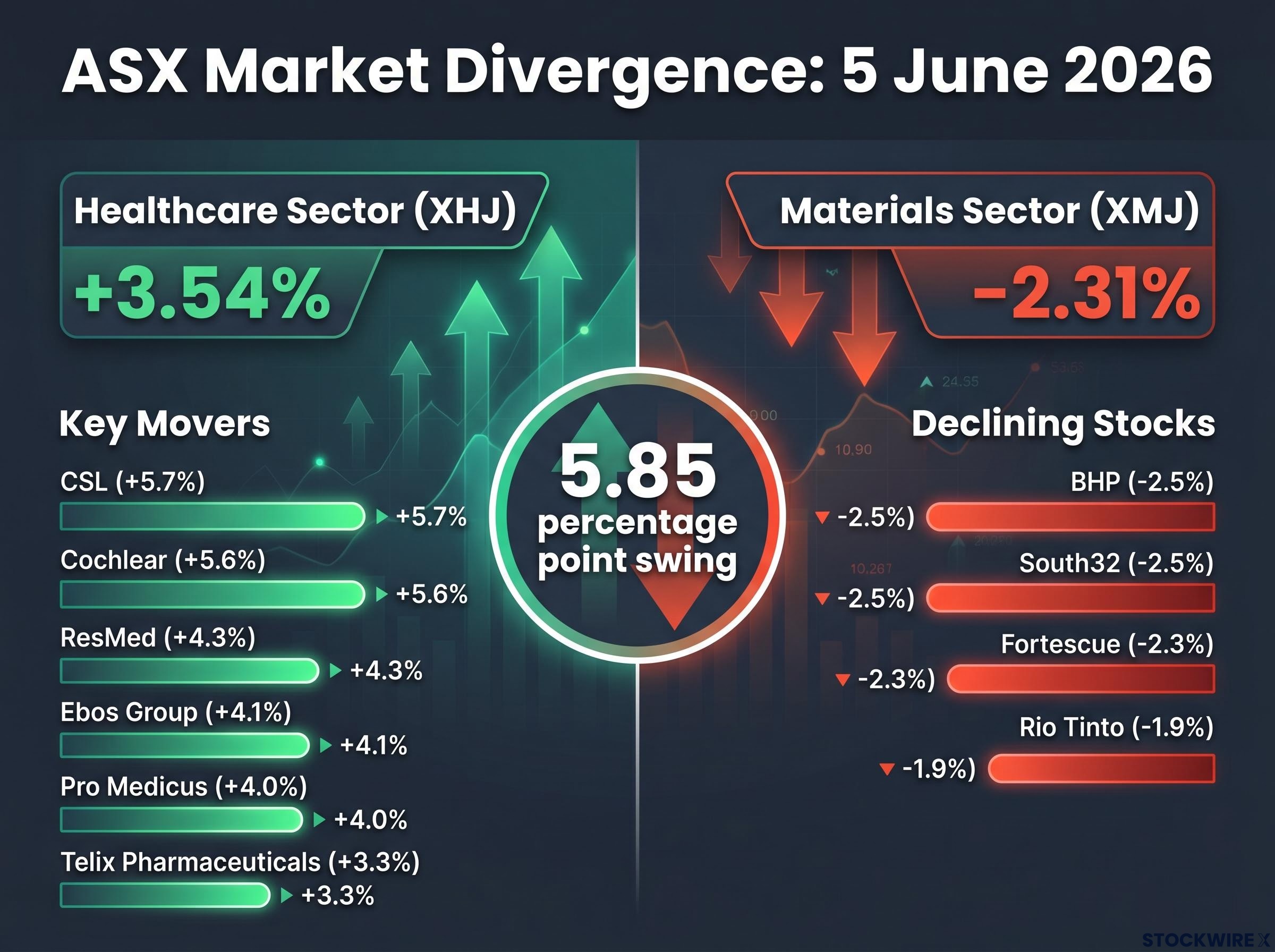

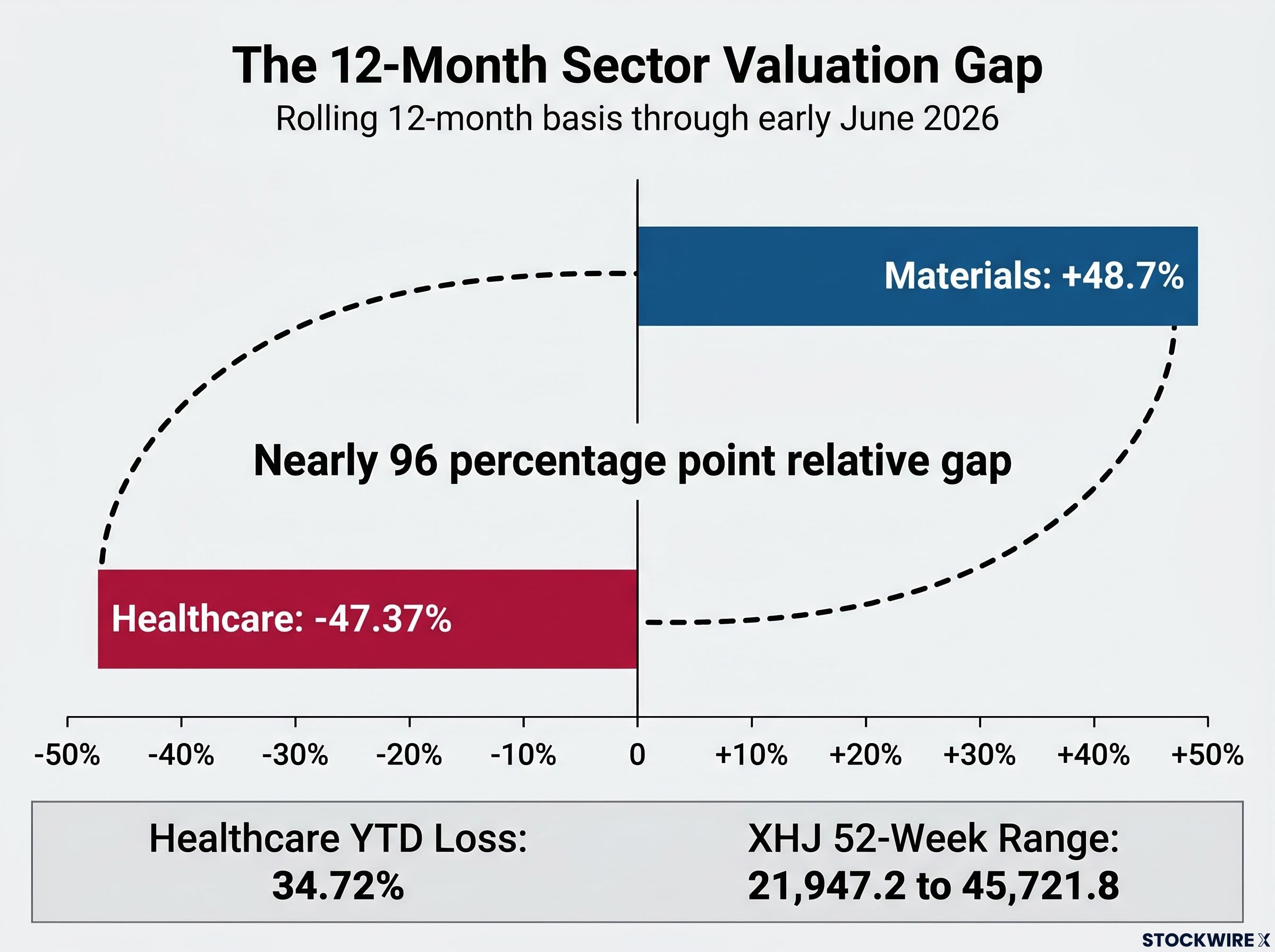

On 5 June 2026, the ASX Healthcare sector posted a 3.54% single-session advance while Materials fell 2.31% on the same day. The divergence between the market’s worst-performing major sector over the prior twelve months and its best amounted to roughly 5.85 percentage points in a single session. That kind of swing does not happen by accident. It reflects a deliberate and rapid repricing by institutional capital, and it arrives at a moment when Healthcare’s rolling 12-month drawdown of approximately 47% has made it the most out-of-favour major sector on the exchange.

