A small-cap company announces a private placement that could issue 18% of its shares at a 15% discount to market. No shareholder vote is scheduled. Whether that transaction is permissible depends on a set of NYSE listing rules that most retail investors have never read, yet these rules directly determine how much dilution can occur without shareholders being asked. NYSE Rules 312.03(b) and 312.03(c) govern when listed companies must seek shareholder approval before issuing new shares. For small-cap investors, these provisions represent the primary structural protection against insider-favourable or excessively dilutive capital raises proceeding without their input. The May 2026 SEC proposal to allow semiannual reporting has generated discussion about reduced compliance burdens for smaller issuers, but it does not touch these listing standards. What follows explains how the NYSE 20% rule works mechanically, when it applies, what the meaningful exceptions are, how the companion insider issuance rule operates alongside it, and what practical questions investors should ask when a small-cap company announces a new capital raise.

The problem these rules are solving

Small-cap companies listed on the NYSE have ongoing needs to raise capital after their initial listing. Each new issuance, however, dilutes existing shareholders. Without guardrails, a company could issue large blocks of shares to insiders or at steep discounts in private deals that shift value away from public shareholders, and minority investors would have no formal mechanism to object before the shares were issued.

Small-cap quality deterioration in public markets compounds the dilution risk this article addresses: as private capital absorbs the highest-quality growth companies and buyouts remove profitable incumbents, the issuers most likely to pursue repeated discounted private placements are disproportionately concentrated in what remains of the public small-cap universe.

NYSE listing standards, not SEC disclosure rules, are the mechanism that requires shareholder input on the most consequential of these transactions. The distinction matters:

- NYSE listing standards (Rules 312.03(b) and 312.03(c)) govern when a company must obtain a shareholder vote before issuing new equity. They are enforced by the exchange as a condition of continued listing.

- SEC reporting rules (Forms 10-Q, 10-K, 8-K) govern how and when a company discloses financial information to the public.

- These are independent regulatory regimes. Changes to one do not modify the other.

Investors who understand what these rules are designed to prevent are better positioned to interpret a capital raise announcement and identify when a company’s claimed exception deserves scrutiny.

