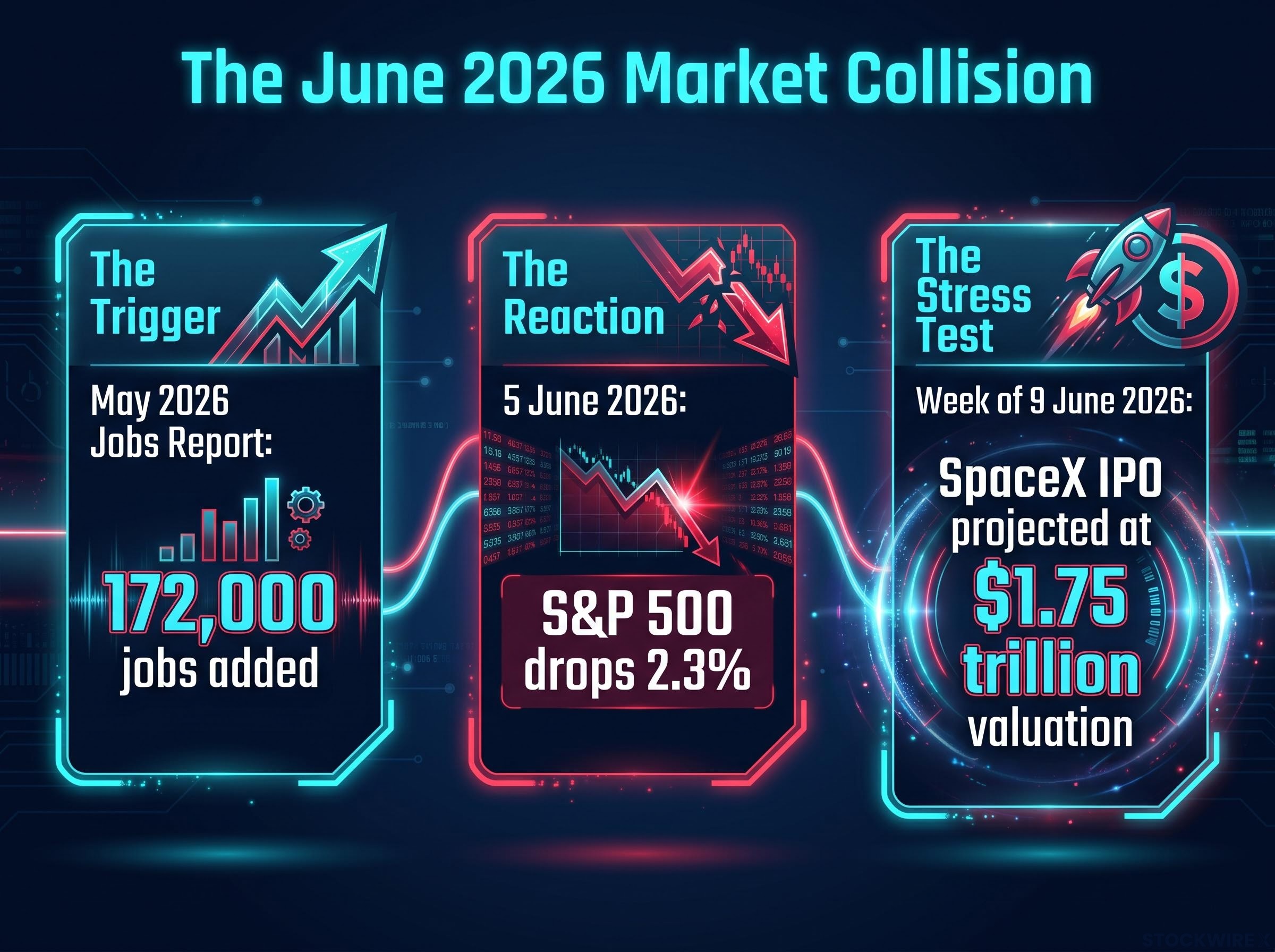

On 5 June 2026, the S&P 500 dropped approximately 2.3% after a single employment figure landed above expectations, and in doing so, it exposed a fault line running beneath the most richly valued corner of the equity market. The trigger was the May 2026 jobs report, which showed 172,000 positions added, a figure that exceeded analyst forecasts and immediately shifted the calculus on Federal Reserve rate cuts. Technology stocks, carrying the highest sensitivity to discount rate changes of any major sector, absorbed the worst of the blow. The timing was not incidental. SpaceX, with a projected valuation of $1.75 trillion, is expected to price its initial public offering during the week of 9 June 2026. What follows is an analytical framework for understanding why strong economic data can punish the sector that benefits most from innovation, why the proximity to the SpaceX IPO transforms this from a routine selloff into a sentiment test, and what the combined signals reveal about risk appetite in mid-2026.

