Micron Surges 12% After Record Earnings and $50B Guidance

2 hrs ago

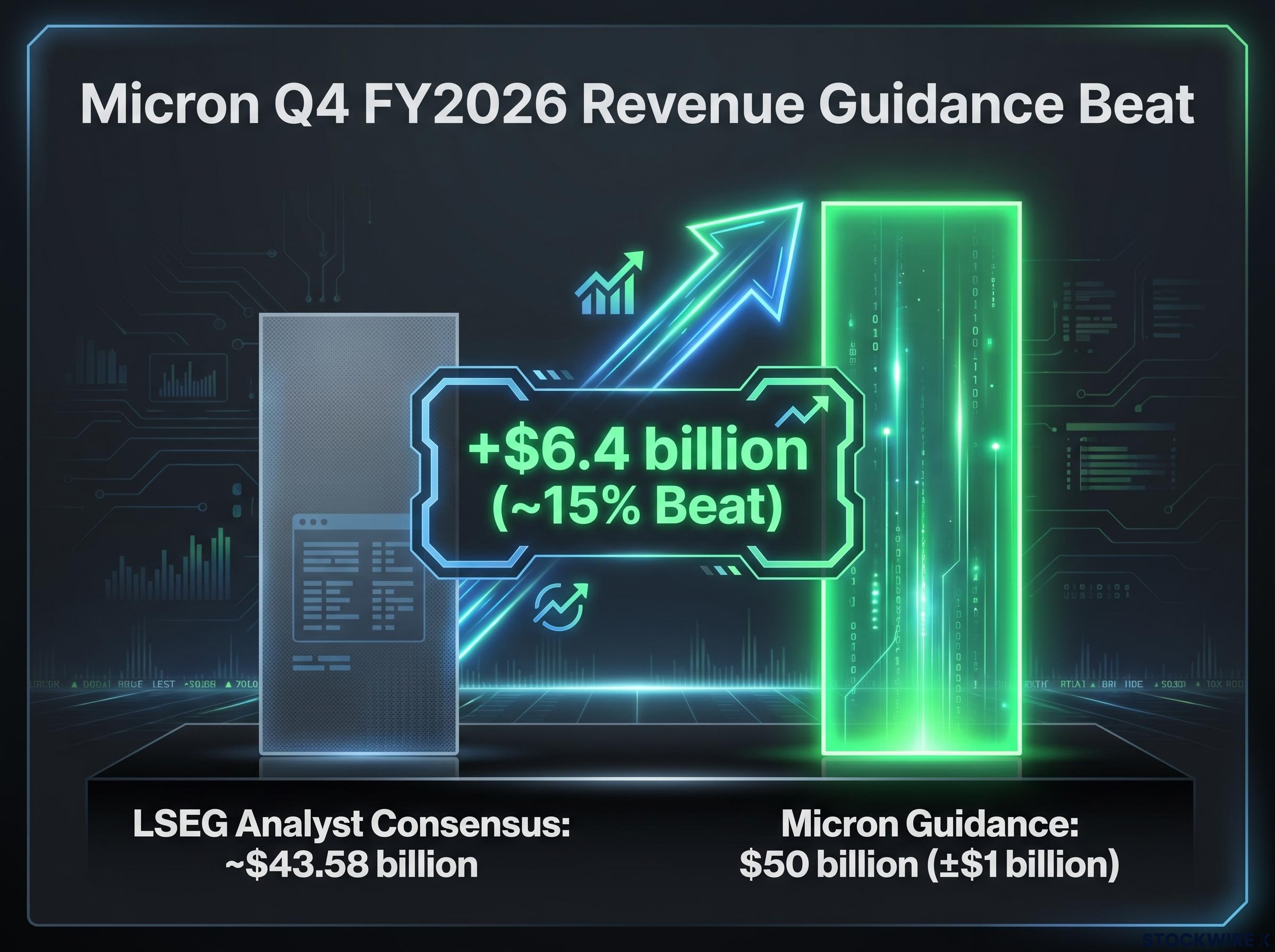

Micron just guided Q4 FY2026 revenue to $50 billion, roughly $6.4 billion above the Wall Street consensus compiled by LSEG, and shares surged approximately 9.47% in after-hours trading on 24 June 2026.

