Why AI Is Splitting Semiconductor Stocks From the Rest of Tech

2 hrs ago

Sixty-two of Australia’s actively managed equity funds have quietly built one of the most lopsided sector bets in years, and it is not where most retail investors are looking. Morgan Stanley’s June 2026 research note maps the stock and sector positioning of every fund in the tracked cohort, and the picture that emerges is striking: professional conviction is concentrated in a handful of structural themes, while a remarkably wide consensus is betting against some of the ASX 200’s most heavily weighted names.

What follows maps exactly where that professional money is sitting, where it has moved over the past six months, and what the positioning shifts signal about how fund managers are reading the macro environment into the second half of 2026. The positioning data gives you a clear framework for stress-testing your own portfolio exposures against the current professional consensus.

Healthcare and Consumer Staples remain the two largest above-benchmark sector allocations across the 62 funds. That sounds straightforward. The direction of travel complicates it.

CSL occupies an unusual position in this dataset: it carries the broadest and deepest individual overweight across all funds tracked, yet it also saw the sharpest single-stock active weight cut recorded in May 2026. That is not a contradiction. It is profit-taking and de-risking from a very large position, not a wholesale exit.

ResMed tells a sharper version of the same story.

ResMed’s active weight has been wound back to roughly half the position size managers held six months earlier, placing it among the most significantly reduced Healthcare names over that period.

The current positioning status across the key Healthcare and Staples names:

Consumer Staples is the second-largest above-benchmark sector, and unlike Healthcare, conviction here is stable rather than being trimmed. Most funds sit above benchmark. The preference for Coles over Woolworths as the primary Staples expression reflects an earnings resilience and dividend quality call. Metcash appearing among the five largest May 2026 additions reinforces the defensive tilt rather than signalling a new theme.

What this combination tells you: professionals still want defensive quality exposure, but they see meaningfully less upside in CSL and ResMed than they did six to twelve months ago. If you are currently building or holding concentrated positions in either name, the direction of professional conviction, not just its current level, is a relevant signal.

For years, Industrials was a sector that active managers structurally underweighted. Not slightly. Consistently. The sector sat below benchmark as a default setting across the full history of the 62-fund dataset.

That has now completely reversed. Industrials is the only sector across the dataset’s full history to have moved from a persistent underweight to a clear overweight position, and it has attracted greater active weight accumulation than any other sector in recent months.

Three thematic pillars are driving the accumulation:

Ventia and Orica were among the five largest active weight additions in May 2026, and both sit squarely within those themes.

| Sector | Previous positioning | Current positioning | Key names | Primary thesis |

|---|---|---|---|---|

| Industrials | Structural underweight | Clear overweight (historic first) | Ventia, Orica | Infrastructure, defence, capex services |

| Healthcare | Large overweight | Still overweight, being trimmed | CSL, ResMed | Quality defensives, but less upside seen |

| Energy | Overweight (Woodside-led) | Overweight (Santos-led rotation) | Santos, Woodside | Relative-value call on project mix |

When professional money builds a position this methodically across an entire sector it historically ignored, it typically reflects conviction about a multi-year earnings cycle rather than a near-term price catalyst. For investors seeking sectors where professional conviction is still growing rather than being trimmed, Industrials is the clearest current signal.

ASX Industrials valuation is the natural next question once the positioning case is established: the sector has returned 6.1% annualised over five years against the broader ASX 200’s 4.2%, and the infrastructure pipeline underpinning that performance sits at $242 billion across FY2024-25 to FY2028-29 according to Infrastructure Australia’s 2025 Market Capacity Report.

