What a $2B Government Equity Stake Means for Quantum Stocks

7 mins ago

On 9 June 2026, two of the world’s largest companies by market capitalisation each shed roughly 8-10% of their value in a single trading session. The very next day, they clawed back 9-15%. No earnings restatement. No lost customer. No product failure. Just 48 hours of AI chip stock volatility that exposed a structural truth most investors in the sector have not fully priced.

Samsung Electronics and SK Hynix both achieved trillion-dollar valuations in May 2026, carried there by the AI memory supercycle. Their two-day swing in early June is not an outlier. It is a diagnostic event that reveals how these stocks actually behave, and why.

What follows unpacks the three specific triggers behind the sell-off and recovery, explains why violent moves are structurally built into AI memory names, introduces the concept of layered concentration risk, and equips readers with five questions to apply to any position in the sector.

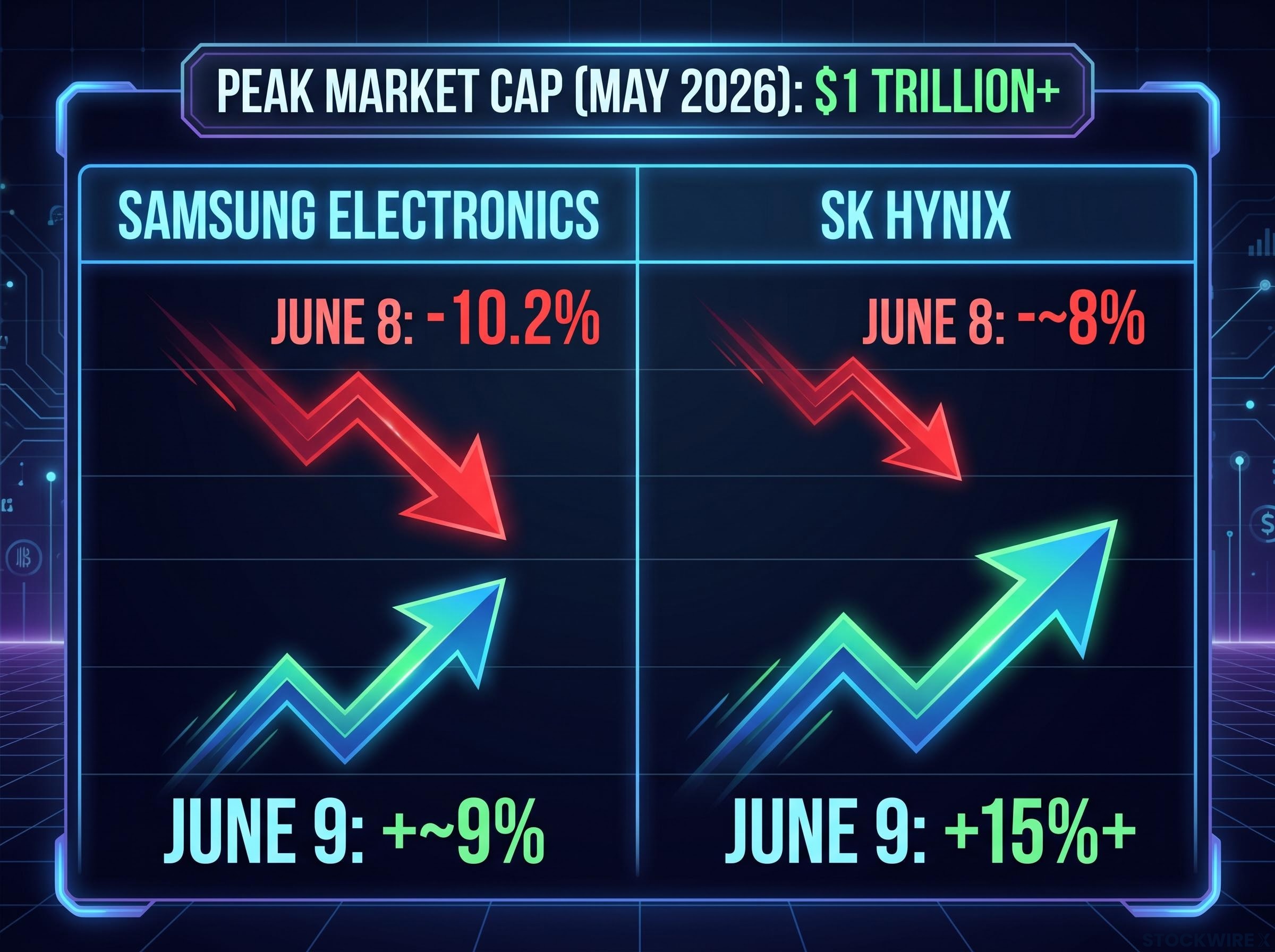

Samsung fell 10.2% on 8 June. SK Hynix dropped roughly 8%. One session later, Samsung advanced approximately 9% and SK Hynix surged more than 15%. The table below captures the full sequence.