A 15% guidance beat at this revenue scale is not quarterly noise. For a mature semiconductor company, a miss of that magnitude would trigger an analyst scramble; a beat of that magnitude signals something structural is driving demand faster than the professional forecasting apparatus can keep up.

Here is what that guidance tells you about AI memory demand, what it changes about how to evaluate Micron as an investment, and why the consensus gap matters well beyond a single stock.

For Q4 FY2026, Micron set its revenue target at $50 billion, with a tolerance of plus or minus $1 billion. According to data compiled by LSEG, the average analyst estimate stood at roughly $43.58 billion. The gap between those two numbers is roughly $6.4 billion, or about 15% above what Wall Street expected.

Micron’s official Q3 FY2026 earnings release confirms the Q4 FY2026 revenue guidance of $50.0 billion, plus or minus $1.0 billion, providing the primary source figures underlying the consensus gap analysis in this article.

| Metric | Figure |

|---|---|

| Micron Q4 FY2026 guidance | $50 billion (±$1 billion) |

| LSEG analyst consensus | ~$43.58 billion |

| Absolute beat | ~$6.4 billion |

| Percentage beat | ~15% |

A 15% guidance beat at this scale is not a rounding error. It tells you the demand environment shifted faster and more decisively than the professional forecasting apparatus had priced in.

Put differently, $6.4 billion is larger than the total quarterly revenue of most semiconductor companies. When a company at Micron’s maturity posts a gap that size against a consensus compiled from dozens of institutional models, it means the models themselves are missing something structural, not just running conservative.

The stock told the same story the numbers did, only faster.

The contrast matters. Micron drifted slightly lower through the regular session on 24 June, giving no signal of what was coming. The guidance dropped after the close, and within minutes the stock repriced by nearly 10%.

A move of that magnitude on a stock already trading above $1,000 is not retail enthusiasm. It is institutional investors recalculating forward earnings in real time and deciding the prior models were too low. The speed of the repricing tells you a meaningful portion of the upside surprise is already embedded in the price before the next regular session open, which changes the calculus for anyone considering entering now.

The guidance beat did not appear in a vacuum. It sits on top of a specific demand mechanism that is worth understanding clearly, because it is the reason Micron’s revenue trajectory has diverged from traditional memory cycles.

AI data centres and large language models (LLMs, the technology behind tools like ChatGPT) require two types of memory at volumes and specifications that standard products do not meet:

Each generation of larger AI models requires more memory per chip, per server, and per inference cycle. That creates demand that compounds rather than mean-reverts: the next model is always bigger than the last, and the infrastructure to run it always needs more memory.