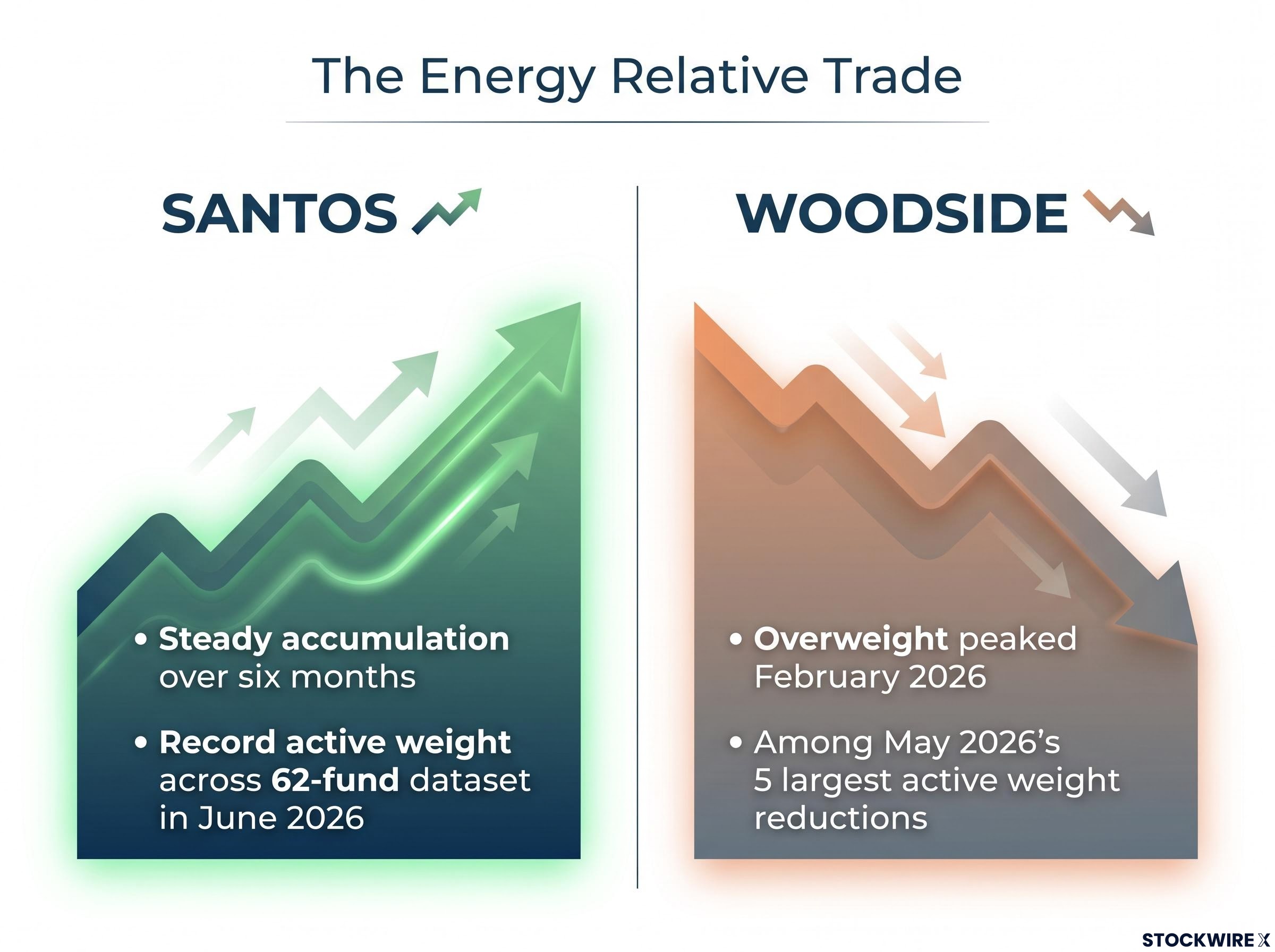

The Energy positioning story is not a sector call. It is a relative trade playing out between two names.

Santos has climbed to a record active weight across the 62-fund dataset as captured in the June 2026 note, establishing it as the dominant active Energy expression for the cohort.

The other side of that trade is Woodside. Woodside’s overweight peaked in February 2026 and has since been cut. It appeared among the five largest active weight reductions in May 2026.

The positioning trajectories tell the story clearly:

This is a relative-value and project-mix call, not a broad Energy sector exit. Managers still want Energy exposure. They want it through Santos rather than Woodside at current prices. For investors holding Woodside as their default large-cap Energy position, the professional consensus has moved decisively, and that reflects a considered view on relative upside rather than a sector-wide bearish stance.

Active weight is the measure that makes all the positioning data in this analysis meaningful. It is the difference between a fund’s holding in a stock or sector and that stock or sector’s weight in the benchmark index, expressed in percentage points. It captures what a manager is deliberately choosing to do, not just what they happen to own.

ASIC’s portfolio disclosure rules for active funds, set out in Regulatory Guide 282, determine the frequency and completeness of holdings data that actively managed products must publish, which shapes how quickly positioning shifts like those tracked in the Morgan Stanley cohort become visible to the broader market.

Worked example: If CBA represents 9% of the ASX 200 but a fund holds only 3%, the fund’s active weight in CBA is negative 6 percentage points. That is a deliberate, significant bet against the stock.

This distinction matters because not every addition is bullish. In May 2026, both CBA and Westpac appeared among the five largest active weight additions. That sounds like managers were buying the banks. They were not.

Once you understand this distinction, you can correctly interpret the CBA and Westpac additions as passive maintenance rather than a change in view. That prevents a common misreading of fund flow data, and it makes the rest of this analysis genuinely interpretable rather than just descriptive.

ASX sector rotation in June 2026 provides a real-time corroboration of the positioning signals in this dataset: on 2 June 2026, the ASX 200 Information Technology sub-index gained 4.71% in a single session as fund managers closed underweight positions in globally exposed names, a move that is consistent with the same rebalancing mechanics that produced the CBA and Westpac additions flagged in the active weight data.

The underweight picture is not a collection of mild preferences. These are deliberately held, large negative bets.

