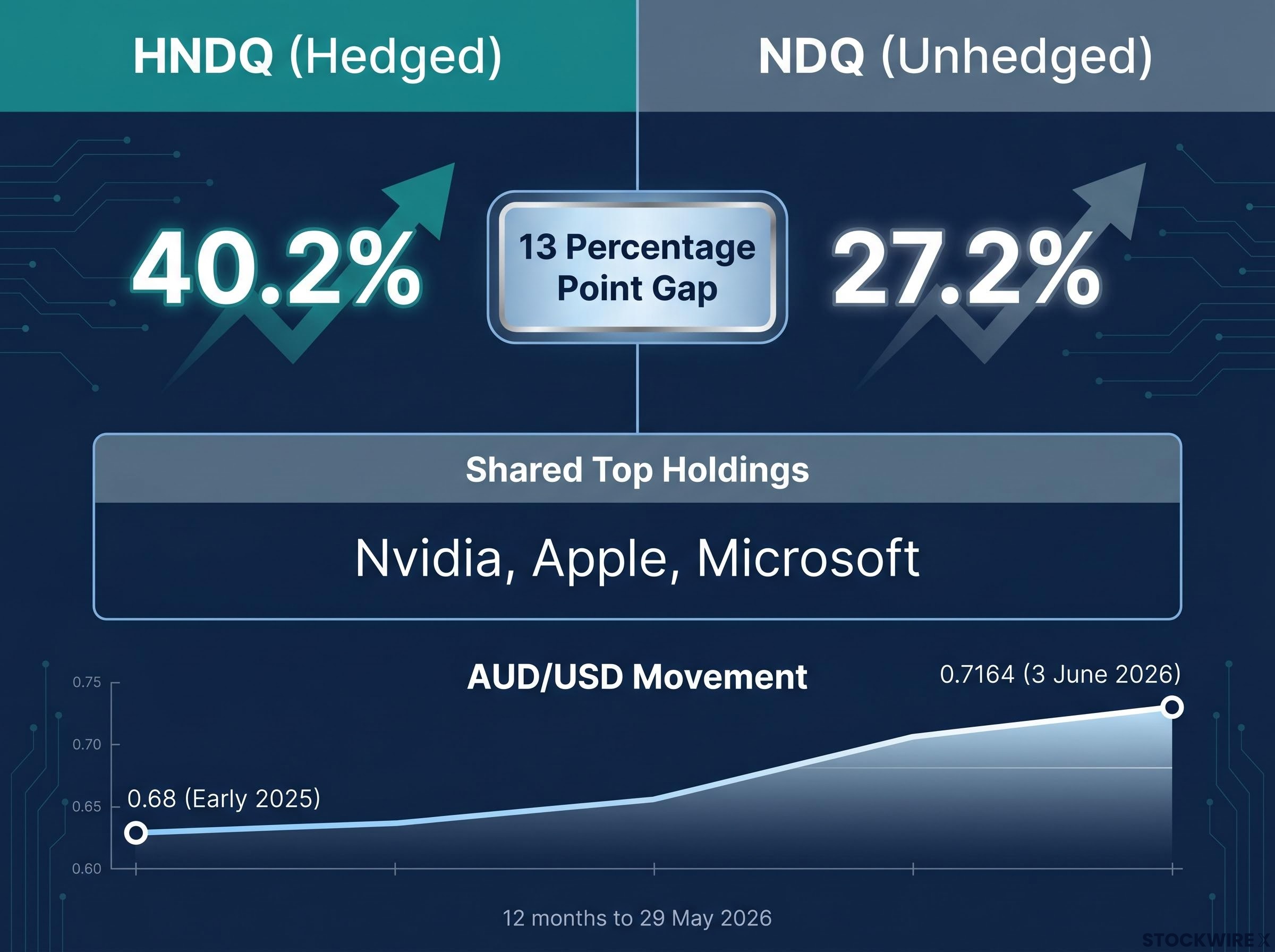

Two ETFs tracking the same index, the same technology giants, the same underlying market. One returned 40.2% over the past year. The other returned 27.2%. The difference was not stock selection, manager skill, or luck. It was the Australian dollar.

Over the 12 months to 29 May 2026, the BetaShares NASDAQ 100 Currency Hedged ETF (ASX: HNDQ) outperformed its unhedged sibling, the BetaShares NASDAQ 100 ETF (ASX: NDQ), by approximately 13 percentage points. Both funds hold the same stocks: Nvidia, Apple, Microsoft, and the rest of the NASDAQ-100. The gap exists entirely because one fund neutralises AUD/USD movements and the other does not. In a year when the Australian dollar strengthened meaningfully against the US dollar, that distinction was worth more than most active stock-picking calls.

