The Federal Reserve held its policy rate steady at 3.50%-3.75% on 16-17 June 2026, and in most cycles that would be the end of the story. It is not. Kevin Warsh, sworn in as the 17th Fed chair on 22 May 2026, used his first FOMC meeting to strip the policy statement down to its frame, remove forward guidance, and recentre the institution’s public message on a single objective: price stability. After five consecutive years of missing the 2% inflation target, the Fed’s new leader chose to say less, not more.

For investors and market participants trying to interpret what the Fed is doing and where rates are heading, the June 2026 FOMC meeting is a more useful entry point than any single rate decision. What follows is an analysis of what changed, what the internal committee split reveals about genuine policy uncertainty, and how to use the upcoming Core PCE release on Thursday, 25 June 2026 as a practical signal rather than a source of noise.

The stripped-down statement that told markets everything

The rate hold was the least informative part of the June outcome. Rates at 3.50%-3.75% had been widely expected. The policy statement itself carried the actual signal.

Warsh’s first statement as chair was significantly shorter than those issued under his predecessor. Forward guidance, a fixture of FOMC communications for the better part of a decade, was absent. There was no explicit easing bias, no language telegraphing the next move, no reassurance that cuts remained on the table.

The statement’s brevity was not an oversight. It was the message. By stripping out forward guidance, Warsh signalled that the Fed would no longer pre-commit to a direction, and that markets should read incoming data, not press conference language, for clues about what comes next.

The omission was calculated. A shorter statement with no directional bias gives the Committee maximum flexibility meeting to meeting, and it forces market participants to do their own analytical work rather than parse Fed sentences for hidden promises. That shift in burden is itself a policy choice.

Investors wanting to understand how the Fed’s communication architecture got to this point will find our full explainer on Federal Reserve forward guidance, which traces the expansion from 130-word statements in 2002 to nearly 900 words at the 2014 peak and examines the two most consequential guidance failures, the 2013 taper tantrum and the 2021-2022 transitory inflation episode, as case studies in what happens when prior commitments diverge from subsequent action.

When big ASX news breaks, our subscribers know first

What “price stability” means when a Fed chair says it twice

Warsh’s public remarks around the June meeting returned repeatedly to two themes: price stability and institutional credibility. The repetition was deliberate, and it marks a departure from the communication posture that prevailed before his appointment.

The prior regime leaned heavily on reassurance. Forward guidance was offered freely, easing timelines were signalled well in advance, and the implicit message to markets was: the Fed will tell you what it plans to do before it does it. Warsh has withdrawn that comfort.

His stated framework is data-dependent and meeting-by-meeting. In practical terms, this means no pre-committed rate path, no dot plot treated as a promise, and no press conference language designed to hold the market’s hand through the next quarter.

Why this changes how data releases land

The consequence is immediate and measurable. When the Fed pre-signals its path, individual data releases carry less marginal weight because the market already knows (or believes it knows) where policy is heading. When that guidance is pulled back, every inflation print, every jobs report, and every wage reading carries more policy information than it did six months ago. The volatility around data releases is not a side effect of Warsh’s approach. It is the mechanism.

