What Equity Lines of Credit Actually Cost Small-Cap Investors

7 hrs ago

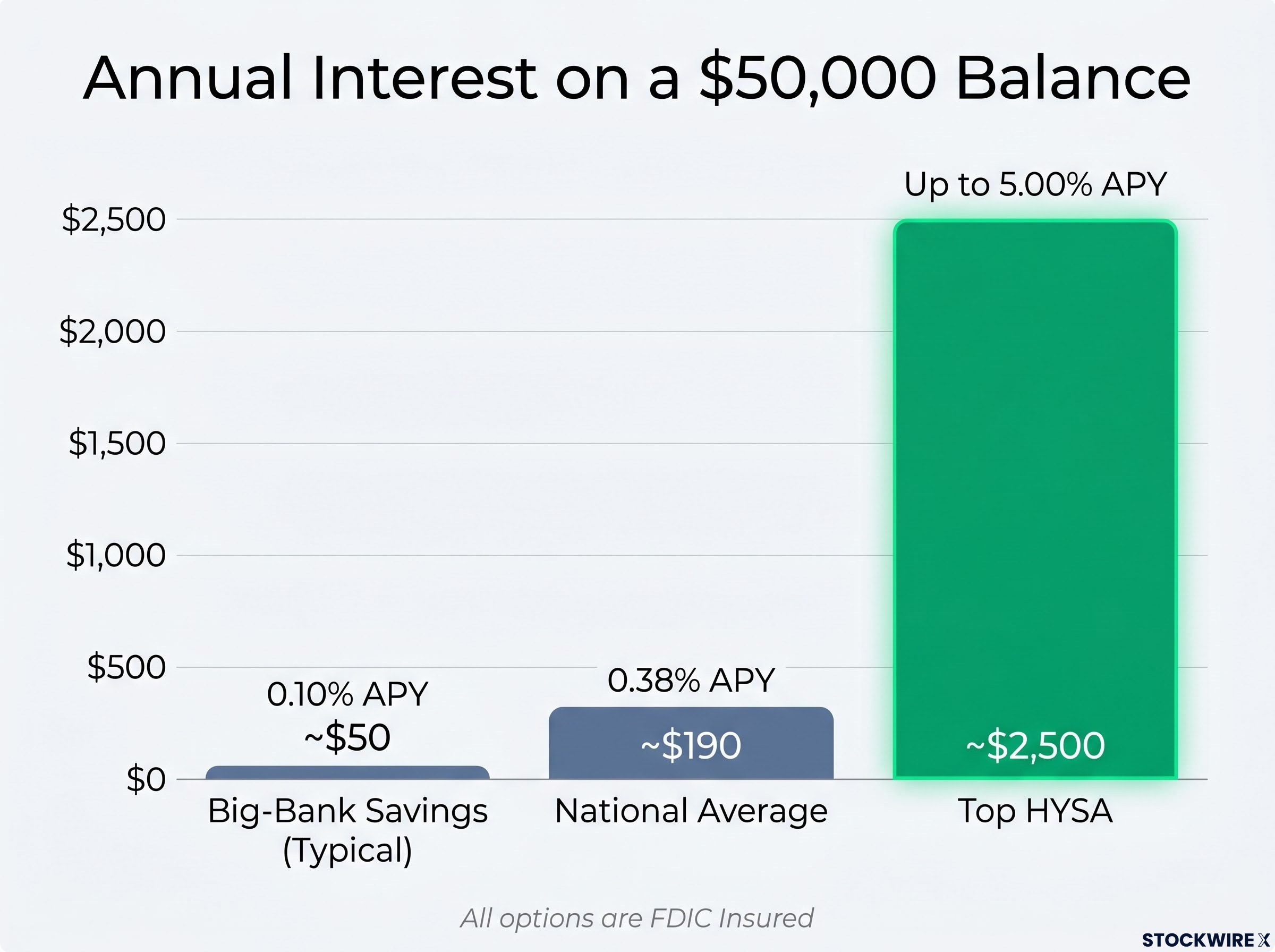

On a $50,000 balance, the typical big-bank savings account pays roughly $50 a year in interest. Moving that same cash into a Treasury bill or a top high-yield savings account currently pays more than $1,800 to $2,500 a year, with identical or stronger government backing behind every dollar.

In mid-2026, the gap between what major U.S. banks pay on standard savings accounts (as low as 0.01-0.25%) and what equally safe alternatives offer has never been more visible, or more expensive to ignore. The spread is not a minor rounding difference. Over a few years, it represents thousands of dollars in foregone income on cash that carries no additional risk in any of these vehicles.