What follows uses the HNDQ/NDQ divergence as a case study to explain how currency hedging works inside an ETF, when it helps and when it hurts, and how Australian investors can think through the hedge decision for their own portfolios.

A 13-percentage-point gap from the same underlying index

Start with the holdings. Both HNDQ and NDQ track the NASDAQ-100. Both own the same companies in the same proportions. An investor looking at the top-ten positions of either fund would see an identical list.

Now look at the returns. Over the year to 29 May 2026, HNDQ delivered 40.2%. NDQ delivered 27.2%. Same stocks. Same index. A 13-percentage-point gap.

The 13-percentage-point divergence between HNDQ and NDQ over a single year is among the clearest illustrations of how much currency movements can shape the returns Australian investors actually receive from international ETFs.

The explanation sits in the exchange rate. AUD/USD traded at approximately 0.68 in early 2025. By 3 June 2026, it had risen to 0.7164. That appreciation meant every US dollar of NASDAQ-100 return converted back into fewer Australian dollars for the unhedged NDQ investor. HNDQ, which hedges out that currency movement, captured the full index gain in AUD terms.

| Fund | ASX code | One-year return | Currency treatment | Top holdings |

|---|---|---|---|---|

| BetaShares NASDAQ 100 Currency Hedged ETF | HNDQ | 40.2% | Hedged (AUD) | Nvidia, Apple, Microsoft |

| BetaShares NASDAQ 100 ETF | NDQ | 27.2% | Unhedged | Nvidia, Apple, Microsoft |

For any Australian investor holding international ETFs, this gap illustrates that currency movements can overshadow the differences created by fund selection or tactical allocation.

When big ASX news breaks, our subscribers know first

What currency hedging inside an ETF actually does

Two funds, same stocks, different returns. The mechanism behind the gap is the currency hedge, and understanding how it works removes the mystery from every hedged-versus-unhedged comparison an investor will encounter.

Currency-hedged ETFs use financial instruments called FX forward contracts to neutralise the impact of exchange-rate movements. An FX forward is an agreement to exchange one currency for another at a predetermined rate on a future date. The effect is to lock in the exchange rate so that the fund’s AUD return tracks the underlying USD index performance rather than incorporating AUD/USD swings.

The mechanics follow a clear sequence:

- The ETF purchases USD-denominated assets (the NASDAQ-100 constituents).

- The fund simultaneously enters an FX forward contract to sell USD and buy AUD at a predetermined rate.

- When AUD strengthens over the period, the gain on the forward contract offsets the currency drag that would otherwise reduce the value of the underlying USD assets when converted back to AUD.

- The investor receives a return that closely reflects the NASDAQ-100’s performance in USD terms, regardless of where AUD/USD moved.

For the unhedged NDQ investor, no such contract exists. Each USD of return is converted at the prevailing spot rate. When AUD rises, the conversion yields fewer Australian dollars than it would have at the start of the period, creating a drag on the reported return.

The cost of maintaining the hedge

Hedging is not free. Fund managers must roll forward contracts periodically, typically on a monthly basis, and these roll costs introduce a small but persistent expense. Hedged ETFs also tend to carry slightly higher management expense ratios than their unhedged equivalents to cover the operational cost of maintaining the hedge.

The cost is typically modest in absolute terms. Over multi-year holding periods, however, it compounds and should be factored into any like-for-like comparison. Tracking error, the small divergence between the hedged ETF’s return and the underlying index return, is another imperfection that results from the mechanics of rolling contracts and timing mismatches.

Management expense ratios for hedged ETFs typically sit a few basis points above their unhedged equivalents, and while this gap appears trivial in isolation, Morningstar research identifies fees as a more reliable predictor of long-term relative returns than past performance, making the cost difference a factor worth quantifying before committing to a structure.

