Until recently, a company listing on Nasdaq under the Net Income Standard could satisfy its float requirement with as little as $5 million in freely tradeable shares. That threshold has nearly tripled to $15 million, closing what advisers privately called the low-float back door to a Nasdaq listing. SEC Release 34-104450, approving rule filing SR-NASDAQ-2025-068 on an accelerated basis, amends Rules 5405(b)(1)(C) and 5505(b)(3)(C) to set a uniform $15 million Market Value of Unrestricted Publicly Held Shares (MVUPHS) floor across all Nasdaq listing standards. The change is already in effect.

What follows explains what MVUPHS actually measures, why the change matters most for companies going public via De-SPAC transactions, and what deal teams need to do differently to ensure a clean listing.

The old float thresholds created a gap that Nasdaq just closed

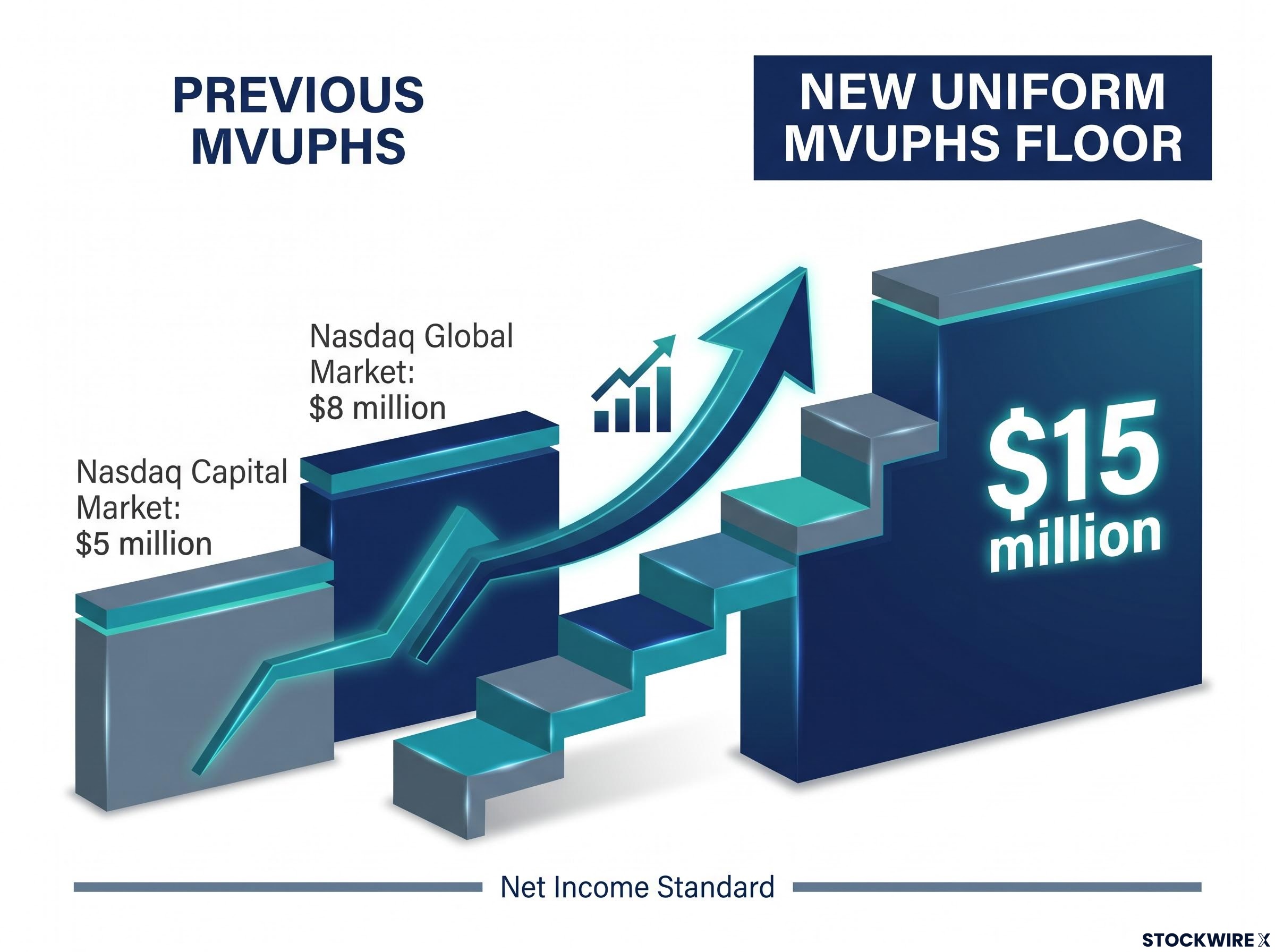

Every Nasdaq listing standard except one already required at least $15 million in MVUPHS. The Net Income Standard was the outlier, and the gap was not small.

