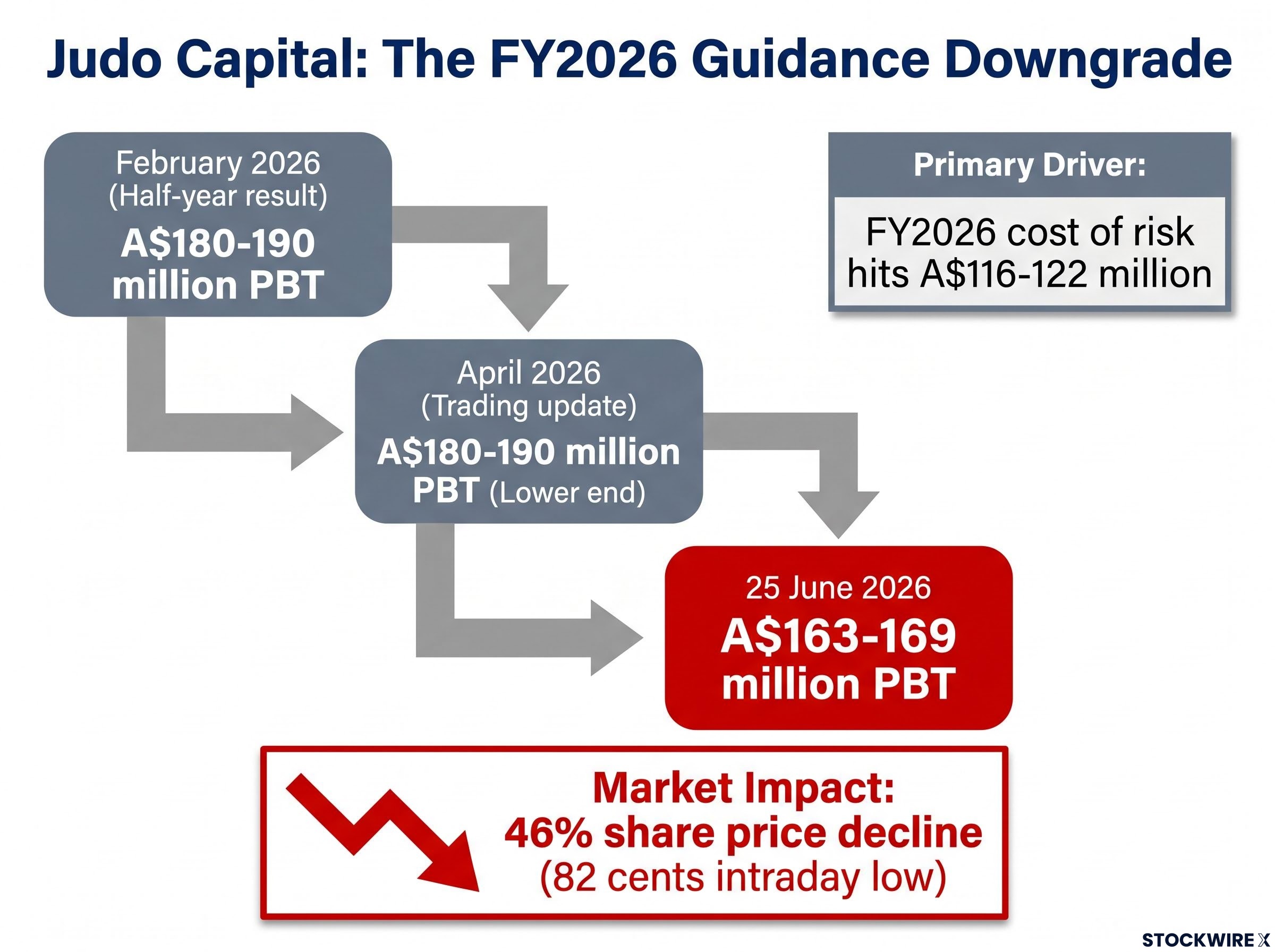

The severity of the move reflects more than a single bad quarter. It reflects a credibility event. Management had reaffirmed a profit before tax (PBT) range of A$180-190 million as recently as April 2026, even as it was simultaneously lifting collective provisions. The June disclosure that FY2026 PBT will now land at A$163-169 million arrived fast enough to trigger a fundamental repricing of the stock and a reassessment of what future guidance from this management team is actually worth.