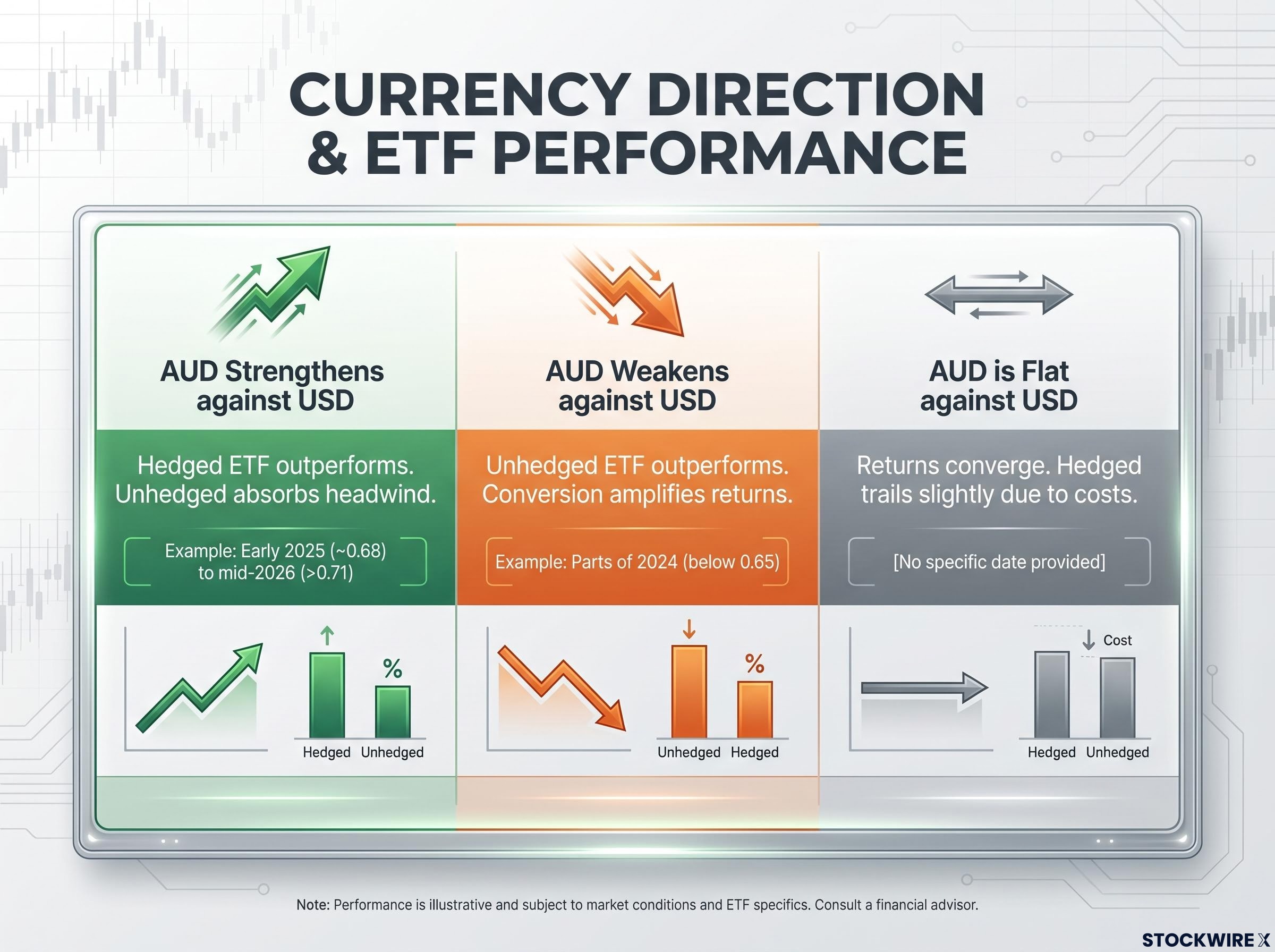

When the AUD rises, hedging wins. When it falls, hedging costs you.

The 13-percentage-point HNDQ advantage is a product of a specific AUD/USD path over a specific 12-month window. It is not evidence that hedged funds are structurally superior.

The logic is symmetrical. AUD/USD rose from approximately 0.68 in early 2025 to above 0.71 by mid-2026. That appreciation penalised the unhedged NDQ investor and left the hedged HNDQ investor unaffected. Had the Australian dollar weakened over the same period, the relationship would have reversed entirely: NDQ investors would have received a currency tailwind, and HNDQ would have trailed.

The hedged fund outperforms when the Australian dollar strengthens. The unhedged fund outperforms when the Australian dollar weakens. The NASDAQ-100 itself is the same in both cases. The only variable is currency direction.

Historical context reinforces the point. AUD/USD traded below 0.65 in parts of 2024, a period that would have favoured unhedged exposure. The three scenarios map cleanly:

- AUD strengthens against USD: the hedged ETF outperforms because the unhedged fund absorbs a currency headwind.

- AUD weakens against USD: the unhedged ETF outperforms because currency conversion amplifies returns.

- AUD is flat against USD: returns converge, with the hedged fund trailing slightly due to hedge costs.

The most common mistake investors make after observing a performance gap like this is to chase the recent winner. The “winner” changes with the currency cycle, not with the quality of the fund.

How to think about the hedge decision for your own portfolio

The question is not which fund performed better last year. The question is which structure aligns with an investor’s circumstances. Three variables drive the decision.

Time horizon is the first. Over shorter periods, currency movements can dominate returns. Over 10-plus year horizons, fund manager and academic commentary broadly holds that AUD/USD movements tend to even out, reducing the structural importance of the hedge choice. A retiree drawing down capital over five years faces a materially different currency risk than a 30-year-old accumulating wealth over decades.

