How the NYSE 20% Rule Protects You From Share Dilution

1 hr ago

A company with $0.3 million in cash and 1.5 million shares outstanding registered 5.1 million new shares for sale through a single equity line facility. That ratio captures why equity lines of credit have become one of the most consequential, and least understood, financing tools in small-cap markets. As of mid-2026, equity lines function as the dominant post-listing capital mechanism for small-cap issuers shut out of conventional underwritten offerings. The SEC is actively scrutinising these structures through comment letters, and retail investors in micro-cap names are routinely exposed to their dilutive effects without a clear framework for evaluating the risk. This article explains how equity lines work, how the SEC classifies and regulates them, what the registration constraints mean for capital structure, and what existing shareholders should examine before the dilution begins.

The equity line does not arrive because a board prefers it. It arrives because the alternatives have already closed.

Three structural barriers systematically exclude small-cap issuers from conventional post-listing financing:

Once these barriers are in place, the friction of repeatedly negotiating one-off PIPEs or underwritten offerings makes the ongoing, discretionary access of an equity line structurally attractive to boards and CFOs, even when the per-share costs are high.

The structural barriers that force small-cap issuers toward equity lines are not temporary market conditions; the hollowing out of small-cap capital access by private equity and venture capital has systematically removed the highest-quality companies from public markets while leaving the most capital-constrained issuers behind, a dynamic that makes unconventional financing tools more prevalent, not less, over time.