Here is what actually changed in the numbers, why the credit story matters more than the headline profit miss, and what Judo’s FY2027 guidance would need to hold true for the recovery thesis to survive. If you follow ASX financials or hold JDO shares, you will come away with a clear framework for assessing what comes next.

Judo Capital shares collapsed on Thursday morning after the company released a trading and asset quality update for FY2026. The key market reaction facts:

The scale of the move makes it one of the most severe single-day declines on the ASX 200 in 2026. Panic selling, forced liquidation, and quant-driven flows likely amplified the drop beyond what pure fundamental repricing would imply, but that does not mean the repricing itself was unwarranted.

A 46% intraday decline on a disclosure that had been partially flagged (rising provisions were already visible in April) tells you that markets are not just repricing the numbers. They are repricing how much trust to place in management’s forward statements.

The timeline matters here as much as the numbers themselves. Judo had reaffirmed FY2026 PBT guidance of A$180-190 million at its February 2026 half-year result and again at its April 2026 trading update, where management indicated the result was tracking toward the lower end of the range. Then, in June 2026, the range was cut to A$163-169 million.

The provision build was not invisible before Thursday: Judo disclosed in its April 2026 trading update that collective provisions had risen five basis points to 94 basis points of gross loans, with targeted overlays applied across agriculture, construction, retail trade, manufacturing, and transport, sectors management flagged as facing elevated macroeconomic uncertainty.

| Guidance version | PBT range | Date communicated | Status |

|---|---|---|---|

| Original guidance | A$180-190 million | February 2026 (half-year result) | Superseded |

| April reaffirmation | A$180-190 million (lower end) | April 2026 (trading update) | Superseded |

| Revised June guidance | A$163-169 million | 25 June 2026 | Current |

Management has framed the revised result as delivering approximately 30% growth over FY2025, positioning it as strong earnings progression even after the cut. The primary driver of the downgrade is the FY2026 cost of risk, the total credit cost the bank expects to absorb this year:

FY2026 cost of risk: A$116-122 million. This is the provisioning expense that accounts for almost the entire gap between the old guidance and the new one.

A guidance cut within the same fiscal year, following multiple public reaffirmations, is precisely the pattern that causes markets to apply a credibility discount to future targets. Any future single-point guidance reaffirmation from Judo now carries a wider confidence interval than it did before today.

