Intel Stock Surges 10% to Record High on Apple Chip Deal

21 hrs ago

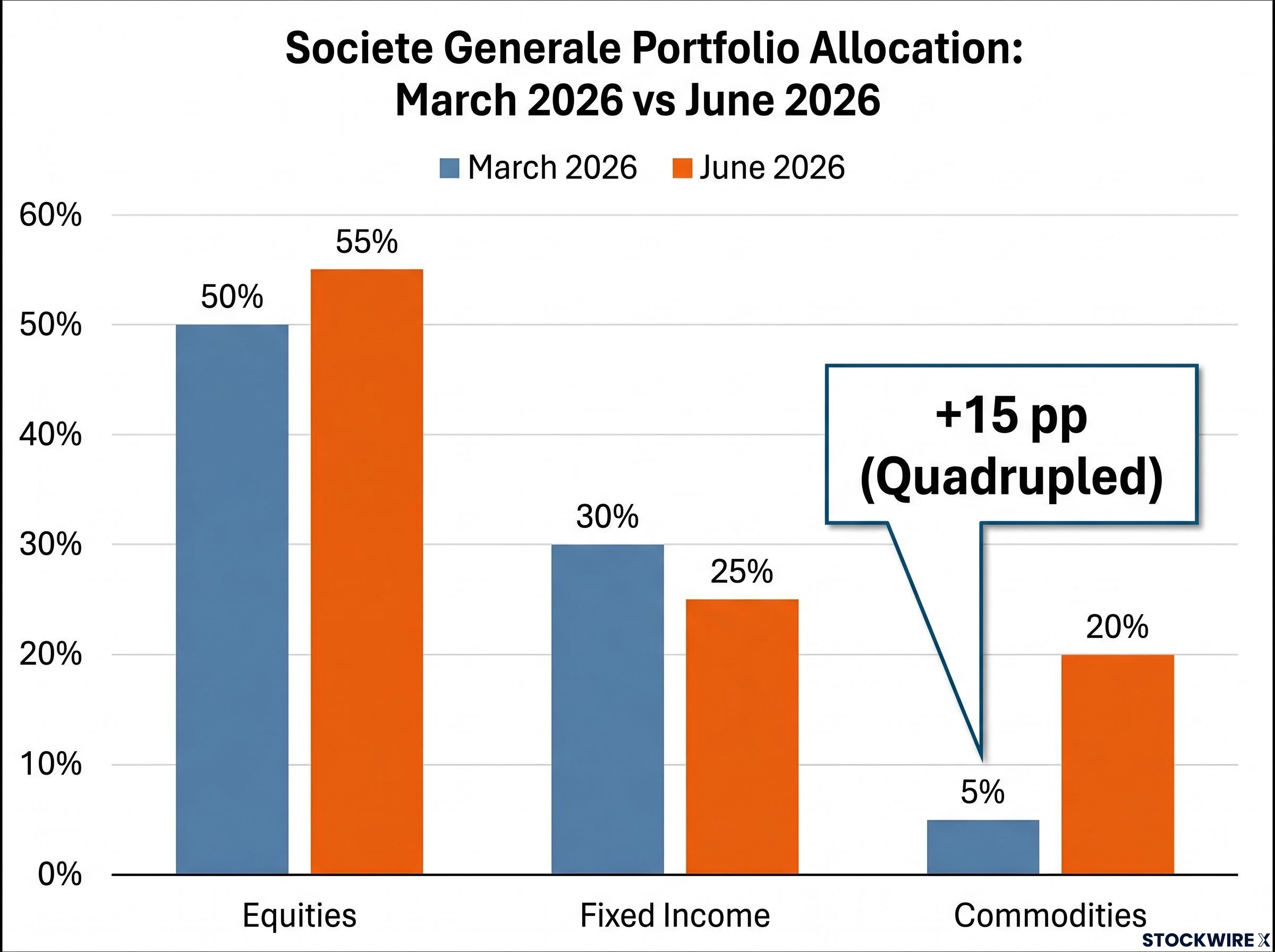

Societe Generale has quadrupled its commodities allocation in a single rebalancing, the most aggressive asset class move in the bank’s June 2026 portfolio update. Published yesterday by strategist Alain Bokobza, the updated model portfolio pushes equities to 55% and commodities to 20%, funded entirely by a reduction in fixed income. The combined shift reflects a macro view that moderate inflation and tolerant central banks will sustain the current risk rally through the second half of 2026. What follows is a breakdown of every change in the updated Societe Generale portfolio allocation, the macro logic behind each move, and what the combined signal means for investors monitoring institutional positioning.