Whether that creates opportunity or a trap is the question investors now face. This analysis unpacks what drove the sector’s strongest single-day performance in years, what the concurrent collapse in Materials reveals about the rotation’s mechanics, and what the combination of extreme undervaluation and insider buying activity at CSL actually signals about the sector’s direction from here.

How the 5 June session actually played out across the market

The breadth of the Healthcare advance was the first thing that mattered. This was not a single-stock event dragging an index higher. Six large-cap names gained between 3.3% and 5.7% on the session, with participation spanning diagnostics, therapeutics, medical devices, and distribution.

CSL led with a 5.7% gain to $97.91. Cochlear followed at +5.6% to $100.45. ResMed rose 4.3% to $27.64, Pro Medicus gained 4.0% to $165.64, Ebos Group advanced 4.1% to $16.72, and Telix Pharmaceuticals added 3.3% to $13.31. The ASX 200 Healthcare Index (XHJ) closed at 23,227.2.

The uniformity of gains across names with different earnings drivers, geographic exposures, and subsector classifications pointed to a sector-level allocation decision rather than stock-specific news flow.

The 5 June session did not emerge in isolation: the ASX sector rotation on 2 June had already shown institutional capital exiting rate-sensitive domestic positions and entering globally exposed technology and base metals names, meaning the 5 June reversal into defensives represented a second directional shift within the same trading week rather than a standalone event.

The other side of the trade: Materials retreats as metals pull back

The selling was equally broad. The ASX 200 Materials Index (XMJ) fell 2.31% to 24,486.4, with BHP down 2.5%, Fortescue off 2.3%, Rio Tinto declining 1.9%, and South32 losing 2.5%.

Base metals drove the pressure. LME aluminium fell 1.5% to US$3,739 per tonne, LME nickel dropped 2.3% to US$18,375 per tonne, and COMEX copper futures declined 1.7% to US$6.424 per pound. SGX iron ore futures edged 0.4% higher to US$102 per tonne, but iron ore equities fell for a second consecutive session, with Simandou supply ramp-up concerns acting as a persistent headwind.

The defensive character of the session extended beyond Healthcare. Consumer Staples (XSJ) rose 1.13%, led by Coles at +1.9% and Woolworths at +1.2%. Utilities (XUJ) gained 0.44%.

| Sector / Stock | Move | Close |

|---|---|---|

| XHJ (Healthcare) | +3.54% | 23,227.2 |

| CSL | +5.7% | $97.91 |

| Cochlear | +5.6% | $100.45 |

| ResMed | +4.3% | $27.64 |

| Pro Medicus | +4.0% | $165.64 |

| Telix Pharmaceuticals | +3.3% | $13.31 |

| Ebos Group | +4.1% | $16.72 |

| XMJ (Materials) | -2.31% | 24,486.4 |

| BHP | -2.5% | |

| Fortescue | -2.3% | |

| Rio Tinto | -1.9% | |

| South32 | -2.5% |

When big ASX news breaks, our subscribers know first

Why Healthcare had fallen so far in the first place

The 5 June move landed against a backdrop of severe prior underperformance. The XHJ had declined approximately 47.37% on a rolling 12-month basis through early June 2026, with a year-to-date loss of roughly 34.72%. The index’s 52-week range of 21,947.2 to 45,721.8 illustrates how far valuations had compressed.

Over the same rolling 12-month period, the Materials sector gained approximately +48.7%, creating a relative valuation gap of nearly 96 percentage points between the market’s strongest and weakest major sectors.