| Company | June 8 Move | June 9 Move | Peak Market Cap (May 2026) |

|---|---|---|---|

| Samsung Electronics | -10.2% | +~9% | $1 trillion+ |

| SK Hynix | -~8% | +15%+ | $1 trillion+ |

Three triggers converged on the sell-off:

SK Hynix’s sharper rebound is the detail worth holding. A multi-year supply agreement with Nvidia to deliver high-end memory chips gave buyers a contracted demand signal that Samsung lacked. In a macro scare, contracted revenue acts as a floor, and the market rewarded it with a 15%+ bounce versus Samsung’s 9%.

No company-specific fundamental had changed. The question is why trillion-dollar companies moved this violently on external signals alone.

The June 8-9 swing was not bad luck. It was the predictable output of three structural features baked into how this market operates, each compounding the last.

Companies such as Broadcom, Nvidia, and the major hyperscalers function as forward demand signals for the entire AI hardware supply chain. When Broadcom’s guidance fell short of elevated expectations, the read-through to high-bandwidth memory (HBM), the specialised memory used in AI accelerators, was immediate. If AI server build-outs slow, HBM demand will be lower than the market had just priced in.

The AI chip supply chain concentrates meaningful power in a small number of non-interchangeable layers, with Nvidia, TSMC, ASML, and Broadcom each occupying a position that no competitor can readily substitute, and that structural configuration is precisely what makes a guidance miss from any one node so consequential for downstream memory producers.

Memory producers sit at the “consumables” layer of AI compute. Their earnings are sensitive to each incremental rack of GPUs that gets built, or does not. The market does not wait for DRAM or HBM companies to confirm a slowdown; it marks their future earnings down on the day the bellwether reports.

Samsung and SK Hynix have delivered year-to-date gains exceeding 100% at various points during the AI rally, with SK Hynix surging well over 200% at its peak. A large share of that appreciation reflects multiple expansion: investors paying more for each dollar of expected future earnings, not just earnings themselves growing.

When multiples are stretched, even a modest shift in rate expectations compresses valuations sharply. Future cash flows five to ten years out, discounted at higher rates, are mechanically worth less today. Add geopolitical stress to the rate picture, and the result is a broad risk-off regime in which the most extended, crowded names sell first.

