Most investors still think of SpaceX as a rocket company. The label is understandable: Falcon 9 launches dominate global manifests, and the imagery of boosters landing on drone ships has defined the brand for over a decade. Yet the company’s business model, as revealed through its recent filing disclosures and commercial partnerships, tells a materially different story. At least four distinct revenue and growth vectors now sit inside the corporate structure: launch services, satellite broadband, wholesale mobile infrastructure through Direct-to-Cell, and early-stage ambitions in AI compute and custom semiconductors. Most retail pricing models are built around the first of these. The other three are where the valuation case, and the analytical complexity, actually lives. What follows maps each business line, explains the strategic logic connecting them, and frames how investors should evaluate a multi-segment technology company where each segment sits at a different stage of maturity.

The rocket business is important but it cannot carry the valuation alone

Falcon 9 has structurally changed launch economics. Booster reusability and high launch cadence have made SpaceX the dominant commercial and governmental launch provider by volume, including for NASA and commercial satellite operators. That dominance is real, and it was earned through engineering execution that no competitor has replicated at comparable scale.

The constraint is the market itself. The entire global launch industry generates an estimated $6-21 billion annually, depending on methodology and the scope of services included in the count. Even at the upper bound, the figure is too small to justify the private valuations being discussed for SpaceX as a whole.

Global Market Insights’ commercial space launch market sizing placed the industry at USD 8.2 billion in 2024, with a projected growth path to USD 31.9 billion by 2034, figures that illustrate both why Falcon 9’s dominance is commercially significant and why launch revenue alone cannot anchor a valuation in the hundreds of billions.

The global launch market sits at roughly $6-21 billion per year. SpaceX’s implied private valuation requires revenue and margin sources well beyond what launch alone can deliver.

That gap is the analytical starting point. It forces a direct question: if launch economics cannot explain the valuation, what can? The answer sits in the business lines that launch infrastructure enables, starting with the one that is already commercially live.