On the Nasdaq Global Market, companies listing under the Net Income Standard needed just $8 million in unrestricted publicly held float. On the Nasdaq Capital Market, that figure was $5 million. Meanwhile, the Equity, Market Value, and Total Assets/Total Revenue standards on the same tiers required $15-$20 million.

| Listing Tier | Standard | Previous MVUPHS | New MVUPHS |

|---|---|---|---|

| Nasdaq Global Market | Net Income | $8 million | $15 million |

| Nasdaq Capital Market | Net Income | $5 million | $15 million |

| Both Tiers | Equity / Market Value / Total Assets | $15-$20 million | $15-$20 million (unchanged) |

The asymmetry meant that earnings-positive companies with thin floats could access Nasdaq through the Net Income Standard while bypassing the float discipline every other standard enforced. That path no longer exists.

“A company listing on any Nasdaq tier, under any listing standard, will have to satisfy the MVUPHS requirement of at least $15 million.”

For deal teams that defaulted to the Net Income Standard as the most natural fit for an earnings-positive target, this is not a minor adjustment. On the Capital Market tier, the minimum float requirement has tripled.

When big ASX news breaks, our subscribers know first

MVUPHS is not market cap, and the difference changes everything

Most readers encountering the term for the first time assume MVUPHS is a proxy for market capitalisation. It is not. MVUPHS measures a far narrower slice of a company’s equity: only shares that are simultaneously publicly held (not owned by officers, directors, or affiliates) and unrestricted (not locked up or otherwise limited for resale).

