Why Drug Reformulation Carries Less Risk Than Investors Price in

3 hrs ago

Most retail investors who buy a single AI thematic ETF end up with accidental concentration in one narrow slice of the stack. Whether it is chips, generative AI software, or US mega-caps, a single fund leaves the rest of the AI value chain untouched. That is a structural problem, not a minor gap.

AI is now characterised by analysts as one of the most powerful structural growth trends of the current decade, underpinned by escalating capital expenditure, surging demand for compute infrastructure, and broad productivity improvements across industries. Yet the standard retail response, buying one thematic fund or waiting for a broad index to do the work, leaves meaningful exposure either unconstructed or structurally unintentional. This guide explains how to build a deliberate, layered AI ETF portfolio using four distinct allocation layers, complete with example weightings, sizing logic, overlap management, and a framework readers can scale to their own risk tolerance.

Broad global and US equity index funds do hold AI winners. The problem is that exposure is indirect, concentrated in a handful of mega-cap names, and diluted across hundreds of other holdings that have little connection to the AI build-out. A significant share of current AI-related profits sits with a small number of mega-cap firms, meaning passive index exposure is structurally thin outside those names.

A dedicated AI sleeve is not a replacement for index holdings. It is a deliberate addition on top of them. Three reasons explain why index funds alone underdeliver:

The current AI capital expenditure cycle has now surpassed every prior technology investment peak, with US IT hardware and software spending reaching a record 4.9% of GDP in Q1 2026 and combined hyperscaler commitments sitting in the $600-$805 billion range for the year, a scale that structurally underpins the case for deliberate portfolio exposure rather than passive reliance on index weights.

AI has been described as “one of the most powerful structural trends of the current decade,” supported by rising capital expenditure, growing compute demand, and productivity gains across multiple industries.

Even a modest dedicated technology ETF allocation may potentially enhance long-term returns given AI’s structural role as a growth multiplier contributing materially to global GDP over the next decade. Recognising the gap in passive exposure is the first step toward correcting it deliberately.