When big ASX news breaks, our subscribers know first

Starlink Direct-to-Cell is already a business, not a concept

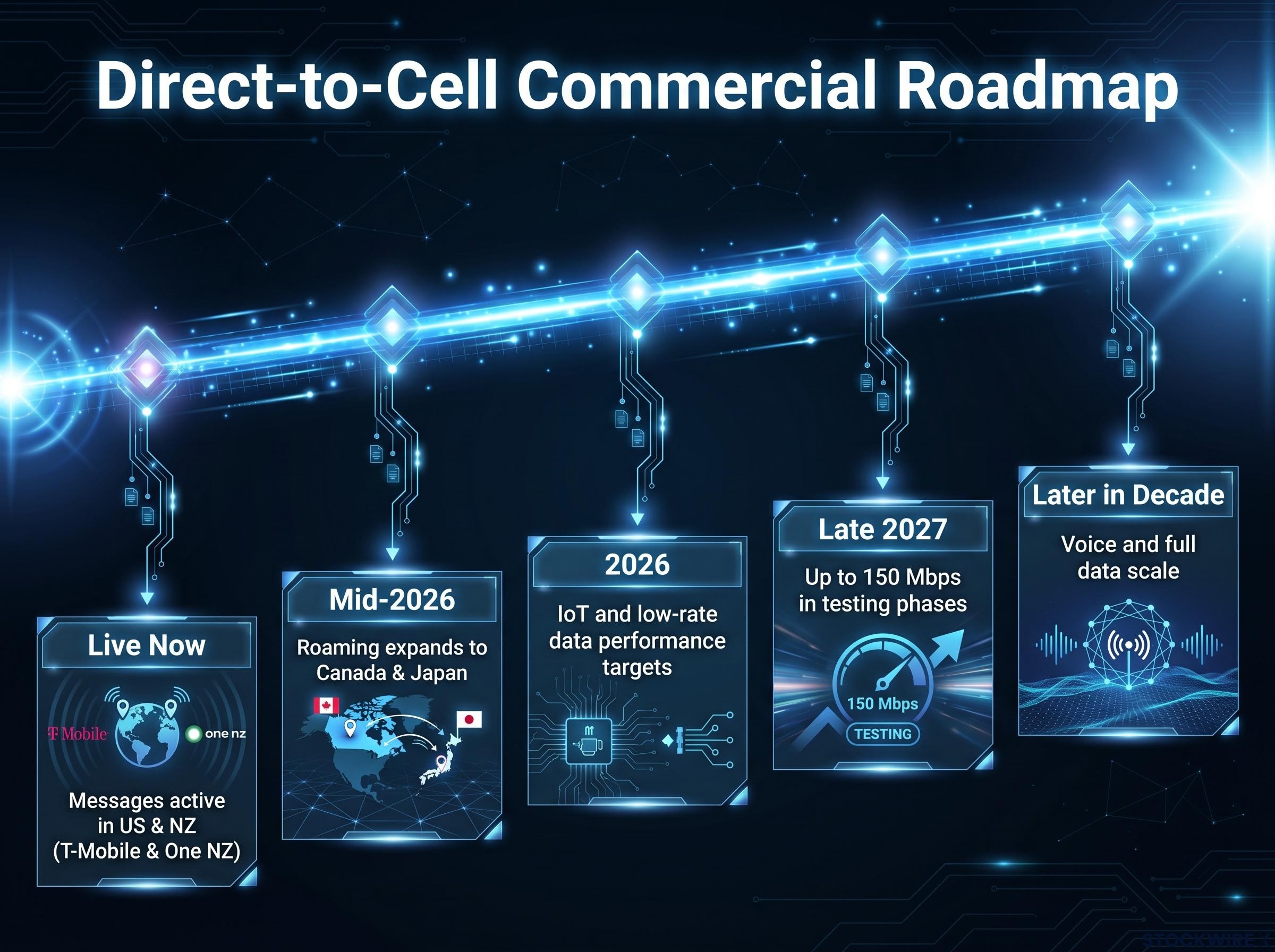

Direct-to-Cell text messaging is commercially available today. T-Mobile’s T-Satellite service in the United States and One NZ in New Zealand are both live, with roaming expanding to Canada and Japan for T-Mobile subscribers as of mid-2026. Standard 4G LTE smartphones connect directly to Starlink satellites carrying onboard eNodeB modems (the technical name for a 4G base station), with no hardware modifications and no special app required. The satellite acts as a cell tower in orbit.

That is what exists now. The roadmap extends considerably further.

- Messages: Text and SMS service commercially live in the US and New Zealand

- IoT and low-rate data: Improved performance targeted through 2026, with higher-speed targets (up to 150 Mbps) in testing phases planned for late 2027 onward

- Voice and full data: Expected to scale later in the decade, contingent on additional satellite deployment, spectrum utilisation, and regulatory approvals

The FCC has already authorised satellite-to-mobile spectrum usage in the US, removing one of the largest single regulatory hurdles.

The FCC Supplemental Coverage from Space license granted to SpaceX and T-Mobile in December 2025 formalised satellite-to-mobile spectrum access as a standardised commercial utility, cementing the regulatory foundation that Direct-to-Cell’s wholesale carrier model depends on for international expansion.

What the carrier-partnership model means for revenue structure

SpaceX is not trying to become a retail mobile carrier. The commercial model is wholesale infrastructure. SpaceX provides the satellite network and backhaul; the carrier, whether T-Mobile or One NZ, owns the customer, the SIM, and the billing relationship. Revenue is tied to carrier subscriber bases and wholesale pricing, not to hardware margins from dish sales.

This structure avoids the need for SpaceX to acquire and defend its own mobile spectrum in each country. It also reduces competitive friction with carriers, because SpaceX operates as a coverage extender rather than a direct rival.

The structural advantage is geographic. Terrestrial networks cannot economically cover a large fraction of Earth’s surface. Direct-to-Cell targets the incremental value of connectivity where ground-based towers are uneconomic: rural areas, oceans, disaster zones, and aviation corridors. That is a structurally uncontested market segment, and the overlay payload was built on a constellation SpaceX was deploying anyway, making the incremental economics significantly better than a pure-play satellite venture starting from zero.

What broadband connectivity actually is for a satellite company

Starlink’s broadband service and its Direct-to-Cell offering both rely on the same low-earth orbit (LEO) constellation, but the customer experience and the business model differ substantially.

LEO (Low Earth Orbit) refers to the orbital band where Starlink satellites operate, low enough for low-latency communication, high enough for broad geographic coverage from a constellation of satellites. An eNodeB is a 4G LTE base station; each Direct-to-Cell satellite carries one onboard, effectively functioning as a cell tower in space.

