SpaceX IPO Hits $3 Trillion Market Cap in 72 Hours

9 mins ago

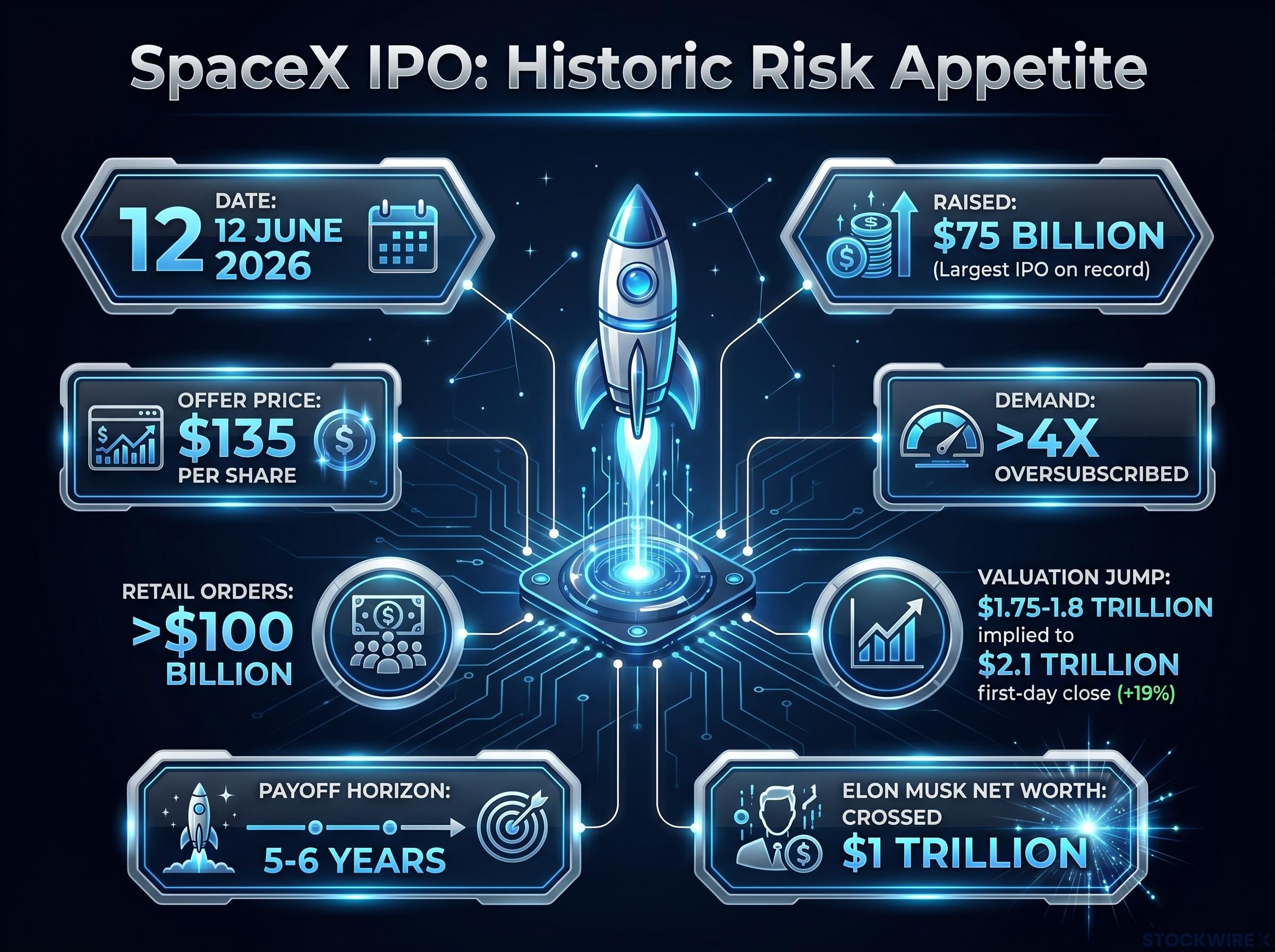

The largest initial public offering in history closed last week, more than four times oversubscribed, with retail investors alone submitting over $100 billion in orders for a company whose projected payoff remains five to six years away under optimistic assumptions. SpaceX listed on 12 June 2026, but the event did not happen in isolation. It crystallised something that has been building across markets for months: capital is piling into frontier technology at prices that require extraordinary things to go right, for a long time, before investors get paid back. For Australian investors with index exposure or thematic allocations, the implications run deeper than a single headline. This analysis separates the technological case for AI from the valuation case, examines the structural mechanics pushing prices away from fundamentals, and maps the specific sectors and conditions where disciplined, fundamentals-driven investors are finding genuine margin of safety right now.