One jobs report, one market jolt: what May’s 172,000 figure actually triggered

The number itself looked healthy. The U.S. economy added 172,000 jobs in May 2026, comfortably clearing analyst expectations, according to Reuters reporting by Noel Randewich. By conventional logic, an economy creating jobs at that pace should support equity valuations. Investors should, in theory, welcome confirmation that consumer spending power remains intact.

The May 2026 jobs report delivered a headline that nearly doubled the 85,000 analyst consensus, with broad-based gains across leisure, local government, and health care lending durability to the figure that markets could not easily dismiss as a statistical anomaly.

That is not what happened.

The paradox in one frame: 172,000 jobs added in May 2026, above expectations. The S&P 500 fell approximately 2.3% on the day.

The gap between those two data points contains the entire story of rate-sensitive markets in 2026.

Why good news becomes bad news in a rate-sensitive market

Strong employment data reduces the probability of near-term Federal Reserve rate cuts. When the labour market shows no signs of cooling, the central bank has less justification to ease monetary policy. Markets had been pricing in some expectation of rate relief; the May jobs print shifted that calculus in a single morning.

The mechanism is direct. When rate cuts become less likely, the discount rate applied to future corporate earnings rises. That repricing hits every equity, but it hits some far harder than others. The S&P 500’s approximately 2.3% decline on 5 June was a broad-market response, not a sector-isolated event, signalling how pervasive the rate-expectation anxiety had become across asset classes.

When big ASX news breaks, our subscribers know first

Why technology stocks carry more rate risk than almost any other sector

The instinct is familiar: when interest rates rise (or stay elevated longer than expected), technology stocks fall harder than the rest of the market. The mechanics behind that instinct are precise and worth understanding, because they determine how any future rate-relevant data release will ripple through portfolios.