Financials is the largest sector underweight by a significant margin. Around 87% of the 62 funds are positioned below benchmark in the sector, producing an average active weight of negative 8.0 percentage points.

At the centre of that call sits one stock.

Commonwealth Bank sits at the top of the underweight rankings by a substantial margin, with the scale of funds’ short position running at roughly four times the size of the next most underweight name. The primary argument is valuation: CBA’s index weight and price-to-earnings premium to global banking peers are widely viewed as not justified by fundamentals.

CBA’s valuation premium is not simply a matter of analyst opinion: at roughly 28x trailing earnings, CBA sits approximately 73% above its Big Four peer average, a gap that compulsory superannuation inflows and ASX 200 index weighting mechanics help sustain regardless of whether that premium is justified by fundamentals.

Not every major bank sits in the same position. Over the past year, ANZ has shifted from an underweight to an overweight, becoming the sole major bank where the cohort sits above benchmark. Westpac and NAB remain below. The ANZ exception is a meaningful intra-sector signal: managers are not anti-bank in principle, they are anti-CBA-valuation specifically.

Materials is underweight overall, but the positioning is a relative call rather than an outright sector exit. Within large-cap diversified mining, funds have moved away from BHP in favour of Rio Tinto as the preferred holding.

Real Estate is broadly unloved: fewer than one quarter of funds hold the sector above benchmark. Higher rates, funding costs, and uncertainty around commercial property valuations are keeping more than three-quarters of managers below benchmark heading into the second half of 2026.

| Sector | Funds below benchmark | Average active weight | Key stocks | Primary rationale |

|---|---|---|---|---|

| Financials | ~87% | −8.0 percentage points | CBA (largest underweight), Westpac, NAB below; ANZ above | CBA valuation premium; index weight seen as stretched |

| Materials | Majority | Below benchmark | BHP underweight, Rio Tinto preferred | Relative-value call within diversified miners |

| Real Estate | ~78% | Below benchmark | Broad sector underweight | Higher rates, commercial property uncertainty |

The breadth and depth of the CBA underweight represents the single largest active consensus call in the Australian market. For any investor with significant CBA exposure, understanding the professional reasoning around valuation stretch is directly relevant to your next portfolio review, even if you ultimately disagree with the conclusion.

This is not a buy or sell list. Positioning data reflects professional views as of mid-2026 and does not replace individual valuation work or risk assessment. What it does provide is a structured set of questions worth asking.

Key positioning calls for quick reference:

Source: Morgan Stanley research, June 2026, 62 active funds.

For investors wanting to move from identifying the positioning signals to systematically adjusting their own exposure, our dedicated guide to beta-weighted position sizing covers the step-by-step process of converting dollar allocations into market-risk-equivalent weights, including a worked rebalancing workflow that applies directly to the kind of sector concentration decisions this positioning data raises.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Not all positioning shifts carry the same weight. Some reflect structural commitment. Others are tactical trims that could reverse next quarter. Separating the two gives you a more durable frame for using this data.

Building momentum:

Trimming momentum:

The next inflection points to watch are the direction of CBA’s index weight, which mechanically influences how large the underweight grows, and whether Industrials earnings delivery matches the expectations that have driven the historic positioning shift.

This data is a mid-2026 snapshot from 62 actively managed funds, sourced from Morgan Stanley research. Positioning shifts continuously. The value is in understanding the current professional consensus and its direction, not in treating it as a static blueprint. Structural momentum in Industrials and Santos signals a multi-year professional commitment, and that has different implications for your portfolio positioning than a tactical month-to-month trade.

These statements reflect positioning data and professional fund manager views as of mid-2026. Past positioning does not guarantee future returns. Financial projections and forward-looking assessments are subject to market conditions and various risk factors.

—

Active weight is the difference between a fund's holding in a stock or sector and that stock or sector's weight in the benchmark index, expressed in percentage points. A negative active weight means the fund is deliberately holding less than the index, which is a bet against that stock or sector.

According to Morgan Stanley's June 2026 research covering 62 active funds, Industrials is the sector attracting the most accumulation, having flipped from a persistent structural underweight to a clear overweight for the first time in the dataset's history, driven by infrastructure spending, defence supply chains, and capex-cycle services.

The primary argument is valuation: at roughly 28x trailing earnings, CBA sits approximately 73% above its Big Four peer average, a premium that around 87% of the 62 tracked funds view as unjustified by fundamentals, producing an average active weight of negative 8.0 percentage points against the stock.

This is a relative-value and project-mix call, not a broad Energy sector exit. Santos has climbed to a record active weight across the 62-fund cohort while Woodside's overweight peaked in February 2026 and has since been cut, appearing among May 2026's largest active weight reductions.

Both remain overweight positions across the cohort, but conviction is being trimmed: CSL recorded the largest single-stock active weight reduction in May 2026, and ResMed's active weight has been wound back to roughly half the position size managers held six months earlier.