The magnitude of Healthcare’s underperformance becomes sharper when set against the Materials sector rally in early May, when lithium stocks including Liontown Resources, Pilbara Minerals, and Mineral Resources were hitting new 52-week highs while Healthcare and Consumer Discretionary were simultaneously producing the most new annual lows on the exchange, a breadth divergence that quantified the valuation gap now being closed.

The decline was driven by macro factors rather than a structural breakdown in the underlying businesses. No single PBS or Medicare policy change has been identified as a primary catalyst for the drawdown. Instead, three forces converged:

- Yield-driven valuation compression: Higher global yields weighed disproportionately on long-duration healthcare growth stocks, where a larger share of expected cash flows sits years into the future.

- AUD/USD dynamics: Currency movements added a layer of complexity for globally exposed names such as CSL, Cochlear, and ResMed.

- Capital rotation toward cyclicals: Persistent institutional flows into Materials and Energy created a sustained funding headwind for Healthcare allocations.

A drawdown caused by macro conditions is, in principle, reversible when those conditions shift. Identifying the cause of the decline is what reframes the recovery question from “if” to “when.”

What sector rotation mechanics mean for Australian equity investors

Sector rotation describes the process by which institutional capital shifts between sectors of the equity market as macro conditions change. On the ASX, the pattern of rotating from cyclical sectors (Materials, Energy) into defensive sectors (Healthcare, Consumer Staples, Utilities) is well-established and tends to occur around turning points in the yield cycle, commodity price momentum, or both.

The mechanism is straightforward. When base metals prices weaken or yields stabilise, the relative earnings growth advantage that justified overweight positions in cyclicals begins to narrow. Capital then flows toward sectors where earnings are less tied to commodity prices, compressing their valuations less and, in many cases, triggering a mean-reversion rally in sectors that had been sold down hardest.

The 5.85 percentage point divergence between Healthcare and Materials on 5 June is a quantitative marker of the rotation’s intensity. The concurrent gains in Consumer Staples and Utilities corroborate the defensive character of the move.

Reading the signal: one session or a structural shift?

A single session cannot confirm a sustained rotation. However, the conditions that would be consistent with a genuine sector leadership change are observable and specific:

- Yield stabilisation or decline: A sustained flattening or fall in Australian and global bond yields would relieve the valuation compression on long-duration healthcare names.

- Commodity price momentum reversal: A continued pullback in base metals (copper, nickel, aluminium) would weaken the relative earnings case for Materials and sustain flows into defensives.

- Broadening insider buying at sector heavyweights: Multiple directors committing personal capital at major healthcare names, as occurred at CSL in May and June, would add a qualitative confirmation layer.

Mean-reversion rotations that begin from extreme relative valuation dislocations tend to be more durable than those triggered by single events. The gap between Healthcare’s -47% and Materials’ +48.7% qualifies as extreme by any historical standard.

CSL as a case study in insider confidence at a sector low

Three disclosed director transactions at CSL between 15 May and 5 June 2026 offer a window into board-level sentiment at a moment when the stock was trading near multi-year lows.

On 15 May 2026, Alison Watkins acquired 2,540 indirect shares at approximately $98.66. On 26 May 2026, Gordon Naylor purchased 1,100 indirect shares at approximately $98.00. On 5 June 2026, a third director bought 1,036 ordinary shares for $99,342 via an on-market transaction.

| Director | Shares | Approx. Price | Date |

|---|---|---|---|

| Alison Watkins | 2,540 | ~$98.66 | 15 May 2026 |

| Gordon Naylor | 1,100 | ~$98.00 | 26 May 2026 |

| Undisclosed director | 1,036 | ~$95.89-$99 | 5 June 2026 |

All three transactions were executed on-market at prices in the $98-$99 range. On-market purchases carry a stronger signal than other forms of director share acquisition (such as dividend reinvestment or option exercises) because they represent personal capital committed at prevailing market prices. When multiple directors act within a three-week window, at consistent prices near multi-year lows, the convergence is one of the more credible qualitative signals available to external investors.

