Why an 11% Yield Fund Left Investors $20,000 Behind

10 hrs ago

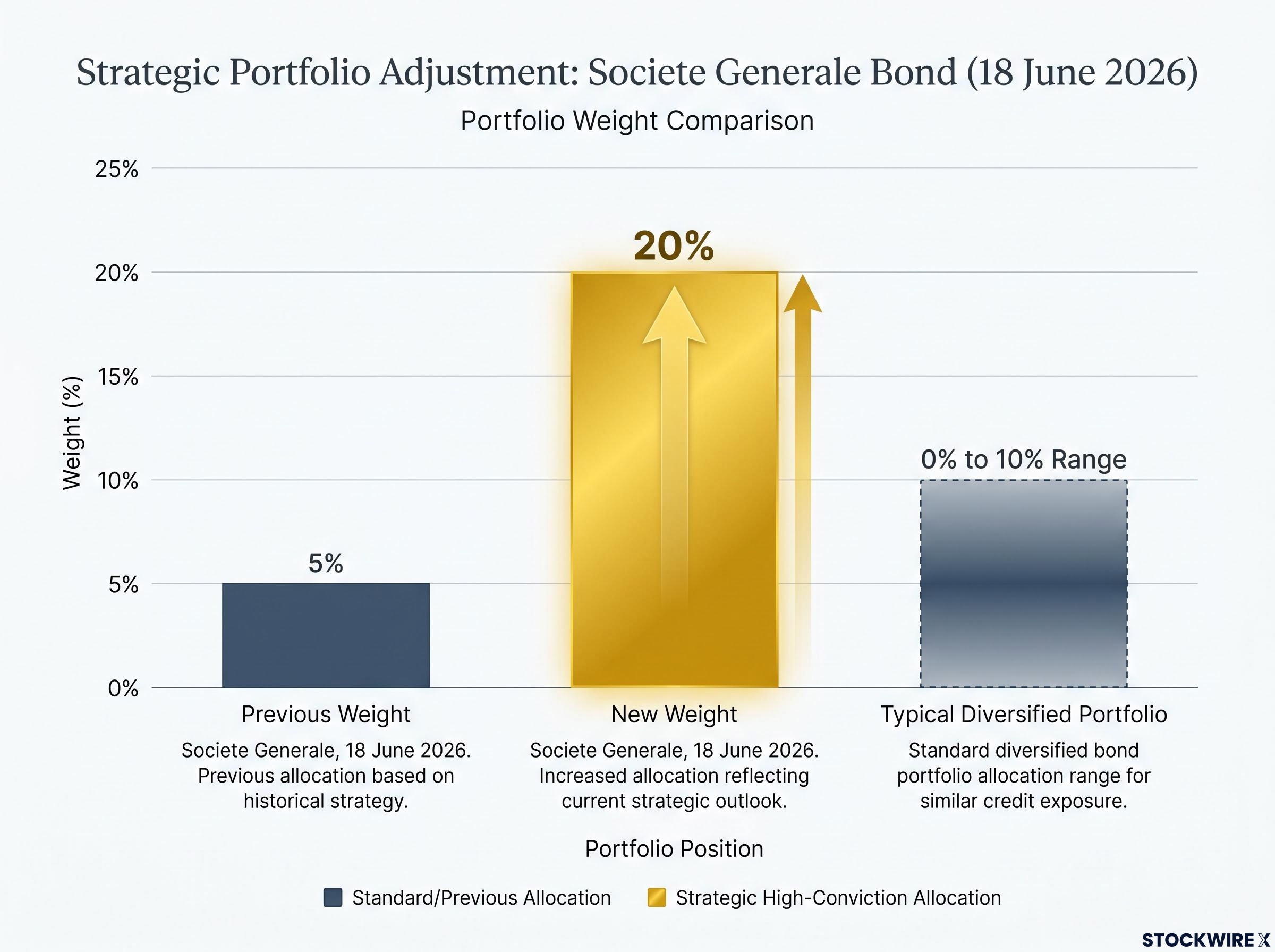

In a single allocation update published on 18 June 2026, Societe Generale quadrupled its recommended commodities weighting, lifting the position from 5% to 20% of a model portfolio. A 15-percentage-point shift in one step sits at the outer edge of what diversified institutional portfolios typically hold in real assets. It signals not a tactical tilt but a regime-level conviction that the next capital cycle will be materials-intensive in ways the past decade was not.