Starlink broadband requires a dedicated dish terminal with a phased-array antenna to track rapidly moving satellites. The primary end markets are residential broadband in underserved areas, enterprise connectivity, maritime and aviation backhaul, and disaster-response communications. The commercial model is a direct subscription relationship between Starlink and the end customer.

Direct-to-Cell, by contrast, requires no dedicated hardware. It works with standard smartphones through carrier partnerships, and its commercial model is wholesale infrastructure rather than retail subscription.

| Attribute | Starlink Broadband (Dish-Based) | Direct-to-Cell |

|---|---|---|

| Customer device required | Dedicated Starlink dish terminal | Standard 4G LTE smartphone |

| Primary end markets | Residential, enterprise, maritime, aviation | Mobile carriers seeking coverage extension |

| Commercial model | Direct subscription (retail) | Wholesale infrastructure via carrier partners |

| Maturity stage | Operating at scale globally | Early commercial rollout (SMS live, data/voice on roadmap) |

The constellation already numbers in the thousands of satellites, giving SpaceX a scale advantage over any new entrant attempting to replicate either service. That installed base is why the Direct-to-Cell overlay was commercially rational: it leverages existing orbital infrastructure rather than requiring a dedicated network build.

AI compute and custom chips: strategic logic meets execution risk

The Musk ecosystem’s pattern of vertical integration, building in-house what others buy from suppliers, has extended into AI compute and semiconductors. The strategic logic is coherent. Whether the execution can match the ambition is a separate question, and investors need to hold both simultaneously.

xAI’s Colossus GPU cluster, described as among the largest AI training data centres, was expanded significantly during 2024-2026 and reportedly supports training for xAI’s Grok models. Agreements with external partners including Google and Anthropic for capacity access have been reported, with leasing arrangements valued in the billions cumulatively.

The Colossus GPU cluster is now a confirmed S-1 disclosure rather than a reported figure: the filing names Nvidia as primary supplier across both Colossus I and Colossus II, with approximately 320,000 accelerators across H100, GB200, and GB300 generations and a combined planned capacity of one gigawatt, giving investors a direct primary source for the infrastructure claims embedded in most SpaceX valuation models.

SpaceX’s connection to this compute infrastructure sits primarily through ecosystem relationships, including siting, power, and Starlink backhaul arrangements, rather than through a fully independent, disclosed compute-leasing business within SpaceX itself.

What is validated versus what remains reported but unverified:

- Validated: Global shortage of high-end AI compute (GPU capacity) as the market context driving demand for large clusters

- Validated: Tesla’s Dojo chip programme as the closest precedent for Musk-ecosystem vertical integration in semiconductors

- Reported but unverified: Specific leasing agreements with Anthropic and Google valued in the billions cumulatively

- Early stage: TerraFab-style chip initiatives described in filings and commentary as under development or evaluation as of 2026

The Vision for Space-Based Compute

The concept of space-based compute carries structural appeal: abundant solar power, natural radiative cooling, and the ability to sidestep terrestrial permitting constraints that increasingly slow hyperscale data centre development. Starship’s substantially higher payload capacity could enable such large-scale orbital applications.

The counterbalancing constraints are substantial. Latency to and from orbit limits which AI workloads make sense in space. Radiation hardening, maintenance, and reliability challenges remain non-trivial engineering problems. There is no meaningful revenue from space-based compute today.

From a valuation perspective, orbital compute belongs in low-probability, high-upside scenario analysis rather than base-case cash-flow modelling. It is best understood as a speculative proposition contingent on Starship achieving routine, low-cost orbital access.