The Fed’s inflation credibility problem and why it shapes everything now

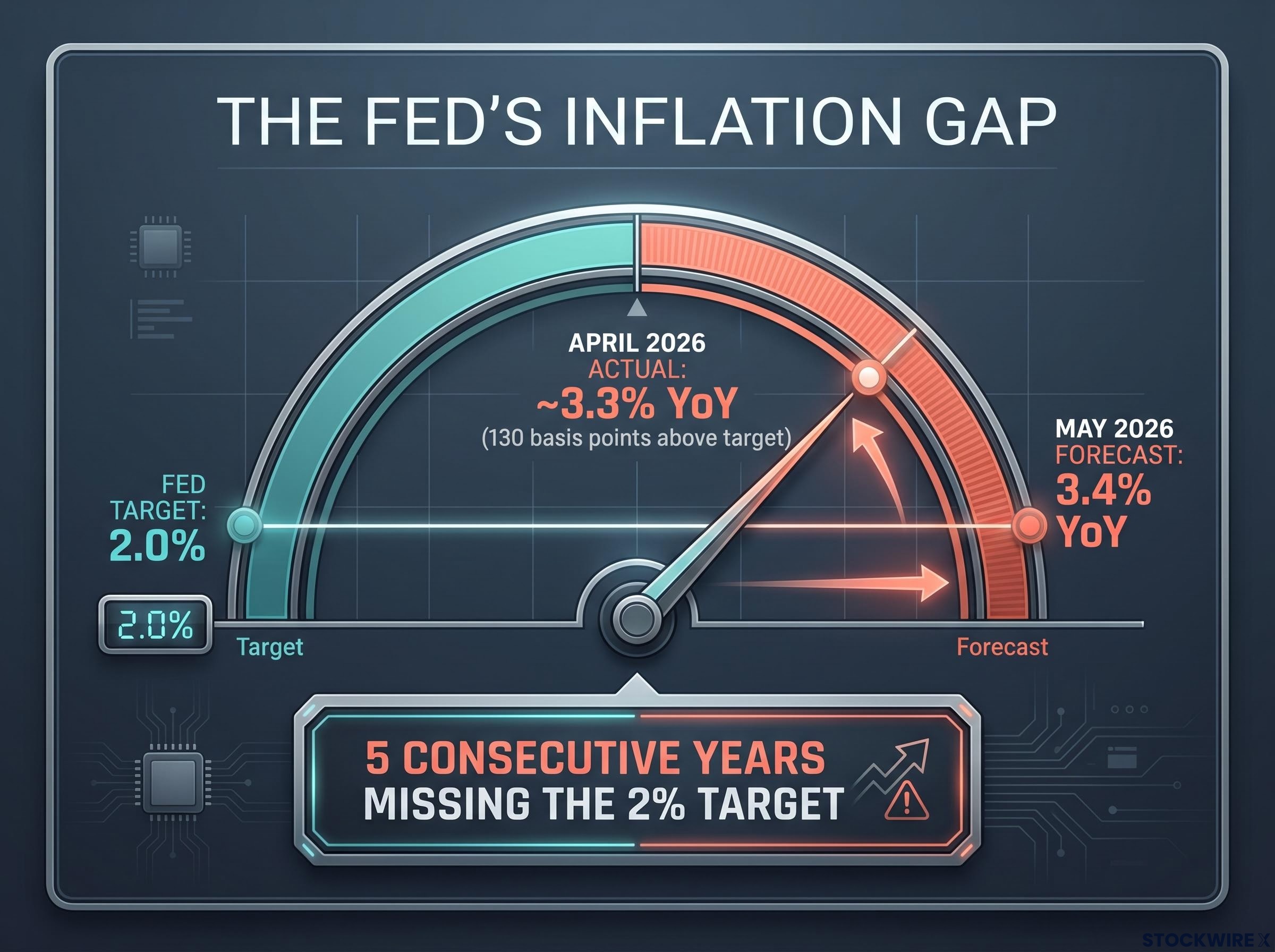

The hawkish posture does not exist in a vacuum. It is a response to a specific institutional problem: the FOMC has failed to deliver on its 2% inflation target for five consecutive years.

Warsh’s hawkish inheritance was visible before he chaired a single meeting: the committee he stepped into had already recorded four dissents at its April session, long-end yields were rising independently of rate decisions, and a Strait of Hormuz-driven oil shock was still feeding through to core price measures.

Core Personal Consumption Expenditures (Core PCE) is the Fed’s preferred measure of underlying inflation. It tracks the prices of goods and services purchased by consumers but strips out food and energy, which tend to be volatile and can obscure the trend. The Fed watches Core PCE more closely than headline Consumer Price Index (CPI) because it provides a cleaner read on the persistent inflation pressures that monetary policy is designed to address.

The April 2026 Core PCE reading came in at approximately 3.3% year-on-year. Monthly readings have ranged between 0.2% and 0.4% in recent months. Both figures sit well above the level that would signal convincing progress toward 2%.

The BEA Core PCE price index data confirms the April 2026 reading at 3.3% year-on-year and schedules the May 2026 release for 25 June 2026, making it the definitive source for the inflation figures that will determine whether the Warsh Fed’s hawkish bias hardens into action.

- Core PCE includes services, housing, healthcare, and goods prices but excludes direct food and energy costs

- It captures the underlying price pressures that do not reverse quickly when oil falls or harvests improve

- The Fed considers it a more reliable gauge of trend inflation than headline PCE or CPI

| Metric | Value | Period | Policy Implication |

|---|---|---|---|

| Core PCE (year-on-year) | ~3.3% | April 2026 (actual) | Still 130 basis points above the 2% target |

| Core PCE (month-on-month range) | 0.2%-0.4% | Recent months | Monthly pace too elevated for rapid convergence to 2% |

| Inflation target gap | 2.0% | FOMC objective | Five consecutive years of overshooting |

Five years of missing the target is not a recent blip. It is a structural credibility problem, and it explains why Warsh’s posture reads as hawkish rather than cautious. Rebuilding that credibility requires the Fed to demonstrate it will hold rates restrictive until the data confirm real progress, not simply forecast it.

