The Federal Reserve is expected to hold its benchmark interest rate unchanged at 3.75% today, but the formal decision is already priced in. The real event begins at 2:30 p.m. ET, when Kevin Warsh delivers his first press conference as Fed Chair. With consumer price inflation running at 4.2% year-over-year in May 2026, the fastest pace in three years, and a potential US-Iran peace deal already pushing crude oil prices lower, the Fed sits at an unusual inflection point. The rate hold matters far less than the signals that follow it. What Warsh says about inflation persistence, Middle East risks, and the conditions for future cuts will shape how equities, bonds, and rate expectations move for the remainder of 2026. Here is what investors need to watch.

The Fed holds at 3.75%, but this meeting is anything but routine

The Federal Open Market Committee (FOMC) is widely expected to keep the federal funds target range at 3.50%-3.75% when it announces its decision at 2:00 p.m. ET today. Markets have fully priced in the hold. Attention has shifted elsewhere.

Two variables make this particular meeting historically distinct. First, Warsh, sworn in as Chair on 22 May 2026, will face reporters for the first time in the role. Second, a live geopolitical development, a pending US-Iran memorandum of understanding, is already moving oil prices and could alter the inflation calculus the Fed has used to justify its current stance.

The press conference, not the statement, is the catalyst.

Key facts at a glance:

- Current federal funds target range: 3.50%-3.75%

- Fed Chair: Kevin Warsh (sworn in 22 May 2026)