Mapping SpaceX’s segments the way an investor should

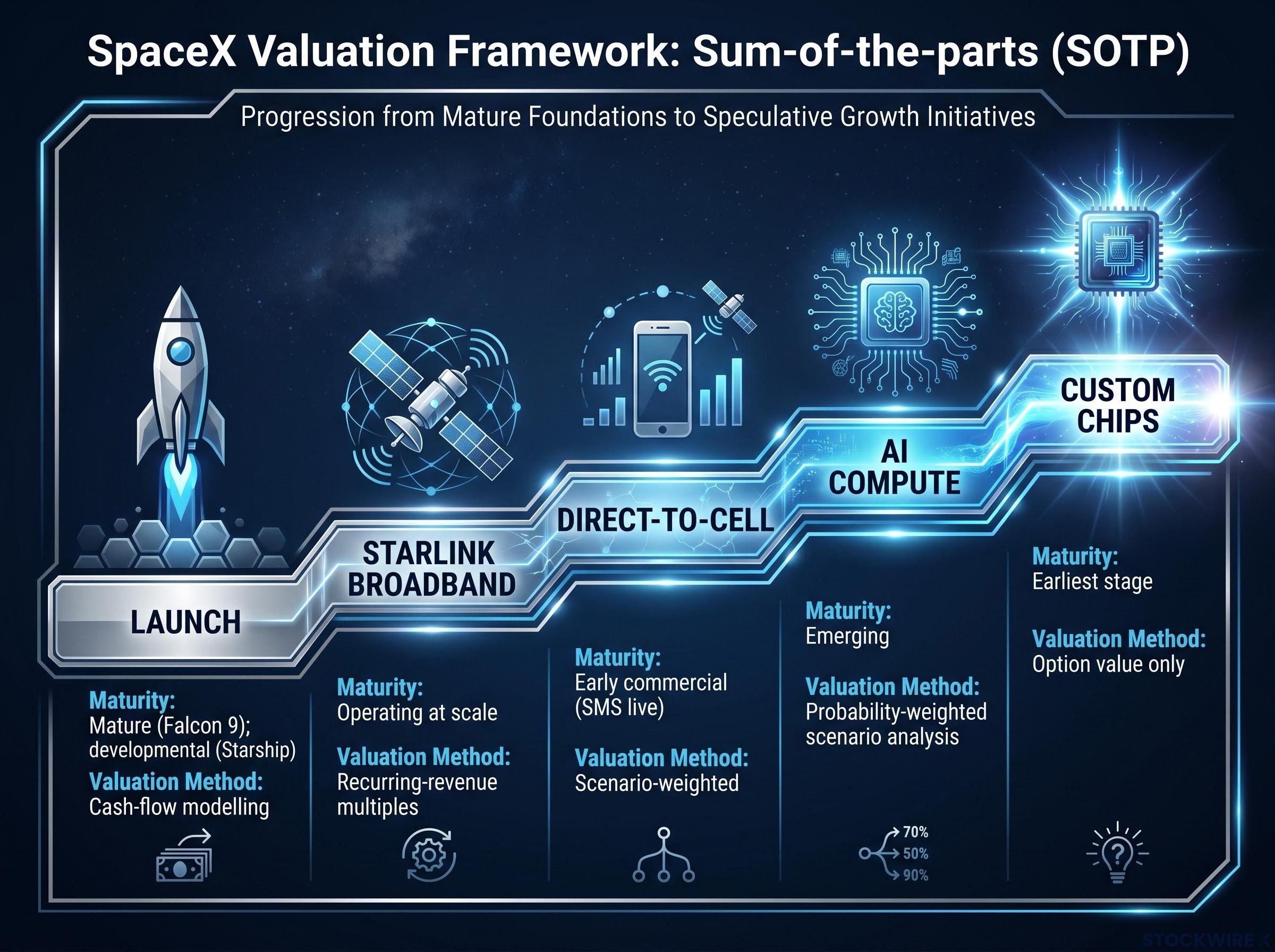

A company with discrete business lines at different stages of development requires a valuation framework that respects those differences. Sum-of-the-parts (SOTP) is the appropriate starting methodology: value each segment separately using relevant comparables, then aggregate with adjustments for overhead and capital structure.

Sum-of-the-parts valuation works because terminal value assumptions, which typically drive 60-80% of a DCF model’s total implied output, can be calibrated separately for each segment rather than applied as a single blended growth rate across businesses at fundamentally different stages of maturity.

The analytical discipline lies in matching the right valuation method to each segment’s maturity. Cash-flow modelling is plausible for launch and Starlink broadband, where revenue is recurring and the competitive position is established. For compute, chips, and orbital data centres, probability-weighted scenario analysis is more honest, assigning a range of outcomes and a probability of success rather than a single point estimate.

The implied 250x EBITDA multiple at the reported $2 trillion valuation is the arithmetic expression of that optionality premium; multiple analyst assessments have flagged approximately 30% overvaluation risk against current fundamentals, a gap that sits entirely in the probability-weighted scenarios for Starship economics, orbital compute, and the carrier partnership scaling trajectory.

