Hyperscalers are projected to spend more than $700 billion on physical infrastructure in 2026 alone, yet most investors chasing AI exposure are concentrated in the same handful of software and semiconductor names trading at roughly 25 times forward earnings. The physical layer of the AI buildout, the copper wiring, the nuclear fuel rods, the rare earth magnets inside cooling motors, is where a growing number of institutional analysts argue the relative value opportunity actually sits.

Every GPU rack requires copper for power delivery and liquid cooling. Every data centre requires reliable baseload electricity. Every battery storage system used to firm that power requires lithium, nickel, and graphite. The commodity demand embedded in the AI infrastructure supercycle is structural, multi-year, and increasingly recognised by major research houses as a parallel investment thesis to direct AI equity exposure.

What follows is a framework for understanding which commodities benefit most from AI infrastructure growth, in what quantities, and how that demand signal translates into what Goldman Sachs, Bank of America, J.P. Morgan, and others argue is a mispriced opportunity sitting in plain sight.

Why AI infrastructure runs on copper, not just code

Most investors have not visualised what an AI data centre actually looks like from a materials perspective. The racks are not ethereal. They are dense, hot, and wired with metal.

AI capital expenditure commitments from the four largest hyperscalers now sit in the $600-$805 billion range for 2026 alone, a figure that contextualises why the materials embedded in every rack, every cooling loop, and every grid connection carry a demand signal unlike anything the commodity system has processed before.

Copper serves two distinct functions inside an AI-optimised hyperscale facility:

- Power delivery: Copper wiring carries electricity from the grid connection through transformers and distribution panels to each individual GPU rack.

- Liquid cooling thermal interface: Modern high-density GPU racks generate heat loads that air cooling cannot manage. Liquid cooling systems, now standard in AI-optimised facilities, use copper as the thermal interface between the processor and the cooling water.

The transition from air cooling to liquid cooling is not incremental. It has fundamentally changed the copper intensity of each rack.