This guide quantifies exactly what that gap costs on a real dollar amount, explains the three most practical savings account alternatives (high-yield savings accounts, Treasury bills, and Series I bonds), covers the state tax angle most readers miss, and closes with a concrete allocation structure any reader can implement this week.

A $50,000 balance sitting in a typical big-bank savings account at 0.10% APY generates approximately $50 per year. Even at the FDIC-reported national average of 0.38% APY as of mid-2026, that same balance produces only about $190.

The FDIC national average savings rate data, published monthly by the Federal Deposit Insurance Corporation, confirms that standard savings accounts across U.S. banks remain clustered well below 0.50% APY, which is the structural floor that makes the gap with competitive alternatives so persistent.

Those numbers look modest in isolation. Over five years, though, the cost of leaving that cash in a standard savings account instead of 3-month Treasury bills yielding approximately 3.71% compounds into something harder to dismiss.

Over five years, keeping $50,000 in a standard savings account versus Treasury bills represents an estimated $8,325 in uncollected interest income, at no additional risk to the saver.

The low rate is not a bank failing its customers. It is a structural feature of branch-based banking: physical locations, staffing costs, and a depositor base that rarely comparison-shops. The good news is that every alternative covered in this guide carries the same FDIC insurance or direct U.S. government backing that a standard savings account provides.

This is not a risk-return trade-off. It is an awareness gap.

The comparison between a 0.10% savings account and a 3.71% T-bill is a nominal one; the real purchasing power of any cash holding also erodes as inflation runs above the interest rate earned, meaning the true cost of an underperforming account includes both foregone interest income and silent purchasing power loss.

A high-yield savings account (HYSA) is structurally identical to the savings account at a big bank. It carries the same FDIC insurance (up to $250,000 per depositor, per bank), the same deposit protection, and the same basic functionality. The difference is the rate.

Online-only banks operate without branch networks, which strips out the overhead that prevents traditional banks from paying competitive yields. That cost advantage flows directly into higher interest rates for depositors.

The difference on a $50,000 balance is difficult to misread:

| Account Type | Rate (APY) | Annual Interest on $50,000 | FDIC Insured |

|---|---|---|---|

| Big-bank savings (typical) | 0.10% | ~$50 | Yes |

| National average savings | 0.38% | ~$190 | Yes |

| Top HYSA | Up to 5.00% | ~$2,500 | Yes |

Rates on HYSAs are variable and may shift as broader market interest rates change. Some top rates are conditional on balance tiers or specific account requirements.

Opening a HYSA typically takes minutes online. Most accounts charge no monthly fee, require minimal or no balance minimum, and allow transfers to a linked checking account within 1-2 business days. For most savers, this single step is the highest-impact, lowest-effort financial move available right now.

Treasury bills are short-term U.S. government debt with maturities from 4 to 52 weeks. They carry the full faith and credit of the U.S. government, which means for large balances they have no insurance cap and no credit risk beyond what the government itself carries. The 3-month T-bill was yielding approximately 3.71% as of mid-2026, producing roughly $1,855 per year on a $50,000 balance.

The mechanics of how T-bill yields are set, through competitive Treasury auctions and continuous secondary-market repricing based on inflation data and Fed policy expectations, explain why the 3-month rate tracks the federal funds rate closely and why it will shift as monetary policy evolves.

The nominal yield on a T-bill may look lower than a top HYSA rate. But the comparison shifts once state taxes enter the equation.

Interest earned on Treasury bills is exempt from state and local income tax. It remains federally taxable, but the state exemption can meaningfully change the after-tax return for residents of high-tax states.

Consider a saver in a state with a 10% state income tax rate. A HYSA paying 5.00% APY produces an after-state-tax yield of roughly 4.50%. A T-bill yielding 3.71% keeps the full 3.71% at the state level because no state tax applies. The gap narrows considerably, and in states with rates above 10% (California, New York, New Jersey), the T-bill can effectively match or outperform a nominally higher HYSA on an after-tax basis.

The advantage scales directly with the saver’s state tax rate. For residents of states with no income tax, the exemption offers no incremental benefit, and the choice between HYSAs and T-bills comes down to rate, liquidity, and convenience.

One important liquidity distinction: T-bills held to maturity return full face value with no market risk. Selling before maturity through a brokerage is possible, but the price can fluctuate slightly with interest rates. Unlike a savings account, funds are committed for the duration of the term, typically 4-13 weeks for the most common cash-management maturities.