The bank’s thesis rests on five structural demand drivers, a specific equity sector map, a separately treated gold recommendation, and a quantitative portfolio construction argument that commodities improve long-term efficiency in higher-volatility macro regimes. What follows unpacks each layer of that conviction: what is driving the call, how the structural themes compound, which sectors the bank flagged, and how to use the framework to evaluate commodity-linked exposure in an existing portfolio.

The arithmetic alone is worth pausing on. Societe Generale moved from a 5% commodity allocation to 20%, a fourfold increase executed in a single step on 18 June 2026. In most diversified multi-asset portfolios, commodities occupy somewhere between 0% and 10%, treated as a diversifier rather than a growth engine.

A 20% strategic allocation to commodities is at the very high end of what diversified institutions run in traditional multi-asset portfolios, where the asset class has historically served a supporting role.

A move of this scale communicates three things at once:

The macro backdrop underpinning the bank’s conviction is a structural inflation regime in which all thirteen forces that drove four decades of disinflation have not only stalled but reversed simultaneously, a configuration that 150 years of inflation cycle data suggests resolves over decades rather than quarters.

That framing is the prerequisite for taking the structural thesis seriously. This is a high-conviction call from an institution with the systematic research to back it, not a routine quarterly rebalance.

The bank identified five long-term demand drivers behind its allocation upgrade. Each one is either policy-locked or politically sticky, which means the demand it generates is multi-year rather than cyclical. Understanding which physical materials each force consumes is where the thesis becomes investable rather than abstract.

| Structural Driver | Key Commodities | Relevant Equity Sectors |

|---|---|---|

| Electrification | Copper, aluminium, steel, lithium, nickel, manganese | Utilities, metals/mining, industrials |

| AI Infrastructure | Copper, steel, concrete, power generation | Utilities, industrials, energy services |

| Defence Spending | Steel, aluminium, titanium, specialty alloys | Industrials, aerospace/defence |

| Energy Independence | Steel, cement, copper, rare earths | Oil and gas equipment/services, utilities, nuclear |

| National Sovereignty and Reshoring | Critical minerals, rare earths, battery metals | Metals/mining, industrials, semiconductors |

Electrification of transport, industry, and buildings is one of the largest capital programmes of the next two decades, requiring grid upgrades and renewable build-outs that are lagging targets globally. AI data centres are extremely power-intensive, driving new generation capex plus copper for power delivery and cooling. Defence procurement programmes, once ramped, typically run for years and generate sustained demand for metals and specialty alloys.

The AI commodity supercycle has become one of the most quantified demand arguments in institutional research, with S&P Global projecting that data centres and associated grid upgrades will add approximately 1.0-1.2 million tonnes of copper demand per year by 2030, equivalent to roughly 4-5% of total global supply at that time.

Energy independence operates through two channels simultaneously: traditional fossil infrastructure and transitional investment in renewables, storage, and grid resiliency. Sovereignty politics channel capital into domestic industrial bases, strategic mineral stockpiling, and onshoring of battery and semiconductor manufacturing. Each driver individually would be notable. Together, they form the foundation of the bank’s structural case.

The five drivers are not independent bets running in parallel. They are overlapping claims on the same physical materials, and that overlap is what makes the thesis harder to derail than a single-theme commodity call.

The specific intersections are worth mapping:

The IEA critical minerals demand outlook projects accelerating consumption of rare earth elements and battery metals driven by electrification, AI data centres, robotics, and defence systems, reinforcing the multi-sector overlap that underpins Societe Generale’s structural case.

The stacked set of motives (climate, growth, security, and technological competitiveness) makes it unlikely that any single political or market shift dismantles the entire cycle. Societe Generale’s 15-point allocation increase reflects precisely this logic: the bank’s view that multiple forces will sustain above-trend materials demand simultaneously across the 2026-2030 planning horizon, not that one theme will dominate. That compounding quality is what separates a structural thesis from a cyclical bet.