From rack to grid: scaling the copper demand signal

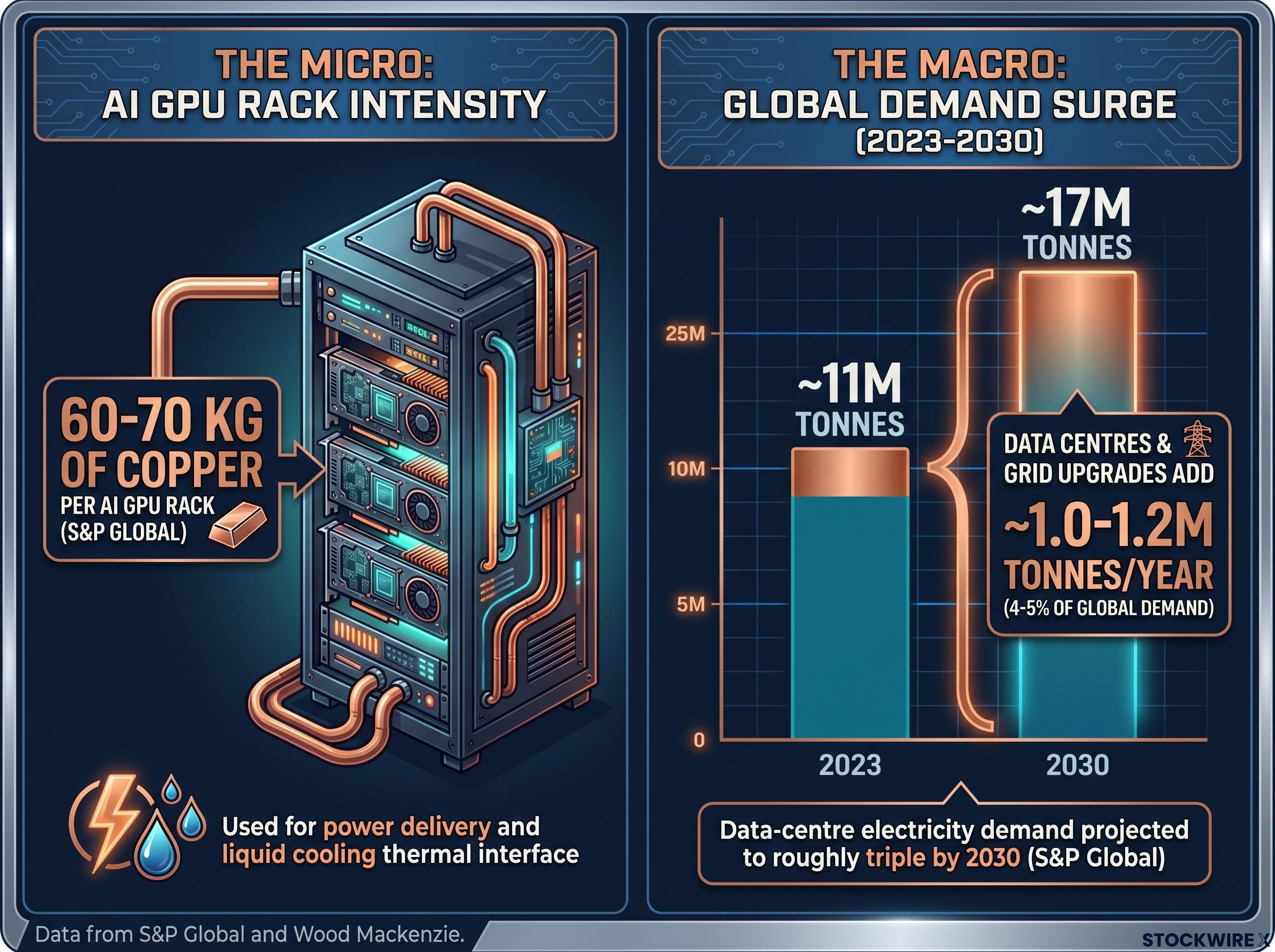

A single AI GPU rack in a hyperscale data centre requires an estimated 60-70 kilograms of copper, according to S&P Global’s usage assumptions for AI-optimised facilities. That figure accounts for both the power delivery wiring and the liquid cooling infrastructure.

Multiply across the fleet and the numbers become difficult to dismiss. S&P Global Commodity Insights projects that global data-centre electricity demand will roughly triple between 2023 and 2030.

S&P Global’s Copper in the Age of AI study projects a 50% increase in total copper demand by 2040, with AI data centres and defence spending each expected to roughly triple their copper consumption over that period, representing a combined 4 million metric tonnes of additional demand.

S&P Global estimates that data centres and associated grid upgrades will add approximately 1.0-1.2 million tonnes per year of copper demand by 2030, equivalent to roughly 4-5% of total global copper demand at that time.

The demand is split between on-site data-centre copper (racks, cooling loops, internal power distribution) and off-site grid infrastructure copper needed to connect new facilities to the power supply. Wood Mackenzie projects global copper demand rising from approximately 11 million tonnes in 2023 to approximately 17 million tonnes by 2030, with several hundred thousand tonnes of that increase attributed specifically to data centres.

When big ASX news breaks, our subscribers know first

What the copper market actually looks like right now

The forward-looking demand thesis does not exist in a vacuum. The copper market is already exhibiting the tightness the thesis requires.

The copper market deficit for 2026 is now projected at approximately 520,000 metric tonnes by UBS, more than double the prior year shortfall, with three simultaneous supply failures converging: China’s sulphuric acid export halt, a force majeure at Freeport-McMoRan’s Grasberg operation, and reduced output guidance from Teck Resources, each of which compounds the structural tightness the AI demand signal is landing on.

| Metric | Figure | Source | Date |

|---|---|---|---|

| COMEX copper price | ~$4.80/lb (~$10,600/t) | Financial Times | 31 May 2026 |

| LME three-month copper | ~$10,500/t | Reuters | Late May 2026 |

| Goldman Sachs demand growth forecast | ~3.5-4% annual growth to 2030 | Goldman Sachs via Financial Times | April 2026 |

| S&P Global data-centre copper demand addition | ~1.0-1.2 Mt/year by 2030 | S&P Global Commodity Insights | May 2026 |

Goldman Sachs attributes approximately 40% of incremental copper demand growth to electrification, including AI data centres and cloud infrastructure, with AI specifically contributing roughly 0.4-0.6 percentage points to annual demand growth by 2030.

Goldman Sachs has characterised copper as “the new oil of the AI age”, arguing that copper miners provide under-appreciated leverage to AI infrastructure growth and that miner valuations do not fully reflect the AI demand impulse.

The supply side compounds the picture. New copper mines typically take 15-20 years from discovery to production. The market is pricing in some of the thesis already; the question for investors is how much structural tightness remains unpriced.