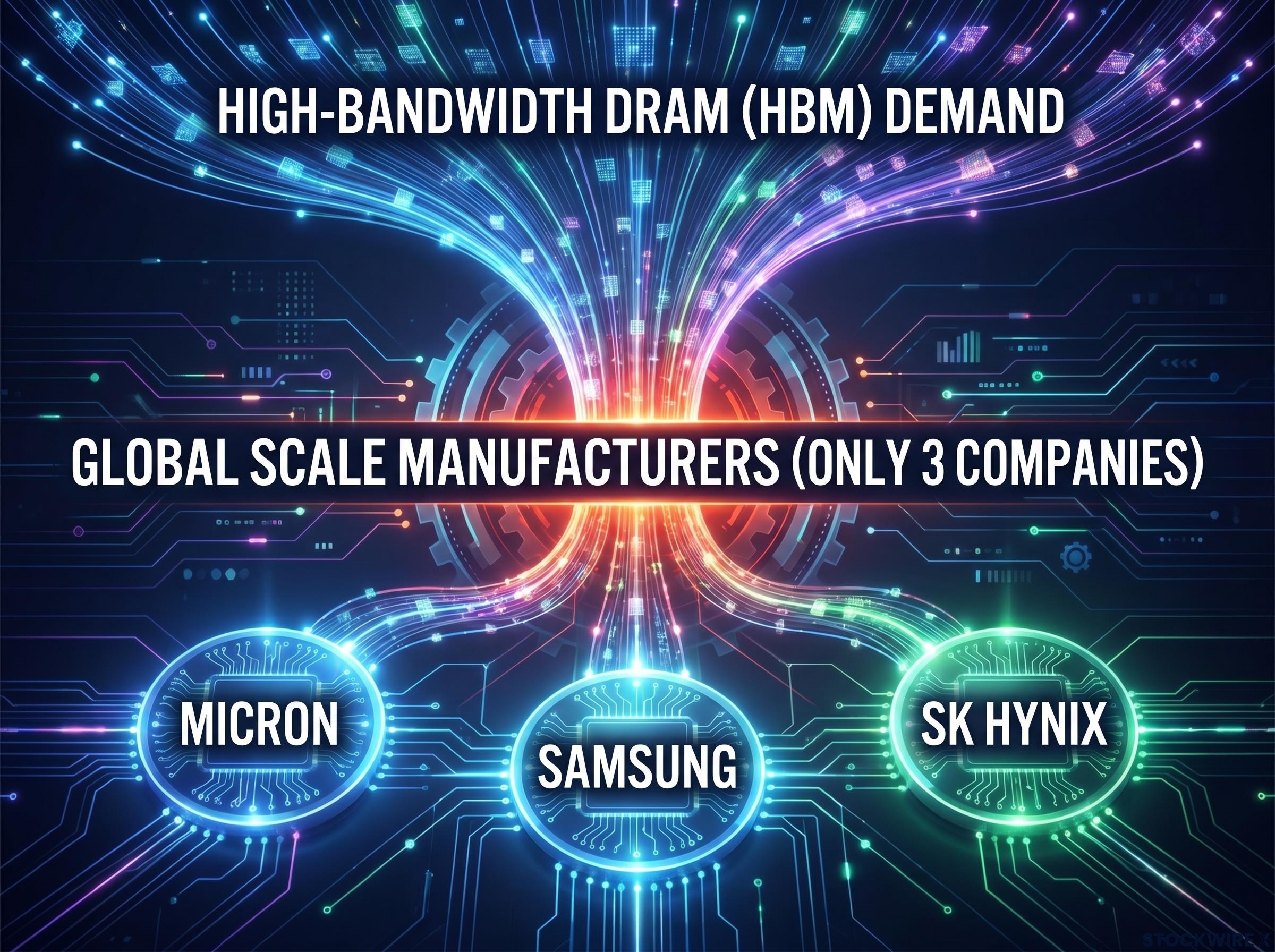

The global DRAM shortage underpinning that demand surge is structural rather than cyclical: SK Hynix projects supply tightness through 2030, HBM inventory sits at just 3-4 weeks industry-wide, and all three major producers were fully sold out through 2026 even before Micron’s latest guidance revision.

Only three companies globally can manufacture HBM at scale: Micron, Samsung, and SK Hynix. That supply concentration is the leverage point. When AI capital expenditure accelerates, the memory demand concentrates in three pairs of hands, and pricing power follows.

HBM4 supply qualification for Nvidia’s next-generation Vera Rubin platform illustrates the competitive dynamics within that three-player bottleneck: SK Hynix holds an estimated 60-70% of initial volume allocations, Samsung secured a secondary position, and Micron, while holding the smallest share, secured a supplier foothold that positions it to compete for larger allocations in future platform generations.

Micron’s Q4 guidance reflects exactly that dynamic. The $6.4 billion consensus gap is not routine forecasting variance; it reflects systematic underestimation of how much memory AI workloads actually consume. For you as an investor, the question is whether this demand is a multi-year structural tailwind or a pull-forward of future orders, and Micron’s guidance argues directly for the former.

