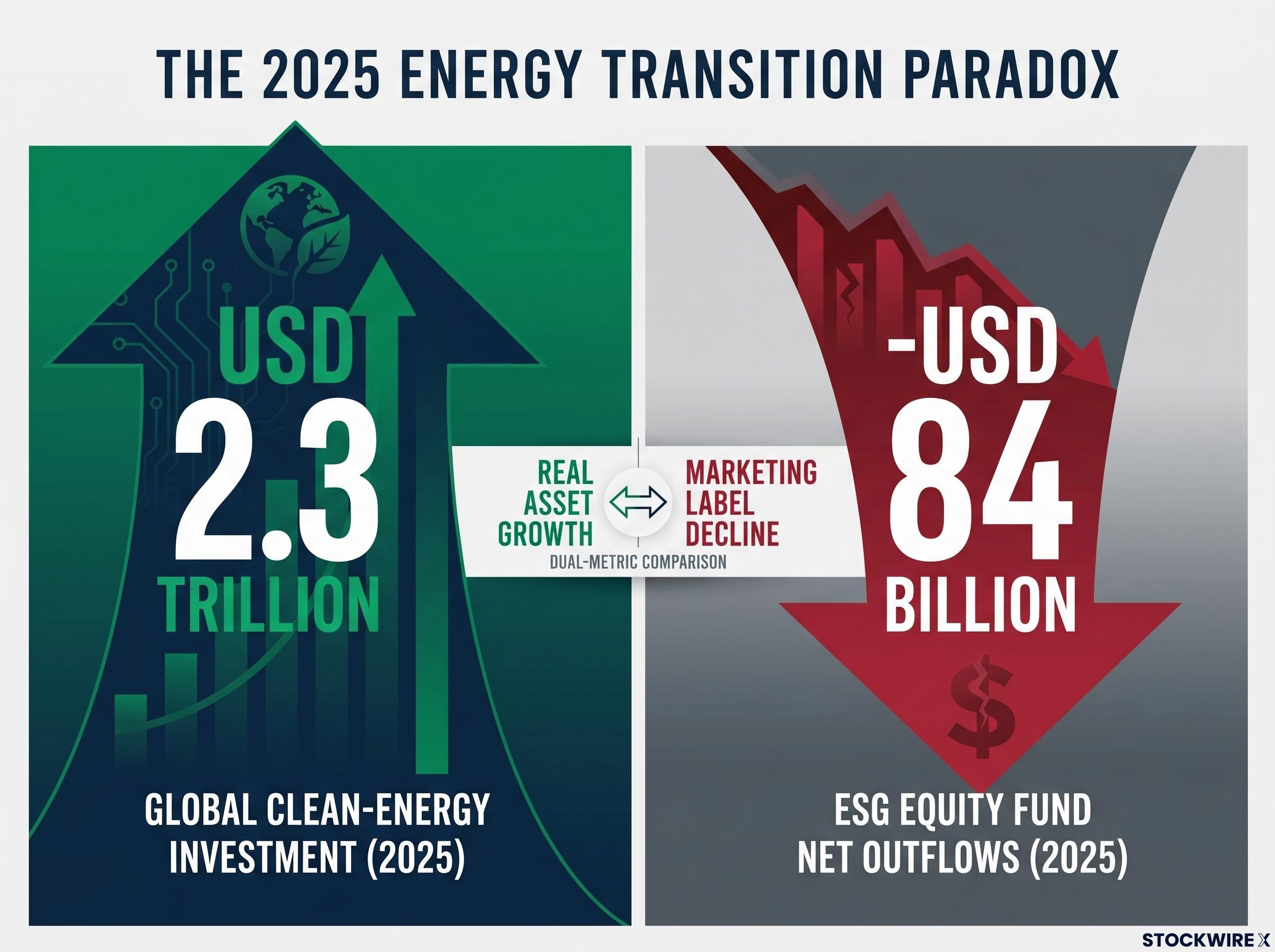

Global clean-energy investment reached USD 2.3 trillion in 2025, a record high by any measure. Over the same period, ESG-labelled equity funds bled USD 84 billion in net outflows, the worst calendar-year figure ever recorded for the asset class.