When big ASX news breaks, our subscribers know first

How the NYSE 20% rule actually works

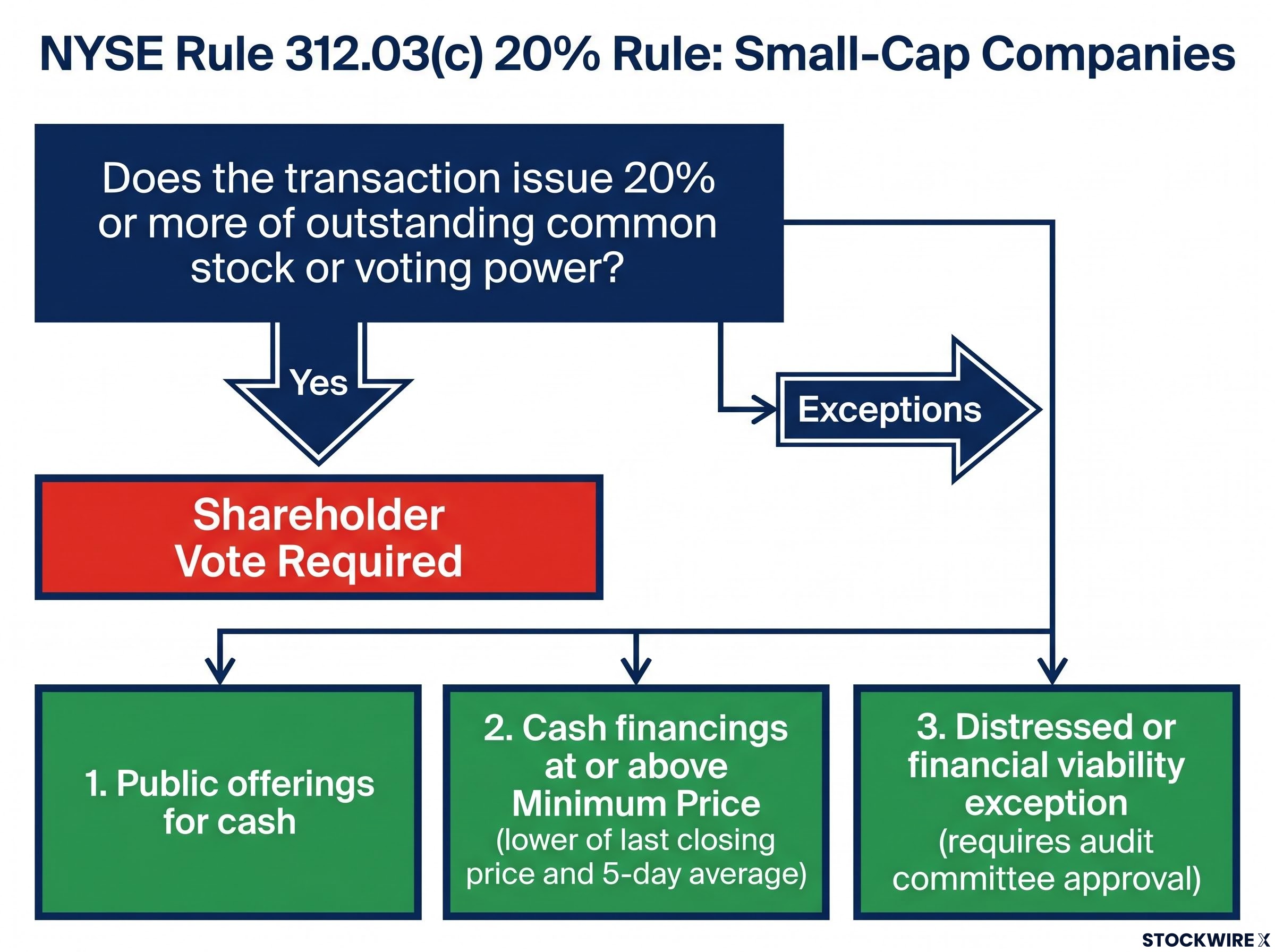

When a small-cap company files an 8-K disclosing a private placement, the first number to check is how many shares the deal could put into the market relative to what is already outstanding. That ratio determines whether NYSE Rule 312.03(c) applies.

The baseline rule: shareholder approval is generally required when a transaction, or series of related transactions, could result in the issuance of 20% or more of outstanding common stock or voting power, measured before the deal.

Three categories of exception exist where the protective trigger does not apply, even above the 20% threshold:

- Public offerings for cash. Firm-commitment underwritten follow-ons or broadly distributed shelf takedowns for cash are generally exempt regardless of size.

- Cash financings priced at or above the Minimum Price. Private placements for cash that are priced at or above the Minimum Price, defined as the lower of the last closing price and the five-day average prior to signing, do not require a vote. Each draw must satisfy this pricing condition independently.

- Distressed or financial viability exception. In narrow situations where delay would seriously jeopardise the company’s financial viability and the audit committee approves reliance on the exception, NYSE may permit a 20%+ issuance without prior shareholder approval.

The 2019 and 2021 amendments replaced the prior “bona fide private financing” construct with this current Minimum Price framework.

“Under NYSE Rule 312.03(c), shareholder approval is generally required for private financings that could result in the issuance of 20% or more of the company’s outstanding common stock or voting power, unless the deal is a public offering for cash or a cash financing priced at or above the Minimum Price.”