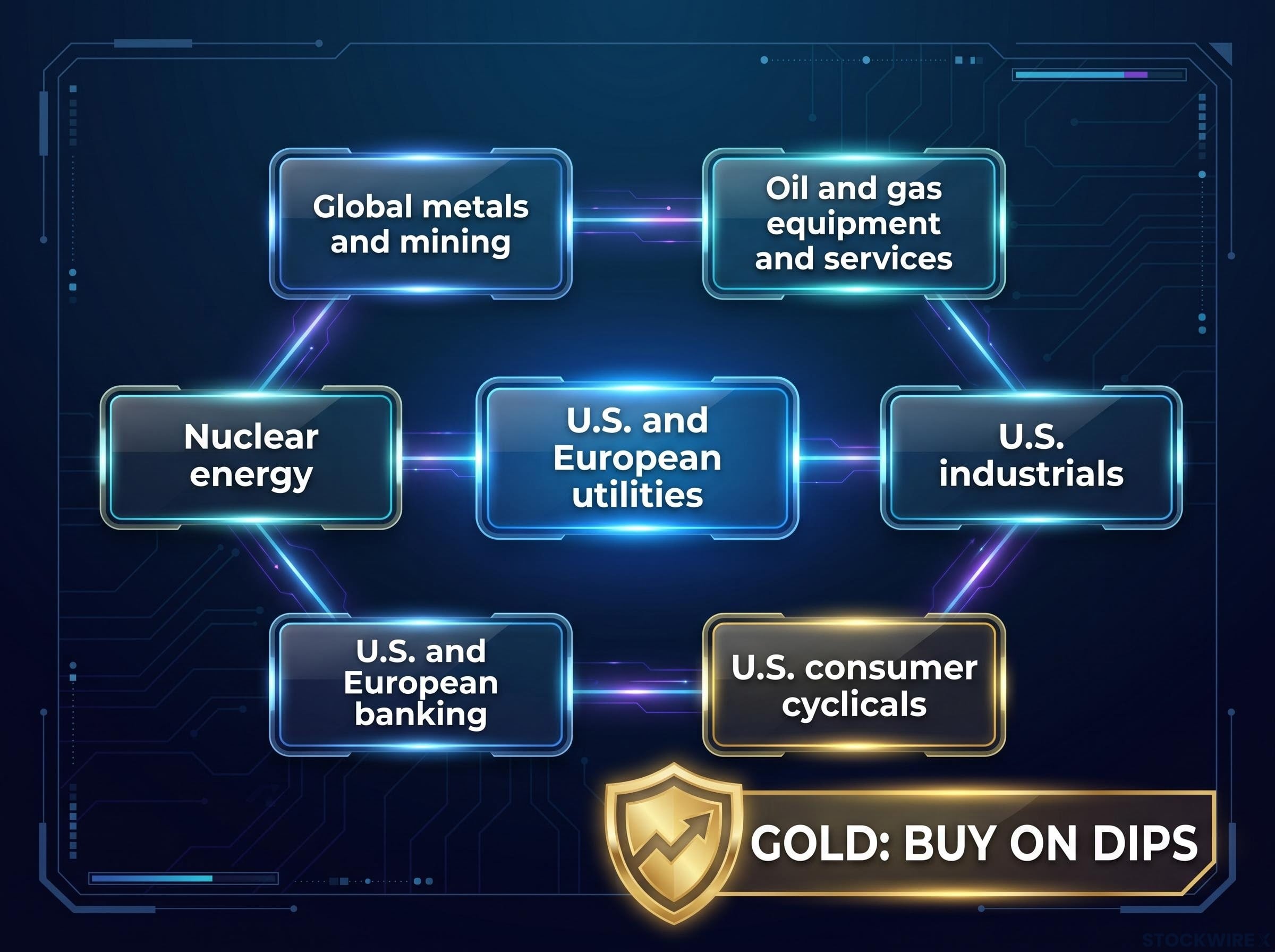

The macro case is one thing. Where it becomes actionable is in the specific sectors Societe Generale identified as preferred holdings within its updated framework. The bank flagged seven equity sectors:

Each connects directly to the underlying commodity thesis. Metals and mining offers the most direct equity exposure to the materials cycle. Utilities and industrials capture the capex flowing into power generation, grid expansion, and infrastructure build-out. Oil and gas equipment and services benefits from energy independence spending. Nuclear energy sits at the intersection of power demand, decarbonisation, and energy security. Banking exposure reflects the financing activity that a multi-year infrastructure cycle generates.