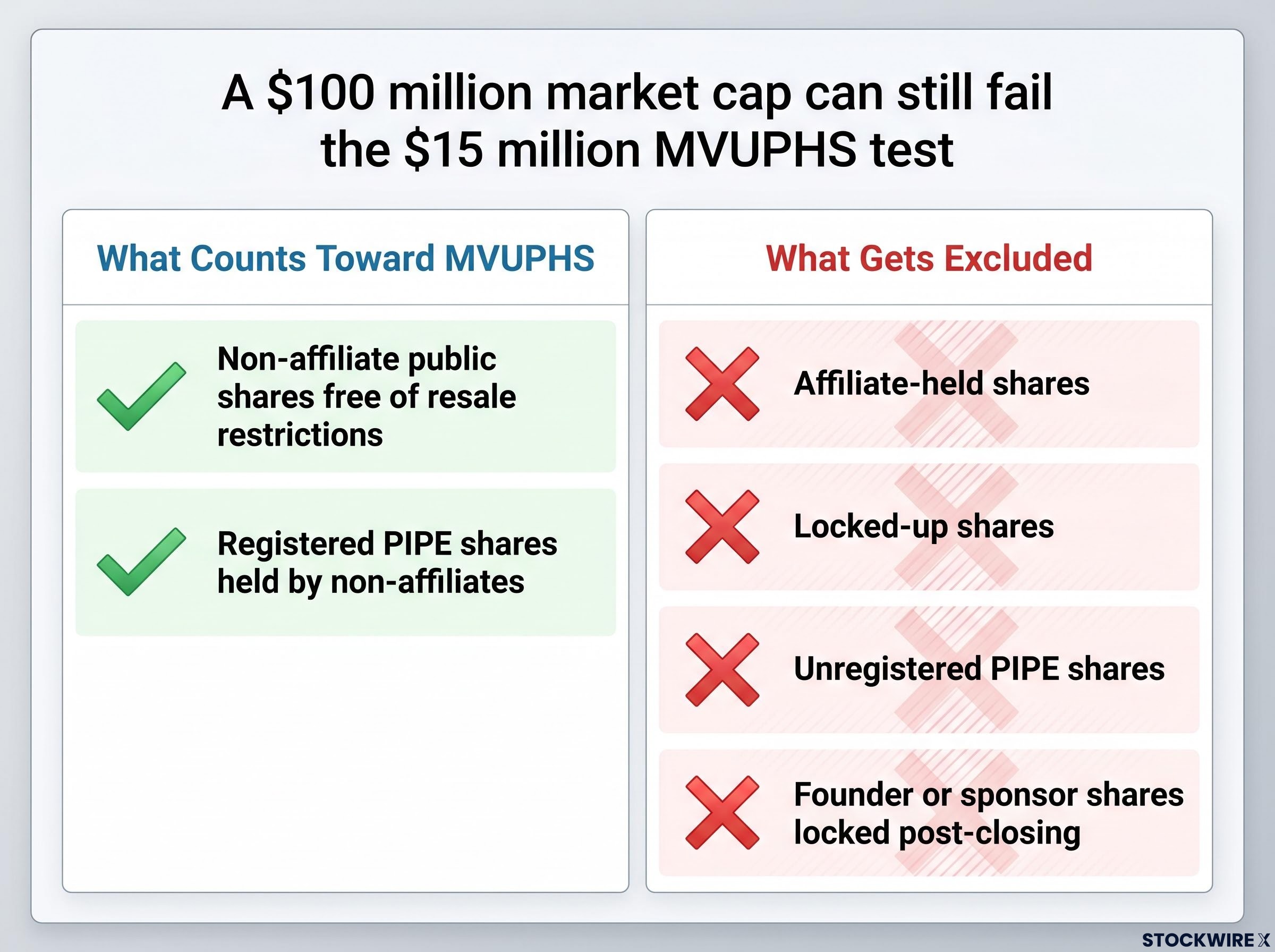

The distinction matters because a company can carry a $100 million market capitalisation and still fail the $15 million MVUPHS test if the bulk of its shares sit in locked-up insider hands. Total equity value counts every share outstanding. MVUPHS counts only the shares that a non-affiliated investor could sell on the open market on day one.

What generally counts toward MVUPHS:

- Non-affiliate public shares free of resale restrictions

- Registered PIPE shares held by non-affiliates, once freely tradeable under an effective registration statement

What generally does not count:

- Affiliate-held shares (officers, directors, controlling shareholders, SPAC sponsors)

- Locked-up shares, regardless of who holds them

- Unregistered PIPE shares

- Founder or sponsor shares locked post-closing

What gets excluded

In a SPAC structure, the exclusion categories are not edge cases. They describe the majority of the cap table. Sponsor founder shares are routinely locked up after closing. Insider equity carries transfer restrictions. Unregistered PIPE shares remain restricted until a resale registration statement becomes effective.

The practical result is that the $15 million MVUPHS threshold must typically be satisfied by a narrow slice of the overall equity, not the full capitalisation figure that appears in a press release.

Why SPAC structures are acutely exposed to this requirement

The rule does not single out SPACs. However, a De-SPAC transaction is treated as an initial listing on Nasdaq, and the combined company must satisfy MVUPHS on its first trading day. Two mechanics embedded in SPAC structures make the $15 million floor a binding constraint rather than a formality.

The MVUPHS requirement sits inside a broader set of IPO mechanics that consistently favour institutional participants over retail investors: allocation priority, information advantages, and lock-up structures all operate to the benefit of insiders who entered at lower prices long before public trading begins.

The first is redemptions. Public SPAC shareholders can redeem their shares for trust value at the business-combination vote. Each redemption removes a share that would otherwise count toward MVUPHS, directly compressing the float even if the combined company’s total enterprise value is unchanged. The pattern of high-redemption SPAC deals is well documented across recent cycles, meaning this risk is structural, not theoretical.

SPAC Research redemption data documents rates consistently approaching 90% across recent deal cycles, giving empirical weight to the argument that redemption-driven float compression is a structural feature of De-SPAC transactions rather than a tail-risk scenario.

The second is founder share lock-ups. Sponsor founder shares are routinely locked up post-closing and contribute zero to MVUPHS on day one. A substantial portion of a typical SPAC cap table consists of sponsor and insider equity, none of which qualifies.

These two dynamics compound:

- The redemption vote reduces public shares available for MVUPHS.

- Founder and sponsor lock-ups remove another block entirely.

- The pool from which MVUPHS can be drawn shrinks to non-redeemed public shares plus registered, freely tradeable PIPE shares.

- If that pool falls below $15 million, the listing fails the initial requirement.

“The entire $15 million MVUPHS requirement often must be met solely from non-redeemed public SPAC shares plus registered, freely tradeable PIPE shares.”

Float risk is now embedded in the mechanics of a De-SPAC transaction itself. It is not an afterthought at listing.

PIPE financing as the float gap’s primary repair tool

PIPE (Private Investment in Public Equity) financing gives De-SPAC issuers a planning lever that conventional IPOs lack. Once PIPE shares are registered for resale under an effective registration statement and held by non-affiliates without lock-ups, they generally count toward MVUPHS. The PIPE can therefore be sized specifically to backfill the MVUPHS lost to redemptions.

Three conditions must be met for PIPE shares to count:

- Shares must be held by non-affiliates

- Shares must be registered under an effective resale registration statement

- Shares must be free of contractual transfer restrictions

If redemption modelling shows a shortfall, the PIPE should be sized so that registered PIPE shares plus residual public shares together reach at least $15 million of MVUPHS on the first trading day.

The complication is timing.

Getting the timing right

Until the resale registration is effective, PIPE shares remain restricted and do not count toward MVUPHS. Registration timing is therefore a deal-structuring variable, not an administrative afterthought.