The 15% beat was not the first time consensus missed the mark on AI memory demand. It fits a pattern, and the pattern has structural causes that are worth naming, because they explain why this is likely to keep happening.

The models are not just conservatively positioned. They are structurally lagging a demand environment that has moved faster than their frameworks can accommodate.

That matters for you because it suggests further positive surprises are more probable than negative ones until the sell-side recalibrates its assumptions. Understanding this pattern separates informed optimism from blind momentum-chasing.

For existing Micron shareholders, the guidance validates the AI infrastructure thesis that presumably anchored the original position. Earnings trajectory is tracking above prior market expectations, and the structural demand drivers described above remain intact.

The structural compounder rerating argument gained institutional traction in late May 2026 when UBS tripled its Micron price target to $1,625, citing multi-year supply contracts and agentic AI workloads that run continuously rather than episodically as the basis for applying a growth multiple rather than the trough-adjusted commodity multiple that memory stocks have historically received.

The decision is different if you are not yet in the stock.

The near-10% after-hours move has already embedded a portion of the positive surprise into the price. At approximately $1,147.77, you are not buying at the pre-announcement level. The entry decision now turns on two specific questions:

Against those questions, three risk factors require honest weighting:

The guidance beat is good news for the bull case on MU, but the price has moved and the question is no longer whether Micron is benefiting from AI demand. It is whether that benefit is already fully priced.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Micron’s Q4 FY2026 guidance, $50 billion against a $43.58 billion consensus, is a data point about the entire AI infrastructure spending cycle, not just one company’s execution. A $6.4 billion gap is large enough to represent structural signal, not statistical noise.

The $6.4 billion consensus miss is not a one-company story. It suggests AI infrastructure spending is exceeding legacy models across the memory segment.

That implies other memory-adjacent suppliers and AI infrastructure component makers may also be underrepresented in current sell-side models. For the next earnings cycle, three variables will determine whether this guidance beat marks the beginning of a broader model recalibration or a peak surprise:

The semiconductor supercycle debate extends well beyond Micron: the PHLX Semiconductor Index added approximately $3.8 trillion in market value over six weeks through May 2026, with Intel reaching a 26-year high and Sandisk surging 492%, raising the same structural-versus-speculative question that Micron’s own guidance forces investors to confront.

One note on the data itself: research sourcing contains a conflict on the fiscal quarter designation (Q4 per Reuters/LSEG versus Q3 per unverified sources) for the same 24 June 2026 release. The figures cited throughout this article use the pre-verified Reuters/LSEG sourcing. Verify the fiscal quarter designation through Micron’s investor relations filings before acting on any specific figures.

High-bandwidth memory (HBM) is specialised DRAM that feeds data to AI processors fast enough to support training and inference workloads; because only three companies globally can manufacture it at scale, including Micron, concentrated supply gives producers significant pricing power as AI infrastructure spending accelerates.

The gap reflects structural underestimation of AI memory demand: hyperscalers lock in long-term capacity commitments months before they appear in guidance, and sell-side models built on traditional memory-cycle mean-reversion assumptions consistently fail to capture the compounding volume requirements of successive AI model generations.

Micron shares surged approximately 9.47% in after-hours trading on 24 June 2026, rising from a regular session close of $1,047.20 to roughly $1,147.77, a gain of around $100 per share.

Three risks require honest weighting: memory industry cyclicality that elevated AI demand has moderated but not eliminated, competitive pressure from Samsung and SK Hynix in DRAM and HBM markets, and valuation risk on a stock near $1,150 after a large AI-driven run if the demand narrative stumbles or semiconductor multiples compress.

A $6.4 billion consensus gap at Micron's scale is large enough to represent a structural signal about the broader AI infrastructure spending cycle, suggesting other memory-adjacent suppliers and AI infrastructure component makers may also be underrepresented in current sell-side models heading into the next earnings season.