After accounting for these exceptions, the transactions that actually require a shareholder vote tend to be large, discounted private placements. Understanding the exceptions is as important as understanding the rule itself: when a company says no vote is required on a large private placement, it is claiming one of these exceptions, and investors can evaluate whether that claim holds up.

| Transaction Type | Shareholder Vote Required | Key Condition |

|---|---|---|

| Public offering for cash | No | Broadly distributed for cash |

| Cash private placement at or above Minimum Price | No | Pricing condition must be met independently per draw |

| Large discounted private placement | Yes | 20%+ of outstanding shares and no exception applies |

| Distressed exception | No | Narrow; requires audit committee approval |

The insider issuance rule that sits alongside it

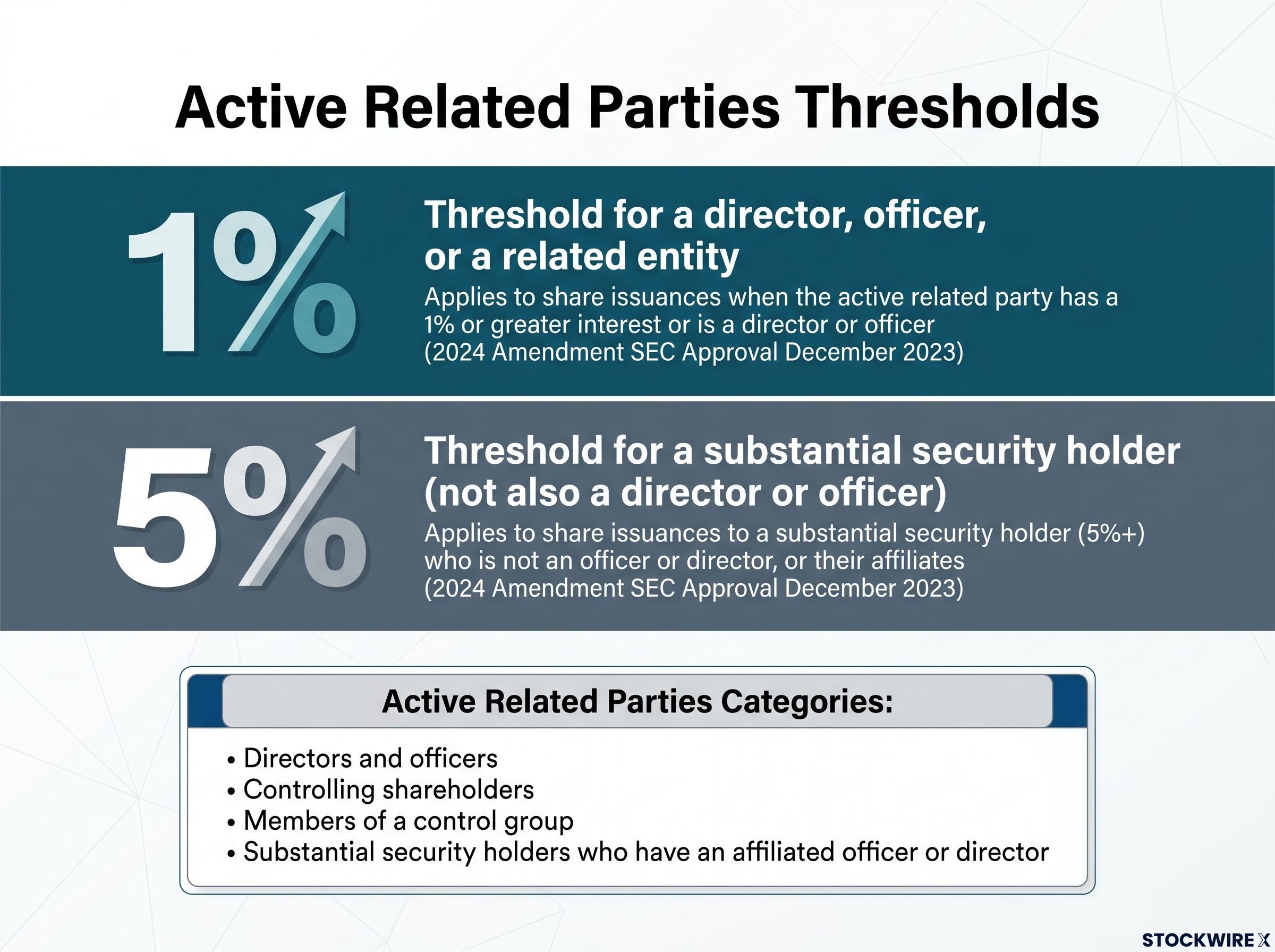

The 20% threshold is a size-based trigger. NYSE Section 312.03(b) operates on a different axis entirely: it is triggered not by deal size but by who is buying. Even a small transaction can require a shareholder vote if the right parties are involved.