- Decision announcement: 2:00 p.m. ET

- Press conference: 2:30 p.m. ET

- Next FOMC meeting: 28-29 July 2026

When big ASX news breaks, our subscribers know first

Why inflation and the jobs market have kept the Fed’s hands tied

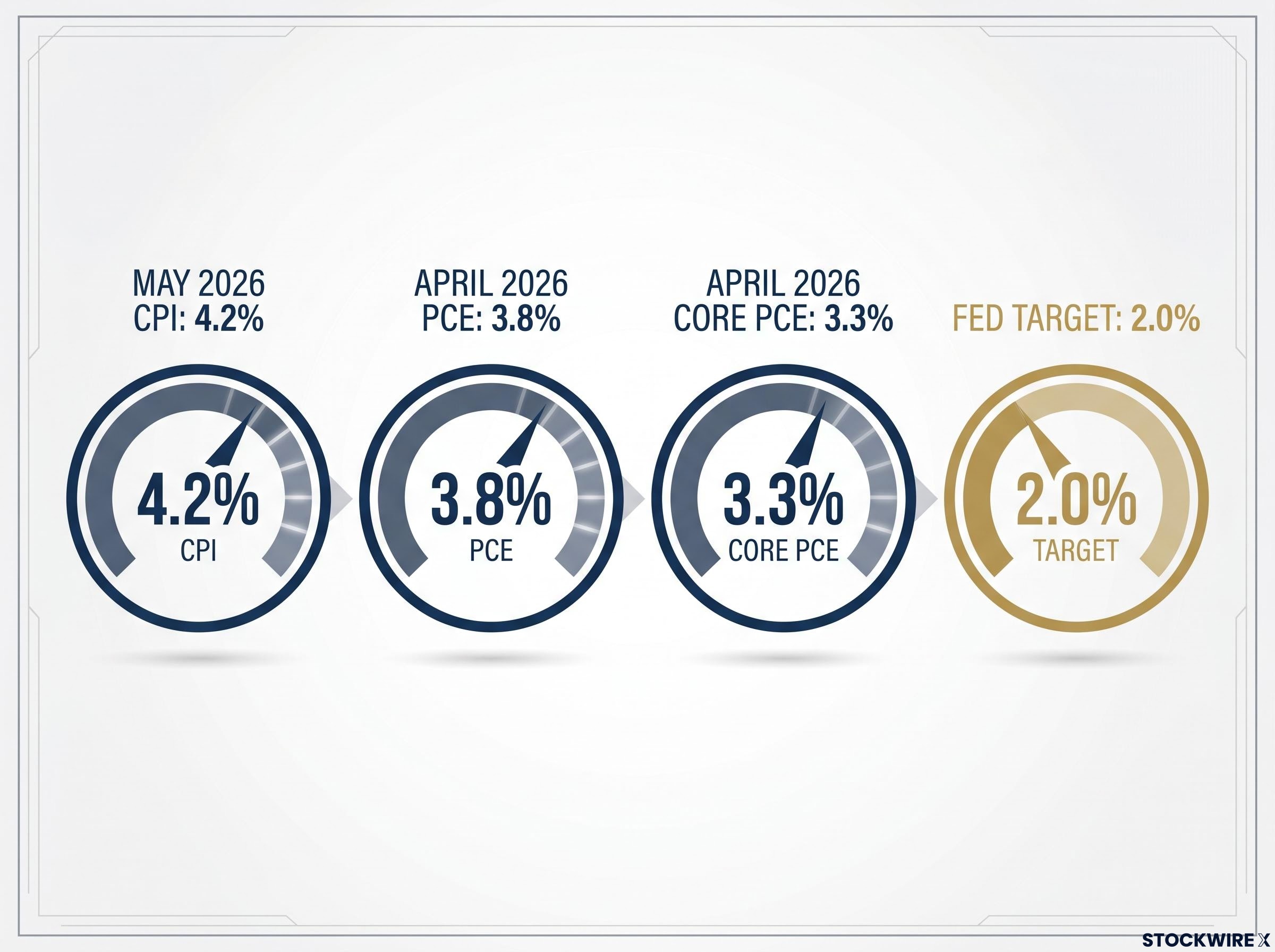

The Fed’s preferred inflation gauge, the Personal Consumption Expenditures (PCE) price index, rose 3.8% year-over-year in April 2026. Core PCE, which strips out food and energy, came in at 3.3%. The consumer price index (CPI) reached 4.2% in May 2026. By every measure, inflation is running roughly double the Fed’s 2% target.

The contrarian case against the current inflation narrative rests on the composition of the energy-driven inflation spike: Fisher Investments has noted that prices for chemical-intensive household goods actually fell roughly 0.7%, suggesting limited broad-based pass-through into the wider consumption basket, and subdued M2 money supply growth leaves firms with less room to sustain higher consumer prices than a headline CPI number implies.

The April FOMC statement explicitly cited elevated inflation driven in part by higher global energy prices and flagged developments in the Middle East as a key source of economic uncertainty.

That institutional framing is the one Warsh inherits today.

The labour market offers no urgency to cut

The unemployment rate has been little changed in recent months, and economic activity continues to expand at a solid pace. A stable labour market removes the second justification the Fed would typically need to lower rates: deteriorating employment conditions.

The result is a data environment that argues against cutting now from every angle. Inflation is too high. Employment is too stable. Each data point that might justify patience simultaneously removes the case for easing. Understanding this trap gives investors the framework to judge whether Warsh’s language today represents a genuine shift or a continuation of the current stance.

Who is Kevin Warsh, and why does his communication style matter today

Warsh is a former Fed governor who has publicly argued that the central bank should provide less explicit forward guidance about the future path of rates. His position is straightforward: detailed guidance can “tie the Fed’s hands,” constraining future decisions before the data arrives.

In practical terms, this means fewer calendar-style hints about the number of cuts in a given year, greater emphasis on each meeting being “live” and data-dependent, and a deliberate step back from the granular rate-path signalling that markets grew accustomed to under previous chairs. Investors who still expect that level of detail will be working with the wrong model.

The committee Warsh now chairs is not a unified one: the fractured FOMC at the April meeting produced four dissenting votes, the broadest internal split in years, with hawks outnumbering the lone dovish dissenter three to one, leaving Warsh to either build consensus or preside over continued division from his first press conference.

One specific metric to watch: Warsh has signalled a preference for trimmed mean PCE, which strips out extreme price moves, over headline or standard core measures. If he names it repeatedly today, it reveals how he will scorecard future progress on inflation.

Several Fed officials are already discussing the possibility of eventual rate hikes rather than cuts if inflation persists near 4%. The three questions investors should be listening for at the press conference:

- What specific metric or condition would trigger a rate cut?

- How does Warsh rank the risks: still tilted to the upside on inflation, or beginning to acknowledge balanced, two-sided risks?

- How much does he say about future meetings, and does he deviate from his stated preference for minimal forward guidance?

The Iran wildcard: how a potential peace deal changes the Fed’s calculus

A pending US-Iran memorandum of understanding, with a signing anticipated around 16-17 June 2026, is expected to reopen the Strait of Hormuz shipping corridor. The agreement has already contributed to declining crude oil prices.

The transmission mechanism runs in a single direction on inflation. Lower oil feeds into lower headline CPI, which removes one of the primary reasons the Fed has held rates at current levels. The April FOMC statement already flagged Middle East developments as a key driver of uncertainty; a durable resolution would weaken that justification considerably.

