SpaceX IPO: Is SPCX Worth Buying at 95x Revenue?

24 mins ago

SpaceX closed the largest initial public offering in market history on 12 June 2026, raising $75 billion on the Nasdaq under the ticker SPCX. The listing generated the kind of media spectacle that makes investors feel they need to act immediately. They do not. The more consequential story sits beneath the headlines: what a $75 billion injection of new equity supply, arriving at the front of a broader 2026 IPO pipeline, means for the stocks investors already own. This article breaks down the equity supply mechanics set in motion by the SpaceX listing, how a record buyback surge partially offsets them, what history reveals about buying into newly listed stocks, and five principles for navigating the months ahead with discipline rather than excitement.

The core facts of the listing speak for themselves:

SpaceX’s debut is the largest IPO in market history as of June 2026.

That designation will generate weeks of coverage. But the first-day performance of any single stock, no matter how large the offering, tells investors very little about what happens next to their portfolios. What matters more is the supply-side chain reaction this listing has initiated, and the fact that SpaceX is being characterised as the first in a series of major 2026 listings rather than a standalone event.

Stock markets operate on supply and demand. When a company goes public, it expands the total pool of shares available for investors to buy and sell. If more shares enter the market and investor demand does not grow proportionally, that expanded supply creates downward pressure on prices across the broader market.

SpaceX added 555.6 million shares to the market in a single session. That is a meaningful supply event on its own. The more important point is what comes after it.

The listing has been framed by market commentary, including analysis from Fisher Investments, as the opening act in a broader wave of anticipated major listings throughout 2026. A single large IPO creates a temporary supply shock. A sustained pipeline of large listings creates cumulative supply expansion that shifts the balance over months, not days. Investors tracking only SpaceX’s share price are watching the wrong variable. The equity supply curve across the full year is what shapes the environment for all US equities.

Standard Chartered global CIO Steve Brice flagged market digestion difficulties as a specific risk for the summer months of 2026, noting that SpaceX, Anthropic, and OpenAI are collectively valued at approximately $3.5 trillion and are all targeting listings within a compressed mid-to-late 2026 window.

The supply picture is not the same everywhere. In the United States, equity supply is growing as new listings add shares to the market. In overseas developed markets, the opposite is happening.

European and Japanese markets have seen equity supply contract as companies buy back their own shares and consolidation reduces the number of listed entities. Fewer shares available for purchase, with demand held constant, tends to support prices.

State Street Global Advisors analysis on Japanese buybacks shows that Japanese companies materially increased their average annual share repurchase activity through 2024 and 2025, providing measurable evidence that equity supply contraction in developed markets outside the US is grounded in corporate behaviour rather than projection.

| Market | Equity Supply Trend | Implication for Prices |

|---|---|---|

| United States | Expanding (new IPO listings, 2026 pipeline) | Supply growth may pressure valuations if demand does not keep pace |

| Europe | Contracting (buybacks, consolidation) | Shrinking supply could support prices, all else equal |

| Japan | Contracting (buybacks, consolidation) | Shrinking supply could support prices, all else equal |

This divergence offers a concrete, mechanism-based reason to consider geographic diversification. The case for holding non-US developed market exposure is not a generic risk-management platitude; it is grounded in measurable differences in share supply dynamics that are playing out right now.

US equity home bias has become a structural concentration risk rather than a passive default: the average US investor holds 70-76% of their equity portfolio in domestic stocks, a 9-15 percentage point overweight relative to the MSCI ACWI benchmark, at the precise moment when S&P 500 earnings growth forecasts are disproportionately reliant on a small number of AI-exposed firms.

New IPO supply does not operate in isolation. When companies repurchase their own shares, they reduce the total number of shares outstanding, effectively shrinking equity supply and working in the opposite direction to new listings.

More than $500 billion in stock buybacks were announced during April and May 2026 combined, with technology companies leading the activity.

That figure represents a record pace of repurchase activity over just two months. In practical terms, the 555.6 million shares SpaceX added to the market are being partially absorbed by established companies pulling their own shares out of circulation at an unprecedented rate.

The buyback doctrine that drives this activity is rooted in a capital allocation philosophy that has accelerated since the 1980s, with S&P 500 companies repurchasing a record $942.5 billion in shares during 2024 alone, a pace that reflects structural incentives built into executive compensation rather than simply opportunistic responses to rising cash balances.

The qualification matters, though. Buyback programmes can be scaled back quickly if corporate earnings weaken or management sentiment shifts. The current buyback tailwind is real and measurable, but it is a present-tense support for US equity prices rather than a guaranteed backstop. Investors should factor it in without depending on it.