That paradox sits at the centre of one of the most important questions in global finance right now: does the ESG investing label still matter, or has the energy transition become so large that it operates entirely on its own logic, independent of the marketing category that once defined it? This piece traces the full arc from the 2021 peak through the political and reputational backlash to the present, and explains why understanding the gap between ESG fund flows and clean-energy capital deployment may be the most useful reframe an investor can make in 2026.

From USD 645 billion to backlash: how ESG became a liability

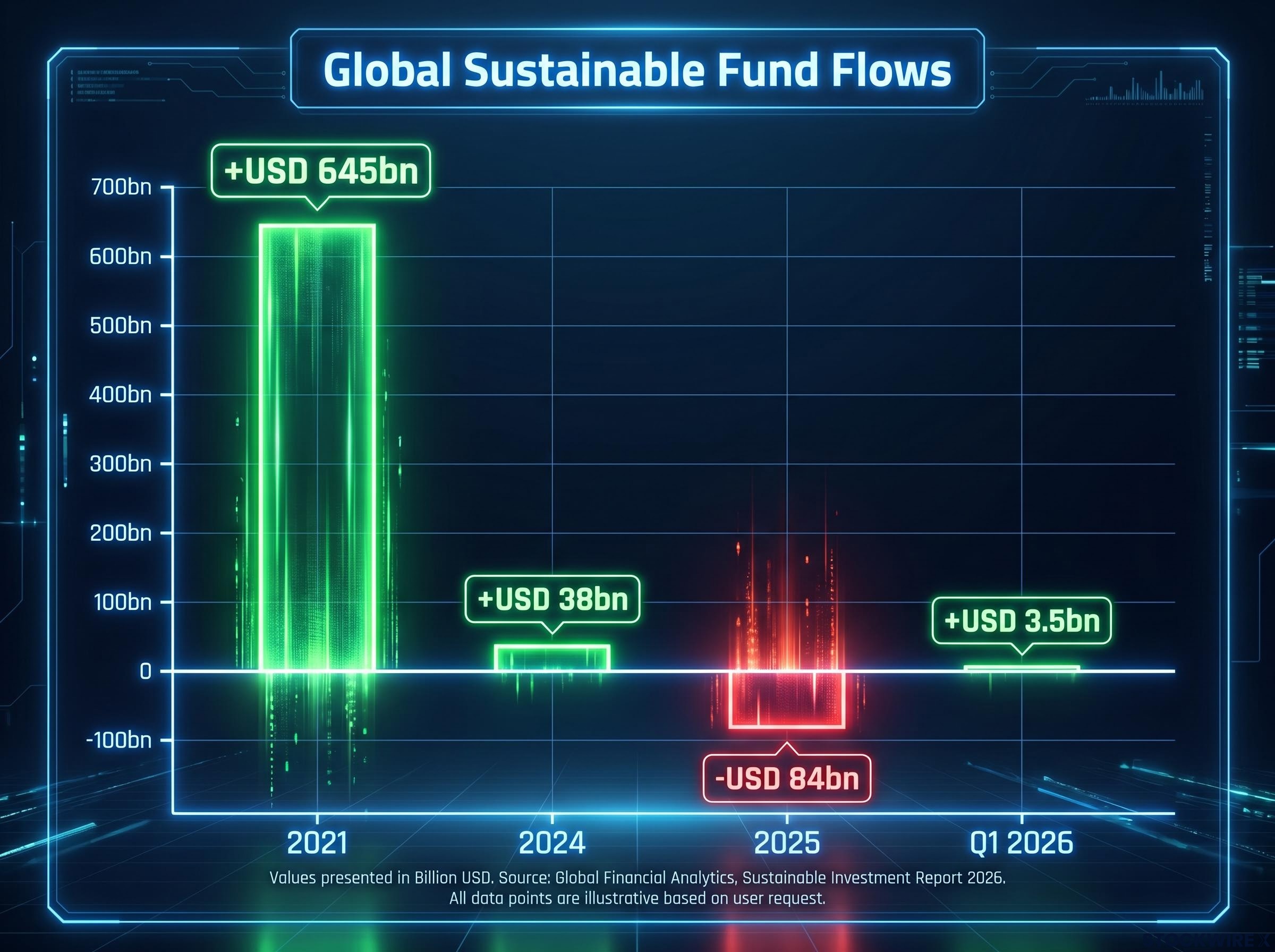

In 2021, global sustainable funds absorbed a record USD 645 billion in net inflows. The number was not merely large; it reshaped product strategies, corporate communications, and regulatory expectations simultaneously. Asset managers raced to rebrand existing vehicles with ESG-adjacent terminology. Governments competed to announce net-zero targets ahead of COP26. For a brief period, sustainability appeared to represent the direction of the financial industry itself.

