ASX 200 Posts Four-Day Run as WiseTech Sheds 18% in One Session

3 hrs ago

Bank of America has abandoned its earlier dovish stance and now forecasts three Federal Reserve rate hikes in 2026, no cuts before 2028, and an inflation trajectory that has decisively moved against the transitory narrative. The call, authored by BofA analyst Aditya Bhave and informed by the June 2026 Federal Reserve Summary of Economic Projections, marks a deliberate hawkish reversal from the bank’s prior scepticism about rate increases. With Fed Chair Kevin Warsh signalling that current policy is not particularly restrictive, and with core PCE running well above the 2% target, the conditions driving this forecast are not hypothetical. What follows is a breakdown of exactly what BofA is now projecting, what the inflation and labour market data show, what the Fed’s own projections reveal, and what the rate path means for bonds, equities, and consumer borrowing.

Until recently, Bank of America had been among the more sceptical voices on the need for further Fed rate increases. That position is now gone. BofA has described its earlier stance as premature and replaced it with one of the more aggressive rate calls on Wall Street.

BofA has characterised its prior scepticism about rate increases as premature, marking a full reversal of its earlier positioning.

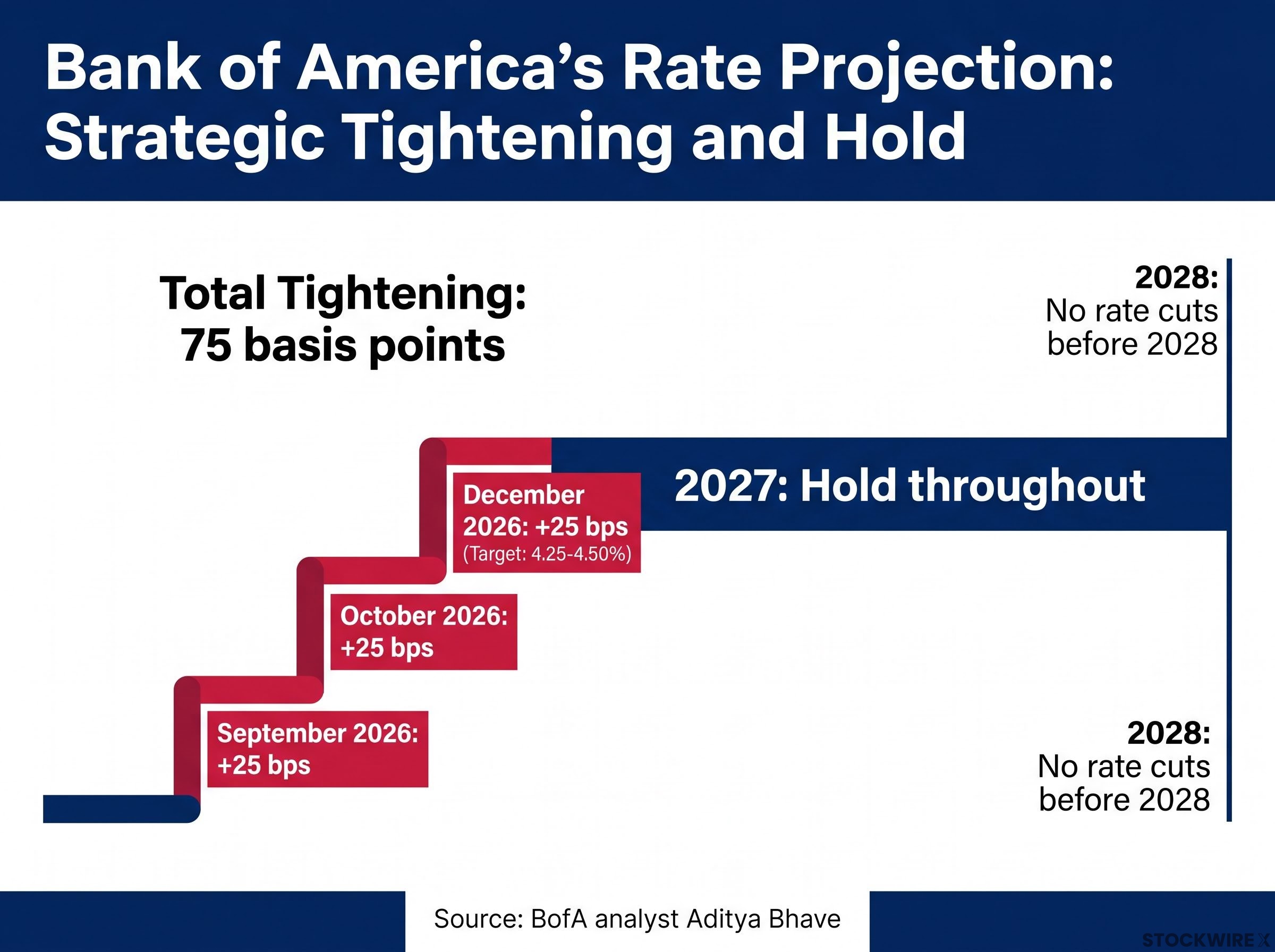

The new forecast from analyst Aditya Bhave projects three 25 basis point hikes before year-end, totalling 75 basis points of tightening. The projected timeline:

After December, BofA expects the Fed to hold throughout all of 2027, with no rate cuts arriving before 2028. This is not a minor recalibration. It is a multi-year policy horizon that resets the baseline for anyone still positioning for near-term rate relief.

