US Inflation Hits 4.2% but Core Data Tell a Calmer Story

20 hrs ago

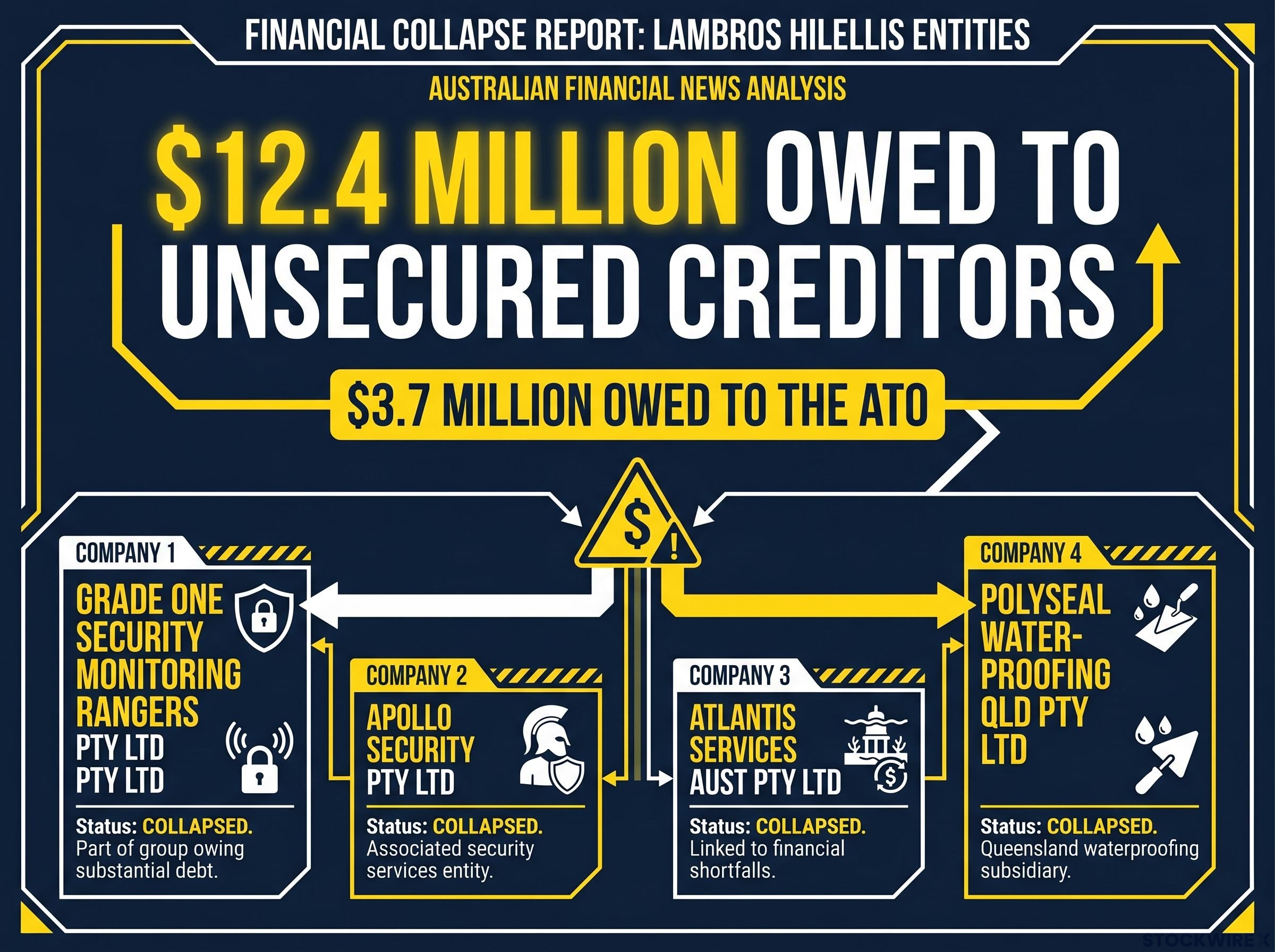

ASIC has imposed the maximum five-year director ban it can hand down without going to court, disqualifying Lambros Hilellis of Kingsgrove, New South Wales from managing corporations until 29 March 2031. The action, announced on 28 April 2026 via media release 26-085MR, followed the collapse of four companies in the security services and building and construction sectors, leaving approximately $12.4 million owed to unsecured creditors. ASIC described the conduct as falling into “the worst category of misconduct” in terms of honesty, integrity, and disregard for director’s duties. The findings draw on supplementary liquidator reports funded through the Assetless Administration Fund, and the case serves as a direct signal about which patterns of director behaviour will attract the regulator’s hardest available administrative response.

The creditor losses alone set this case apart. Across four companies wound up within the relevant statutory window, approximately $12.4 million was owed to unsecured creditors. Of that, roughly $3.7 million was owed to the Australian Taxation Office (ATO), adding a public-interest dimension that extends beyond commercial losses between private parties.