The raw numbers deserve a moment on their own:

The oversubscription data carries most of the analytical weight here. Retail investors collectively submitted enough orders to fill the offering more than once over, for a business whose monetisation timeline stretches to the end of the decade. Institutional demand added multiples on top. That level of demand, at that valuation, for that payoff horizon, is a statement about where risk appetite sits in mid-2026.

The IPO arrived into a market already carrying significant baggage: sell-side consensus forecasts for technology growth had climbed above independent industry-level estimates, and the BofA Global Fund Manager Survey showed global managers most overweight US technology since before the 2021 peak, both conditions associated with stretched tech market valuations that leave little room for disappointment.

Michael Malseed, Head of Institutional Portfolio Management at Morningstar Investment Management, characterised the IPO as an “accelerant” to risk appetite around frontier technology.

The 19% first-day gain and the trillionaire milestone are vivid. They are not, by themselves, evidence that the entry price was right. What they confirm is that the market’s willingness to absorb risk at demanding valuations remains extraordinarily high, and that willingness is shaping the price of every AI-adjacent name in global indices, including those embedded in Australian superannuation and diversified portfolios.

AI’s technological significance is not the question under examination here. The question is narrower and more consequential for investors: do current prices reflect a realistic estimate of intrinsic value, or do they reflect narrative enthusiasm that has outrun the underlying economics?