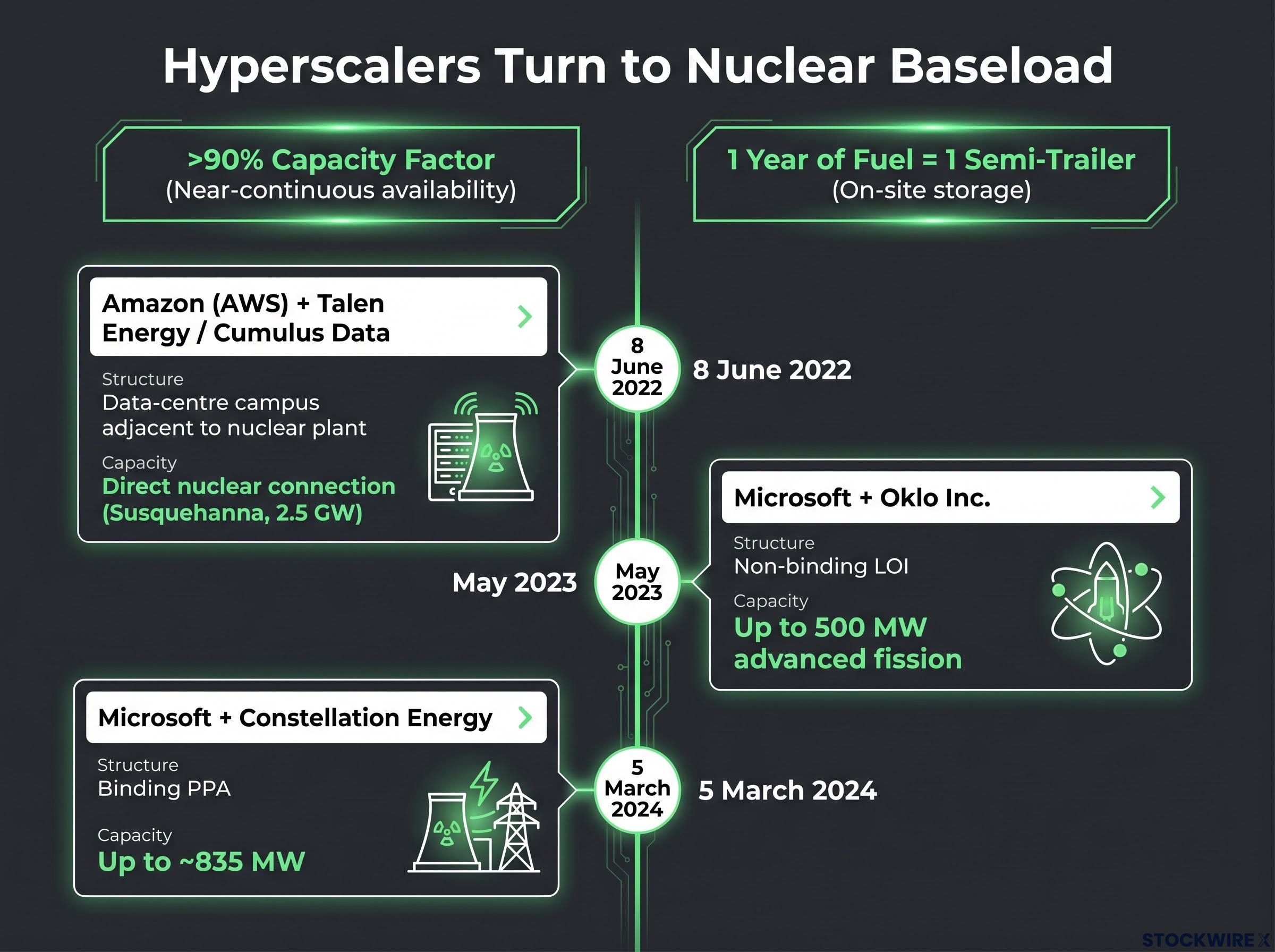

Nuclear power has become the preferred energy source for hyperscalers, and uranium supply cannot keep up

Hyperscalers are not passively waiting for grid power to materialise. They are contracting nuclear capacity years in advance, which reveals what their own internal models suggest about future power scarcity.

Nuclear energy suits data-centre power requirements for three structural reasons:

- Near-continuous availability: Nuclear plants operate at capacity factors exceeding 90%, providing the around-the-clock baseload that AI workloads demand.

- On-site fuel storage: One year of uranium fuel for a nuclear plant fits in a single semi-trailer, eliminating pipeline or delivery-chain vulnerability.

- Carbon-free generation: Nuclear satisfies hyperscaler net-zero procurement commitments without the intermittency of wind and solar.