The shareholder primacy doctrine provides important context for understanding why ESG emerged as a distinct marketing category in the first place: it represented an institutional challenge to a capital allocation philosophy that had, since the 1970s, centred executive incentives and board decisions almost entirely on short-term share price performance.

The reversal was neither gradual nor inevitable. It was driven by four identifiable forces:

- Greenwashing allegations: Regulators and media investigations revealed that many ESG-labelled products held portfolios indistinguishable from conventional funds, eroding credibility.

- U.S. political weaponisation: State-level anti-ESG campaigns turned the acronym into a partisan target, prompting institutions to distance themselves from the label.

- Regulatory scrutiny: The EU’s Sustainable Finance Disclosure Regulation (SFDR) and SEC fund-naming rule tightening forced managers to justify ESG claims with evidence, exposing mismatches.

- Institutional rebranding: Major firms quietly replaced the term in public communications while retaining the underlying analytical frameworks.

BlackRock CEO Larry Fink stated in 2023 that he was “ashamed of being part of this conversation” around ESG, signalling a turning point in how the industry’s largest asset manager positioned itself publicly.

BlackRock shifted toward “transition investing” and “climate-aware” framing. The analytical work continued; the label was the casualty. That distinction matters enormously, because by 2025 the headline figure, USD 84 billion in net outflows, reflected the collapse of a marketing category rather than the abandonment of an investment thesis.

When big ASX news breaks, our subscribers know first

What the numbers actually show about sustainable fund flows

The retreat from ESG-labelled products has been neither linear nor geographically uniform. According to Morningstar, global sustainable funds still recorded USD 38 billion in net inflows in 2024, a figure that contradicts the assumption of a multi-year slide. The real break came in 2025, when outflows accelerated sharply, reaching USD 27 billion in Q4 alone and USD 84 billion for the full year.

| Period | Global Net Flows | Key Driver |

|---|---|---|

| 2021 | +USD 645bn | Record ESG inflows; COP26 momentum |

| 2024 | +USD 38bn | Modest global inflows; Europe resilient |

| 2025 | -USD 84bn | U.S. political backlash; SFDR reclassification |

| Q1 2026 | +USD 3.5bn | Partial rebound led by European focused funds |

The Q1 2026 rebound of USD 3.5 billion is a tentative signal of stabilisation rather than a confirmed reversal. What it does suggest is that the most specifically labelled and focused vehicles may be finding a floor.

Europe versus the United States: two very different retreats

The regional breakdown changes the interpretation considerably. European Article 9 (“dark green”) funds recorded modest net inflows in Q1 2025 even as broader Article 8 (“light green”) products continued to shed assets. SFDR reclassification, not political sentiment, drove much of the European outflow, as regulators forced managers to downgrade loosely labelled funds. The result is a smaller but arguably more credible product set.

U.S. sustainable products experienced persistent outflows through 2025, driven predominantly by political conditions. The pressure was sentiment-based rather than regulatory or performance-based, which makes it potentially more reversible if the domestic political environment shifts.

Morningstar sustainable fund flow data covering the 2021-2025 period confirms the regional divergence at the heart of this analysis: European Article 9 products proved considerably more resilient than U.S.-domiciled sustainable funds, where politically driven sentiment rather than performance or regulatory pressure drove the bulk of recorded outflows.

Why the energy transition does not need the ESG label to keep growing

The scale of real-asset deployment now operates on logic that has little to do with ESG fund flows. According to the IEA’s World Energy Investment 2025 report, clean-energy investment reached approximately USD 2.2 trillion in 2025. BloombergNEF’s Energy Transition Investment Trends 2026 placed the figure at USD 2.3 trillion, up 8% year on year. Total energy investment stood at roughly USD 3.3 trillion, meaning clean energy now represents approximately two-thirds of all new energy capital expenditure globally.