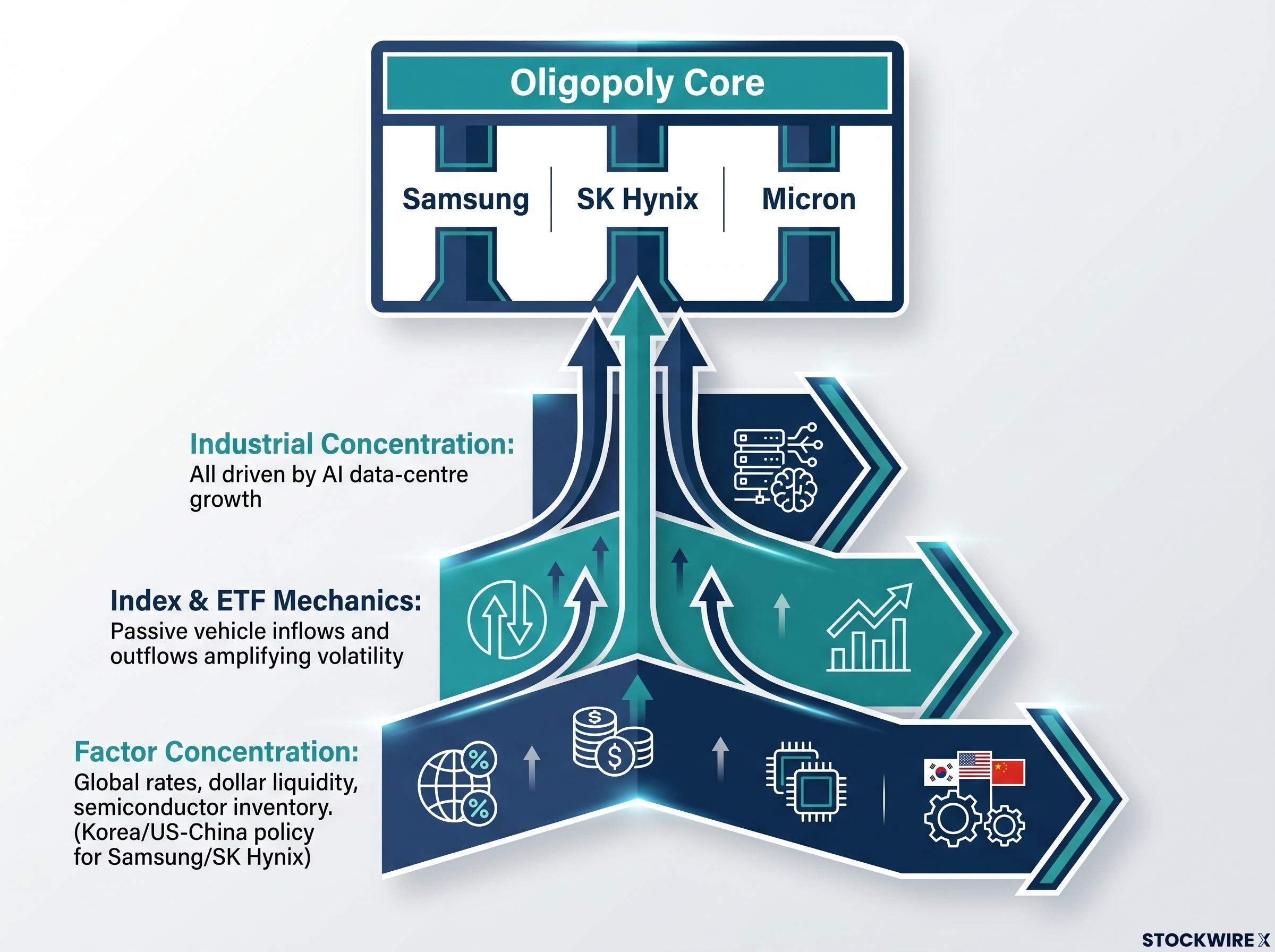

Samsung, SK Hynix, and Micron are the only material suppliers of advanced AI memory. At the high end, HBM for AI accelerators, only these three companies meaningfully supply the market. Barriers to entry are measured in tens of billions of dollars and decades of process expertise.

HBM supply constraints are proving more durable than capital alone can resolve: SK Hynix projects tightness through 2030, industry-wide HBM inventory sits at roughly 3-4 weeks, and all three major producers are sold out through 2026, a supply vacuum that reinforces why the oligopoly chokepoint this article describes is not a temporary feature of the market.

Owning the only three suppliers of AI’s most critical memory component means every macro shock hits the same names simultaneously. There is no fourth or fifth competitor to absorb or dilute the impact.

That scarcity drove the run-up. It also concentrates every negative headline into the same tiny set of stocks, with no shock absorber available anywhere in the market.

Many investors believe they have managed AI memory risk by spreading across multiple names or through exchange-traded funds. The June 8 sell-off suggests otherwise. Three distinct layers of concentration compound on top of each other, and most portfolios are exposed to all three simultaneously.

Position sizing, not stock selection within the sub-sector, is the only real lever investors control when all three layers are correlated in stress events.

On 9 June 2026, while Samsung and SK Hynix were rebounding from the prior session’s sell-off, Applied Digital announced a 15-year lease arrangement with an undisclosed U.S.-based hyperscaler customer. The deal covers 210 megawatts of computing capacity at the company’s new Delta Forge 2 AI campus, with projected revenue of approximately $5.2 billion over the contract term. If extended to 30 years, the total value could reach an estimated $12.7 billion.

Applied Digital shares rose more than 11% in U.S. premarket trading. Following the deal, approximately 70% of the company’s contracted revenue is attributable to large-scale U.S. technology companies.