Hilellis was an officer of all four entities:

| Company | Sector | ACN |

|---|---|---|

| Grade One Security Monitoring Rangers Pty Ltd | Security services | 156 567 967 |

| Apollo Security Pty Ltd | Security services | 154 881 973 |

| Atlantis Services Aust Pty Ltd | Building and construction | 600 383 775 |

| Polyseal Waterproofing Qld Pty Ltd | Building and construction | 149 962 872 |

ASIC’s findings relied on supplementary liquidator reports prepared by Stephen Hundy and Chad Rapsey of Rapsey Griffiths, funded through the Assetless Administration Fund. That funding mechanism matters:

Four failures, one director. The pattern is the story.

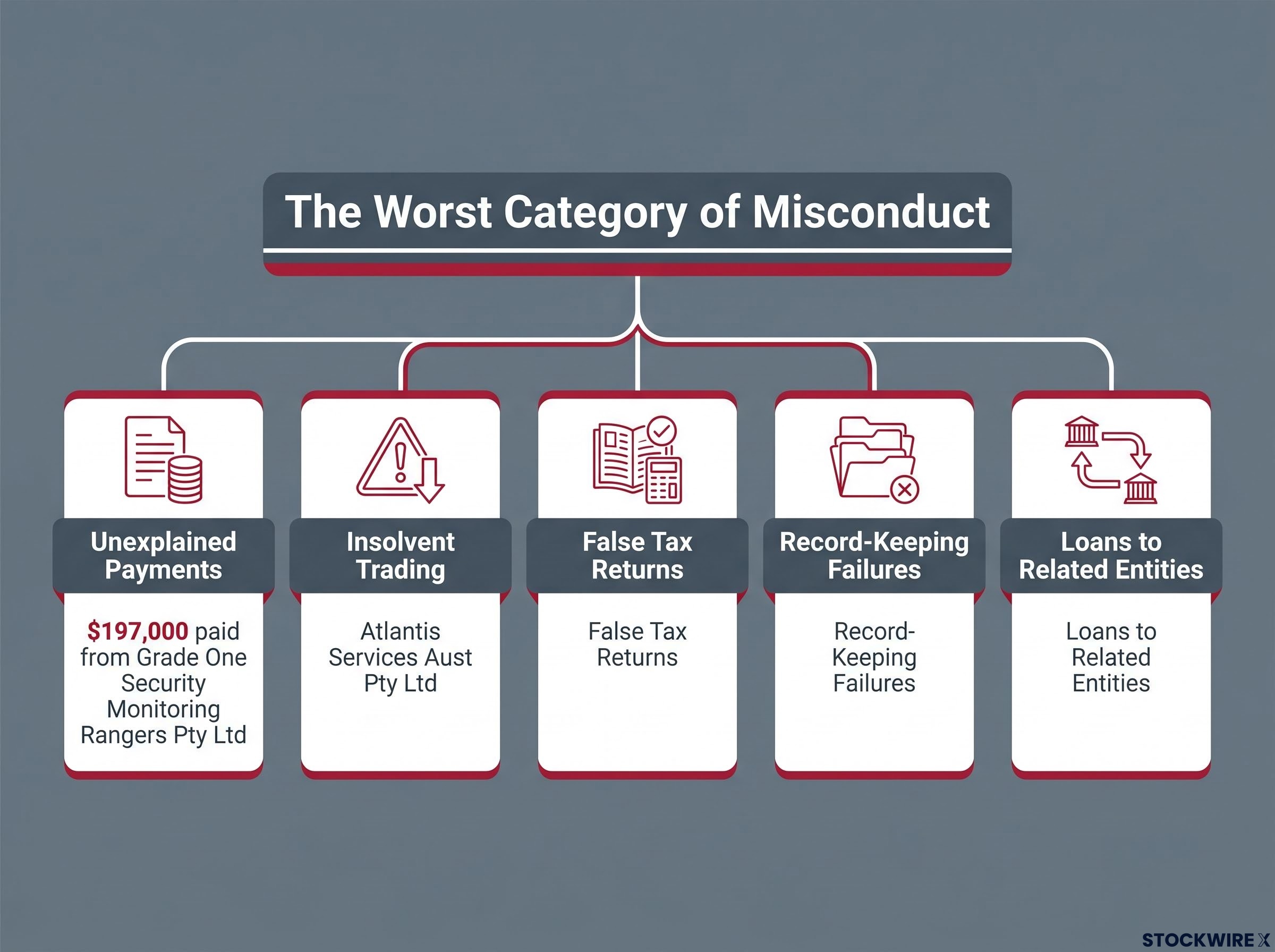

Companies fail for many reasons. ASIC’s findings against Hilellis describe conduct that goes well beyond mismanagement into territory the regulator characterised as deliberate.

ASIC found that Hilellis’ conduct fell into “the worst category of misconduct” in terms of honesty, integrity, and disregard for director’s duties.

The specific findings span five categories:

The distinction between negligence and dishonesty is the line that separates a manageable regulatory outcome from a maximum-penalty disqualification. The false tax returns, the unexplained payments, and the loans to related entities without repayment prospects all sit on the dishonesty side of that line. Record-keeping failures and insolvent trading compound the picture, but it was the honesty findings that placed this case, in ASIC’s assessment, at the ceiling.