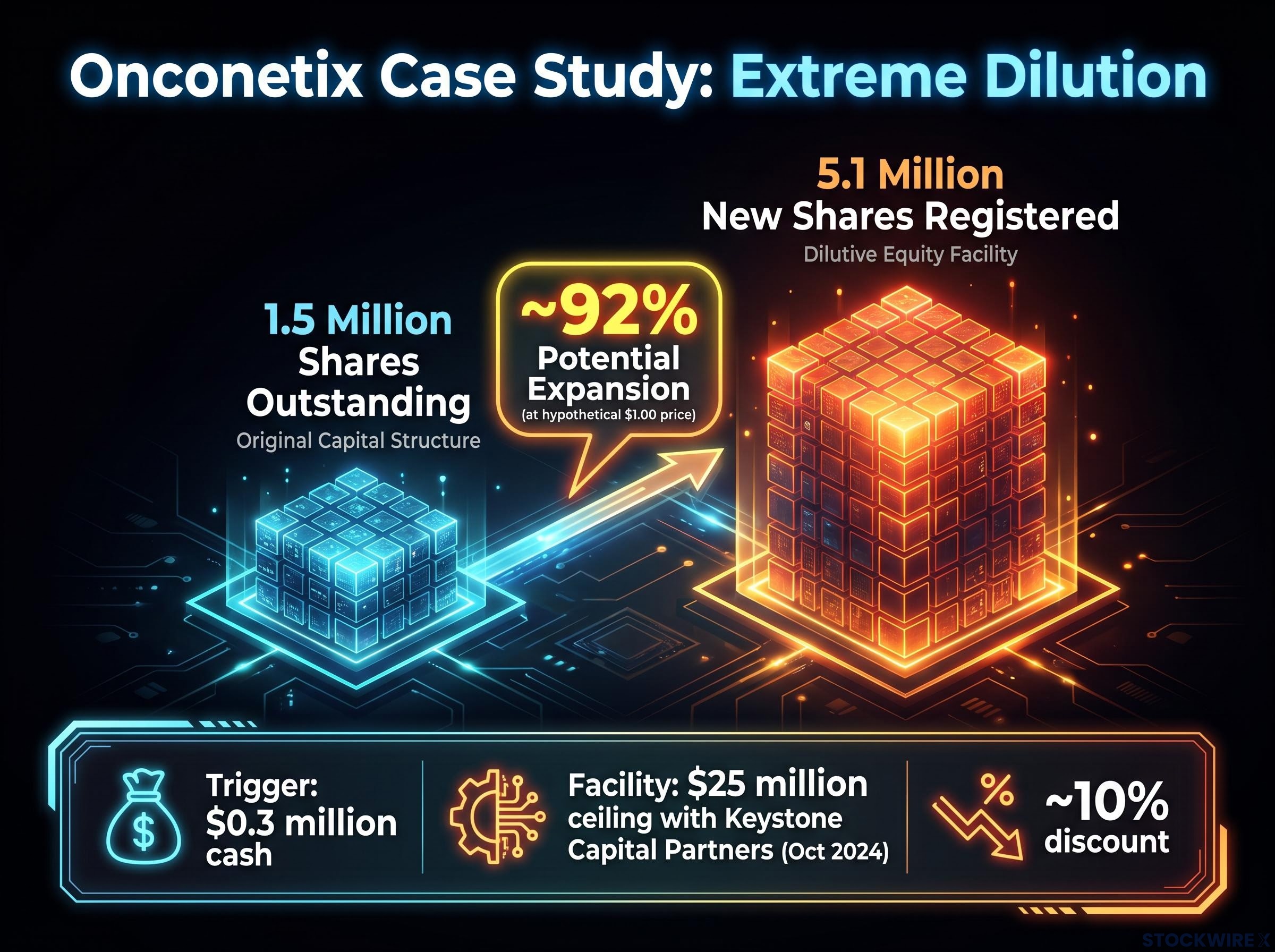

Onconetix, Inc. illustrates the endpoint. Carrying a going-concern qualification and holding approximately $0.3 million in cash, the company executed Series C, D, and E preferred placements alongside its equity line facility, layering multiple instruments because no single channel could deliver the capital needed. The equity line was not a first choice. It was the financing mechanism that remained after conventional doors had shut.

The first signal is usually a filing: a new S-1, a prospectus supplement, or an 8-K announcing a “purchase agreement” with an investor most shareholders have never heard of. Behind that filing sits a contractual arrangement with specific mechanics that determine exactly how, and at what cost, new shares enter the market.

An equity line of credit is a contractual right, not an obligation, for the issuer to sell newly issued shares to a committed investor over time, up to a predetermined dollar ceiling. The issuer controls when to draw. The investor commits to buying when called upon.

The purchase price on each draw is set at a discount to the volume-weighted average price (VWAP), the average trading price weighted by the number of shares traded at each price level, measured over a window of 1-3 trading days after the draw notice. That discount typically runs 3-6% in more standard transactions, widening to 5-15% for riskier or smaller issuers. Facility sizes generally range from $15 million to $350 million with terms of 18-36 months, per major law firm surveys, though these ranges carry a degree of variation.

Onconetix’s facility provides a concrete illustration: a $25 million ceiling, approximately 10% discount, established with Keystone Capital Partners in October 2024.

