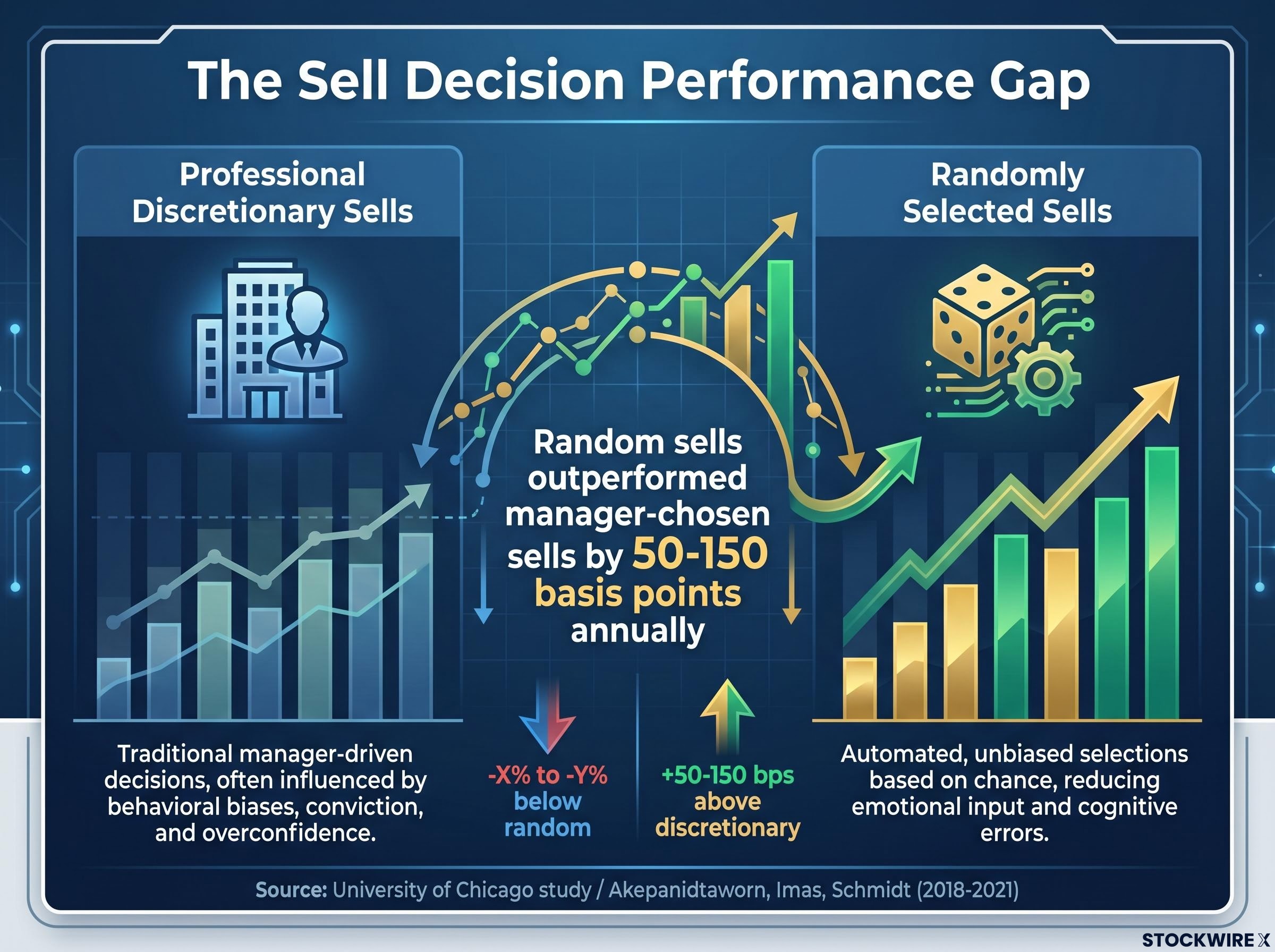

A University of Chicago study found that randomly selected sell decisions outperformed the sell decisions of professional portfolio managers by up to 150 basis points annually. The managers were not failing at stock selection. They were failing at exit.

Most investment content, most investor psychology, and most financial media attention concentrates on what to buy. The sell decision receives far less systematic scrutiny, yet behavioural finance research consistently identifies it as the moment where cognitive and emotional errors are most acute and most costly. The conditions at exit (time pressure, emotional salience, compelling crisis narratives, the absence of structured research processes) are structurally worse than the conditions at entry. What follows traces the specific investing biases that degrade sell decisions, quantifies their cost with the strongest available evidence, and builds the case that reducing decision frequency is not a passive default but a rational, research-backed defence.