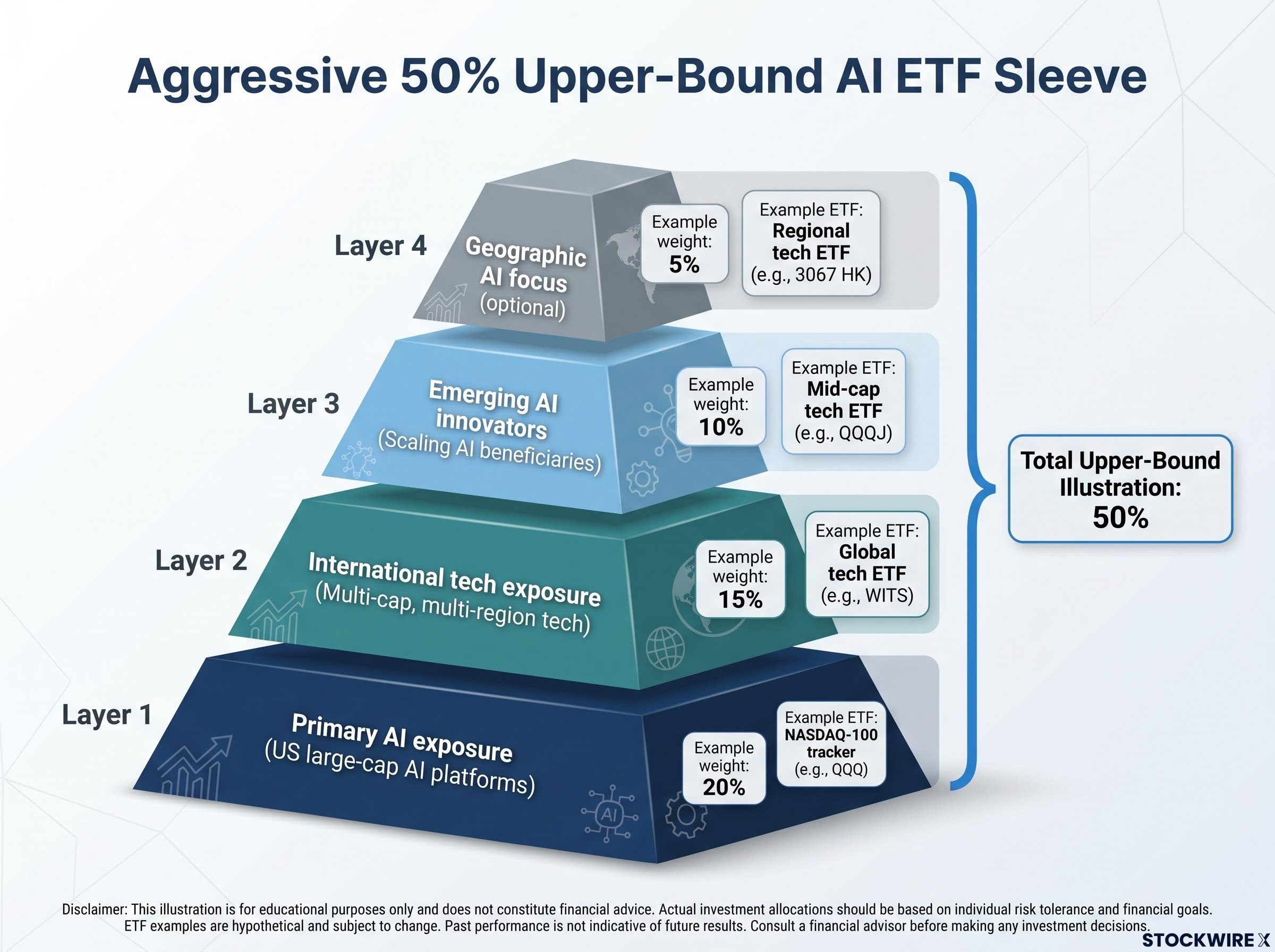

The framework below uses four layers, each with a discrete role. The example weightings assume an investor comfortable with up to 50% of their total portfolio in technology and thematic ETFs, an aggressive upper-bound case used for illustration.

Layer 1: Primary AI exposure (example weight: 20%). A NASDAQ-100 tracker or similar US large-cap tech ETF forms the foundation. It provides heavy exposure to the mega-cap platform companies integrating AI into cloud, productivity, advertising, and consumer applications. These names offer established revenues, strong balance sheets, and high liquidity. Layer 1 covers the top of the AI stack: models and software at scale. It misses non-US names, mid-cap innovators, and physical infrastructure.

Layer 2: International tech exposure (example weight: 15%). A global or multi-cap technology ETF reduces US mega-cap concentration. The AI build-out is global; Asian and European firms are active across chips, 5G, data centres, and industrial automation. A multi-cap fund deliberately includes smaller companies alongside the largest names, providing additional access to the compute and data centre layer through international chipmakers and hardware manufacturers.

Layer 3: Emerging AI innovators (example weight: 10%). A mid-cap technology ETF adds upside from earlier-stage AI beneficiaries: enterprise SaaS with native AI features, cybersecurity platforms, data analytics, and workflow automation tools. These are established companies still scaling, and a successful mid-cap compounding into large-cap status can offer more relative upside than an incremental move in a trillion-dollar name. Ultra-narrow thematic funds (pure-play robotics, quantum computing) can sit as satellites inside this layer but are not substitutes for a broader mid-cap allocation.

Layer 4: Geographic AI focus (example weight: 5%, or 0%). This layer is genuinely optional. It expresses a specific regional thesis, whether Asia, Europe, or emerging markets. Use it only with a clear, researched view on a region’s AI ecosystem, policy environment, and risk profile. Many investors should leave this layer at 0% and reallocate those points to Layers 1-3.

| Layer | Focus | ETF type example | Example weight |

|---|---|---|---|

| 1. Primary AI exposure | US large-cap AI platforms | NASDAQ-100 tracker (e.g., QQQ) | 20% |

| 2. International tech exposure | Multi-cap, multi-region tech | Global tech ETF (e.g., WITS) | 15% |

| 3. Emerging AI innovators | Scaling AI beneficiaries | Mid-cap tech ETF (e.g., QQQJ) | 10% |

| 4. Geographic AI focus (optional) | Specific regional AI thesis | Regional tech ETF (e.g., 3067 HK) | 5% |

The 50% total tech and AI sleeve shown above is an upper-bound, aggressive illustration, not a default target or recommendation for most investors. Many retail portfolios should scale all four layers down proportionally.