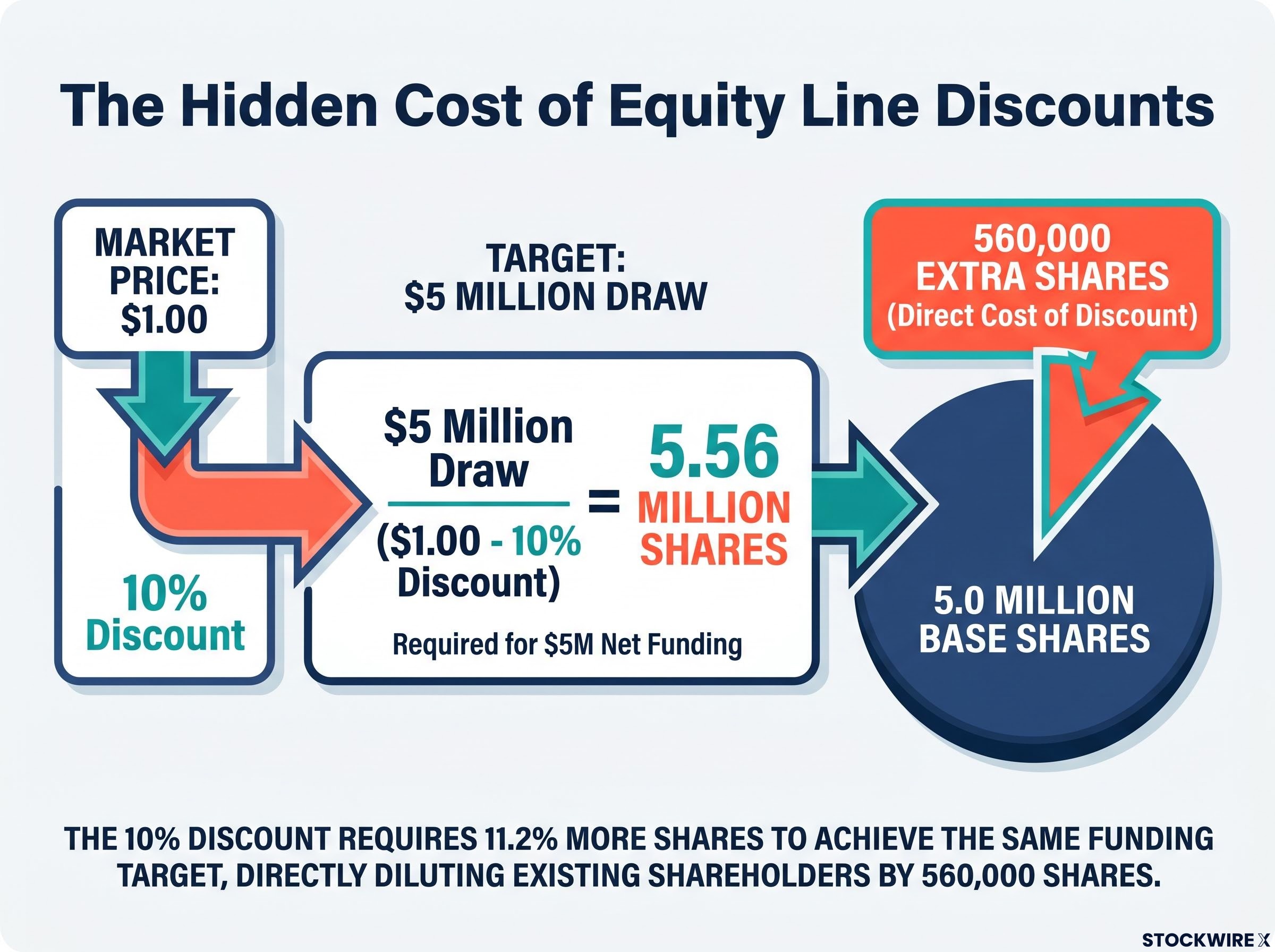

The discount creates hidden share issuance. A $5 million draw at a $1.00 market price with a 10% discount requires issuing approximately 5.56 million shares, not 5.0 million, to deliver $5 million in proceeds. The extra 560,000 shares are the direct cost of the discount.

The equity line is often compared to an ATM (at-the-market) programme, but the structural distinction matters:

That private placement step is also what creates the regulatory complexity covered next.

The SEC’s analysis of any equity line starts with a single question: is the investor an “underwriter” under Section 2(a)(11) of the Securities Act?

If yes, the transaction is not a genuine secondary resale by a shareholder. It is a primary offering, a distribution of new securities by or on behalf of the issuer, and an entirely different set of registration rules applies.

The staff’s analytical framework, reflected in Securities Act Sections C&DIs (Questions 139.12 and 139.13), evaluates several factors to determine whether the equity line investor functions as an underwriter:

SEC C&DI Questions 139.12 and 139.13 set out the staff’s interpretive framework for determining when an equity line investor crosses into underwriter territory, weighting factors such as the size of the registered block relative to float, the discount level, and whether the investor bore meaningful market risk or functioned primarily as a distribution conduit.

This is a staff interpretive position driven by comment letters and C&DIs, not explicit rule text, which means it operates through the review process rather than a bright-line statutory trigger.

In a May 2025 comment letter directed at Tivic Health Systems, Inc. (CIK No. 0001787740), SEC staff raised precisely these questions, asking whether the equity line investor should be designated as an underwriter and whether the transaction qualified as a genuine secondary offering. This is not an isolated inquiry; it is a repeat pattern in staff reviews of micro-cap equity line filings.

Onconetix took the direct approach: the company explicitly acknowledged in its filing that Keystone meets the Section 2(a)(11) underwriter definition, conceding the classification rather than contesting it.