The distinction between direct commodity exposure (futures, exchange-traded funds) and equity exposure matters. Direct instruments offer cleaner price-level linkage. Equities provide leveraged exposure to the capex cycle with earnings growth potential and dividends, but carry company-specific risks.

Gold: buy on dips. The bank singled out gold with a specific buy-on-dips recommendation, treating it as both a structural holding (supported by central bank buying and reserve diversification) and a portfolio hedge against monetary and market regime uncertainty. The stance implies confidence in a structural price floor even during short-term volatility.

Central bank buying of 244 tonnes in Q1 2026 alone provides the structural floor for gold that underpins the bank’s buy-on-dips stance, with reserve managers from emerging market central banks treating gold accumulation as a multi-year reserve diversification programme rather than a tactical hedge.

The value of the bank’s analysis lies in using it as a lens for evaluating existing holdings, not in replicating a 20% weight. Individual risk tolerance, liquidity needs, and current exposures should determine sizing; 20% is an institutional model portfolio weight, not a universal prescription.

Five dimensions offer a structured diagnostic:

The bank’s own sector selections span U.S. industrials, European utilities, and global miners, reflecting a view that the infrastructure cycle is not confined to one region. Matching that geographic breadth in portfolio exposure reduces concentration risk tied to any single policy environment.

A thesis without a stated risk case is a sales pitch. Five scenarios could delay or attenuate the structural commodity cycle:

China remains the swing factor for base metals. Its outsized role in global commodity consumption means that the pace of Chinese industrial activity is the single most concrete near-term variable that could weaken demand for copper, steel, and aluminium regardless of how strongly the other structural drivers perform.

Each risk is better understood as a condition that could delay the thesis rather than immediately invalidate it, given the multi-year planning horizon and the compounding nature of the demand drivers.

For investors stress-testing the timing of their commodity positioning, our full explainer on bond yield headwinds for commodities walks through the two distinct transmission channels by which rising Treasury yields suppress gold, copper, and broader resources prices, using the May 2026 global selloff across ASX and US resources stocks as a live worked example.

Societe Generale’s move is a high-conviction signal that the next capital cycle will be structured around physical infrastructure and real assets in ways that the preceding decade, dominated by financial assets and technology platforms, was not. The 2026-2030 planning horizon frames this as an institutional consensus view of a multi-year shift, not a quarterly tactical call.

The bank’s own systematic research shows that commodities and gold improve long-term portfolio efficiency in higher macro-volatility regimes, anchoring the allocation shift in quantitative portfolio construction logic rather than only a narrative macro view. That quantitative foundation is what justifies the scale of the move.

PGIM research on real assets and portfolio performance found that portfolios including real assets have historically delivered higher average returns, lower volatilities, and better risk-adjusted outcomes during periods of high and rising inflation, providing quantitative grounding for the scale of Societe Generale’s allocation shift.

For investors evaluating their own positioning, the thesis is most useful as a framework for identifying where earnings durability in commodity-linked sectors originates. Holdings that sit at the intersection of multiple structural drivers, whether utilities exposed to both AI power demand and electrification, or miners supplying both defence and battery supply chains, carry a different risk profile than single-theme exposures. That distinction, more than any specific portfolio weight, is the durable takeaway from the bank’s analysis.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and commodity markets are subject to significant volatility and various risk factors.

Societe Generale raised its recommended commodities weighting from 5% to 20% of a model portfolio on 18 June 2026, a fourfold increase executed in a single step that reflects structural conviction rather than a routine tactical tilt.

The bank identified electrification, AI infrastructure build-out, rising defence spending, energy independence investment, and national sovereignty and reshoring policies as the five long-term demand drivers, each generating multi-year rather than cyclical commodity consumption.

The bank flagged global metals and mining, oil and gas equipment and services, nuclear energy, U.S. and European utilities, U.S. industrials, U.S. and European banking, and U.S. consumer cyclicals as the seven preferred equity sectors connected to its structural commodity view.

The bank issued a specific buy-on-dips recommendation for gold, treating it as both a structural holding supported by central bank buying (244 tonnes in Q1 2026 alone) and a portfolio hedge against monetary and market regime uncertainty.

Key risks include a faster-than-expected supply response from new mine capacity, policy reversal or fiscal austerity slowing infrastructure programmes, technological substitution reducing commodity intensity, boom-bust demand destruction, and a sharper-than-expected deceleration in China's industrial economy.