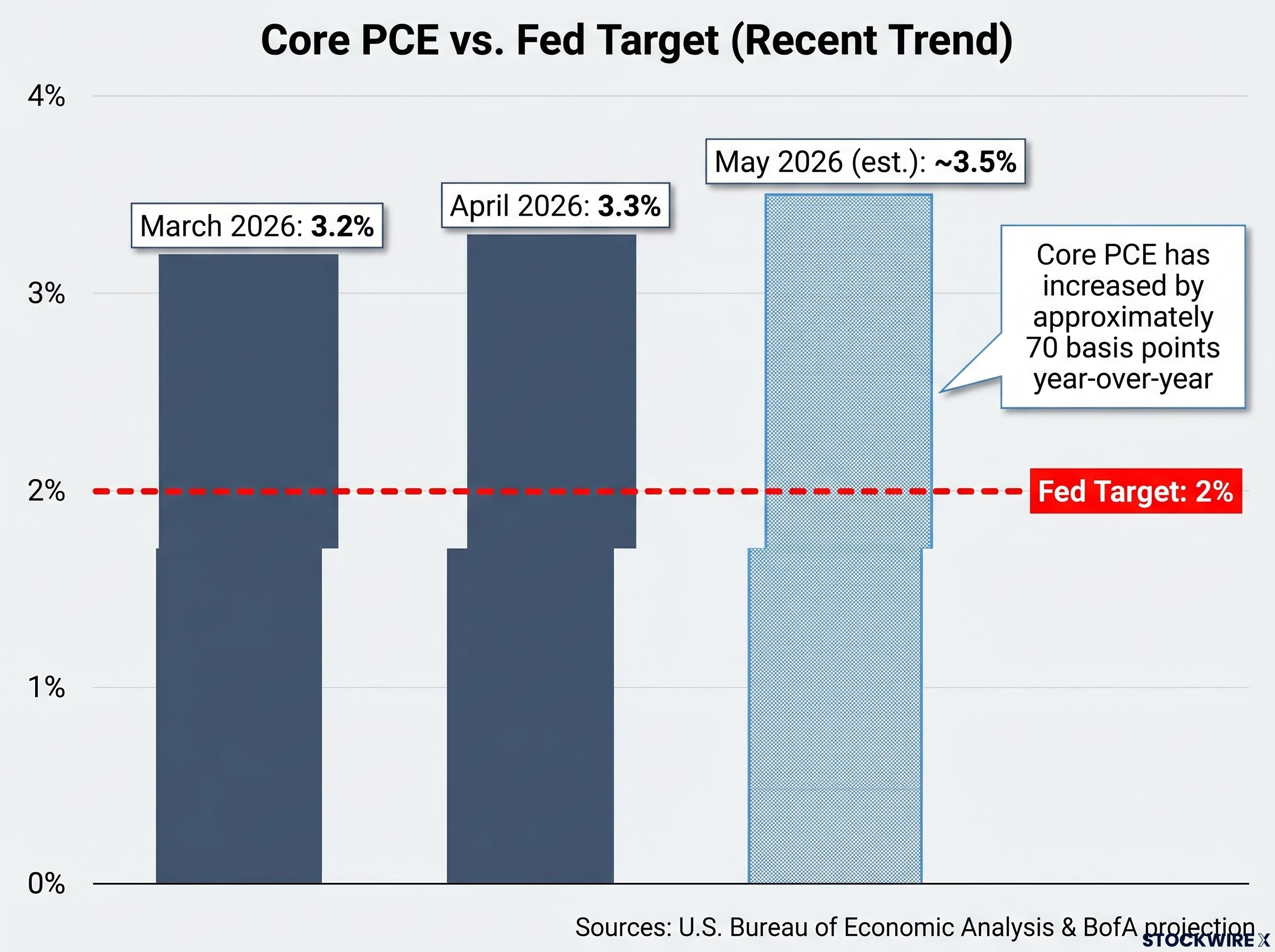

Start with March 2026: core PCE came in at 3.2% year-over-year. Then April 2026: 3.3%, confirmed by the U.S. Bureau of Economic Analysis on May 28, 2026. Now BofA projects May 2026 core PCE could reach approximately 3.5%, with that reading due for release on June 25.

| Period | Core PCE (y/y) | Source |

|---|---|---|

| March 2026 | 3.2% | U.S. Bureau of Economic Analysis |

| April 2026 | 3.3% | U.S. Bureau of Economic Analysis (released May 28, 2026) |

| May 2026 (est.) | ~3.5% | BofA projection (Aditya Bhave) |

The direction is clear. The gap between these readings and the Fed’s 2% target is not narrowing; it is widening.

Core PCE has increased by approximately 70 basis points year-over-year, a trajectory that directly undercuts any remaining transitory framing.

For investors pricing in rate relief, that sequential drift upward is the single most important data point to watch.

The headline CPI divergence in the May 2026 print, where headline inflation reached 4.2% while core held at 2.9%, matters for the PCE trajectory because energy-driven headline pressure can feed second-round effects into services costs over the following two to three quarters, even when initial core readings appear contained.

The conventional brake on Fed tightening has always been the labour market. Raise rates too aggressively and unemployment climbs, creating political and economic pressure to reverse course. That brake appears to have failed.

Bureau of Labor Statistics data released on June 5, 2026 tells the story:

One year ago, rates were 75 basis points higher than current levels. Unemployment has remained essentially flat over that period. The economy absorbed tighter policy without visible job damage.

BofA’s conclusion is direct: downside risks to employment have largely faded. If the labour market is not deteriorating under previous tightening, it no longer functions as a reason to hold off on further hikes. That removes what has historically been the most powerful counterargument to rate increases.

Labour market quality signals complicate the surface-level stability reading: ISM Manufacturing Employment and ISM Services Employment were both in contraction territory simultaneously in April, and involuntary part-time employment surged by 445,000 to 4.9 million, suggesting the headline unemployment rate of 4.3% may be understating the degree of underlying softening.

The June 2026 Summary of Economic Projections revealed that the Fed itself is split, but the split leans hawkish.

The June 2026 Summary of Economic Projections published by the Federal Reserve on June 17 shows that nine of eighteen FOMC participants anticipated at least one further rate hike in 2026, providing the primary data source underpinning BofA’s revised forecast.

That second point is the more striking signal. Half the committee sees further tightening as appropriate even with the labour market holding steady. The Fed’s internal framework for when hikes are warranted has shifted.