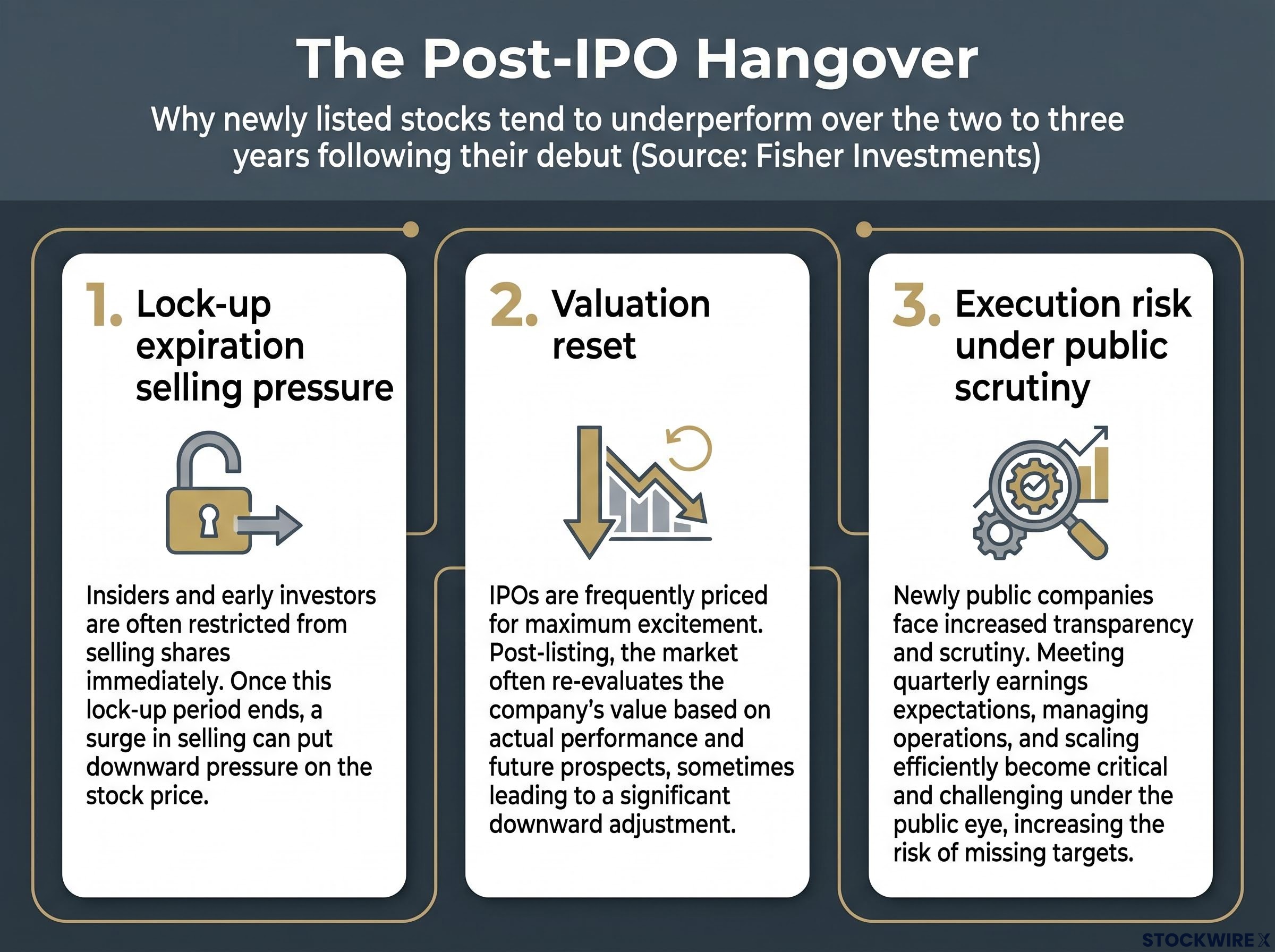

The first-day gain on a high-profile listing generates enthusiasm. The subsequent two to three years tend to dampen it. On historical average, newly listed stocks have tended to underperform both the broader market and their sector peers over the two to three years following their debut, according to Fisher Investments analysis.

The post-IPO underperformance pattern is not anecdotal: data spanning 1980 to 2024 shows newly listed companies underperforming comparably sized established peers by an average of 3.3% per year over their first five years, a drag that compounds a $10,000 investment into $12,577 rather than the $14,693 a peer-matched position would have produced.

The pattern is well-documented. What receives less attention is why it persists.

None of this means SpaceX is destined to disappoint. But the excitement surrounding a debut is a sentiment event, not an investment signal. Waiting through at least one or two earnings cycles, and past the first major lock-up expiration, before committing meaningful capital is the approach more closely aligned with historical outcomes.

The supply dynamics, buyback data, and historical track record covered above translate into five concrete principles:

The business story of SpaceX going public will dominate financial media for weeks. The market-mechanics story will shape portfolio outcomes for longer. Three forces are now in motion: rising US equity supply as the 2026 IPO pipeline develops, contracting supply in overseas developed markets creating a geographic divergence, and record buyback activity partially offsetting the new issuance.

As additional major listings arrive in the months ahead, investors who understand the supply-demand equation will be positioned to make decisions grounded in market structure rather than narrative excitement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The SpaceX IPO was the largest initial public offering in market history, closing on 12 June 2026 on the Nasdaq under the ticker SPCX, raising $75 billion through the sale of 555.6 million shares at $135 per share.

The SpaceX listing expanded total equity supply by 555.6 million shares in a single session, and with a broader pipeline of major 2026 listings anticipated, cumulative supply expansion could create downward pressure on broader US equity prices if investor demand does not grow proportionally.

Historically, newly listed stocks have underperformed the broader market and sector peers by an average of 3.3% per year over their first five years, driven by lock-up expiration selling, valuation resets, and execution risk under public scrutiny.

While US equity supply is expanding due to new listings, European and Japanese markets are seeing supply contract through buybacks and consolidation, which could support prices in those regions and provides a data-grounded reason for investors to consider geographic diversification.

More than $500 billion in share repurchase programmes were announced by US companies, predominantly in technology, during just April and May 2026, partially offsetting the new equity supply introduced by IPOs like SpaceX, though buyback programmes can be scaled back quickly if corporate earnings weaken.