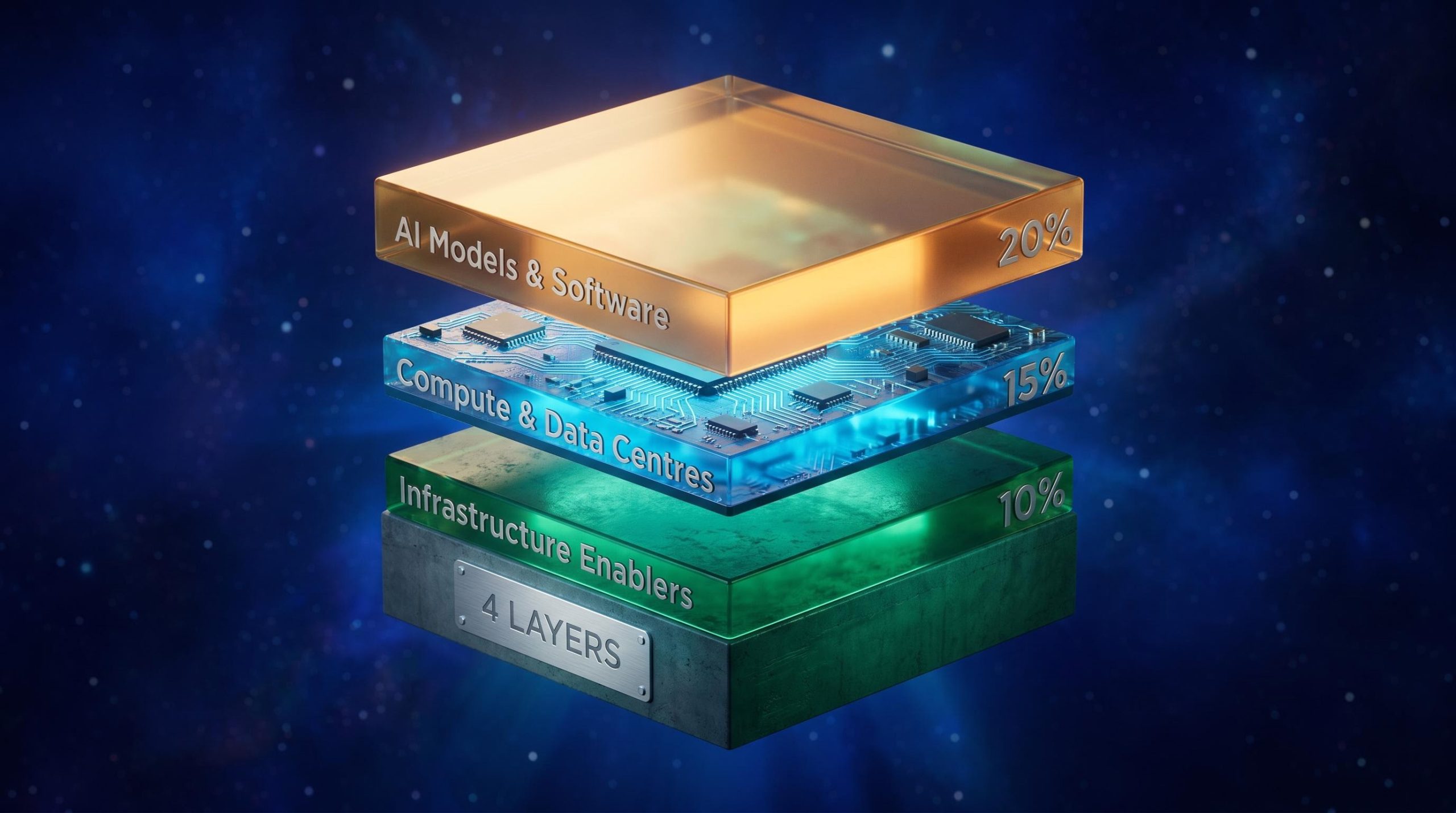

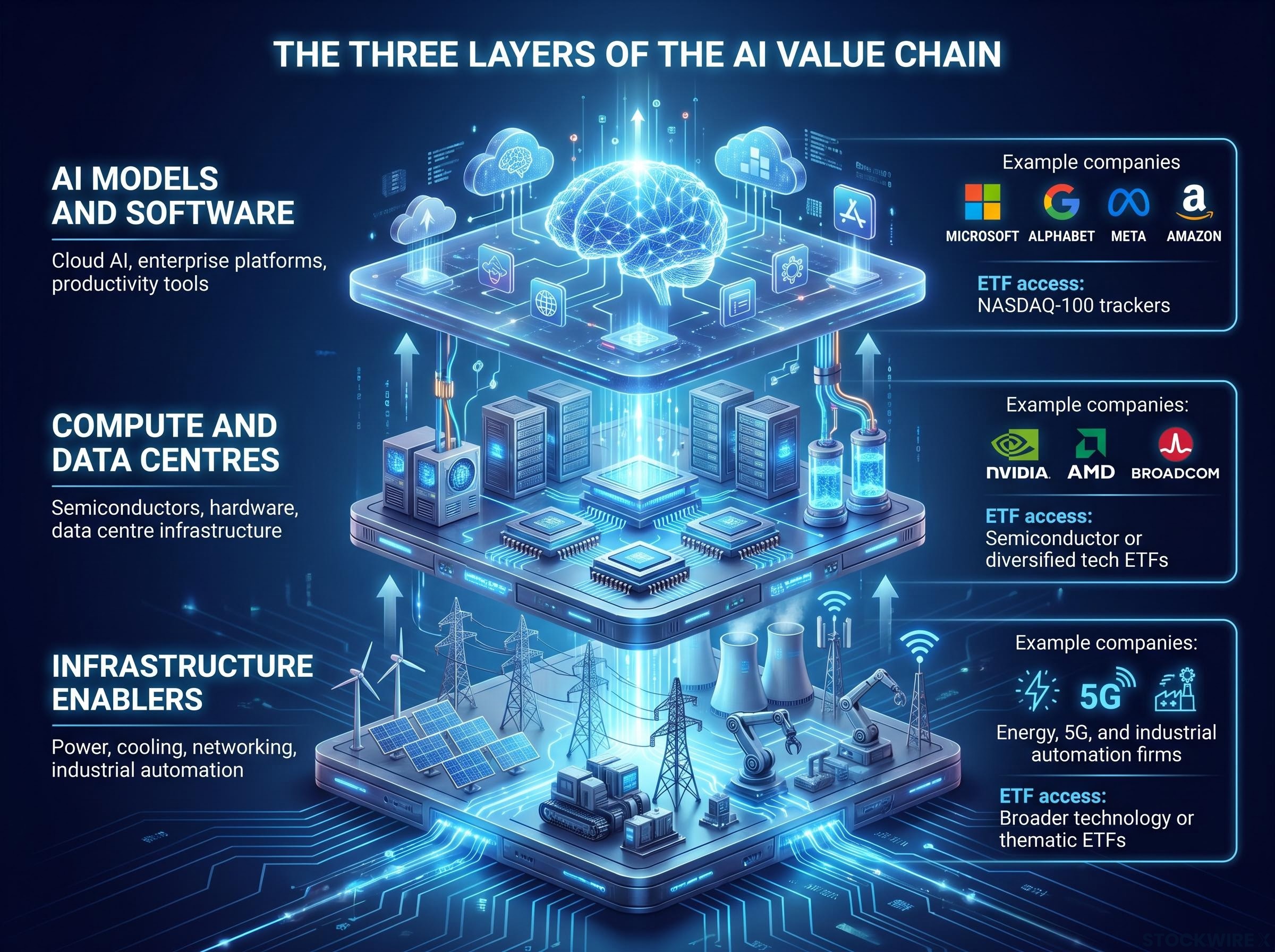

The AI economy is not a single industry. Most providers now describe it as a stack with three distinct infrastructure layers, and understanding this structure turns ETF selection from a brand choice into a structural decision.

At the top sit AI models and software: the hyperscalers and platform companies delivering cloud AI, enterprise tools, and productivity applications. Microsoft, Alphabet, Meta, and Amazon operate here, and NASDAQ-100 trackers provide the most direct access.

The middle layer covers compute and data centres: the semiconductor and hardware infrastructure powering model training and inference. NVIDIA, AMD, and Broadcom are the most prominent names, accessible through diversified or semiconductor-focused ETFs.

At the foundation sit infrastructure enablers: power generation, cooling systems, networking equipment, and industrial automation. These companies are accessible indirectly through broader technology or thematic ETFs, and they include energy, 5G, and related industrial enablers.

No single ETF captures all three layers well. Relying on one fund risks overweighting one part of the stack while leaving the others uncovered entirely.

AI supply chain profit concentration is more uneven than the value chain diagram suggests: foundries and memory producers like TSMC and SK Hynix retain structural leverage because every custom and third-party AI chip depends on the same fabrication and high-bandwidth memory ecosystem, while legacy application software multiples have compressed approximately 41% over the trailing twelve months as AI-native alternatives attract investor capital.

| Value chain layer | What it covers | Example companies | Typical ETF access |

|---|---|---|---|

| AI models and software | Cloud AI, enterprise platforms, productivity tools | Microsoft, Alphabet, Meta, Amazon | NASDAQ-100 trackers |

| Compute and data centres | Semiconductors, hardware, data centre infrastructure | NVIDIA, AMD, Broadcom | Semiconductor or diversified tech ETFs |

| Infrastructure enablers | Power, cooling, networking, industrial automation | Energy, 5G, and industrial automation firms | Broader technology or thematic ETFs |

Understanding this structure lets investors evaluate any ETF by asking which layer it covers and which it misses.