The contrast with memory manufacturers is instructive. Both are legitimate “AI plays,” but investors who treat them as interchangeable AI exposure are misclassifying risk. A 15-year lease covering 70% of contracted revenue is a fundamentally different instrument from HBM spot-market pricing exposed to quarterly guidance revisions.

| Attribute | AI Memory Manufacturers | AI Data-Centre Lessors |

|---|---|---|

| Revenue driver | DRAM/HBM pricing cycles, AI server build-out pace | Occupancy, power utilisation, long-duration lease rates |

| Contract structure | Mix of long-term agreements and spot-market procurement | Multi-year leases (15+ years) with hyperscaler tenants |

| Volatility profile | Large daily swings on earnings, guidance, rates, demand signals | Lower sensitivity to quarterly chip guidance; exposed to counterparty and infrastructure risk |

| Key risk factors | Bellwether dependency, multiple compression, geopolitical headlines | Technology obsolescence, credit cycles, tenant concentration |

Distinguishing between these profiles gives investors a concrete framework for allocating AI exposure across a risk spectrum rather than treating the theme as a single bet.

AI infrastructure risk stratification extends beyond the memory-versus-data-centre comparison this article draws: power and NAND flash storage represent a third category characterised by physical scarcity and high switching costs, attributes that have historically produced outperformance during technology buildout cycles precisely because they lack the quarterly guidance volatility that defines memory producer stocks.

The following five questions translate the mechanisms this analysis has examined into a repeatable checklist. Each one ties directly to what the June 8-9 sequence revealed.

Samsung and SK Hynix occupy genuinely strategic positions in the AI supply chain. They are oligopoly producers of the memory that AI accelerators cannot function without, and the long-term demand story remains intact after the June 8-9 episode. Both companies reached trillion-dollar valuations in May 2026 for real, supply-scarcity-driven reasons.

The same oligopoly features making these businesses powerful long-term holdings also make their stocks behave like high-beta leveraged instruments on AI capital expenditure and interest rates in the short and medium term. An 8-10% drawdown followed by a 9-15% recovery within 48 hours is not an aberration; it is the volatility regime these structural features produce.

Treating trillion-dollar memory manufacturers as low-beta, sleep-well-at-night mega-caps is a category error, not a minor miscalibration.

They are best understood, and sized, as concentrated, high-volatility instruments on the AI data-centre growth cycle and the interest-rate regime. The thesis may well prove correct over time. The position size is what determines whether an investor survives the path to get there.

For investors who want to translate the position sizing principles in this article into a concrete portfolio structure, our dedicated guide to AI infrastructure allocation walks through a three-layer hardware, cloud, and software framework, with specific allocation percentages, valuation benchmarks for each layer, and the risk parameters that distinguish appropriate sizing for aggressive growth versus core holdings.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

AI chip stock volatility refers to the large, rapid price swings seen in semiconductor and memory stocks tied to AI infrastructure demand. It is extreme because these stocks are sensitive to bellwether guidance misses, rate changes, and geopolitical headlines all at once, as demonstrated when Samsung fell 10.2% and SK Hynix dropped roughly 8% in a single session on 8 June 2026.

Three triggers converged simultaneously: Broadcom delivered disappointing forward guidance that repriced AI hardware demand expectations, rate anxiety and Middle East geopolitical tensions triggered a broad risk-off move, and profit-taking accelerated after both stocks had reached trillion-dollar valuations in May 2026.

SK Hynix had a multi-year supply agreement with Nvidia for high-end memory chips, giving investors a contracted demand signal that Samsung lacked. In a macro-driven scare, contractually anchored revenue acts as a floor, which is why SK Hynix surged more than 15% on the recovery day versus Samsung's approximately 9%.

Concentration risk in AI memory stocks has three compounding layers: industrial concentration (Samsung, SK Hynix, and Micron all move on the same demand factor), index and ETF mechanics that amplify inflows and outflows into the same names, and shared factor sensitivity to rates, inventory cycles, and geopolitical policy. Investors who spread across multiple memory names or hold semiconductor ETFs may still be fully exposed to all three layers simultaneously.

Because AI memory stocks behave as high-beta, leveraged instruments on AI capital expenditure and interest rates, position sizing is the primary risk control available. Investors should map bellwether dependencies, assess how much recent price appreciation reflects multiple expansion rather than earnings growth, identify contractually anchored revenue, and look through ETFs to calculate true concentration before committing to a size.