When the SEC treats an equity line as a primary offering, the issuer faces two resolution paths. Both trace back to a February 2015 staff review of Recro Pharma, Inc.’s equity line with Aspire Capital (File No. 333-201841):

This two-path pattern has recurred consistently in SEC comment letters on oversized equity line registrations. The practical effect is that primary classification either slows the drawdown pace or reduces the facility size, directly constraining how much capital the issuer can access and how quickly.

Even after the classification question is resolved, the registration pathway itself determines how fast a company can draw on its facility.

To register an equity line as a primary shelf offering on Form S-3, an issuer must satisfy three eligibility requirements:

Issuers that clear these requirements still face a further constraint. Under Instruction I.B.6, the “baby shelf” rule, companies with a public float below $75 million may sell no more than one-third of their public float via primary shelf offerings in any rolling 12-month period.

An issuer with a $10 million public float may raise no more than approximately $3.3 million via primary shelf sales in any 12-month window.

The one-third cap applies to all primary takedowns off the S-3 combined, including ATMs, equity lines, and other shelf offerings, not each facility in isolation. The baby shelf constraint only becomes binding when the SEC classifies the equity line as a primary offering rather than a true secondary resale, which is why the classification question in the previous section carries direct economic consequences.

Many micro-cap issuers cannot use Form S-3 at all, either because they have not yet seasoned for 12 months post-IPO or because they have fallen behind in periodic reporting. Their only path is Form S-1, which is slower and subject to closer staff scrutiny.

| Form used | Key eligibility requirement | Primary shelf cap | Practical implication |

|---|---|---|---|

| S-3 (float above $75M) | 12+ months reporting, current filings | Unrestricted | Full facility access on standard timeline |

| S-3 with baby shelf (float below $75M) | 12+ months reporting, current filings | One-third of public float per 12 months | Draws capped relative to float; large facilities take years to fully utilise |

| S-1 (not S-3 eligible) | None beyond Securities Act requirements | No shelf mechanism available | Each registration reviewed individually; slower, more staff-intensive process |

The discount mechanics and the registration constraints both point toward the same question every existing shareholder faces: what does this facility actually cost me?

The answer has two distinct layers, and they are cumulative.

Layer 1 is the direct value transfer from the per-share discount. When the equity line investor pays $0.90 for stock trading at $1.00, the $0.10 per share represents economic value transferred from existing shareholders to the investor. Across millions of shares, this becomes material in aggregate. The illustrative $5 million draw at a 10% discount requires issuing approximately 5.56 million shares rather than 5.0 million, and those additional 560,000 shares are the direct cost of the discount alone.

Layer 2 is the ongoing reduction in each existing shareholder’s percentage ownership from share count expansion. Every draw expands the outstanding share base, diluting each holder’s proportional claim on the company’s equity and, in any future earnings scenario, their earnings-per-share claim. This layer operates independently of the discount and compounds with it.

Onconetix illustrates both layers at the extreme end of the spectrum. With approximately 1.5 million shares outstanding, the equity line registration covering 5.1 million shares represented approximately 92% of the company’s outstanding equity at a hypothetical $1.00 share price.

Regulatory caps, including the baby shelf limit, the 19.99% exchange cap, and the 4.99% beneficial ownership cap, do not eliminate dilution. They sequence it across time. Onconetix subsequently obtained shareholder approval to issue shares above the 19.99% threshold, confirming that the exchange cap functions as a timing gate rather than a permanent ceiling.

| Dilution layer | Mechanism | Who bears the cost | Onconetix illustration |

|---|---|---|---|

| Layer 1: Discount-driven value transfer | Investor purchases shares below market price; additional shares issued to fill the dollar amount | All existing shareholders (value transferred per share) | ~10% discount requiring ~11% more shares per draw |

| Layer 2: Ownership percentage reduction | Each draw expands outstanding share count, reducing existing holders’ proportional stake | All existing shareholders (ownership and EPS dilution) | 5.1M shares registered vs. 1.5M outstanding (~92% potential expansion) |

The facility size-to-float ratio is the single most important number to calculate first when evaluating any equity line. It determines the maximum dilution exposure before a single share is drawn.

Tracking intrinsic value per share before and after a series of equity line draws is the most direct way to measure whether the capital raised generates returns that offset the dilutive cost; a facility that funds projects with returns exceeding the discount rate used in a discounted cash flow model can be value-accretive despite the per-share discount mechanics, while one that funds cash burn without a clear return path will show permanent impairment in any rigorous valuation.