Then there is the new chair. Kevin Warsh, sworn in on May 22, 2026, has set a clear tone in his early tenure.

Warsh has stated publicly that current policy is “not particularly restrictive” and that restoring price stability is the priority.

When the Fed chair frames the current rate environment as insufficiently tight, that is a forward signal about tolerance for further increases. BofA’s Bhave has drawn a direct line between Warsh’s posture and the bank’s revised forecast: this is a chair who will not hesitate before tightening further if the data supports it.

BofA’s base case calls for three hikes and a multi-year hold. But the bank also identified three specific data signals that could interrupt that path. All three are characterised as tail risks, not probable outcomes, but they are worth monitoring as concrete indicators rather than abstract possibilities.

These are the three metrics to watch. If all three hold at current levels, BofA’s hiking path remains intact.

For investors who want to stress-test BofA’s hawkish assumptions before repositioning, our full explainer on the transitory inflation case for 2026 lays out the contrarian argument in detail, covering subdued M2 money supply growth, energy-driven pass-through limitations, and the leading indicators that could signal a faster-than-expected disinflation path.

BofA’s no-cuts-before-2028 horizon transforms the rate environment from a temporary headwind into a structural planning assumption. The implications cascade across asset classes.

| Asset Class | Key Exposure | Mechanism |

|---|---|---|

| Fixed income | Duration risk on longer-dated bonds | Yields adjust upward to reflect a hold-through-2027 environment, pressuring bond prices |

| Equities | Real estate, utilities, long-duration growth stocks | Higher discount rates compress valuations with no near-term cut relief |

| Consumer borrowing | Mortgages, auto loans, HELOCs, credit cards | Multi-year hold creates sustained cost pressure, not a temporary spike |

| FX / International | Firmer USD vs. easing peers | Pressures foreign earnings of US multinationals; headwinds for dollar-denominated EM debt |

For fixed income investors, duration risk remains elevated as the yield curve reprices around a 4.25-4.50% terminal rate. For equity holders, the sectors most exposed are those that depend on cheap capital: real estate, utilities, and long-duration growth names face valuation compression with no relief on the horizon before 2028.

Payrolls as a lagging indicator is precisely why BofA’s equity market exposure table warrants more attention than the labour market section: by the time monthly job figures confirm deterioration, equity markets will have already repriced the shift, meaning the structural planning assumption of higher rates through 2027 is more actionable for portfolio positioning than waiting for unemployment to visibly climb.

For consumers, the message is blunter. Mortgage rates, auto loans, HELOCs, and credit card rates stay elevated for years, not months. Anyone waiting for cheaper borrowing will be waiting past 2027 at minimum.

A tighter Fed relative to easing central banks abroad also supports the dollar, creating additional pressure on US multinationals’ foreign earnings and on emerging market borrowers carrying dollar-denominated debt.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding future rate projections are speculative and subject to change based on market developments and economic data.

Bank of America projects three 25 basis point Fed rate hikes in 2026, scheduled for September, October, and December, bringing the fed funds target rate to 4.25-4.50% by year-end.

Bank of America expects no rate cuts before 2028, with the Fed holding rates steady throughout all of 2027 after completing its projected 2026 tightening cycle.

Core PCE is the Fed's preferred inflation measure and has risen from 3.2% in March 2026 to 3.3% in April 2026, with BofA projecting approximately 3.5% for May 2026, a trajectory that is widening the gap from the Fed's 2% target rather than narrowing it.

Bank of America identified meaningful payroll deceleration from the current 172,000 monthly pace, softer core PCE readings below the 3.2-3.3% range, and a sharp equity market selloff as the three tail risks that could interrupt its base case of three hikes.

Fixed income investors face elevated duration risk as yields reprice around a 4.25-4.50% terminal rate, while equities in rate-sensitive sectors such as real estate, utilities, and long-duration growth stocks face valuation compression with no cut relief expected before 2028.