Three asset classes moved simultaneously, and bonds funded the entire shift. Equities rose 5 percentage points to 55%, building on the 50% weighting set as recently as March 2026. Commodities jumped 15 percentage points to 20%, quadrupling in a single rebalancing. Fixed income fell 5 percentage points to 25%.

Societe Generale Cross Asset Research, led by Alain Bokobza, published the updated allocation on 18 June 2026.

The arithmetic is straightforward: equities and commodities gained a combined 20 percentage points of portfolio weight, and bonds surrendered only 5 percentage points. The remaining rebalancing reflects internal shifts between sub-asset classes rather than a drawdown of cash or alternatives. The scale of the commodities move, in particular, stands out as structurally unusual for a single quarterly update.

| Asset Class | Previous Weighting | New Weighting | Change |

|---|---|---|---|

| Equities | 50% | 55% | +5 pp |

| Commodities | 5% | 20% | +15 pp |

| Fixed Income | 30% | 25% | -5 pp |

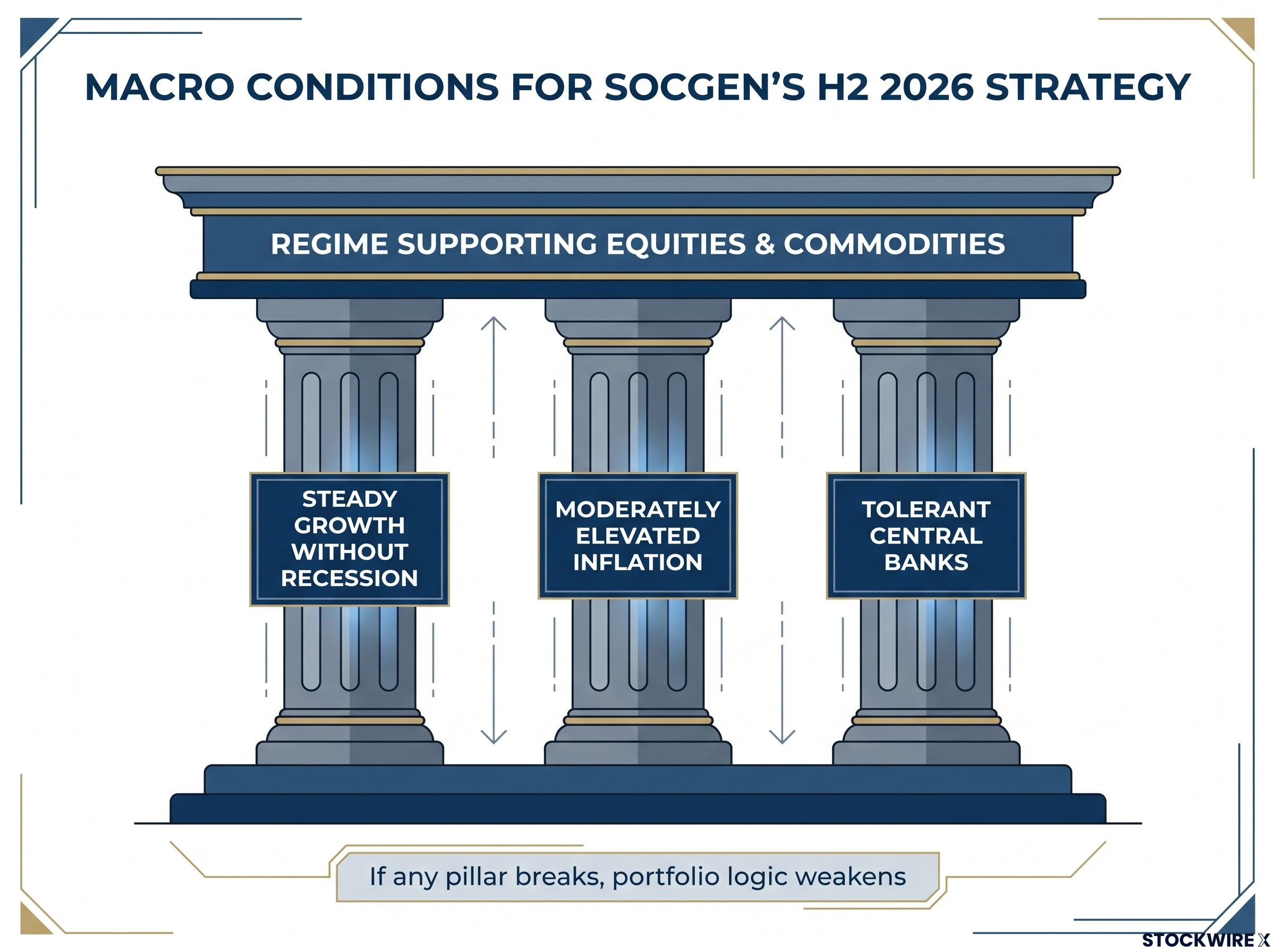

The reallocation rests on three simultaneous macro calls, and the portfolio only works if all three hold. SocGen’s strategists are betting on a specific regime rather than a generalised bullish outlook.

The combination of these three conditions, growth plus moderate inflation plus tolerant central banks, is the regime that historically supports equities and real assets while pressuring bond returns, particularly from duration-heavy government debt. SocGen’s view is that this regime will persist through the second half of 2026, making the reallocation a half-year directional call rather than a short-term trade. If any one of the three pillars breaks, the internal logic of the portfolio weakens considerably.

Regime-aware portfolio construction, the practice of designing allocations around specific macro conditions rather than long-run averages, has become the institutional consensus response to a world where AI capital concentration and modern mercantilism are simultaneously reshaping the return profiles of equities, bonds, and real assets.

The headline equity weighting of 55% is not a passive market bet. The construction beneath it reveals a set of active geographic and structural views.