Global clean-energy investment reached approximately USD 2.2-2.3 trillion in 2025, according to the IEA and BNEF, a record high funded overwhelmingly by utilities, corporates, and state entities rather than ESG-labelled mutual funds.

Five structural forces now separate deployment from ESG product sentiment:

- Policy pull: The U.S. Inflation Reduction Act (IRA), EU REPowerEU, and China’s 14th Five-Year Plan lock in multi-year subsidies and tax credits, creating predictable revenue streams that attract mainstream infrastructure capital.

- Cost competitiveness: Solar PV, wind, and batteries are the lowest-cost new power options in most regions on a levelised-cost basis, making the investment case independent of ESG marketing.

- Energy security: The post-2022 energy crisis accelerated government investment in domestic renewables to reduce exposure to imported fossil fuels.

- Corporate transition risk management: Net-zero commitments and disclosure regimes (TCFD/ISSB) drive corporate capital allocation toward clean-energy assets as hedges, regardless of ESG-labelled fund vehicles.

- Scale and liquidity of infrastructure capital: With annual investment exceeding USD 2 trillion, the sector draws generalist infrastructure investors, private equity, and utilities, reducing reliance on ESG-branded funds as the marginal buyer.

The practical implication is that an investor who exited clean energy because ESG fund headlines turned negative may have made a category error, conflating the performance of a marketing label with the trajectory of an economy-wide capital expenditure cycle.

The analytical reframe that most clearly captures the shift is treating climate tech as an infrastructure cycle rather than a venture or thematic theme: when annual investment exceeds USD 2 trillion, the marginal buyer is a regulated utility or pension fund infrastructure allocation, not a retail ESG product.

The gap between listed equities and real-asset deployment

The numbers produce a dissonance that deserves examination before explanation. The S&P Global Clean Energy Index fell approximately 20-25% in 2023 and a further 15-20% in 2024. The iShares Global Clean Energy ETF (ICLN) declined roughly 21% in 2023 and 10-15% in 2024. Several benchmarks remained more than 50% below their 2021 peaks.

Over the same period, annual clean-energy investment reached USD 2.2-2.3 trillion, a record.

| Indicator | 2023 | 2024 | 2025 |

|---|---|---|---|

| S&P Global Clean Energy Index | ~-20% to -25% | ~-15% to -20% | Subdued; below broad market |

| ICLN ETF | ~-21% | ~-10% to -15% | Single-digit rebound; well below 2021 highs |

| IEA/BNEF clean-energy investment | Record growth | Record growth | USD 2.2-2.3 trillion (record) |

The U.S. case is particularly instructive: IRA-related investment commitments in batteries, solar manufacturing, EVs, and hydrogen surged across multiple states during 2023-2025, according to analysis by the Brookings Institution, Rhodium Group, and BNEF, even as U.S. ESG fund outflows accelerated.

Interest rates, valuations, and the clean-energy equity derating

The structural explanation is straightforward. Utility-scale renewables and grid infrastructure are highly capital-intensive and often project-financed with leverage. When real interest rates rose sharply in 2022-2023, equity valuations compressed even as physical deployment accelerated. Many clean-energy names had also entered 2021 at elevated valuations; subsequent earnings disappointments compounded the rate-driven derating.

The investor implication is that owning listed clean-energy equipment manufacturers, which are cyclical, rate-sensitive, and margin-volatile, represents a materially different exposure to the energy transition than owning contracted infrastructure assets or diversified transition vehicles. The same rate sensitivity that punished listed equities in 2022-2024 could become a tailwind if rates normalise, though building an investment thesis around rate predictions alone carries its own risks.

Risks that matter regardless of what you call the thesis

Macro conviction about the energy transition does not eliminate the need for risk management at the product and portfolio level. The following risks are not arguments against the thesis; they are the specific failure modes investors need to price.

- Policy reversal: U.S. IRA implementation risk remains the most discussed near-term concern, while European permitting and taxonomy uncertainty continues to delay projects. These represent execution risks rather than structural reversals of the deployment trend.

- Interest-rate sensitivity: Capital-intensive assets remain vulnerable if real rates stay elevated, compressing project valuations and listed equity multiples.