AUD-denominated spending needs are the second. An investor who will spend their returns in Australian dollars, paying a mortgage, funding retirement income, covering living costs, is more exposed to the risk that a rising AUD erodes the value of unhedged offshore holdings precisely when those funds are needed.

Volatility tolerance is the third. Hedged funds deliver smoother AUD returns because one source of volatility (currency) has been removed. Unhedged funds introduce an additional layer of return variability that some investors find uncomfortable, particularly in periods of sharp currency moves.

Morningstar commentary has characterised the hedged-versus-unhedged choice as primarily a risk-management decision, not a return-maximisation one.

| Investor type | Time horizon | AUD spending needs | Suggested hedge stance |

|---|---|---|---|

| Retiree or near-retiree | Under 5 years | High | Hedged (e.g., HNDQ) |

| Mid-career investor | 5-15 years | Moderate | Either; match to volatility tolerance |

| Young long-term accumulator | 15-plus years | Low (spending decades away) | Unhedged (e.g., NDQ) generally acceptable |

The role of an explicit AUD view

Some investors layer a directional currency view on top of these structural considerations. If an investor believes AUD will rise further from current levels above 0.71, a hedged fund removes the expected headwind. If they expect AUD to fall, an unhedged fund captures the expected tailwind.

A note of caution is warranted. Currency forecasting is notoriously unreliable, and investors without a high-conviction view on AUD direction are generally better served making the hedge decision on structural grounds (time horizon, volatility tolerance, spending needs) rather than on a directional bet.

AUD/USD movements have been far from linear over this period: the pair fell 98 pips across the Trump-Xi summit in mid-May 2026 alone, with US inflation at a three-year high of 3.8% and crude oil near $102 per barrel combining to pin the Aussie below 0.73, a reminder that the directional currency view underpinning any hedge decision can shift sharply within weeks.

The broader context: why currency exposure matters more than many investors realise

The HNDQ/NDQ gap is a specific case, but the principle extends to every international ETF an Australian investor holds. Returns from any offshore fund have two components: the underlying asset’s return in its local currency, and the AUD/foreign currency exchange-rate movement. Both components can be large, and both can move in either direction.

Currency exposure functions as a second risk factor layered on top of equity market risk. An investor who selects an international ETF based purely on index, fees, and past performance may be overlooking the variable that ultimately shapes half the return outcome in AUD terms.

ASIC MoneySmart guidance on ETFs outlines that international investment returns are shaped by both local-currency asset performance and AUD/foreign currency movements, a distinction that becomes particularly consequential when the Australian dollar moves sharply within an investor’s holding period.

Australian ETF net flows reached a record $53 billion in 2025, according to the BetaShares Australian ETF Review. A growing number of Australian retail investors now hold offshore ETF exposure, many without fully understanding the currency mechanism embedded in their returns.

International ETF flows reached $6.9 billion in Q1 2026 alone, with all generational cohorts shifting toward offshore index products simultaneously, a pattern that makes the currency mechanism embedded in those funds more consequential than ever for a broadening share of Australian retail portfolios.

ASIC’s MoneySmart guidance acknowledges that international investment returns are shaped by both local-currency asset performance and AUD/foreign currency movements. The scale of recent flows makes this a question that applies to a broadening share of the Australian investor base.

Before buying any international ETF, three questions are worth asking:

- Does this fund hedge currency exposure, and if so, to which currency?

- What is the AUD trend against the fund’s underlying currency over the intended holding period?

- Are there AUD-denominated spending needs within the investment horizon that make currency-driven volatility a material concern?

The HNDQ/NDQ gap is a lesson, not a signal

The 13-percentage-point divergence between HNDQ (40.2%) and NDQ (27.2%) over the year to 29 May 2026 is real, material, and entirely explained by the Australian dollar’s appreciation from approximately 0.68 to above 0.71 against the US dollar. Both funds continue to hold the same NASDAQ-100 constituents. The decision between them is a currency-risk decision, not an equity-selection decision.

That gap will reverse in a different currency environment. The investor who switches to HNDQ today because it outperformed over the last 12 months is making a currency bet, not a fund-quality assessment.

The best hedge stance is the one consistent with an investor’s time horizon and spending needs, not the one that outperformed in the last 12 months.

The right response to this case study is not to chase the recent winner. It is to assess time horizon, volatility tolerance, and AUD-denominated spending needs against the framework outlined above, and to choose the structure that fits the investor’s own profile.

International ETF selection involves more than index choice: the ASX 200’s 52% concentration in financials and materials means investors seeking technology or consumer exposure must look offshore, and the currency treatment of those offshore funds then becomes a live structural question rather than a secondary consideration.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Currency movements are inherently unpredictable, and forward-looking statements about exchange rates are speculative and subject to change based on market developments.