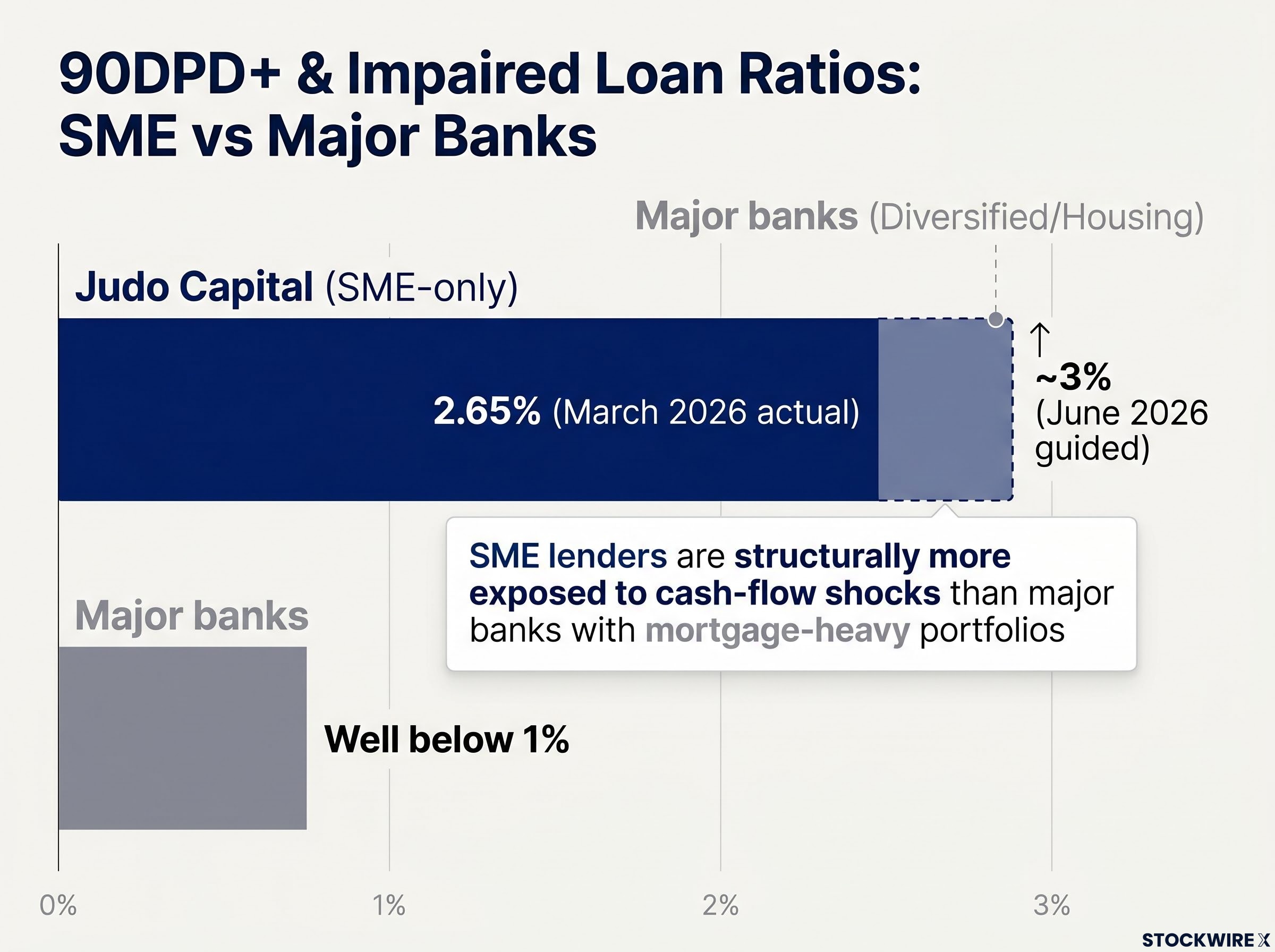

Before assessing the severity of Judo’s credit deterioration, it helps to understand what these metrics actually measure and why SME lending carries structurally different risk to the big-four banks’ mortgage-heavy portfolios. Three credit quality metrics matter here:

SME borrowers are structurally more exposed to cash-flow shocks and refinancing risk than households with prime mortgages. They carry thinner margins, higher operating leverage, and greater sensitivity to interest rate changes. That structural difference means a 3% impaired ratio at Judo cannot be directly compared to sub-1% group-level impaired asset ratios at the major banks. The loan books are fundamentally different in composition.

| Metric | Judo Capital (March 2026 actual) | Judo Capital (June 2026 guided) | Major banks (group level) | Loan book composition |

|---|---|---|---|---|

| 90DPD+ / impaired ratio | 2.65% of GLA | ~3% of GLA | Well below 1% | SME-only vs diversified (primarily housing) |

At 30 June 2026, collective provision coverage is projected to hold at roughly 94 basis points of gross loans and advances (GLA), a figure that translates to approximately 1.09% of standardised credit risk-weighted assets and was in line with the third-quarter trading update. The stability of that coverage ratio suggests management does not currently see broad-based portfolio stress, even as specific provisions have risen sharply.

When you see Judo’s 3% impaired ratio alongside a big-four bank’s sub-1% group figure, you are looking at fundamentally different credit exposures, not evidence that Judo is three times worse than the majors.

Judo’s credit challenge is unfolding within a broader ASX banking sector pressure environment: the major banks shed 7%-14% during May 2026 reporting season as margin misses and an $800 million collective provision build reset sector sentiment, leaving the entire sector navigating a tighter credit and funding cycle simultaneously.

A credit quality problem is not the same thing as a capital adequacy problem, and separating the two is the first step in assessing whether today’s selloff represents a temporary earnings hit or something more structural.

A RAC ratio above 15% tells you that Judo is not heading toward a capital crisis. A lender with adequate capital can absorb losses and recover; one with thin buffers cannot. But the capital ratio does not tell you whether the credit losses stop here or continue expanding. That distinction is the one that actually determines the forward earnings story, and it depends on data that has not yet been reported.