The SEC’s disclosure requirements are not bureaucratic overhead. They are the primary analytical toolkit available to retail shareholders in companies using these facilities.

The staff’s insistence on thorough disclosure, through S-1/S-3 reviews, comment letters, and mandated prospectus detail, exists so that investors can see the forward-looking dilution arithmetic and price the risk or exit the position rather than absorbing overnight capital structure changes without warning.

Five specific data points, located in the prospectus or prospectus supplement, answer the questions that matter most:

The Onconetix prospectus (Registration No. 333-290904, filed 7 November 2025 under Rule 424(b)(3)) discloses all five: the 10% discount, the 4.99% ownership cap, the 19.99% exchange cap, the underwriter designation for Keystone, and the ratio of registered shares to outstanding shares. It serves as a practical model of what complete disclosure looks like in this context.

Retail investors who know which five numbers to locate in a prospectus can assess forward-looking dilution risk in minutes rather than treating an equity line announcement as an unknowable variable.

Capital raise transparency is one of the clearest signals separating credible small-cap management teams from those that treat shareholders as a passive funding source; professional investors assess whether boards signal financing intentions well in advance, since a surprise equity line announcement at distressed prices is a planning failure that compounds the dilutive economics of the facility itself.

The equity line is not a standalone instrument. It is a product of the regulatory architecture that gives it its specific form.

The SEC’s classification framework determines whether the offering is treated as primary or secondary. The baby shelf limits cap how much capital an eligible issuer can access through a primary shelf. The exchange listing rules gate dilution at 19.99% absent shareholder approval. Together, these constraints shape the structure of every equity line facility signed today, regardless of the stated ceiling.

That architecture serves a dual function. The same guardrails that raise the cost and complexity of equity line financing are also the primary protections retail investors have against unconstrained overnight dilution. The May 2025 comment letter to Tivic Health Systems confirms that staff scrutiny of micro-cap equity lines remains active and current. The post-2020 withdrawal of certain prior C&DIs (related to Questions 139.12 and 139.13) reflects the staff’s willingness to update its interpretive framework as market practice evolves.

For distressed issuers, the equity line rarely operates alone. Onconetix’s layering of Series C, D, and E preferred placements alongside its equity line illustrates how companies deploy multiple instruments simultaneously when no single facility can meet their full capital requirements.

The instrument is defined by its constraints. Investors who understand the regulatory architecture can evaluate future equity line deals, comment letters, and prospectuses with a stable analytical framework, rather than treating each new filing as a situation without precedent.

For investors tracking how the SEC’s disclosure framework is evolving in parallel with its equity line scrutiny, our full explainer on the SEC reporting proposal covers the mechanics of the proposed quarterly-to-semiannual shift, including which issuers are eligible, what Form 8-K obligations remain intact, and why critics argue the change widens the information gap for shareholders of smaller public companies.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

An equity line of credit is a contractual arrangement giving an issuer the right to sell newly issued shares to a committed investor over time, up to a predetermined dollar ceiling, with the purchase price set at a discount to the volume-weighted average price (VWAP) measured over a short window after each draw notice.

Dilution from equity lines operates in two layers: first, the per-share discount transfers economic value from existing shareholders to the investor on every draw; second, each draw expands the total share count, reducing every existing holder's proportional ownership and earnings-per-share claim.

The baby shelf rule (Instruction I.B.6 on Form S-3) limits companies with a public float below $75 million to raising no more than one-third of their public float via primary shelf offerings in any rolling 12-month period, which can cap how quickly a small issuer draws on a large equity line facility.

Investors should locate five data points in the prospectus or prospectus supplement: the facility size ceiling, the discount percentage, the ratio of shares registered to shares currently outstanding, the exchange and ownership caps, and whether the equity line investor has been designated as an underwriter under Section 2(a)(11) of the Securities Act.

The SEC applies a multi-factor test from Securities Act C&DI Questions 139.12 and 139.13, weighing the size of the registered block relative to float, the depth of the discount, and how quickly the investor resells shares; if these factors suggest the investor is acting as a distribution conduit rather than a genuine investor, the transaction is reclassified as a primary offering with stricter registration requirements.