SocGen chose the equal-weight S&P 500 as its primary U.S. vehicle, a decision that carries a specific conviction: market breadth will improve through the second half of 2026, with mid-cap and non-technology sectors participating more fully in returns. The equal-weight approach reduces concentration in the largest mega-cap technology names, implicitly positioning the portfolio for a rotation toward broader earnings growth rather than continued index-level dependence on a handful of stocks.

The equal-weight S&P 500 approach reduces the portfolio’s exposure to the largest mega-cap technology names by assigning identical weights to all constituents, a meaningful structural difference from cap-weighted indices where five stocks currently account for roughly 23% of total index weight.

Alongside the U.S. core, the portfolio adds index-level exposure to four international markets, each with a distinct rationale:

The combined equity construction is geographically diversified, cyclical, and value-tilted, anchored in the U.S. but explicitly global in scope.

A 15-percentage-point increase in a model portfolio allocation during a single rebalancing is structurally unusual. Institutional portfolios typically adjust commodity exposure by 2-5 percentage points per update. The scale of SocGen’s move signals something beyond a tactical tilt.

The logic is internally coherent with the bond reduction. Cutting fixed income to fund commodities expresses a deliberate preference: short real returns in bonds, long real assets. Commodities tend to outperform when inflation sits above target, real rates remain contained, and supply-demand conditions tighten, all conditions that align with SocGen’s stated macro expectations.

The commodity allocation is likely diversified across three sub-categories, each connected to a specific macro driver:

The World Bank Commodity Markets Outlook, published in May 2026, projects metal prices rising 17% across the year, driven by demand from data centres, electric vehicles, and renewable energy infrastructure, providing independent validation of the structural demand thesis underpinning SocGen’s industrial metals exposure.