FY2027 PBT guidance: A$210-220 million. That implies approximately 30% growth over the revised FY2026 base, the same growth rate management is projecting for the year it just downgraded.

CEO Chris Bayliss has pointed to what he sees as strong underlying momentum in the business and expressed conviction in the overall quality of the loan portfolio. On a base-case reading, the guidance is not inherently unreasonable given the capital position and revenue trajectory. Judo’s core SME franchise continues to grow revenue and net interest margin.

But after today’s credibility event, the reader should treat A$210-220 million as a conditional target rather than a floor. The conditions that need to hold are specific, and so are the triggers that would falsify the story:

Understanding which specific variables will confirm or invalidate the FY2027 outlook gives you a structured way to monitor the story rather than reacting to each headline in isolation.

The selloff has forced a repricing, but it has not delivered a verdict. The resolution depends on data that arrives across the next two reporting periods.

The approximately 3% 90DPD+ ratio reflects a handful of identifiable problem loans. Collective provision coverage is stable, the capital position is sound above 15% RAC, and the core SME franchise continues to grow revenue and net interest margin. If specific provisions do not expand materially beyond the guided range and new 90DPD+ formations slow in H1 FY2027, the FY2027 guidance of A$210-220 million PBT remains achievable.

The credit deterioration arrives against a backdrop of genuine franchise strength: NIM expansion to 3.15% in Q3 FY26, a deposit funding cost advantage of approximately 74 basis points below the one-month BBSW, and a gross loan book that grew 3% in a single quarter all represent real operational progress that the credit story has now overshadowed.

The Q3 portfolio review surfaced concentrated but sector-specific stress. If macro conditions deteriorate further, through higher rates, weaker SME cash flows, or increased refinancing failures, the cluster of problem loans could expand. In that scenario, FY2027 guidance requires further downward revision, and the credibility discount on management’s forward statements widens further.

Three monitoring checkpoints, in order of timing:

Two things are now settled. The FY2026 earnings range is materially lower at A$163-169 million, and the management credibility premium that supported Judo’s prior multiple has been removed. Markets will require more evidence before treating forward guidance as reliable.

One thing remains unresolved: whether the credit deterioration is confined to a handful of borrower-specific situations or represents an early warning of widening stress across the broader SME loan book. The 30 June 2026 full-year result and its 90DPD+ ratio will provide the first real answer.

For investors weighing whether today’s price reflects an overreaction or an appropriate re-rating, the current evidence does not support a verdict either way. What it does support is a clearer set of questions and a specific data point to wait for, which is more useful than a conclusion the numbers cannot yet justify.

For investors wanting a structured framework for assessing whether Thursday’s guidance failure is a one-off or a pattern, our dedicated guide to evaluating small-cap management walks through per-share return analysis, transparency red flags, and the specific signals that distinguish compounders from value destroyers, including how to interpret surprise capital raises and guidance revisions as data points rather than isolated events.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Judo Capital shares collapsed after the company cut its FY2026 profit before tax guidance to A$163-169 million, down from A$180-190 million reaffirmed just weeks earlier in April 2026, with a cost of risk of A$116-122 million driving almost the entire gap between old and new guidance.

Cost of risk is the total provisioning expense a bank absorbs to cover expected loan losses in a given year; for Judo Capital, the FY2026 cost of risk of A$116-122 million is the primary driver of its profit downgrade and represents the credit deterioration now under close investor scrutiny.

Management has issued FY2027 PBT guidance of A$210-220 million, implying approximately 30% growth over the revised FY2026 base, though after the June credibility event investors should treat this as a conditional target dependent on the 90-day-past-due ratio stabilising at around 3% and new arrears formation slowing.

Judo Capital's 90DPD+ ratio is guided to reach approximately 3% of gross loans at June 2026, compared to well below 1% at the major banks; this difference reflects the structurally higher credit risk of SME-only lending versus the big four's mortgage-heavy portfolios, not a direct sign of three times worse credit quality.

The three key checkpoints are: whether the 90DPD+ ratio lands at approximately 3% at the 30 June 2026 full-year result, whether new arrears formation slows in H1 FY2027, and whether the collective provision macro overlay remains stable rather than expanding to signal broader SME stress.