Judo Capital Holdings (ASX: JDO) grew its gross loan book 3% in a single quarter to AU$13.8 billion, pushed its deposit base to a record AU$11.5 billion, and reported a net interest margin of 3.15%, more than 120 basis points above regional bank peers. Yet the stock has lost roughly 3% over the past 12 months while the ASX 200 gained approximately 6.1%.

The SME challenger bank presented its Q3 FY26 performance update at the Macquarie Australia Conference on 6 May 2026, giving investors a detailed read on lending momentum, funding costs, credit quality, and capital adequacy heading into the final quarter of the financial year. The combination of record deposits, NIM expansion from the first-half figure of 3.03%, and a reaffirmed pre-tax profit (PBT) guidance range of AU$180-190 million makes this one of the more substantive quarterly data releases in the specialist SME lending space.

What follows works through what the Q3 numbers actually show, how Judo’s margin and capital position compare to ASX peers, what the RBA rate environment means for the investment case, and whether the current AU$1.43 share price reflects the operational momentum on display.

The Q3 numbers that matter and what they signal

The headline metrics tell a story in sequence. Start with scale: gross loans reached AU$13.8 billion as at March 2026, up from AU$12.9 billion at December 2025, approximately 3% quarter-on-quarter growth. Then profitability quality: NIM expanded to 3.15% in Q3 FY26, up from 3.03% reported at the half-year. Then retention: customer attrition fell to an annualised 15% in Q3, down from prior periods.

- Gross loans: AU$13.8 billion (up approximately 7% quarter-on-quarter)

- NIM: 3.15% in Q3, up from 3.03% at 1H FY26

- Active deal pipeline: AU$2.2 billion at an average margin of 4.3%

- Customer attrition: annualised 15%, declining from prior quarters

The NIM expansion is worth isolating. Moving from 3.03% to 3.15% while simultaneously growing the book suggests pricing discipline rather than a passive rate tailwind. The pipeline figure provides a forward anchor the quarterly snapshot alone cannot.

Forward pipeline: AU$2.2 billion in active deals at an average margin of 4.3%, implying the margin trajectory has room to sustain rather than revert.

When big ASX news breaks, our subscribers know first

How Judo’s deposit record changes the funding equation

A record AU$11.5 billion in deposits is the headline achievement. More telling is the composition underneath it: a deposit-to-loan ratio of approximately 83%, which positions Judo among the most self-funded specialist lenders on the ASX.

The deposit cost story is where the structural advantage sharpens. Judo’s deposit pricing sits approximately 74 basis points below the one-month BBSW benchmark, compared with a peer average of approximately 120 basis points. That differential feeds directly into the NIM expansion discussed above.

Deposit cost advantage: approximately 74 basis points below the one-month BBSW, versus a peer average of approximately 120 basis points.

What the Direct Online Savings Account adds to the mix

Launched in February 2026, Judo’s Direct Online Savings Account introduced an at-call product competing with major bank digital savings offerings. Within roughly six weeks, at-call balances surpassed AU$1.1 billion, a pace of deposit gathering that signals strong retail and SME depositor demand.

At-call deposits carry lower structural costs than term deposits. A growing at-call base gives Judo more flexibility to manage overall funding costs regardless of where the RBA moves next, a point that matters more given the shifting rate outlook covered below.

Wholesale funding cost repricing is the structural headwind that most directly connects the regional bank peer group to Judo’s situation: Bendigo Bank’s Q3 FY26 NIM of 1.98% faces exactly the same mechanism Judo manages through its deposit pricing advantage, with term deposit books locked below current market rates eventually rolling onto higher funding costs.

Understanding Judo’s SME banking model (and why NIM alone does not tell the whole story)

Judo operates as a pure-play SME challenger bank, originating secured business loans typically between AU$250,000 and AU$15 million. This is a segment the major banks have systematically underserved through relationship-light models, and Judo’s concentration in that space is the structural reason its NIM sits so far above peers, not a one-off cyclical benefit.

Approximately 85% of Judo’s loan book is variable rate. That structure means the bank’s NIM responds more directly to the RBA cash rate (currently 4.10% as of the 18 March 2026 change) than a mixed residential mortgage portfolio would. The trade-off is concentrated SME exposure: the elevated margin comes with elevated credit risk, which is precisely why the provisioning data in the next section matters.

Specialist lender NIM expansion is not a Judo-specific phenomenon in the current cycle: Heartland Group reported group average NIM of 4.06% in Q3 FY26, up from 3.89% in Q1, driven by Australian operations after the early repayment of a medium-term note, suggesting the structural advantages of focused-segment lenders over diversified bank portfolios are showing up broadly across ASX-listed challengers.

| Metric | Judo (JDO) | Bendigo & Adelaide (BEN) | Bank of Queensland (BOQ) |

|---|---|---|---|

| NIM | 3.15% | ~1.92% | ~1.88% |

| CET1 Ratio | 12.6% | ~11.2% | ~11.18% |

| Gross Loans | AU$13.8B | ~AU$10B (SME) | AU$18B (total) |

| Deposit Cost vs. 1M BBSW | ~74 bps below | ~120 bps below | ~120 bps below |

Readers who understand why Judo’s NIM is structurally elevated, rather than cyclically inflated, are better positioned to judge whether the current share price fairly values that advantage or discounts it because of credit quality concerns.