PIPE terms, lock-up periods, and registration rights must all be coordinated so shares are freely tradeable by the first day of listing. Contractual lock-ups imposed on PIPE investors, even on shares that are technically registered, will exclude those shares from MVUPHS until restrictions lapse. A PIPE that closes on time but registers late creates a float gap that the issuer cannot fill retroactively.

Five structuring moves that reduce listing risk under the new threshold

The De-SPAC timetable (S-4/F-4 review, shareholder vote, closing) provides a predictable window to refine MVUPHS modelling and adjust deal elements before commitments are locked in. That window is a material advantage over a conventional IPO, but only if deal teams use it deliberately.

- Lock in the listing standard early. Determine whether the combined company will list under the Net Income Standard or an alternative, and confirm the associated MVUPHS requirement. This choice drives every subsequent float calculation.

- Run multi-scenario redemption modelling. Test 50%, 75%, and 90% redemption rates against the $15 million floor. If MVUPHS fails in the downside case, the deal structure needs adjustment before the shareholder vote.

- Size the PIPE as a float-building instrument. Design PIPE proceeds to serve MVUPHS compliance, not just the capital plan. A PIPE that funds operations but does not deliver freely tradeable shares by listing day leaves the float gap open.

- Align PIPE lock-ups and registration rights with the listing date. Registration effectiveness must precede or coincide with the first trading day. Lock-up terms that delay free tradeability, even by weeks, disqualify those shares from the MVUPHS count at initial listing.

- Treat all insider and locked-up shares as zero for day-one modelling. Founder shares, sponsor equity, insider allocations, and locked-up PIPE shares should carry a zero MVUPHS value in every model. Advisory memos stress that overestimating the float is the single most common structuring error in this area.

| Action | When in Process | Why It Matters Under New Rule |

|---|---|---|

| Lock in listing standard | Start of structuring | Determines which MVUPHS threshold applies |

| Multi-scenario redemption modelling | Pre-proxy / S-4 drafting | Identifies shortfall before commitments lock |

| Size PIPE for float compliance | PIPE term sheet negotiation | Ensures registered shares fill the gap |

| Align lock-ups and registration timing | PIPE documentation | Prevents shares from being excluded at listing |

| Zero-value insider shares in models | All stages | Avoids overestimating available float |

The $15 million floor signals where Nasdaq’s quality standards are heading

Nasdaq’s stated rationale for the increase centres on liquidity and trading quality at initial listing. Companies listing with very small free floats under the Net Income Standard were prone to wide bid-ask spreads, elevated volatility, and thin trading. The $15 million MVUPHS floor functions as a liquidity filter, ensuring all newly listed companies have a minimum pool of tradeable shares sufficient to support orderly trading from day one.

The SEC approved the change on an accelerated basis, finding it consistent with Exchange Act requirements to promote fair and orderly markets.

Nasdaq’s fast-track listing rule, effective 1 May 2026, allows qualifying mega-cap companies to enter the Nasdaq-100 within 15 trading days of their IPO, a separate but contemporaneous rule change that signals the exchange is actively adjusting its listing and inclusion mechanics across multiple dimensions simultaneously.

Nasdaq’s $15 million MVUPHS floor is designed as a “liquidity filter,” ensuring all newly listed companies carry a minimum pool of tradeable shares sufficient to support orderly trading from the first day of listing.

Separate reporting indicates Nasdaq has also proposed higher float and proceeds requirements, including a reported $25 million MVUPHS requirement for certain China-based IPOs and De-SPACs, though this separate proposal has not been independently confirmed. If accurate, the $15 million floor may represent a direction of travel rather than a ceiling.

The practical principle is clear: float planning is no longer a compliance checkbox performed late in the De-SPAC process. It is a structuring variable that belongs in the first advisory conversation.

Float is now a first-order question for every De-SPAC listing

The $15 million MVUPHS floor has transformed float from a post-structuring administrative check into a primary deal design variable. Three mechanisms determine whether a De-SPAC clears the threshold: the redemption outcome, PIPE registration timing, and sponsor lock-up carve-outs. These operate as an integrated system. Managing one without the others creates gaps that surface only when Nasdaq applies its initial listing review.

Teams planning a Nasdaq listing under the Net Income Standard should treat MVUPHS modelling as a standing agenda item in every advisory meeting from the moment a SPAC target is identified. The rule change is already in effect. The structuring discipline it demands should be, too.

For readers wanting to understand the full regulatory environment a newly listed company enters on day one, our full explainer on SEC reporting obligations covers the proposed shift from quarterly to semiannual filings, what annual Form 10-K and material event Form 8-K requirements remain intact, and what the information asymmetry concerns raised by critics mean for investors tracking newly public companies.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.