The sell decision is where behavioural error concentrates

Consider how most investors enter a position. The buy decision is typically deliberate: screened, researched, discussed, sized. There is a thesis. There is a price target or at least a rationale. The emotional temperature is moderate because the investor is choosing to act, not reacting.

Now consider the sell. It arrives under different conditions. A position has underperformed the investor’s internal timeline. Capital is needed for a more exciting opportunity. A headline triggers a fear response. The research process that preceded the purchase is rarely replicated before the exit.

This asymmetry is not incidental. Research by Akepanidtaworn, Imas, Schmidt and others (circa 2018-2021) examined discretionary sell decisions made by institutional portfolio managers, professionals with full research infrastructure and significant experience. The finding was striking.

The Journal of Finance research on institutional sell decisions by Akepanidtaworn, Di Mascio, Imas, and Schmidt documented this pattern across a large sample of professional portfolios, finding that heuristic-driven exits consistently destroyed value relative to the managers’ own buy-side performance.

Randomly selected sells outperformed manager-chosen sells by approximately 50-150 basis points annually.

When randomness outperforms professional judgment, something is structurally wrong with the judgment environment. The problem is not that these managers lacked skill; their buy decisions added value. The problem is that the conditions surrounding sell decisions, the emotional pressure, the absence of a disciplined process, systematically degraded the quality of their choices. Investors who focus all their discipline on the buy and leave the sell to instinct are, by the evidence, concentrating effort where it matters least.