Infrastructure-specific oil pricing has replaced the broad geopolitical risk premium that dominated earlier cycles: markets now assign material risk only when the Strait of Hormuz, production facilities, or export terminals face direct physical threat, which is precisely why a durable MOU that removes that specific threat has a cleaner transmission into lower headline CPI than the general conflict backdrop would suggest.

Bank of America economist Aditya Bhave expects Warsh to make a case for patience now, while noting there could be room for cuts later in 2026 once the Iran conflict is resolved.

If Warsh explicitly connects de-escalation and lower oil to an earlier potential cut window, markets are likely to read that as a dovish tilt in the Fed’s reaction function, even if the formal statement stays cautious.

| Geopolitical Development | Likely Economic Effect |

|---|---|

| Iran MOU signed | Strait of Hormuz reopens to shipping |

| Crude oil prices decline | Headline CPI eases over following months |

| Energy-driven inflation pressure fades | Fed’s primary justification for holding weakens |

| Inflation trajectory improves | Window for rate cuts opens earlier than currently priced |

What markets are actually pricing in, and where the surprises could come from

Bonds: the 2-year yield is the cleanest signal

The 2-year Treasury yield offers the most direct real-time read on how markets are repricing Fed rate expectations. A more dovish Warsh, one who explicitly acknowledges that falling oil could accelerate progress toward 2% inflation, would push 2-year yields lower. A hawkish tone, particularly any discussion of potential hikes if inflation stays near 4%, would push them higher.

The primacy of the 2-year yield as a policy signal reflects a broader structural shift: Wolfe Research, Bloomberg Opinion, and Apollo have each concluded that bond market stress, not equity selloffs, is now the primary forcing mechanism on White House decision-making, meaning a front-end rally or selloff today carries policy implications that extend well beyond the immediate rate path repricing.

The 10-year yield will reflect how investors re-price the medium-term inflation outlook and the term premium. A scenario of lower oil combined with a Fed open to eventual cuts is consistent with bull-flattening: 2-year yields falling more than 10-year yields. TIPS breakeven inflation (the gap between nominal and inflation-protected Treasury yields) will gauge whether markets are taking the energy-driven inflation easing seriously.

Equities: rate sensitivity and the energy double hit

Rate-sensitive sectors, including REITs, utilities, and small-cap growth, stand to benefit from any dovish surprise. Energy stocks face a different dynamic: already under pressure from the prospect of lower crude, they could take a double hit if broader risk appetite improves simultaneously while their own earnings expectations compress.

Financials sit in between. Bank net interest margins depend on the shape of the yield curve. Signals of earlier cuts can flatten the curve and weigh on margins; a more hawkish Warsh who pushes out cut timing supports a steeper curve and, by extension, bank profitability.

| Asset Class | Dovish Warsh Outcome | Hawkish Warsh Outcome |

|---|---|---|

| 2-year Treasuries | Yields fall; front-end rallies | Yields rise on hike expectations |

| REITs, utilities, small-cap growth | Benefit from earlier expected cuts | Underperform on prolonged high rates |

| Energy stocks | Double pressure: lower oil plus risk rotation | Supported by higher-for-longer crude pricing |

| Financials | Curve flattens; net interest margins compress | Steeper curve supports bank profitability |

The second half of 2026 hinges on what Warsh says in the next two hours

Three variables will determine the rate path for the remainder of the year: Warsh’s communication tone, the trajectory of oil prices, and whether inflation data begins to break lower in the months ahead. Today’s press conference is where all three converge for the first time under a new Chair.

Market expectations have already shifted from pricing in cuts to contemplating possible rate hikes in late 2026 or early 2027 if inflation persists. Warsh’s language today is the primary input for recalibrating that probability. If he frames Middle East risks as two-sided and acknowledges that durable oil relief could accelerate inflation progress, the market will begin re-pricing cut expectations before the next data prints arrive.

The next FOMC meeting is 28-29 July 2026. Whatever Warsh signals today will set the conditions under which that meeting is interpreted. The most informative combination to track through and after the event: 2-year yields, oil prices, and Warsh’s language on Middle East risks. Together, they will indicate whether this hold meeting has quietly opened the door to a different rate path for the second half of the year.

Investors who understand the conditional logic of the Fed’s current posture are positioned to act on confirmed signals rather than react to noise.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding potential rate changes are speculative and subject to change based on economic data and geopolitical developments.