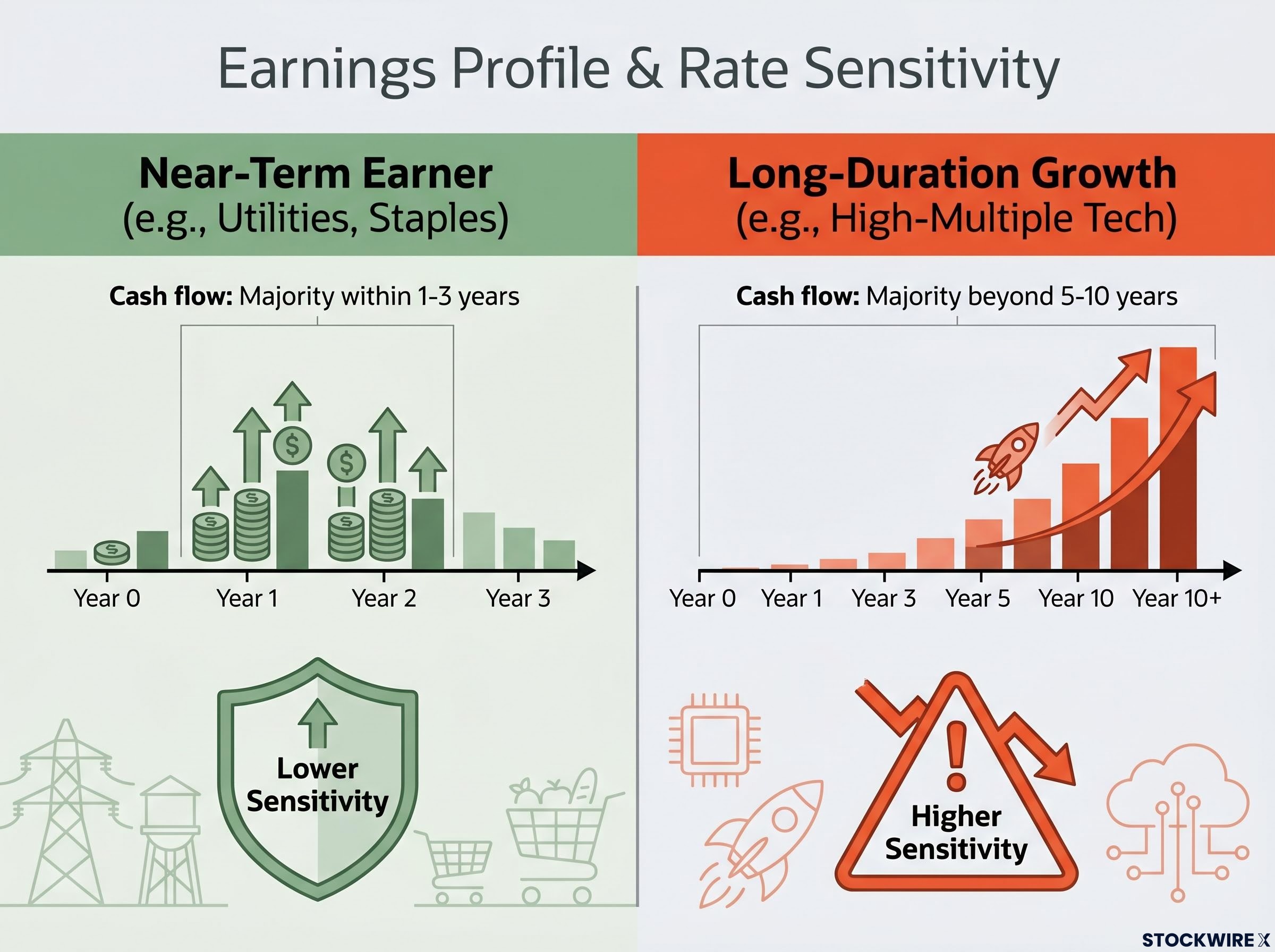

Technology companies derive a disproportionate share of their value from earnings projected years or even decades into the future. In a discounted cash flow framework, the present value of a dollar earned ten years from now shrinks more aggressively when the discount rate rises than the present value of a dollar earned next quarter. A company generating stable near-term cash flows absorbs rate increases with relatively modest valuation compression. A company whose value depends on earnings that have not yet materialised absorbs the same rate increase with far greater price sensitivity.

Peer-reviewed equity duration research on growth stocks confirms the theoretical foundation: long-duration equities, where the majority of value resides in cash flows projected five or more years out, experience disproportionately sharp valuation compression for each unit increase in the discount rate, precisely because the present-value penalty compounds over a longer time horizon.

| Earnings profile | Cash flow timing | Sensitivity to discount rate increase |

|---|---|---|

| Near-term earner (e.g., utilities, staples) | Majority within 1-3 years | Lower: near-term cash flows are discounted less aggressively |

| Long-duration growth (e.g., high-multiple tech) | Majority beyond 5-10 years | Higher: distant earnings compress sharply under rising rates |

Reuters characterised the affected stocks as both rate-sensitive and richly valued. That combination creates a compounding vulnerability:

- Valuation multiples: The higher a stock’s price-to-earnings or price-to-sales ratio, the more dramatic the compression when discount rates move upward.

- Long earnings duration: Future-weighted cash flow profiles amplify the impact of any rate adjustment.

- Momentum-driven positioning: Crowded institutional ownership in high-growth names means selling pressure accelerates when the thesis shifts.

The “higher for longer” interpretation and what it means for Fed watchers

No named Federal Reserve official had commented publicly on the May 2026 jobs print at the time of publication. The market’s reaction was therefore an inference: strong employment data, in the absence of countervailing signals, implies the Fed has room to hold rates at current levels. That inference drove the selling. Until direct Fed communication provides an alternative reading, the “higher for longer” interpretation remains the operative assumption embedded in equity prices.

The SpaceX IPO as a confidence barometer for peak-valued tech

The macro mechanics explain why stocks fell on 5 June. The SpaceX IPO explains why that particular decline carries unusual weight.

SpaceX is expected to list during the week of 9 June 2026 at a projected valuation of $1.75 trillion, according to Reuters. That figure would place the company among the most valuable public listings in history.

The SpaceX pricing details released on June 3, 2026 included a bypassed institutional roadshow, a dual-class share structure giving founders majority voting control, and a total proceeds figure of approximately $75 billion, structural features that add layers of complexity for investors being asked to absorb one of the largest public offerings in history during a risk-off session.

$1.75 trillion. For context, that projected valuation would position SpaceX alongside only a handful of the world’s most capitalised public companies at the time of its debut.

The selloff on 5 June occurred less than a week before a company seeking one of the largest public market valuations in history was set to price. The proximity is not coincidence; it is a stress test. Institutional investors were simultaneously selling richly valued technology positions and being asked to subscribe to an even richer new issue. That tension, between de-risking existing holdings and funding a record-sized newcomer, became visible in the market’s behaviour on Friday.