When big ASX news breaks, our subscribers know first

What is actually happening in the brain at the moment of exit

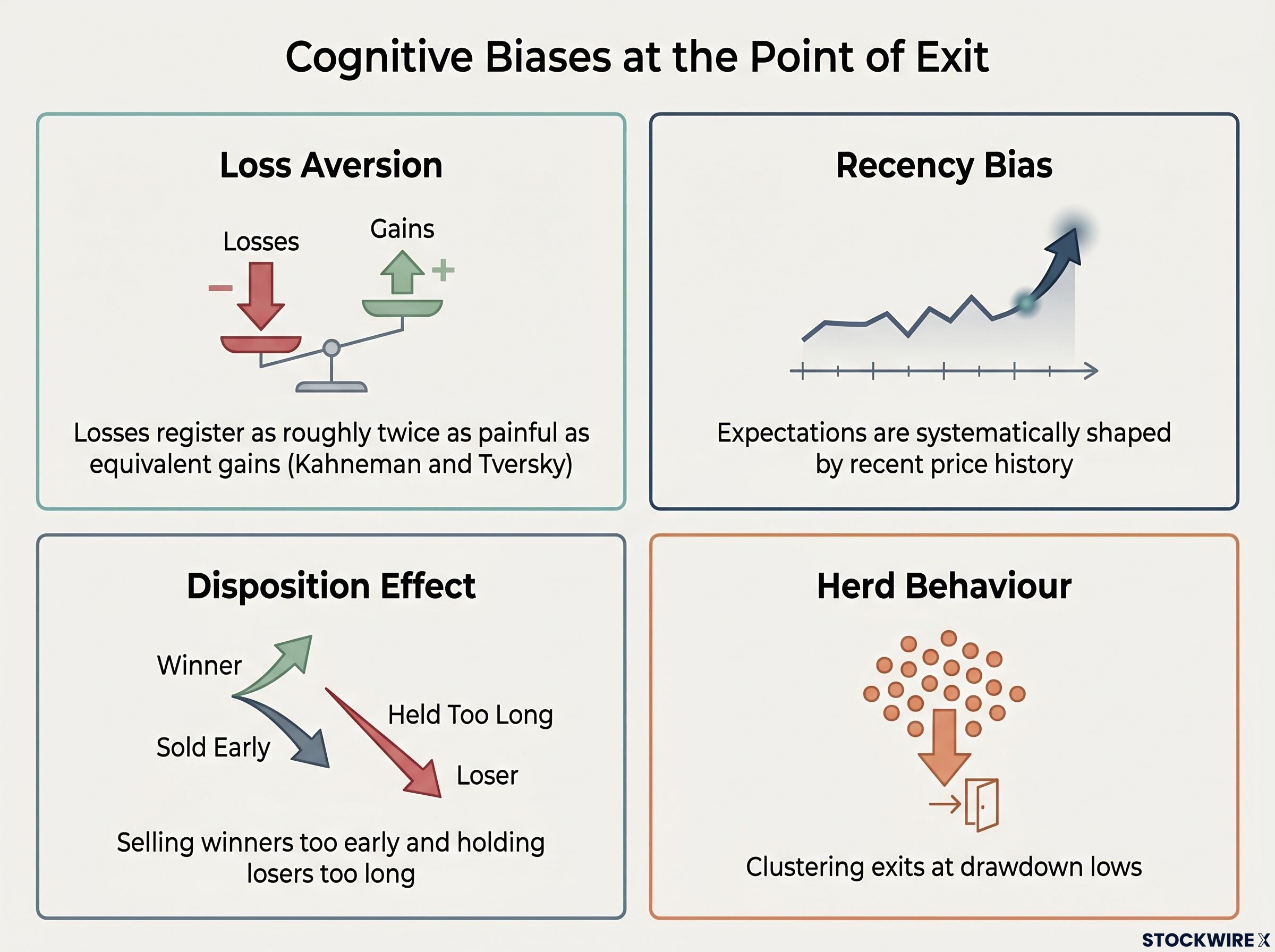

The urge to sell during a drawdown feels rational. The portfolio is falling. Action feels protective. But behavioural finance identifies specific, predictable biases operating at exactly this moment, each with a distinct mechanism:

- Loss aversion: Losses register as roughly twice as painful as equivalent gains feel good, a foundational finding from Kahneman and Tversky. Investors sell to stop the psychological pain, not in response to changed fundamentals.

- Recency bias: Expectations are systematically shaped by recent price history rather than long-term base rates. After a decline, investors project further decline. After a rally, they project further gains. The result is the persistent “buy high, sell low” pattern.

- Disposition effect: Investors sell winners too early (to lock in satisfaction) and hold losers too long (to avoid confirming the loss on paper). This is precisely backwards from what maximises long-run outcomes, driven by mental accounting and status quo bias that makes underperforming holdings particularly sticky.

- Herd behaviour and overconfidence: These amplify the other errors at market turning points, clustering exits at drawdown lows when the cost of selling is highest.

The Kahneman and Tversky research underpinning loss aversion bias has been directly linked to a return shortfall of roughly 1-2 percentage points per year, according to Morningstar’s ‘Mind the Gap’ analysis, with the primary mechanism being investors who sell near market lows and re-enter only after prices have already recovered the steepest gains.

When the exit urge is actually a warning signal, not an instruction

The felt urgency to sell during a drawdown is diagnostically useful. It signals that one or more of these biases is active, not that the underlying rationale for holding the position has changed. Recognising the impulse as a symptom rather than an instruction is the first step toward the structural defences developed later in this analysis.

The compounding cost of leaving at the wrong time

The investor return gap, the persistent finding that investors’ realised returns trail the returns of the underlying instruments they invest in, is driven primarily by poor timing around exits. The cost is not abstract. It compounds.

Research by Elkind et al. (2022), based on brokerage account analysis, found that approximately 30.9% of investors who panic-sold during a significant market downturn did not return to equities.

The Elkind et al. panic selling research used a novel dataset of individual brokerage accounts to identify the behavioural and situational predictors of panic exits, finding that a substantial share of those who liquidated during major downturns never rebuilt equity exposure, permanently severing their participation in subsequent recoveries.

Roughly one-third of panic sellers in the study population never re-entered equities, according to Elkind et al. (2022), permanently forfeiting compounding.

The 2008-2009 and 2020 episodes illustrate what these investors forfeited:

| Episode | Market Decline | Subsequent Recovery |

|---|---|---|

| 2008-2009 financial crisis (S&P 500, peak October 2007 to trough March 2009) | Approximately 57% | Approximately 15% per annum compounding from the March 2009 trough over the following decade |

| 2020 pandemic decline (S&P 500, February to March 2020) | Approximately 34% | Full recovery within months; S&P 500 reached new highs by August 2020 |

An illustrative calculation using the 2008-2009 trough makes the cost tangible: a hypothetical investor who exited equities near the bottom with approximately $450,000 and remained in cash would have missed the equivalent of a roughly 10x increase in portfolio value over the subsequent period, assuming continued S&P 500 exposure and reinvested returns. This is an illustrative figure dependent on index, rate, and holding period assumptions, but the directional point is well supported.

The cost of being out of the market is asymmetric. The best return days cluster around periods of highest volatility, precisely when panic sellers are most likely to be sitting in cash. The compounding loss is not recovered by re-entering once conditions “feel safe,” because by that point the sharpest recovery gains have already occurred.