The corporate commitments are specific, named, and dated.

| Company | Partner | Structure | Capacity | Date |

|---|---|---|---|---|

| Microsoft | Constellation Energy | Binding PPA | Up to ~835 MW | 5 March 2024 |

| Amazon (AWS) | Talen Energy / Cumulus Data | Data-centre campus adjacent to nuclear plant | Direct nuclear connection (Susquehanna, 2.5 GW) | 8 June 2022 |

| Microsoft | Oklo Inc. | Non-binding LOI | Up to 500 MW advanced fission | May 2023 |

The Microsoft–Constellation Energy deal, sourced from the Calvert Cliffs Nuclear Power Plant in Maryland, represents one of the largest 24/7 clean-power agreements announced to date. The AWS–Talen Energy arrangement in Pennsylvania provides direct connection to nuclear-powered baseload electricity. The Oklo letter of intent, while non-binding, signals Microsoft’s interest in next-generation fission as a longer-term capacity source.

The uranium market underpinning this demand is structurally tight. Spot uranium sat at approximately $88-90 per pound as of late May 2026, according to S&P Global and the Financial Times. Bank of America expects uranium markets to remain in structural deficit through at least 2030, forecasting average prices of $80-100 per pound over the second half of the decade, driven by reactor restarts, life-extension programmes, and new builds, including China’s approximately 37 nuclear plants under construction before the end of the decade.

Sprott Asset Management has characterised the market as a “multi-year supply crunch”, with existing and planned mine supply insufficient to meet forecast reactor demand through 2035 under current policies.

Understanding commodity supercycles: why this one may be different

A commodity supercycle is a sustained multi-year period in which commodity prices remain above their long-term trend, driven by a structural demand shift that outpaces the supply system’s ability to respond. The last widely recognised supercycle was the 2000s China industrialisation buildout, which lifted copper, iron ore, and coal prices for the better part of a decade.

What makes the current moment analytically distinct is that demand is not coming from a single source. AI data centres, electric vehicles, renewable energy grids, and defence procurement are all competing for the same metals simultaneously. BCA Research’s commodity strategy team captured the thesis directly.

“AI is not just a software story; it is a metals and power story.” BCA Research, Commodity & Energy Strategy

J.P. Morgan has stated that “AI infrastructure will be metals- and power-intensive, supporting a secular bull case for select commodities.” Goldman Sachs has framed copper miners as providing under-appreciated leverage to the AI buildout. The institutional convergence on this thesis is unusually broad.

Why supply cannot catch up quickly

The mechanism that separates a supercycle from a price spike is the supply-response lag. Three structural constraints limit how quickly the commodity system can respond:

- Mine permitting and development timelines: A new copper mine typically takes 15-20 years from discovery to first production. Uranium mine development faces similar permitting and financing constraints.

- Capital underinvestment: After the post-2010s bear market in commodities, mining companies cut exploration budgets and deferred project approvals. The pipeline of shovel-ready projects is thin.

- Geopolitical concentration risk: Bank of America identifies Kazakhstan and Niger as uranium supply risk factors, given that a material share of global production and reserves sits in jurisdictions with elevated political or sanctions risk.

These constraints are not cyclical. They are structural features of the supply system that persist regardless of how high prices go in the near term.

Critical minerals beyond copper: where AI infrastructure touches lithium, rare earths, and graphite

Not all critical minerals carry the same weight in the AI infrastructure thesis. The distinction between direct demand links and adjacent ones matters for investment positioning.

| Commodity | AI Infrastructure Link | Recent Price Trend | Analyst Outlook |

|---|---|---|---|

| Copper | Direct: power delivery, liquid cooling | ~$10,500-10,600/t (historically elevated) | Structural deficit; 3.5-4% annual demand growth |

| Uranium | Direct: nuclear baseload for data centres | ~$88-90/lb (elevated) | Structural deficit through 2030+ |

| NdPr oxide | Direct: permanent magnets in cooling motors and power systems | Up ~25% from late-2025 levels | Supply constrained; US policy push for domestic sourcing |

| Lithium | Indirect: battery storage firming data-centre power | Rebounded ~40% from mid-2025 lows | ~14-16% demand CAGR to 2030 (Benchmark Mineral Intelligence) |

| Nickel | Tangential: high-temp alloys, not a current bottleneck | Down ~30% from early-2024 highs | Global surplus projected through late 2020s |

| Graphite (synthetic) | Direct: thermal management in high-density AI servers | Firmer pricing than natural graphite | Growing importance in high-density thermal applications |

NdPr oxide prices rose approximately 25% from late-2025 levels as of February 2026, according to the Financial Times, driven by demand for permanent magnets used in data-centre cooling systems, EVs, and wind turbines. Synthetic graphite for battery anodes and high-end thermal management has held firmer pricing while natural graphite remains under pressure from Chinese oversupply.