The director purchases occurred after CSL’s fourth guidance downgrade in approximately two years had erased A$9.48 billion in market capitalisation in a single session in May 2026, pushing the stock to nine-year lows and establishing the price range near A$98-A$100 at which all three subsequent on-market director transactions were executed.

CSL’s +5.7% gain on 5 June was its largest single-session advance since February 2022.

The broader corporate context reinforces the signal. CSL maintains an on-market buy-back programme targeting up to USD 750 million, running from September 2025 through 30 June 2026. The operational focus centres on plasma collection margin recovery and ongoing Vifor integration.

For investors wanting to evaluate the CSL recovery thesis at the fundamental level, our deep-dive into CSL’s earnings and margin pressures examines the specific dynamics behind the stock’s 43% decline, including plasma cost inflation, Vifor integration drag, and the broker consensus split on whether A$98-A$99 represents a genuine floor or a valuation that still embeds unresolved execution risk.

Mean reversion or value trap: how to frame the sector’s valuation question

The case for mean reversion is quantitatively compelling. A sector down 47% on a rolling basis, trading near the low end of a 52-week range of 21,947.2 to 45,721.8, with headwinds that are cyclical rather than structural, fits the profile of a deep valuation dislocation that historically precedes outperformance.

The supporting arguments include:

- No identified regulatory or structural shock driving the decline

- Macro headwinds (yields, commodity rotation) that are inherently cyclical and reversible

- A relative valuation gap versus Materials of nearly 96 percentage points, a level consistent with extreme dislocations that have historically attracted mean-reversion capital

Why not all Healthcare names are equal in a rotation

The counter-argument deserves equal weight. The value trap risks include:

- Earnings visibility varies significantly across the sector; some names may screen as cheap for company-specific reasons beyond the macro

- One strong session does not change underlying fundamentals or the rate environment

- A prolonged period of yield pressure could extend the drawdown further, particularly for names with less defensible competitive positions

CSL, Cochlear, and ResMed have global earnings streams and structurally defensible market positions that make them fundamentally different recovery propositions from smaller or more domestically dependent names within the XHJ. Stock selection and earnings visibility at the individual company level, not sector-level index membership, is the variable that separates genuine mean-reversion opportunities from traps.

The rotation’s next test: what to watch in the sessions ahead

The 5 June session presented the ingredients of a genuine rotation. Whether it develops into a sustained sector leadership change depends on observable conditions in the sessions and weeks ahead.

- Base metals trajectory: COMEX copper at US$6.424 per pound, LME nickel at US$18,375 per tonne, and LME aluminium at US$3,739 per tonne are the benchmarks. Continued weakness would sustain the relative case for defensives over Materials.

- Yield direction: Australian and global bond yield movements in the coming weeks will determine whether the valuation compression on long-duration healthcare names continues to ease or reasserts itself.

- CSL buy-back programme end date: The programme’s 30 June 2026 expiry creates a near-term corporate event. Whether it is extended, expanded, or allowed to lapse will signal management’s assessment of the stock’s valuation at that point.

- Follow-through breadth: A sustained rotation requires multiple sessions of broad-based Healthcare outperformance, not a single day. Narrow, single-stock gains in subsequent sessions would weaken the rotation thesis.

One session does not make a rotation, but this one had the right ingredients

The 5 June session displayed the breadth, the counter-directional catalyst, and the insider confirmation at CSL that characterise a genuine rotation rather than a random bounce. Six large-cap healthcare names advanced between 3.3% and 5.7% while Materials fell 2.31% on a base metals pullback, and three CSL directors had committed personal capital at consistent prices near multi-year lows in the preceding three weeks.

Sustained rotation requires macro follow-through that one session’s data cannot confirm. The yield and commodity price trajectories in coming weeks will determine whether this was a turning point or a pause within a longer drawdown.

For investors who have been underweight the space, Healthcare’s position near 52-week lows, combined with the director buying cluster at Australia’s largest listed healthcare company, makes it a sector worth active monitoring from here.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.