The Berndale Capital Securities collapse offers a close parallel in terms of director misconduct in finance, where co-director Daniel Kirby received a custodial sentence of nearly three years for conduct that included the unlawful movement of company funds, and where ASIC pursued criminal charges rather than administrative remedies alone.

For directors and company secretaries, these categories form a practical checklist of conduct ASIC treats as disqualification-worthy.

The five-year ban Hilellis received is the maximum ASIC can impose through its administrative pathway. Understanding why “maximum” has a ceiling requires distinguishing between the two disqualification mechanisms available under the Corporations Act 2001.

ASIC’s director disqualification powers under s 206F allow the regulator to act administratively, without court proceedings, capping the available penalty at five years and making it the fastest available route to removing a director from corporate management.

Under s 206F of the Corporations Act 2001 (the administrative disqualification power), ASIC can ban a person from managing corporations for up to five years without court proceedings:

Hilellis met the trigger conditions across all four companies. ASIC imposed the full five years, effective until 29 March 2031.

Under ss 206C-206D of the Corporations Act 2001, courts can impose longer bans:

Hilellis retains the right to seek review of ASIC’s decision through the Administrative Review Tribunal. That review right provides due process but does not suspend the disqualification while under review.

The distinction matters for readers who encounter ASIC enforcement coverage regularly. A five-year administrative ban represents the ceiling of one pathway, not the ceiling of regulatory consequences overall.

This disqualification was not a default outcome. ASIC imposed the maximum available penalty, and the factors it cited reveal the threshold at which the regulator reaches for the ceiling of its administrative power:

ASIC found that the conduct demonstrated a “complete disregard for director’s duties.”

The Assetless Administration Fund played a direct role in enabling this outcome. Without funded liquidator reports, the investigation of assetless companies would have stalled. The Fund’s involvement signals that even where company assets are exhausted, ASIC retains the capacity to pursue accountability.

Financial reporting failures sit at the core of ASIC’s 2026 enforcement priorities across multiple company types, with three ASX-listed companies collectively fined $1,170,000 for multi-year non-lodgement of annual reports, a parallel campaign that reinforces the regulator’s appetite to pursue record-keeping and disclosure obligations regardless of company size or sector.

For investors, creditors, and co-directors in multi-entity corporate structures, this case maps the specific combination of factors that triggers ASIC’s hardest available administrative response.

The ban is set. Hilellis cannot manage corporations until 29 March 2031, and doing so during the disqualification period would constitute a criminal offence.

The forward-looking position involves three facts:

That last point warrants emphasis. Creditors and stakeholders in failed company situations often expect regulatory enforcement to translate into financial recovery. It does not. The disqualification prevents Hilellis from repeating the conduct with future companies. It does not return money to the creditors of the four that already failed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASIC’s five-year administrative ban of Lambros Hilellis reflects a deliberate escalation to the ceiling of the power available under s 206F of the Corporations Act 2001. The combination of four corporate collapses, $12.4 million in creditor losses, deliberate dishonesty findings (including false tax returns), and systemic record-keeping failures across multiple entities constitutes the clearest trigger for the harshest available administrative response.

The Assetless Administration Fund is an active enforcement tool, not a dormant one. Even where company assets are exhausted and creditor recoveries are nil, ASIC retains the mechanism and the appetite to investigate, find, and disqualify.

ASIC’s shift toward court penalties as the default enforcement posture is visible across multiple regulatory domains: the $10 million Federal Court penalty against Binance in 2026 and the Corporations Amendment (Digital Assets Framework) Act passed in April 2026 both reflect the same institutional preference for maximum available consequences over guidance-based compliance that characterises the Hilellis disqualification.

An ASIC director ban is an administrative disqualification that prevents a person from managing corporations for a set period. Under s 206F of the Corporations Act 2001, ASIC can impose a ban of up to five years without court proceedings if the person was an officer of two or more companies wound up within the previous seven years and their conduct contributed to those failures.

The maximum ASIC can impose through its administrative pathway under s 206F is five years, which is the ceiling Hilellis received. Longer bans of up to 15 years or permanent disqualification require separate court proceedings initiated by ASIC under ss 206C-206D of the Corporations Act 2001.

ASIC cited five categories of misconduct: unexplained payments of $197,000 from one company's bank account, insolvent trading, false income tax returns lodged with the ATO, systemic record-keeping and reporting failures across all four companies, and loans made to related entities without any reasonable prospect of repayment.

No. The disqualification is a regulatory accountability measure that prevents Hilellis from managing corporations until 29 March 2031, but it does not restore funds to creditors. The $12.4 million owed to unsecured creditors, including $3.7 million to the ATO, is not recovered through a director ban.

The Assetless Administration Fund is a government mechanism that finances liquidator investigations into company failures where recoverable assets are minimal or non-existent. In the Hilellis case, it funded the supplementary liquidator reports prepared by Rapsey Griffiths, enabling ASIC to build its findings even though the collapsed companies had no assets available to cover investigation costs.