The committee is split, and that split is information

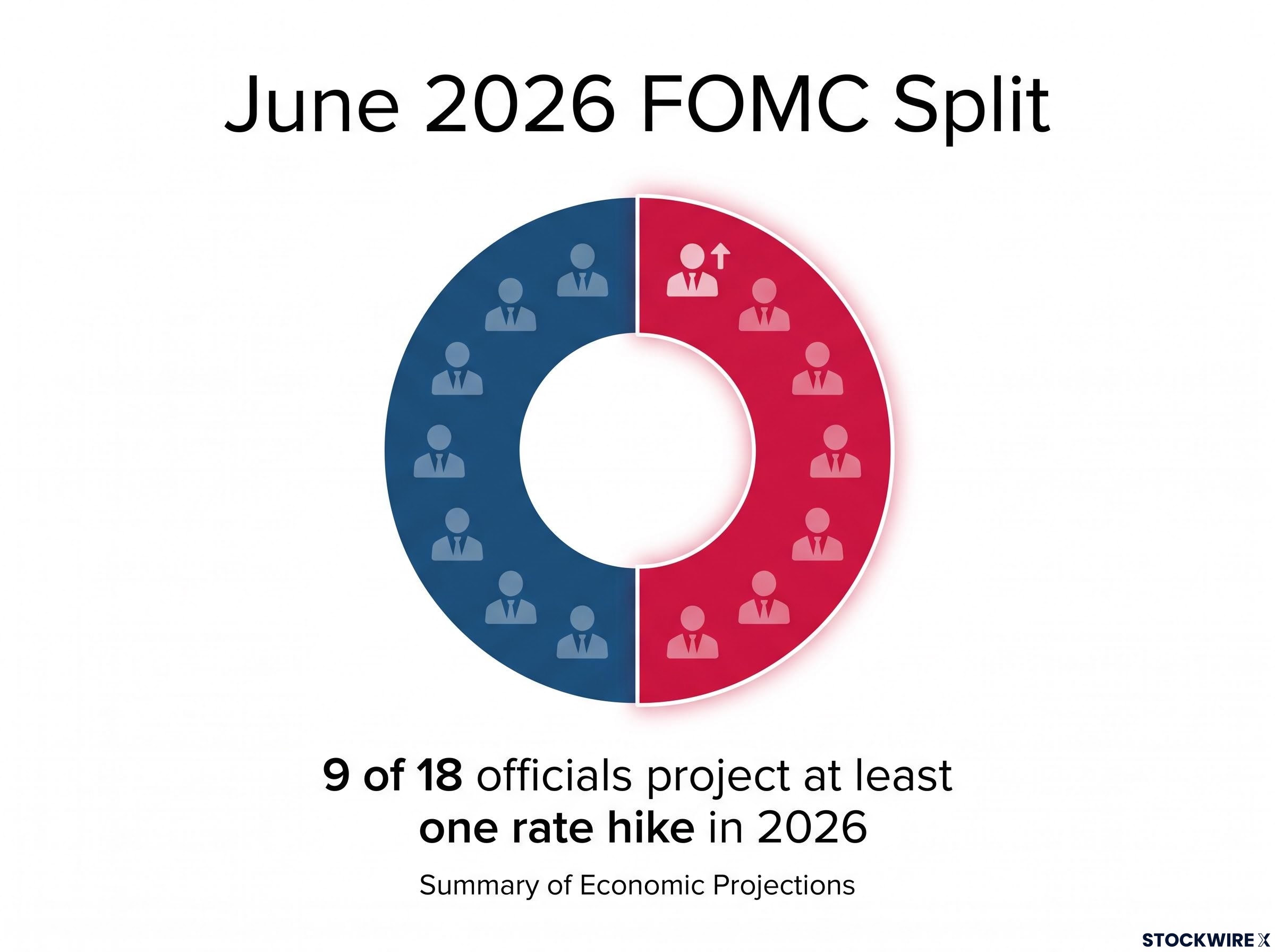

The June 2026 Summary of Economic Projections revealed that 9 of 18 FOMC officials now project at least one rate hike in 2026.

9 of 18. The committee is nearly evenly divided on whether rates need to go higher this year. That split is not dysfunction. It is the most honest representation of genuine policy uncertainty the Fed has offered in years.

A clean hawkish consensus would be simpler to trade around but less accurate. The reality is that roughly half the committee believes current settings are restrictive enough, while the other half sees further tightening as necessary if inflation does not bend. Neither camp has a decisive majority.