Credit quality and provisioning: the risk the bulls are watching

The impaired loan ratio of 2.65% of gross loans as at March 2026 is elevated relative to the major banks. For a concentrated SME lender operating during a period of macro uncertainty, the figure is consistent with the business model, but it is not one that can be dismissed.

- Impaired loans: 2.65% of gross loans

- Collective provisioning: 94 basis points of gross loans

- Cost of risk guidance: 70-75 basis points of average loans for FY26

- Sector concentrations: fuel price-sensitive and adverse economic condition-exposed industries

Judo conducted a portfolio review at the individual client level in response to geopolitical and macroeconomic conditions, and collective provisioning rose to 94 basis points of gross loans. Management’s own cost of risk tolerance band sits at 70-75 basis points of average loans for FY26.

The FY26 guidance reaffirmation on 23 April 2026 carried a qualification that mattered: management signalled the result would trend toward the lower end of the AU$180-190 million range, a distinction the market treated as a material earnings revision rather than a minor calibration.

The figure to watch: collective provisioning at 94 basis points of gross loans, the metric distinguishing the bear and bull camps on JDO.

The gap between 94 basis points of provisioning and 70-75 basis points of guided cost of risk tells investors something about the buffer Judo is building. Whether that buffer proves conservative or insufficient depends on how the SME cycle unfolds through the second half of FY26.

What the RBA rate environment means for Judo’s margin trajectory

Many investors carry the intuition that rate moves are a simple headwind or tailwind. For Judo specifically, the reality is two-sided.

The RBA cut the cash rate to 4.10% on 18 March 2026. Institutional forecasts, including from Westpac, now project a potential rise toward 4.85% by August 2026, reversing the rate-cut narrative that had shaped earlier JDO commentary.

Westpac forecast: potential cash rate rise to 4.85% by August 2026.

The dynamic runs through three channels:

- NIM support: Judo’s approximately 85% variable-rate book means any rate increase flows through to margin relatively quickly. Management has guided that NIM will finish FY26 at the upper boundary of the 3.00-3.10% target range; Q3’s 3.15% already sits above that guided band.

- Borrower stress: Higher rates increase debt service costs for SME borrowers, which could push the impaired loan ratio higher through the second half of FY26.

- Net guidance implication: FY26 PBT guidance of AU$180-190 million remains intact, though analysts note risks toward the lower end if provisioning costs accelerate.

The rate environment is not a simple positive for JDO at current levels. Holding both sides of this dynamic simultaneously is necessary to assess whether full-year guidance is more likely to be beaten or missed.

Valuation gap or value trap: what the share price is telling investors

The operational story and the share price story are not in agreement. Record deposits, NIM expansion, and reaffirmed guidance all point in one direction. A 3% decline over 12 months, a price-to-book ratio of approximately 0.9x, and underperformance against the ASX 200 point in another.

The April selloff mechanics reveal something important about how the market is pricing JDO: the 20% single-day drop from approximately AU$1.75 to AU$1.40 occurred despite guidance being reaffirmed, which means the market was reacting to the lower-end signal and the provision build rather than any outright guidance cut.