Reactive trading costs compound through four distinct mechanisms: transaction fees, tax drag from forfeiting long-term CGT discounts, timing errors from missing the sharpest recovery sessions, and opportunity cost from sitting in cash during periods of maximum market momentum, with global behavioural finance research estimating a combined return drag of approximately 1.5% per annum attributable to these biases.

Why concentration makes the sell decision even more dangerous

Research by Hendrik Bessembinder at Arizona State University’s W.P. Carey School of Business found that on the order of 1-4% of all stocks accounted for essentially all net wealth creation in U.S. equity markets relative to Treasury bills, using data from 1926 onward. The median stock underperformed or destroyed value over long horizons.

This creates a two-sided problem for concentrated positions. The downside risk of holding any individual stock is real; most stocks underperform the broad market over time. But the cost of truncating a rare compounder is far larger because the gains are convex. An investor who sells a rare winner “too early” permanently forecloses the most valuable portion of that stock’s return contribution.

The Apple illustration captures this asymmetry. An investor who bought shares after the iPod launch at roughly $15 per share and sold at approximately $45 would have felt satisfied with a 3x return, only to watch the stock deliver a further gain of several thousand percent in subsequent years. The specific magnitude depends on split-adjusted prices and dates, but the directional point is clear: the cost of truncating a compounder dwarfs the satisfaction of locking in a moderate gain.

The structural pattern repeats:

Small-cap exit discipline illustrates the concentration problem in its sharpest form: UNSW and University of Sydney research confirms the disposition effect is especially pronounced in smaller stocks, where illiquidity narrows the window for orderly exits and anchoring on peak prices causes investors to hold through the very drawdowns where forced liquidation eventually becomes unavoidable.

- An investor accumulates a large position in a high-performing stock

- Paper gains are treated as permanent wealth, sometimes used to collateralise borrowing

- A decline triggers forced or panic-driven liquidation at precisely the wrong moment

The disposition effect in the context of return distributions

The disposition effect makes investors systematically more likely to sell their rare winners early and hold their underperformers. Given Bessembinder’s finding that winners are extremely rare and gains are convex, this bias truncates the most valuable portion of the return distribution, the exact segment where patient holding generates the greatest compounding benefit.

What the research actually recommends: structure over willpower

Knowing about biases does not reliably prevent them. This is itself a finding of the behavioural literature. Awareness is necessary but insufficient. The interventions that actually work are structural, designed to make reactive exits effortful and deliberate rather than frictionless.

The evidence supports four specific mechanisms:

- Written financial plan as commitment device: A pre-defined, written plan creates a reference point that makes departure from the strategy explicit. Without one, investors lack context during drawdowns and default to emotional reaction.

- Rules-based rebalancing and automation: Automatic contributions, systematic rebalancing, and rules-based trimming remove discretionary judgment from the moments when it is least reliable. Research on pre-commitment strategies, building on work by Thaler, Sunstein, and others, identifies automation as more effective than willpower.

- Pre-set concentration and trimming thresholds: Position-size limits established in advance prevent the accumulation-and-forced-liquidation pattern. These are applied before the emotional stakes are high enough to distort judgment.

- Reduced monitoring frequency: More scrutiny increases the likelihood of trading, and more trading increases the probability of value-destroying decisions. Reducing portfolio review frequency is one of the simplest and most structurally powerful interventions available.

The “do less” posture is not passive or uninformed. It is a rational, evidence-based strategy grounded in the documented costs of discretionary intervention, particularly at the point of exit.

The Imas finding reinforces this: if professional managers with full research access cannot outperform random sells with their judgment, the case for reducing the frequency of discretionary sell decisions is strong.

For investors ready to translate these principles into a written plan, our comprehensive walkthrough of pre-committed investing structures covers the specific mechanics of rules-based rebalancing, position-size thresholds, and automation tools, with worked examples from Australian SMSF and retail account contexts, including how the CGT discount framework interacts with holding-period decisions.

The asymmetry most investors ignore, and what to do about it

Buy decisions are where investors invest attention. Sell decisions are where behavioural finance shows the real damage is done. These two facts together constitute an asymmetry that most portfolios are not built to address.

The University of Chicago result is not a curiosity. It is a structural signal about where human judgment adds negative value. Building decision systems around this finding, rather than hoping for better instincts next time, is the logical response.

The goal is not to make better sell decisions through smarter analysis. It is to make fewer sell decisions through better structure, and to treat the impulse to exit during volatility as diagnostic information rather than as an instruction. Write the plan. Set the rules. Reduce the monitoring frequency. Treat inaction during drawdowns as an active, intentional, evidence-backed choice.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.