What a $1.75 trillion ask requires from the market environment

Mega-IPOs of this scale typically price successfully under specific conditions: stable or declining interest rates, broad risk-on sentiment across equities, and positive momentum in the issuing company’s sector. Friday’s action challenged at least two of those conditions simultaneously. Rate expectations shifted higher, and risk appetite across the S&P 500 contracted measurably. Whether investor demand for the SpaceX offering absorbs that headwind or buckles under it will reveal something important about the durability of conviction in peak-valued technology.

Pattern recognition: what history suggests about macro-driven tech selloffs near major IPOs

The structural tension visible on 5 June is not new. Strong economic data and peak-valuation technology have collided before, and the pattern tends to produce the same sequence: a broad selloff, a rapid debate about whether the decline is a buying opportunity or a leading indicator, and a resolution that depends on whether rate expectations shift durably or reverse within days.

The analytical question is clear: was Friday a one-day volatility event driven by a single data print, or does it reflect a more durable repricing of risk appetite across the technology sector?

The June 5 selloff arrived against a backdrop in which growth stocks at a 21% discount to fair value had already been identified by Morningstar as occurring less than 5% of the time since 2011, a starting point that framed the debate between buying opportunity and structural repricing well before Friday’s jobs print.

The breadth of the decline offers one signal. The S&P 500 fell approximately 2.3%, not a narrow semiconductor or AI sub-sector move but a broad index-level contraction. When the selling extends beyond the most rate-sensitive names and into the wider market, it suggests the rate concern is being priced systemically rather than surgically.

Three questions can help investors distinguish noise from signal after any macro-driven tech selloff:

- How broad was the decline? A narrow sector rotation carries less forward weight than a broad index drawdown.

- Did rate expectations shift durably, or was the repricing confined to the session? Multi-day moves in rate futures carry more analytical weight than intraday swings.

- Is the upcoming macro calendar likely to reinforce or reverse the trigger? A string of strong economic prints would compound the pressure; weaker data would relieve it.

What the rate-valuation squeeze means for investors watching the IPO window

Three forces converge heading into the week of 9 June: a jobs print that exceeded expectations, a market now pricing rates higher for longer, and a $1.75 trillion IPO valuation ask arriving into that environment. Together, they form a coherent picture of a risk environment under pressure.

Two competing interpretations of the 5 June selloff will shape positioning in the days ahead:

- The overreaction thesis: The jobs data produced a single-session repricing that will fade as investors recognise the economy’s strength supports, rather than undermines, long-term tech earnings. Under this reading, the selloff is a buying opportunity ahead of a landmark IPO.

- The signal thesis: The breadth and speed of the decline reflect a genuine narrowing of tolerance for peak-valuation technology assets in a higher-rate environment. Under this reading, the SpaceX IPO faces a structurally less receptive market than it would have encountered a week earlier.

A successful SpaceX debut would suggest that institutional appetite for richly valued technology remains intact despite macro headwinds. A disappointing pricing or first-day performance would confirm that Friday’s action was not noise but a forward signal about the limits of investor willingness to pay peak multiples when rates refuse to cooperate.

The core argument: In a higher-for-longer rate environment, the premium placed on long-duration growth assets is inherently fragile. The 5 June selloff made that fragility visible; the SpaceX IPO will determine whether the market can absorb it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

What comes next after the dust settles on one pivotal week in tech markets

The 5 June selloff is best understood not as an isolated bad day but as the market pricing a simultaneous collision of macro headwinds and valuation extremes. 172,000 jobs, a 2.3% index decline, and a $1.75 trillion IPO in the same week compressed three distinct pressures into a single readable signal.

Two data points will determine whether this moment was a turning point or a temporary disturbance: the outcome of the SpaceX listing and the next Federal Reserve communication on rate direction. Until both arrive, the analytical framework remains the same. In a higher-for-longer rate environment, the premium investors place on long-duration growth assets is not guaranteed. Friday made the fragility of that premium visible. The week ahead will test whether the market can carry it.

For investors who want to stress-test whether May’s strength represents durable labour market momentum or a statistical high before a deceleration, our dedicated guide to reading beneath payroll headlines examines the April 2026 data in depth, covering the ISM contraction signals, the involuntary part-time surge, and the leading indicators pointing toward continued softening through Q3-Q4 2026.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.