The market reaction to the June meeting reflected three distinct inputs, not one:

- The hawkish tone of the stripped-down statement and Warsh’s press conference remarks

- The revised projections showing more members pencilling in a rate hike than in prior meetings

- The removal of easing guidance, which closed the door on the rate-cut expectations that had persisted through early 2026

Vantage Market analyst Jamie Dutta noted that interest rate markets repriced approximately 50 basis points higher on a one-year forward horizon following the meeting. That repricing responded to a shift in probability distribution, not a concrete tightening step. No rate hike was announced. The move was entirely in expectations.

With forward guidance stripped back, the dot plot in this environment functions as a directional bias indicator, not a policy promise. The split should be read as genuine uncertainty, not noise.

Reading the May Core PCE print in context: limits, forecasts, and what shifts policy

The May 2026 Core PCE release, due Thursday, 25 June 2026, is the next significant data checkpoint for the Warsh Fed.

Forecasts point to 0.4% month-on-month and 3.4% year-on-year, which would represent a slight acceleration from the April reading of approximately 3.3% year-on-year.

| Metric | April 2026 (Actual) | May 2026 (Forecast) | What Would Shift Policy Calculus |

|---|---|---|---|

| Core PCE (month-on-month) | 0.2%-0.4% range | 0.4% | A reading at or below 0.2% would suggest disinflation is gaining traction |

| Core PCE (year-on-year) | ~3.3% | 3.4% | A sustained move below 3.0% over multiple months would challenge the hawkish stance |

Before reacting to Thursday’s number, one interpretive caveat deserves attention.

Recent sharp declines in oil prices affect headline PCE first. The pass-through to core inflation operates with a lag, feeding through production costs and services pricing over weeks and months, not immediately. A single core print in a period of falling energy prices may overstate underlying persistence.

The May reading may not yet capture the disinflationary effects of lower energy costs. That does not make the number irrelevant, but it does mean a hot print should be read alongside the energy transmission timeline, not in isolation.

The energy transmission lag the current article flags, where falling oil prices feed through to core services and production costs over weeks and months rather than immediately, runs 6-12 months by historical estimates, which is why June core readings may still reflect energy cost conditions that prevailed in late 2025 rather than the lower-price environment now in place.

How to read a Fed that has stopped telling you what it will do next

The analytical shift is straightforward. With forward guidance stripped back, the primary inputs for anticipating Fed direction are now inflation data and labour market readings, not the dot plot or press conference nuance. The communication architecture itself has changed, and that change is durable.

A practical framework for interpreting Fed signals under the Warsh regime:

- Watch the data, not the tone. Core PCE and wage metrics are the variables that will actually move policy. Hawkish rhetoric without deteriorating data does not produce a rate hike.

- Treat the internal split as genuine uncertainty. With 9 of 18 members projecting a hike, no outcome is pre-determined. The committee can move in either direction depending on what the data deliver.

- Read each print for marginal policy information. Individual data releases now carry more weight than they did under the prior forward-guidance regime. A single Core PCE print that breaks the pattern, in either direction, will shift expectations faster than it would have a year ago.

- Do not pre-position on the dot plot. Warsh’s meeting-by-meeting framework means the dots reflect a moment-in-time bias, not a commitment. Pre-positioning based on the June projections is more speculation than analysis.

The higher-for-longer rate path will only be reversed by decisive, sustained progress toward 2%. Until that progress materialises in the data, the hawkish bias is real and conditional, not performative.

For investors who want to model specific portfolio positions against each possible path, our deep-dive into the 2026 rate outlook scenarios examines how long-duration Treasuries, REITs, and rate-sensitive equities reprice under hold, hike, and cut outcomes, with probability weightings drawn from Fed funds futures at the time the committee fracture first became visible.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A Fed that signals less and reacts more

The June 2026 FOMC meeting changed the regime, not the rate. That distinction matters more than any single basis point.

Warsh has reduced forward guidance to near zero, elevated price stability as the institution’s stated priority, and allowed markets to infer a higher-for-longer path from the data rather than from Fed language. The communication architecture is itself a policy instrument: less signalling, more flexibility, and greater weight on each incoming data release.

What to watch from here is specific. Core PCE trajectory over the next two to three months will determine whether the hawkish bias hardens into action. The evolution of the internal committee split, visible in subsequent Summary of Economic Projections releases, will show whether the 9-of-18 division widens or narrows. And the distance between 3.3% Core PCE and the 2% target remains the single most important number in American monetary policy.

The Fed has stopped telling markets what it will do next. The data will have to do the talking.