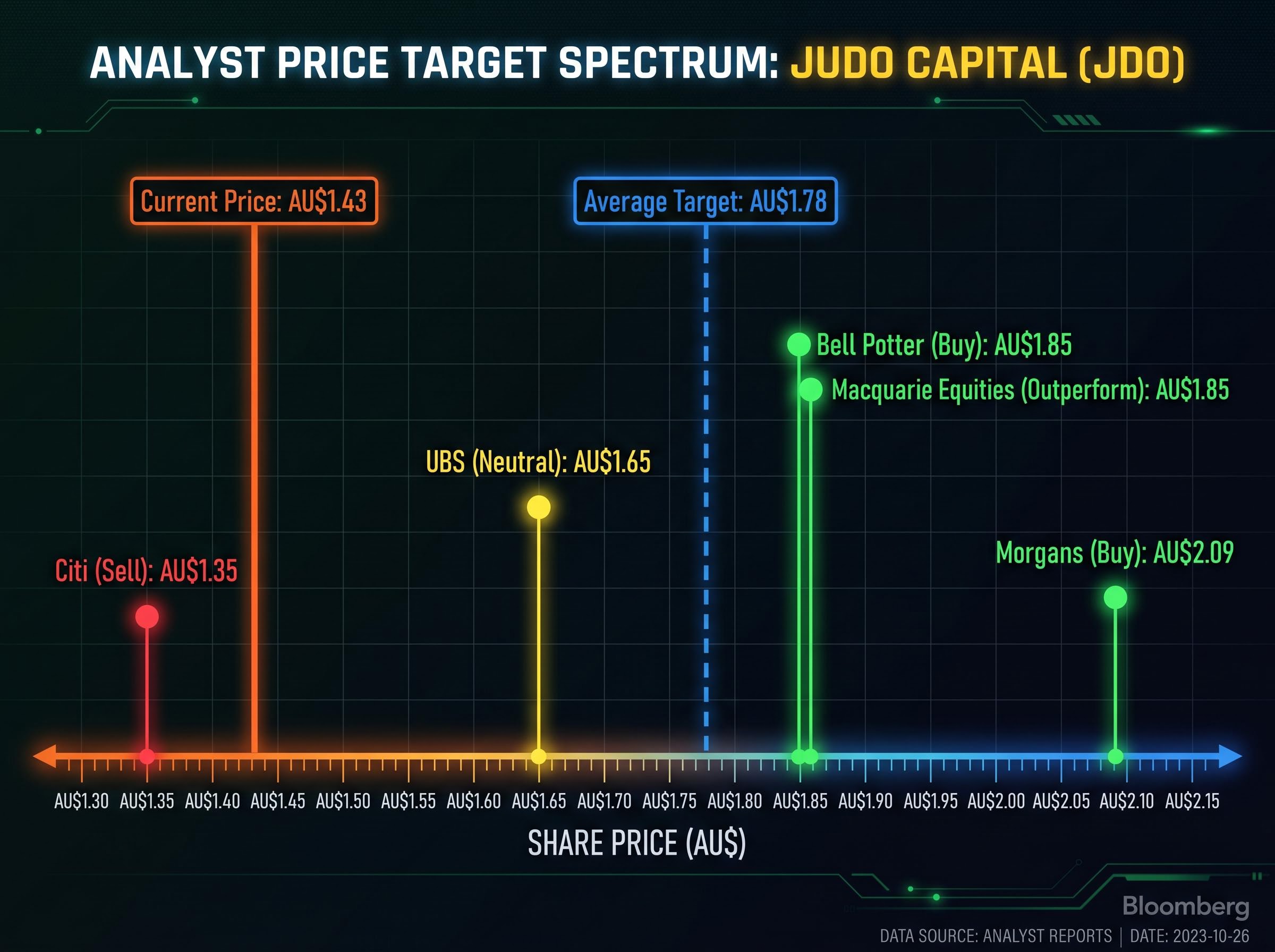

At AU$1.43, Judo Capital trades at a discount to an average analyst price target of approximately AU$1.78, implying roughly 24% upside. FY26 PBT guidance of AU$180-190 million at approximately AU$0.13 consensus earnings per share implies a forward price-to-earnings ratio of approximately 10x.

| Firm | Rating | Price Target | Key Thesis |

|---|---|---|---|

| Macquarie Equities | Outperform | AU$1.85 | Q3 beat on NIM and loan growth; CET1 supports dividends |

| Morgans | Buy (upgraded late April 2026) | AU$2.09 | Most bullish institutional view; upgraded on operational momentum |

| Bell Potter | Buy | AU$1.85 | NIM trajectory to 3.2%+ by FY27; cost-income ratio improving |

| UBS | Neutral | AU$1.65 | Stable asset quality positive; macro headwinds remain |

| Citi | Sell | AU$1.35 | ROE of approximately 8% lags peers; provision build erodes confidence |

The bull case:

- NIM of 3.15% is a competitive differentiator, more than 120 basis points above regional peers

- CET1 at 12.6% is the strongest among comparable ASX lenders

- Price-to-book of 0.9x suggests the market is undervaluing the franchise

- Morgans upgraded to Buy at AU$2.09 in late April 2026

APRA’s capital adequacy standards for ADIs set a minimum CET1 requirement of 4.5% of risk-weighted assets for authorised deposit-taking institutions, with an additional capital conservation buffer of 2.5%, meaning Judo’s 12.6% CET1 ratio sits well above the regulatory floor and provides meaningful headroom for balance sheet expansion or capital returns.

The bear case:

- Return on equity of approximately 8% lags regional bank peers, per Citi’s analysis

- Provision build to 94 basis points signals management caution on credit quality

- SME cycle risk could compress earnings if macro conditions deteriorate

- Citi maintains a Sell rating at AU$1.35, below the current price

The 52-week range of AU$1.31-AU$2.07 captures the breadth of the market’s indecision. At approximately AU$1.62 billion in market capitalisation, whether Judo represents a valuation gap or a value trap depends on a variable neither bulls nor bears can yet resolve: the credit quality trajectory through the second half.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Momentum is real, but the second half will decide the investment case

Loan growth, NIM expansion, record deposits, and CET1 strength all point in the same direction, and the Q3 update gave the bulls more to work with than the bears. The operational case is the strongest it has been since Judo’s listing.

The single most important variable for the remainder of FY26 is whether impaired loans and provisioning stabilise or accelerate. That is the factor most likely to push PBT toward the lower or upper end of the AU$180-190 million guidance range.

The 6 May 2026 Macquarie Australia Conference presentation will add management commentary that either reinforces or qualifies the operational optimism embedded in the Q3 data. From there, the forthcoming FY26 full-year result will deliver the credit quality figures that resolve the valuation gap question. Those two data points are the ones worth watching.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.