Series I savings bonds are U.S. Treasury obligations designed to protect purchasing power against inflation. Their interest rate is a composite of two components: a fixed rate set at purchase that remains constant for the life of the bond, and an inflation-adjusted component that resets every six months based on changes in the Consumer Price Index.

The composite rate for Series I bonds issued May-October 2026 is 4.26%, as confirmed by U.S. Treasury data.

On the maximum annual purchase of $10,000, that rate produces approximately $426 in annual interest. Like Treasury bills, I bond interest is exempt from state and local income tax, and federal tax can be deferred until the bond is redeemed, a feature that allows holders to manage taxable income year by year.

The benefits are real, but the constraints are equally specific. Before committing funds, savers should weigh the following limitations:

The best-fit use case is a defined portion of cash the saver is confident will not be needed for at least one year, where inflation protection is the primary objective. The annual cap means I bonds supplement rather than replace HYSAs or T-bills, but for the right slice of savings, the combination of inflation protection, state tax exemption, and federal tax deferral is genuinely distinctive.

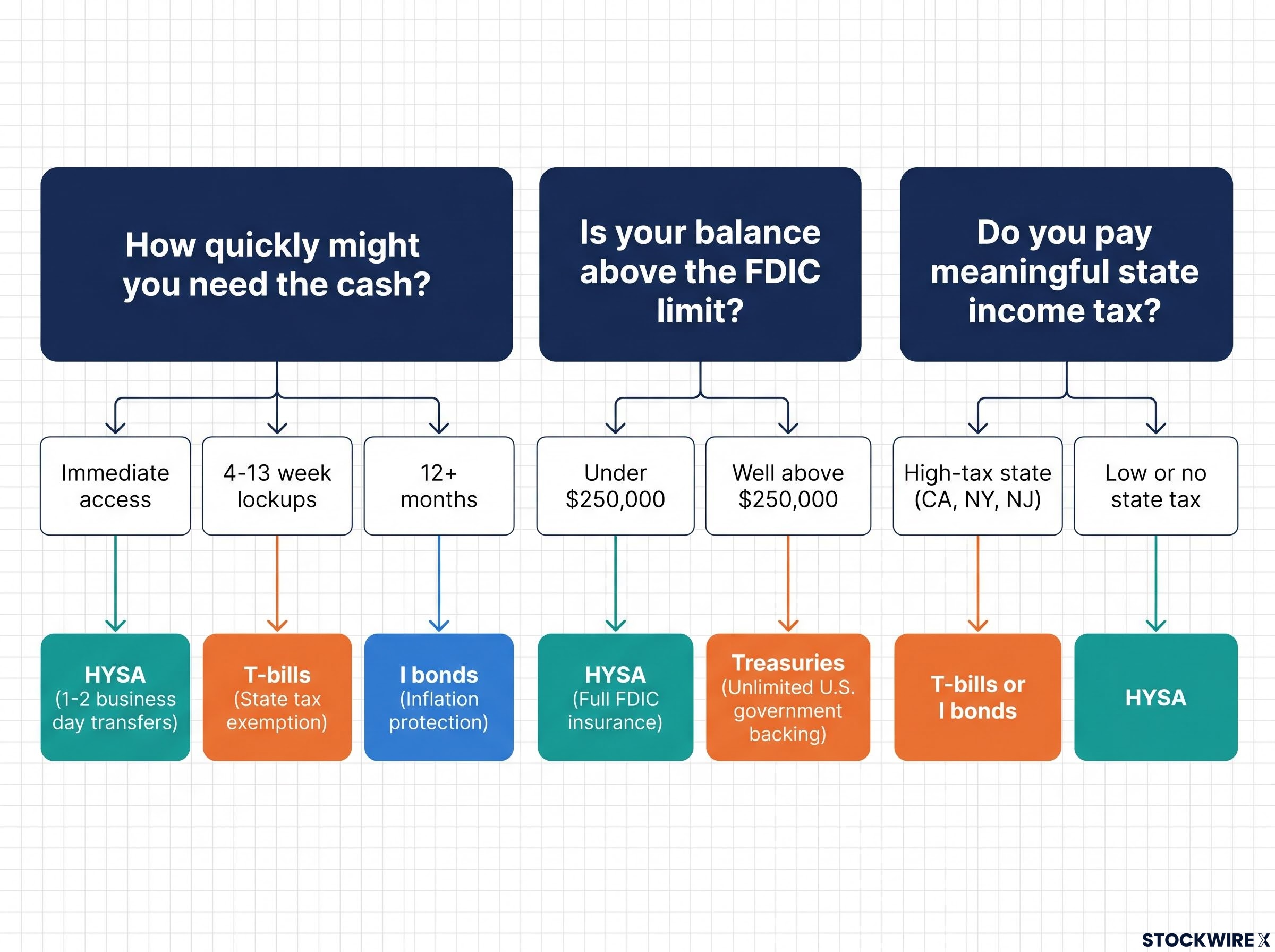

Rather than comparing products side by side, three practical questions sort the decision based on individual circumstances.