Section 312.03(b) focuses on Related Parties, including directors, officers, and certain substantial security holders. Two thresholds apply:

- 1% of outstanding common stock or voting power if the purchaser is a director, officer, or a related entity

- 5% if the purchaser is only a substantial security holder (not also a director or officer)

A financing that looks too small to trigger the 20% rule may still require a shareholder vote under Section 312.03(b) if an insider is participating. This is especially relevant for closely held small-cap companies where management stakes tend to be larger.

Who counts as an Active Related Party after the 2024 amendment

Following the 2024 amendment (SEC approval in December 2023), Section 312.03(b)(i) applies specifically to “Active Related Parties.” The categories include:

- Directors and officers

- Controlling shareholders

- Members of a control group

- Substantial security holders who have an affiliated officer or director

Passive 5%+ holders with no board or officer affiliation are excluded from this particular requirement under the amended rule, though other NYSE rules may still apply to them.

How aggregation works across multiple transactions

NYSE evaluates related transactions as a series when assessing whether the 1% or 5% threshold is crossed. If a Related Party participates in multiple closely related raises, those participations are not always treated independently.

Small insider pieces across a sequence of financings can be aggregated. Investors reviewing a capital raise should check whether the current transaction is part of a series involving the same Related Party.

How companies structure around these rules and what that means for dilution

Small-cap issuers often cannot access conventional underwritten follow-on offerings. Underwriter interest is limited for smaller names. At-the-market (ATM) programmes require Form S-3 eligibility, which includes a minimum public float of $75 million, a threshold many micro-cap issuers cannot satisfy. Best-efforts placement agents, who earn fees without committing their own capital, become the realistic alternative.

The result is a capital programme assembled from multiple instruments rather than a single large transaction.

Why serial structures emerge from eligibility constraints

A typical multi-instrument small-cap capital programme might proceed in stages:

- Initial equity line of credit (ELOC): periodic draws at or near market price, providing baseline liquidity

- Series C or D preferred private placement: a larger block sold to institutional or strategic investors, often at a discount

- Convertible note issuance: debt that converts to equity under specified conditions, frequently with floating conversion prices or reset provisions

- Registered direct or PIPE: a follow-on equity raise placed with a smaller group of investors, typically below market

Each individual draw or round may fall below the 20% threshold independently. The cumulative potential dilution across the full programme, however, can be substantially larger.

NYSE evaluates “a transaction or series of related transactions” for purposes of the 20% test. Interdependent or structured-together tranches can be aggregated. Genuinely separate transactions, such as periodic at-market draws from an equity line that are each independently priced and not conditioned on one another, are often viewed as distinct.

Why the cumulative picture matters more than any single announcement

Total dilution exposure in a small-cap investment is rarely visible from any single deal announcement. It requires tracking the cumulative programme across multiple quarters and instruments.

Conversion terms deserve particular attention. Ratchets, reset provisions, and floating conversion prices can increase actual future share issuance beyond the initial disclosed figures. Investors should review recent 8-K filings and periodic reports for prior preferred placements, PIPEs, registered directs, convertible notes, and equity lines to assess the aggregate picture.

What the May 2026 SEC reporting proposal does and does not change

On 5 May 2026, the SEC issued a proposed rule (Release Nos. 33-11414; 34-105368, File No. S7-2026-15) that would permit eligible issuers to substitute a semiannual Form 10-S for the current quarterly Form 10-Q. As of 16 June 2026, this proposal has not been adopted; it remains in proposed form.

If adopted, the practical effect would be reduced administrative burden for smaller issuers on reporting frequency. It would not modify NYSE listing standards or the shareholder approval requirements under Section 312.03.