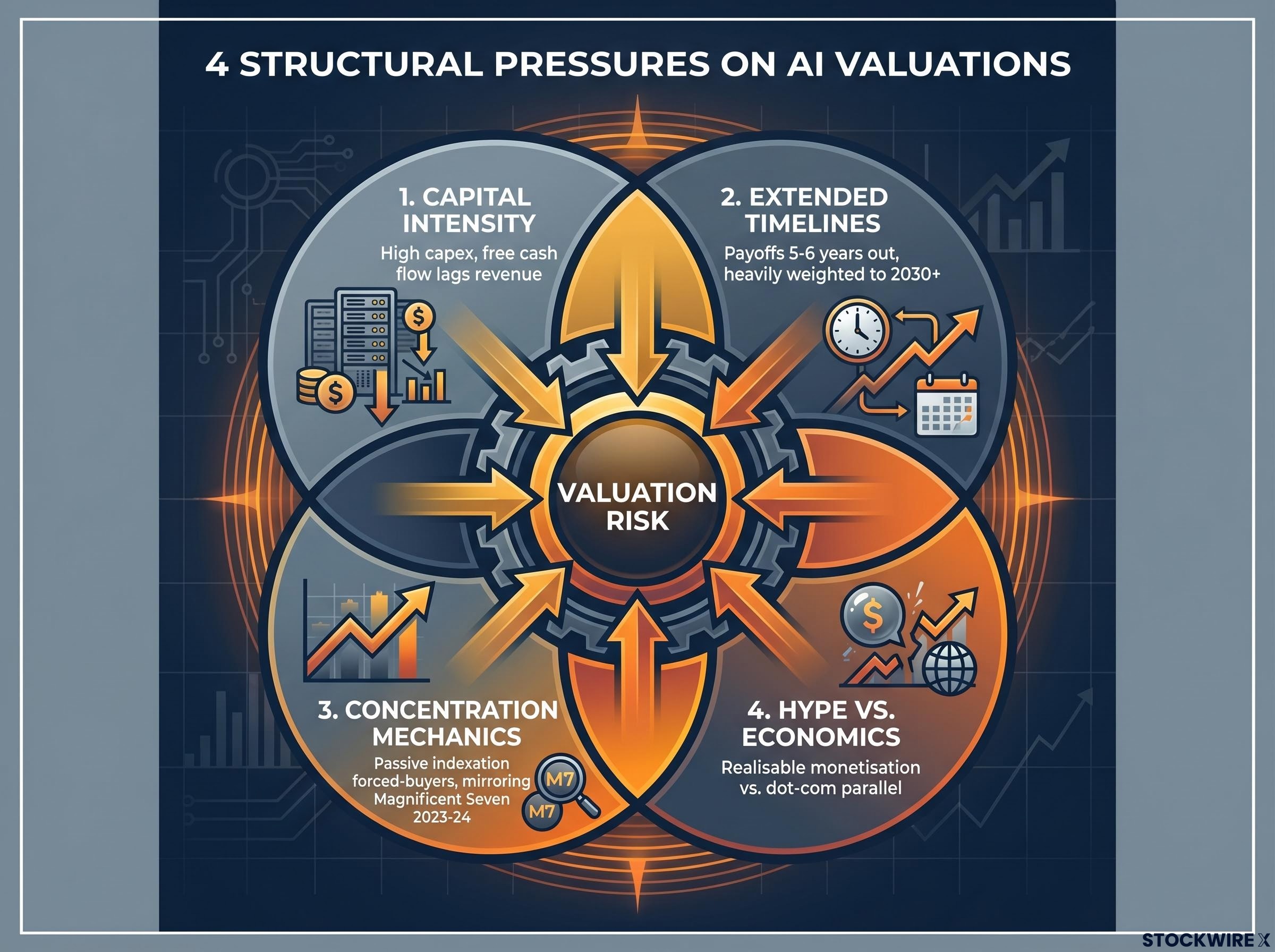

The answer involves four compounding structural pressures, and the important word is “compounding.” Each one would strain valuations independently. Together, they create a problem that is mechanical, not merely sentimental.

The problem is compounded by the way passive vehicles obscure the underlying exposure: low index-level volatility across AI-heavy benchmarks masks a distributional divergence where large opposing moves by individual winners and losers cancel each other out, leaving investors carrying index concentration risk that appears diversified at the benchmark level but is highly concentrated at the company level.

The dot-com parallel deserves precision. It was not a technology failure. It was a pricing failure. The same risk applies to AI exposure today, and the structural pressures listed above make that risk self-reinforcing rather than self-correcting.

Margin of safety, in operational terms, is the gap between an asset’s intrinsic value and the price the market is currently asking. It is not an abstract concept. It is a practical filter that changes shape depending on the type of business being evaluated.

The framing shift that underpins this entire analysis is definitional: value investors do not treat volatility as the primary measure of risk, they treat the probability of permanent capital loss as the governing variable, and that distinction changes which businesses look safe and which look dangerous at any given point in the market cycle.

Consider two risk profiles side by side. In the first, an investor pays a price where everything must go right, across multiple years of capital-intensive buildout, to justify the entry valuation. Revenue must scale on schedule, competition must remain manageable, and interest rates must stay accommodating. In the second, the investor pays a price for a business generating real cash flows today, where the uncertainty is about the growth rate of those cash flows, not their existence.

The difference between those two profiles is the margin of safety in practice. When AI enthusiasm compresses that margin across an unusually broad swath of the market, the distinction becomes directly relevant to portfolio construction.

This is not a case for avoiding AI entirely; it is a case for separating belief in the technology from willingness to pay any price.

According to Malseed at Morningstar Investment Management, stock-specific opportunities remain identifiable through fundamental analysis even at elevated broad market valuations. The sectors where those opportunities are concentrating share a common feature: known risks that are visible, bounded, and already reflected in the price, rather than speculative risks that are assumed away.

The analytical logic is consistent across all three categories below: when a single theme dominates flows, anything outside the story is often sold or ignored indiscriminately. That indiscriminate repricing is precisely where fundamental analysis tends to find value.

| Sector | Key Valuation Appeal | Primary Risk to Monitor |

|---|---|---|

| Healthcare | Defensive cash flows, regulatory moats, demand resilience; known risks (patent cliffs, reimbursement pressure) already priced in | Regulatory changes, pipeline failures, reimbursement compression |

| Consumer Staples / Quality Brands | Established cash flows at fair multiples, higher dividend yields; uncertainty centres on growth rate, not viability | Input-cost inflation, private-label competition, shifting consumer preferences |

| Oversold Non-AI Software | Names down 40-50% on AI displacement fears that may overstate the realistic threat; structural customer stickiness | Actual AI substitution proving faster or broader than expected |

Healthcare offers defensive cash flows without an AI premium baked into the price. Demand is relatively insensitive to the economic cycle. Regulatory moats in specialty drugs, medical devices, and diagnostics provide durable pricing power. The risks, patent cliffs and reimbursement pressure, are well understood and already reflected in valuations. Analysts have characterised the sector as offering reasonable multiples relative to growth and balance-sheet quality.

Consumer staples and quality discretionary names present a similar structural advantage. Investors are paid to own established, ongoing cash flows. The entry price does not require five to six years of flawless execution to be justified. Uncertainty centres on the growth rate of those cash flows, not on whether they exist at all.