Platform premium vs. conglomerate discount: When a multi-segment company demonstrates that its business lines genuinely reinforce each other, markets may value the whole at more than the sum of its parts (a platform premium). When the segments appear loosely connected or poorly executed, markets often apply a conglomerate discount, valuing the whole at less than the sum.

The synergy thesis is intellectually coherent: Starship could make orbital compute viable; Starlink backhauls AI clusters; custom chips could improve satellite performance and reduce supply-chain dependency. Whether SpaceX can execute across launch, broadband, mobile, compute, and semiconductors simultaneously is the question that determines which side of that premium-discount line the company falls on.

| Segment | What SpaceX does | Maturity stage | Appropriate valuation method | Key risk factor |

|---|---|---|---|---|

| Launch | Falcon 9 and Starship orbital delivery | Mature (Falcon 9); developmental (Starship) | Cash-flow modelling with comparables | Market-size ceiling; Starship timeline risk |

| Starlink Broadband | LEO satellite internet via dish terminal | Operating at scale | Recurring-revenue multiples | Subscriber growth rate; capital intensity |

| Direct-to-Cell | Wholesale mobile infrastructure via carriers | Early commercial (SMS live) | Scenario-weighted with carrier adoption | Carrier pricing power; regulatory pace |

| AI Compute | Ecosystem GPU cluster and backhaul | Emerging; limited independent disclosure | Probability-weighted scenario analysis | Execution risk; unclear SpaceX-specific scope |

| Custom Chips | Space-hardened semiconductors (TerraFab) | Earliest stage | Option value only | Capital intensity; semiconductor expertise gap |

The Core Investment Thesis for SpaceX

The rocket company mental model cannot explain SpaceX’s private valuations. It understates the company’s actual strategic footprint and ignores the business lines where the margin and growth assumptions are concentrated.

The through-line across all segments is vertical integration around mass to orbit, orbital infrastructure, global connectivity, and compute. Starlink Direct-to-Cell already demonstrates the pattern working at one layer: a wholesale infrastructure service built on top of a constellation deployed for another purpose, generating recurring revenue through carrier partnerships with T-Mobile and One NZ.

The investor question is not whether SpaceX is worth its valuation as a launch provider. It is a different question entirely.

Investors who accept the execution risk embedded in SpaceX’s multi-segment ambition but cannot access the IPO at the offering price do have an alternative path: publicly traded space stocks including Rocket Lab, Intuitive Machines, and AST SpaceMobile offer exposure to launch services, satellite connectivity, and direct-to-cell infrastructure through accounts at any major brokerage, with no lockup periods or accreditation requirements.

How much of SpaceX’s space-to-ground infrastructure and compute platform will actually work at scale, and on what timeline?

Execution and focus risk across multiple complex domains, not any single product’s technical feasibility, is the central long-run consideration. The portfolio of business lines is expanding before several new segments have reached full maturity.

Four distinct bets at different maturity stages, held inside one corporate structure

The analytical framework maps to four layers, each requiring a different investor posture:

- Launch as foundation: Mature, cash-generating, but constrained by market size. Model with confidence; do not extrapolate the valuation from here alone.

- Starlink broadband and Direct-to-Cell as proven diversification: Operating revenue (broadband) and early commercial traction (DTC). The wholesale carrier model with T-Mobile and One NZ is the template SpaceX aims to repeat across other layers.

- AI compute and chip ambitions as the credible-but-early layer: Coherent strategic logic backed by ecosystem precedent (Tesla’s Dojo), but limited independent disclosure and high capital-intensity risk. Treat as options, not as guaranteed revenue pillars.

- Orbital compute as the long-horizon option: Low probability, high upside, gated by Starship economics and radiation-hardening challenges. Belongs in scenario analysis, not base-case models.

When evaluating any SpaceX coverage, fundraising announcement, or eventual public market filing, the actionable question is: which of these segments is the analysis actually pricing in, and do the assumptions match the maturity stage? SOTP, applied with discipline about which segments deserve cash-flow models and which deserve probability-weighted optionality, is the methodology that prevents the most common analytical error: treating early-stage ambitions with the same confidence applied to businesses already generating recurring revenue.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding SpaceX’s compute, semiconductor, and orbital data centre ambitions are speculative and subject to change based on technological development, market conditions, and company execution.

—