The SEC proposed rule on semiannual reporting, designated Release Nos. 33-11414 and 34-105368 under File No. S7-2026-15, confirms that the proposal targets reporting frequency for eligible smaller issuers and does not amend the exchange listing standards that govern shareholder approval thresholds.

“Changes to SEC reporting frequency may reduce the compliance burden for small-cap issuers, but they do not modify NYSE’s shareholder-approval rules. Those listing standards continue to govern when a company must seek shareholder approval before completing certain dilutive issuances.”

The regulatory boundary is worth drawing clearly: SEC periodic reporting requirements and NYSE listing standards are independent regimes. NYSE Rules 312.03(b) and 312.03(c) remain operative and unchanged by the SEC proposal.

Nasdaq listing standards operate on a parallel but distinct framework, with the exchange’s recent MVUPHS float threshold changes illustrating how exchange-level rules can reshape capital raise mechanics independently of SEC disclosure requirements, the same regulatory separation this article describes for NYSE Rule 312.03.

For investors, this distinction carries a practical implication. Less frequent periodic reporting, if adopted, may actually require more active monitoring of 8-K filings to track dilution events in real time, since quarterly reports would no longer provide a regular checkpoint.

Four questions to ask before a small-cap company raises capital

The rules covered above can be distilled into a practical checklist. When a small-cap company announces a new capital raise, four questions map directly to the applicable thresholds and protections.

- Are insiders or Active Related Parties participating?

- Identify whether directors, officers, or Active Related Parties are buying in the deal

- Check if the issuance exceeds 1% of outstanding common stock or voting power (for directors and officers) or 5% (for substantial security holders without officer or director affiliation)

- Determine whether this transaction is part of a series with the same Related Party, which could trigger aggregation

Small-cap management evaluation frameworks treat a surprise discounted raise as a transparency failure rather than a market event, and credible teams are expected to signal capital needs roughly twelve months in advance rather than presenting shareholders with a fait accompli.

- How large is the issuance and at what effective price?

- Calculate whether the deal could issue 20%+ of outstanding shares or voting power

- If yes, identify which exception the company is claiming: public offering for cash, cash financing at or above the Minimum Price, or distressed or financial viability exception

- Assess whether the claimed exception is supportable based on the deal terms disclosed

- What is the total cumulative dilution across the full capital programme?

- Review recent 8-K filings and periodic reports for prior preferred placements, PIPEs, registered directs, convertible notes, and equity lines

- Calculate total potential share issuance across all instruments, not just the latest round

- Examine conversion terms for ratchets, reset provisions, or floating conversion prices that could increase future dilution beyond initial disclosed figures

- If a shareholder vote is required, what does the proxy disclose?

- Look for full terms of the securities being issued, dilution tables, board rationale, and conflicts of interest analysis

- If a vote appears required but no proxy is forthcoming, that warrants direct scrutiny of whether the company has correctly applied the applicable rules and exceptions

- The proxy is the document where investors find the information needed to make an informed hold or exit decision before new shares hit the market

NYSE’s shareholder approval rules are not a technicality

The NYSE 20% rule and the Section 312.03(b) insider issuance rule are practical investor protection tools, not regulatory formalities. The 20% threshold triggers on size and discount. The insider rule triggers on identity at much lower thresholds. The cumulative picture across a multi-instrument capital programme is where total dilution exposure lives.

As the SEC’s semiannual reporting proposal moves through the comment process, the rules governing when investors get a vote on dilutive capital raises remain intact. Familiarity with them is a durable analytical advantage for any investor holding small-cap names on the NYSE.

NYSE Listed Company Manual Section 312.03 sets out the full text of the shareholder approval requirements, including the specific language governing the Minimum Price definition, the distressed exception criteria, and the Active Related Party categories that were revised by the 2024 amendment.

Investors seeking the current rule text can review the NYSE Listed Company Manual, Section 312.03, directly. When a shareholder vote on a capital raise is scheduled, the proxy statement is the single most important document to read before casting a vote or making a portfolio decision.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.