- Technology and supply-chain concentration: Solar and battery supply chains remain heavily concentrated in Chinese manufacturing, creating geopolitical risk and, simultaneously, potential opportunity for non-Chinese alternatives.

- Valuation cyclicality: Some listed segments may now be fairly valued, but others continue to face earnings volatility and policy-driven boom-bust cycles.

- Permitting bottlenecks: The IEA identifies permitting, grid connection, and planning delays as constraints in advanced economies, capable of reducing project returns even when policy support exists.

- Greenwashing and label risk: Regulatory scrutiny from EU ESMA and the U.S. SEC means mis-labelled funds face enforcement, forced portfolio changes, or asset outflows, regardless of the soundness of the underlying assets.

Greenwashing litigation risk has moved from a theoretical regulatory concern to an active enforcement environment, with the ACCR appeal against Santos testing whether broadly framed net-zero commitments can withstand judicial scrutiny when the Scope 3 footprint covering more than 75% of total emissions carries no binding target.

Past performance does not guarantee future results. Financial projections referenced in this analysis are subject to market conditions and various risk factors.

Beyond the label: how investors are repositioning for the transition economy

The institutional direction of travel is clear, even if the destination remains debated. BlackRock, Schroders, VanEck, and MSCI have all moved toward transition-specific, climate-aware, or impact-oriented framing, normalising ESG analytics as a mainstream risk tool rather than a standalone product category. Schroders frames the shift as moving toward “sustainable value creation” and “transition finance.” MSCI retains ESG as a methodology while shifting focus from broad marketing integration toward explicit objectives: climate transition risk, biodiversity, and governance metrics.

Mandatory climate disclosure regimes are now the primary mechanism through which ESG analytics are being institutionalised: where voluntary TCFD reporting once set the standard, legally enforceable Scope 1, 2, and 3 disclosure requirements are forcing companies to produce evidence rather than narratives, creating a new quality benchmark investors can use to assess transition risk.

Morningstar analysts describe what is underway as a “rebranding” or “narrowing” of ESG, with broad ESG integration falling out of favour as a marketing term while “sustainable,” “impact,” and Article 9/climate-solutions products remain in demand. The Q1 2026 rebound of USD 3.5 billion, concentrated in Europe’s most specifically labelled vehicles, supports this reading.

What “transition investing” looks like without the ESG badge

In practice, the shift means thematic funds focused on grid infrastructure, critical minerals, and electrification rather than generic ESG screens. Private markets and unlisted renewable infrastructure represent the fastest-growing channel, accessible to institutional investors and, increasingly, to retail investors through listed infrastructure vehicles and semi-liquid structures.

The repositioning for investors follows three steps:

- Specific objectives over broad labels: Allocate to climate transition, biodiversity, or governance outcomes rather than a catch-all ESG category.

- Diversified transition exposure over listed clean-energy ETFs: Include infrastructure, private real assets, and regulated utilities alongside public equities.

- Policy-anchored fundamentals over sentiment allocation: Anchor investment decisions to IRA-eligible assets, REPowerEU-supported projects, and cost-competitive technologies rather than fund-flow headlines.

The transition is bigger than the label ever was

USD 2.3 trillion in annual clean-energy investment is not a product story. It is an economy-wide infrastructure cycle, funded by utilities, corporates, state entities, and private capital that operates well below the surface of ESG fund-flow headlines. The label’s decline is therefore largely irrelevant to the trajectory of the capital expenditure it once claimed to represent.

Two specific implications follow for investors. First, distinguish the label from the thesis: ESG fund outflows measure sentiment toward a marketing category, not capital withdrawal from the energy transition. Second, distinguish listed equities from real-asset exposure: weak ETF performance reflects rate sensitivity and valuation cyclicality in a narrow slice of the ecosystem, not a stalling of the broader deployment trend.

The Q1 2026 stabilisation in focused sustainable vehicles, combined with record deployment growth, suggests the most credible and specific parts of the sustainable investing space are finding a new equilibrium. As Schroders has framed it, ESG factors are now embedded in mainstream investment processes, making separate ESG branding less necessary while the analytical work continues.

The question for investors in 2026 is no longer “should I allocate to ESG?” but rather: which part of the energy transition, through which vehicle, anchored to which policy or cost dynamic?

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.