China’s dominance of the rare earth magnet supply chain, estimated at approximately 93% of global permanent magnet production and roughly 99% of heavy rare earth element processing, means that NdPr oxide demand growth from AI cooling systems and data-centre power equipment lands on a supply base with a single dominant geography, a concentration risk that US policy responses so far have not yet structurally resolved.

Lithium’s link is indirect but real: battery storage systems that firm intermittent renewable power at data-centre sites require lithium-ion cells. Benchmark Mineral Intelligence projects global lithium demand growing at approximately 14-16% CAGR from 2025 to 2030. Nickel, by contrast, is not currently a bottleneck; Wood Mackenzie projects continued global surplus through the late 2020s under current Indonesian expansion plans.

US policy is actively supporting the supply chain. The Department of Energy and Department of Commerce expanded funding and tax-credit eligibility for domestic production of critical minerals and data-centre components as of February 2026, covering:

- High-efficiency power electronics

- Advanced cooling systems

- Grid-scale storage components

The valuation gap: why resource equities may offer AI exposure at a discount

The commercial argument at the centre of the resource thesis is a valuation spread. The NASDAQ 100 was trading at approximately 25 times one-year forward earnings, while energy sector stocks were trading at approximately 14 times earnings. S&P 500 projected earnings growth exceeds 20% for the current year, with energy sector earnings growth estimates revised upward from approximately 25% to roughly 50% since March.

The institutional consensus is unusually aligned. Goldman Sachs argues that copper miners provide under-appreciated leverage to AI infrastructure growth, with valuations that do not fully reflect the AI demand impulse. Bank of America suggests investors are under-allocating to resource equities relative to megacap technology, identifying copper, uranium, and select miners as “indirect AI exposure” at more attractive multiples. J.P. Morgan contrasts the high valuations of US mega-cap AI and cloud stocks with more modest multiples for global miners and energy-transition metals producers.

Bernstein has argued that “AI data centres are among the most commodity-intensive digital infrastructure ever built”, cautioning that investors focused solely on chipmakers and hyperscalers may be missing a parallel re-rating opportunity in resource and infrastructure names.

BlackRock has offered a more measured framing, noting that infrastructure and resource equities tied to power grids and data-centre construction could offer “AI-linked cash-flow growth at lower multiples” but exercising more caution on applying the “supercycle” label.

What could disrupt the commodity thesis

The bull case is not without material risks.

- Gas turbines as the near-term power solution: Gas turbines can be deployed in 2-3 years, compared to a decade or more for new nuclear capacity. AI power demand may be met via gas in the near term, moderating the uranium demand timeline.

- Commodity price cyclicality: The supercycle label has been applied and withdrawn before. Nickel’s 2022 spike and subsequent collapse serves as a reminder that structural narratives can unravel when supply responds faster than expected.

- Project execution and permitting risk: Mine-level delays, reactor licensing setbacks, and financing constraints can defer supply additions regardless of how strong the demand signal appears.

These risks do not invalidate the thesis, but they establish that the timing and magnitude of the opportunity are subject to variables that institutional forecasts cannot fully control.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The materials layer is where AI’s physical cost becomes an investor’s opportunity

The AI infrastructure buildout has three distinct commodity legs: copper for power and cooling, uranium for baseload energy, and select critical minerals (NdPr oxide, synthetic graphite, lithium) for the supporting systems that make data centres function at scale. Each carries a different conviction level, supply-side constraint profile, and timeline.

The same AI infrastructure spending driving technology stock multiples higher is creating measurable, durable demand for commodities that trade at a fraction of those multiples. The institutional convergence from Goldman Sachs, Bank of America, J.P. Morgan, Bernstein, and Sprott on this thesis is notable in its breadth, even as BlackRock urges caution on the supercycle framing.

Before acting, the analytical questions worth asking are specific: which miners have balance sheet strength to fund expansion, what is their exposure to AI-specific demand channels (data-centre copper contracts, utility nuclear offtake agreements), and what is their production timeline relative to the demand curve. Readers seeking further detail may find related coverage of copper miners, uranium royalty companies, and critical minerals ETFs useful starting points for building commodity exposure within a broader portfolio allocation framework.

For investors who want to translate the commodity thesis into a specific allocation decision, our deep-dive into mining ETF valuations and the supercycle debate examines the 136% surge in mining ETF assets to $87.4 billion over the past twelve months, breaks down what that capital is actually buying (83.7% precious metals versus industrial metals), and assesses whether the major miners’ current 7-8x EV/EBITDA multiples represent genuine re-rating potential or a crowded trade at risk of reversal.