Several software companies were substantially sold off in early 2026 on fears that AI could fully displace their business models, with some names declining 40-50%. The valuation error embedded in those selloffs is treating AI disruption as binary: if AI can, in principle, do what a software product does, the incumbent is priced as if displacement is immediate and total.

The realistic path is typically partial and gradual. Enterprise software is structurally sticky for three reasons: switching costs are high, compliance and security constraints slow wholesale technology replacement, and incumbent vendors can embed AI into their own products, blunting the threat from AI-native competitors.

The margin-of-safety test for these names is specific. If a stock is down 40-50% on AI fears, is the market pricing moderate disruption over a multi-year horizon, or existential displacement? The analytical work required involves assessing depth of customer dependence, mapping realistic AI adoption timelines for competing tools, and evaluating the incumbent’s own AI integration capability. Where that analysis shows worst-case outcomes extrapolated too quickly, the gap between price and intrinsic value may represent genuine opportunity.

The goal is not to exit AI. It is to avoid unwitting overexposure via passive vehicles that make investors forced-buyers regardless of valuation. Analysts and institutional allocators are operating across four practical dimensions:

APRA’s SPS 530 investment governance standard requires superannuation trustees to conduct annual stress testing and maintain documented concentration risk limits, obligations that become directly relevant when cap-weighted index allocations silently accumulate large exposures to a single thematic sector like AI-adjacent mega-caps.

According to Malseed, focusing on fundamentally sound businesses that have been overlooked is the preferred orientation for cautious institutional allocators. For Australian investors in diversified funds or with direct equity exposure, this framework serves as a practical audit of whether a portfolio is implicitly positioned on AI outcomes that may not have been explicitly chosen.

For Australian investors deciding how to implement a valuation-aware tilt within their existing portfolios, our deep-dive into AI exposure on the ASX examines how market-cap-weighted ETFs compare to individual stock selection across the dot-com cycle and the current AI wave, including concentration data for the NDQ and IVV funds that most superannuation and diversified portfolios already hold.

The SpaceX IPO landed with a $2.1 trillion first-day market capitalisation, a 19% gain, and the creation of the world’s first trillionaire. The demand was real. The technology is real. Those facts are entirely compatible with the entry price being wrong for long-term investors.

For long-term returns, what an investor pays matters as much as what they own. The margin between those two numbers is where returns are made or lost. In a market where a single thematic bet dominates flows and compresses valuations everywhere else, the disciplined response is not enthusiasm or anxiety. It is precision: company-specific analysis focused on cash flows and realistic timelines, applied to every holding regardless of narrative appeal.

Separating belief in the technology from willingness to pay any price is the distinction that defines this market cycle. For Australian investors, the sectors left behind by AI enthusiasm may be where genuine margin of safety is quietly accumulating.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The AI valuation problem refers to the structural gap between current prices of AI-adjacent stocks and their realistic intrinsic value, driven by extended earnings timelines, high capital intensity, index concentration mechanics, and monetisation uncertainty. It matters because investors in cap-weighted index funds may be unknowingly overexposed to these stretched valuations without having explicitly chosen that risk.

Cap-weighted index funds make passive investors structural forced-buyers of AI-adjacent mega-caps regardless of valuation, creating a feedback loop where flows chase performance and multiples rise. Low benchmark-level volatility can mask the fact that large opposing moves by individual holdings cancel each other out, leaving portfolios highly concentrated at the company level even when they appear diversified.

Healthcare, consumer staples, and select oversold non-AI software companies are identified as sectors where known risks are already reflected in prices and cash flows are real today. Some software names declined 40-50% in early 2026 on AI displacement fears that analysts argue overstate the immediate threat, potentially creating a gap between price and intrinsic value.

The dot-com collapse was not a technology failure but a pricing failure: the internet proved transformative, yet early investors suffered severe capital losses because monetisation arrived later and was distributed more narrowly than prices implied. The same structural risk applies to AI today, where payoff timelines of five to six years under optimistic assumptions place most valuation weight on assumptions about 2030 and beyond.

Investors can audit their cap-weighted index exposure to identify hidden AI mega-cap concentration, rebalance toward fundamentals-driven sectors like healthcare and consumer staples, and conduct stock-specific cash flow modelling under less optimistic scenarios. APRA's SPS 530 standard also requires superannuation trustees to stress test and document concentration risk limits, making this audit a regulatory as well as financial priority.