Investors who already hold broad global or US index funds already own some AI exposure through mega-cap index weights. A dedicated AI sleeve is additional concentration on top of that baseline, not a starting point from zero. Sizing it appropriately matters more than optimising for maximum return.

Many asset allocators treat thematic sleeves like AI as 5%-15% of a total portfolio, layered on top of core diversified holdings and adjusted for risk tolerance and time horizon. Most retail investors will find a total AI sleeve of 10%-30% appropriate, well below the 50% upper-bound illustration.

The sizing decision is less about return optimisation and more about personal risk calibration. Three questions help set the right target weight:

The right size for an AI sleeve is the allocation an investor can hold through volatility without selling. Oversizing a thematic allocation is one of the most common retail portfolio construction errors.

Investors wanting to stress-test their sizing assumptions against historical evidence will find our dedicated guide to the thematic ETF behaviour gap particularly instructive: it documents how ARK Innovation’s reported +233% return translated into an estimated -35% investor-experienced loss due to poorly timed inflows, and examines the Morningstar research attributing 2-3% annualised underperformance to timing alone across the thematic fund category.

AI is a long-term structural theme, not a short-term trade. Sizing should reflect a multi-year holding horizon.

Holdings overlap is the primary implementation risk. NVIDIA, Microsoft, and similar mega-caps appear across NASDAQ-100 trackers, global tech funds, and thematic AI ETFs simultaneously. Unchecked overlap undermines the diversification the layered framework is designed to provide. Reviewing ETF holdings before allocating across layers is not a one-time task; it is an ongoing responsibility as index compositions change.

A phased entry reduces timing risk. Dollar-cost averaging into the AI sleeve over several months provides natural checkpoints to reassess both the investment thesis and personal volatility tolerance before fully committing. Three steps form the implementation sequence:

Beyond implementation mechanics, five categories of risk are specific to AI-themed allocations:

The EU Artificial Intelligence Act establishes a comprehensive risk-based legal framework for AI systems operating in European markets, introducing mandatory compliance requirements for high-risk AI applications that directly affect the regulatory environment in which major AI platform companies and their investors operate.

The purpose behind this framework is disciplined, long-term structural participation in AI’s growth across the full stack, not a pursuit of short-term thematic momentum. Five principles anchor the approach:

The practical next step is straightforward: review existing portfolio holdings for current AI exposure through index funds before sizing any new dedicated sleeve. Scale the four-layer framework to personal risk tolerance, starting with a smaller total sleeve if uncertain and adding layers only as conviction and understanding grow.

Stock-level allocation within AI layers follows a separate but complementary framework, with US financial advisors recommending a 50/40/10 hardware-cloud-software split for growth portfolios targeting 20-30% total AI infrastructure exposure, a structure that maps directly onto the ETF layers described here but applies to direct equity selection for investors who want to combine ETF sleeves with individual stock positions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Allocation decisions depend on individual goals, risk tolerance, tax situation, and existing holdings.

—

A layered AI ETF portfolio divides AI exposure across four distinct allocation tiers: US large-cap tech platforms, international multi-cap technology funds, mid-cap emerging AI innovators, and an optional regional geographic focus, ensuring coverage across the full AI value chain rather than concentrating in one narrow segment.

Most retail investors are advised to target a total AI sleeve of 10%-30% of their overall portfolio, layered on top of core diversified holdings, with the 50% upper-bound figure used in illustrative frameworks representing an aggressive ceiling rather than a default recommendation.

Broad index funds deliver AI exposure indirectly through market-cap weighting, concentrating returns in a handful of mega-cap names while leaving mid-cap innovators, semiconductor equipment makers, data centre operators, and infrastructure enablers largely uncovered.

Before allocating across layers, investors should review ETF holdings for duplicate positions in names like NVIDIA and Microsoft, which commonly appear across NASDAQ-100 trackers, global tech funds, and thematic AI ETFs simultaneously, and reassess overlap periodically as index compositions change.

The five key risks are valuation risk from elevated multiples, regulatory risk from evolving AI governance and semiconductor export controls, competitive risk from rapid landscape shifts, supply-chain risk tied to semiconductor and rare earth dependencies, and geopolitical risk particularly relevant for regional ETFs with Taiwan, South Korea, or China exposure.