| Question | If… | Best Fit | Key Reason |

|---|---|---|---|

| How quickly might you need the cash? | Immediate access required | HYSA | 1-2 business day transfers, no lockup |

| Comfortable with 4-13 week lockups | T-bills | Competitive yield plus state tax exemption | |

| Will not need funds for 12+ months | I bonds | Inflation protection with tax advantages | |

| Is your balance above the FDIC limit? | Under $250,000 per bank | HYSA | Full FDIC insurance, same as any bank |

| Well above $250,000 | Treasuries | Unlimited U.S. government backing, no cap | |

| Do you pay meaningful state income tax? | High-tax state (CA, NY, NJ) | T-bills or I bonds | State tax exemption improves after-tax yield |

| Low or no state income tax | HYSA | Highest nominal rate wins when tax is not a factor |

These three options are complementary, not competing. A saver might use all three simultaneously: a HYSA for immediate liquidity, T-bills for the state tax advantage on a portion of cash committed for a few months, and I bonds for a smaller, longer-horizon inflation-protected slice.

The framework is designed to be repeatable. As rates change or personal circumstances shift, running the same three questions produces an updated answer.

Investors approaching or already in retirement who want to formalise how cash, bonds, and equities interact across a multi-decade drawdown period will find our dedicated guide to the retirement bucket strategy covers exactly how to size each bucket based on income gaps, which instruments belong in the short-term liquidity bucket, and when to replenish from longer-horizon holdings.

The $50,000 balance used throughout this guide produces roughly $50-$190 per year in a standard savings account. The following three-step structure, built entirely on FDIC-insured accounts and direct U.S. government obligations, puts that same cash to work at several times the return with no meaningful increase in risk.

Combined, this structure could generate an estimated $2,000-$2,500 or more in annual interest, depending on the specific allocation and prevailing rates, compared to the $50-$190 a standard savings account provides.

HYSA rates are variable and T-bill yields will shift with market rates. The structural advantage, however, persists as long as the gap between big-bank savings rates and competitive alternatives remains wide.

Every option in this guide requires no additional risk tolerance, no investment expertise, and no ongoing management beyond initial setup. The underlying guarantees are the same ones most savers already rely on: FDIC insurance and the full faith and credit of the U.S. government.

Rates will fluctuate. The specific numbers in this guide will look different in six months. But opening a HYSA is the structural upgrade that locks in better default behaviour regardless of where rates move next. It replaces a 0.10% default with a competitive one, and that single change compounds over years.

Savers who max out HYSA and T-bill allocations and then consider yield-chasing beyond safe instruments by moving into high-dividend equities for additional income should note that dividend-paying stocks fell approximately 7.6% peak to trough in early 2026, providing meaningfully less protection than the cash alternatives covered in this guide.

The first step is the simplest: open a HYSA account and move idle cash. Evaluate T-bills and I bonds as a secondary step once the primary upgrade is in place. The process takes minutes. The cost of not starting is measured in thousands.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Interest rates are variable and subject to change based on market conditions.

The three most practical savings account alternatives in 2026 are high-yield savings accounts (HYSAs), Treasury bills, and Series I bonds. Each carries FDIC insurance or direct U.S. government backing, and all three can generate significantly more interest than a standard big-bank savings account.

A high-yield savings account is structurally identical to a standard savings account, including the same FDIC insurance up to $250,000, but online-only banks eliminate branch overhead and pass the savings on as higher interest rates, often many times the national average APY.

Interest earned on Treasury bills is exempt from state and local income tax, though it remains federally taxable. For savers in high-tax states, this exemption can meaningfully narrow or eliminate the yield gap between T-bills and a nominally higher-rate HYSA on an after-tax basis.

Series I bonds have an annual purchase cap of $10,000 per person, cannot be redeemed within the first 12 months under any circumstances, and carry a penalty of three months of interest if redeemed within the first five years. They also can only be purchased through TreasuryDirect, not through a brokerage account.

You can purchase Treasury bills directly from the U.S. Treasury at TreasuryDirect.gov with a minimum of $100 and no commission. Automatic rollover at maturity is available, making the process largely hands-off once the account is set up.