SocGen’s strategists have framed the move as a response to a global multi-year infrastructure cycle and real-asset scarcity, positioning it as a structural allocation rather than a fleeting momentum trade.

A model portfolio published by a major bank is a statement of macro conviction and institutional positioning. It is not a personalised recommendation for individual investors to replicate mechanically.

This allocation reflects where SocGen’s Cross Asset Research team sees the highest risk-adjusted return potential across asset classes. It functions as an institutional communication tool, not a blueprint for personal portfolios.

If multiple large institutions adopt similar overweight equities and commodities, underweight bonds stances, the consensus trade becomes self-reinforcing until crowding risk builds. The positioning works until enough capital concentrates in the same direction to make the trade fragile on any macro surprise.

Three regime risks would invalidate the allocation:

Investors monitoring the thesis can track several forward indicators:

Major investment banks publish recommended portfolio allocations to communicate their macro views to institutional and sophisticated clients. These allocations function as structured expressions of directional conviction rather than legally binding investment advice. Societe Generale Cross Asset Research, the unit behind this update, is one of several strategy teams across global banks that publish comparable updates on a roughly quarterly cadence.

The percentage weightings reflect relative confidence across asset classes rather than precise instructions. Implementation varies widely across the institutional clients who use these publications as inputs. Some adopt the directional tilt while maintaining different absolute weightings; others use the changes between updates as a signal of shifting conviction.

Changes to these allocations, particularly large ones like the commodities quadrupling, attract market attention because they can indicate where institutional capital flows may shift in the weeks following publication. The prior equity weighting of 50%, set in March 2026, provides the reference point against which the current update’s acceleration can be measured.

SocGen’s June 2026 reallocation is a coherent directional bet on a specific macro regime, not a generalised call that risk assets will rise. The portfolio’s internal logic, more equities, significantly more commodities, fewer bonds, depends on all three conditions holding simultaneously: growth stays durable, inflation stays manageable, and central banks stay tolerant.

The update represents an acceleration of the pro-risk direction the bank had already established in March 2026, signalling increasing conviction rather than a new thesis. The second half of 2026 will answer two questions that determine whether this positioning holds: whether growth proves durable enough to sustain corporate earnings, and whether inflation remains contained enough to keep central banks on the sideline.

For investors wanting to understand the specific risks to the central bank tolerance pillar in the weeks immediately ahead, our dedicated guide to the June 2026 central bank decisions examines how the ECB, Federal Reserve, Bank of Japan, and Bank of England all delivered policy signals within an eight-day window, including the implications of Kevin Warsh chairing his first Fed meeting and what each outcome means for rate expectations through H2 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A model portfolio allocation is a structured expression of a bank's macro convictions across asset classes, published to communicate directional views to institutional and sophisticated clients. It is not personalised financial advice but a signal of where the bank's strategists see the highest risk-adjusted return potential.

Societe Generale raised its commodities weighting by 15 percentage points in a single rebalancing, moving from 5% to 20%, which quadrupled its commodity exposure. This scale of adjustment in one quarterly update is structurally unusual for institutional model portfolios.

The portfolio rests on three simultaneous conditions: steady economic growth without recession, moderately elevated inflation that does not spiral into a severe shock, and central banks that remain tolerant rather than aggressively raising rates. If any one of these three pillars breaks, the internal logic of the allocation weakens considerably.

Societe Generale selected the equal-weight S&P 500 to reduce concentration in the largest mega-cap technology names and to position for improving market breadth, where mid-cap and non-technology sectors participate more fully in returns through H2 2026. In a cap-weighted index, five stocks currently account for roughly 23% of total index weight.

The portfolio added index-level exposure to China A-shares (targeting policy easing and depressed valuations), India NIFTY (structural growth and demographic tailwinds), Japan (corporate governance reform and supportive policy), and the FTSE 100 (value, global cyclicals, and commodity-linked sectors).