Three of the most anticipated private companies in a generation are moving toward public markets within months of each other. SpaceX, Anthropic, and OpenAI, collectively valued at roughly $3.5 trillion, are each advancing through the IPO process in a compressed window that stretches from mid-June through late 2026. The concentration is not just a headline; it is a structural stress test for market liquidity. Steve Brice, global chief investment officer of wealth solutions at Standard Chartered, warned on 2 June 2026 that the near-simultaneous absorption of these listings is expected to create digestion difficulties for equity markets over the summer months. What follows is an examination of the three IPO timelines, the mechanics of market absorption under pressure, and a practical framework for how investors might think about positioning as the wave builds.

Three companies, one compressed window: the IPO pipeline at a glance

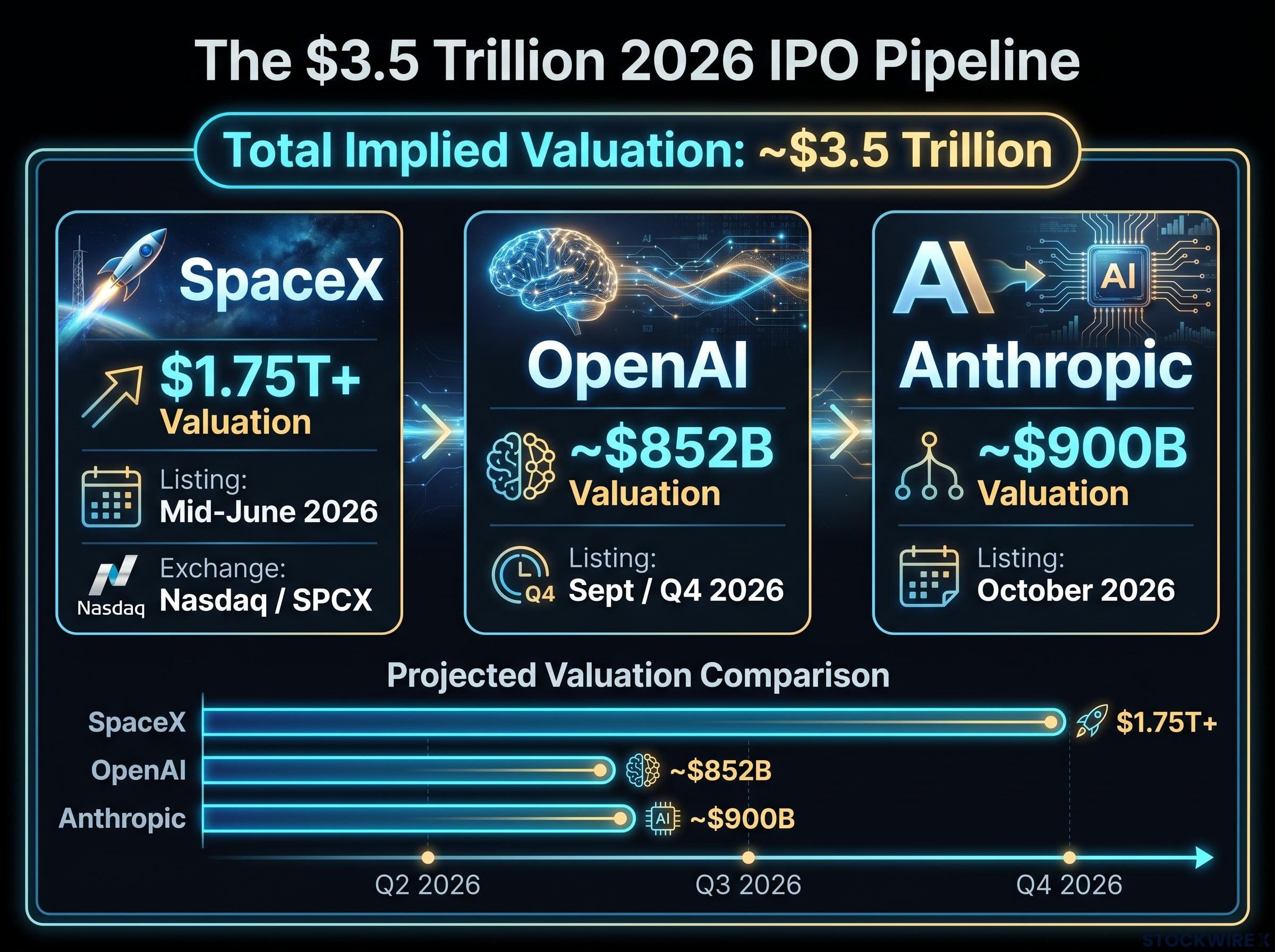

SpaceX is furthest advanced. The company filed its S-1 publicly on 20 May 2026, listing under the ticker SPCX on the Nasdaq. A roadshow is targeted to begin around 4 June 2026, with a potential listing as early as mid-June. Reported valuation discussions reference a range of $1.75 trillion and above.

The valuation range cited in bookbuilding discussions is anchored primarily to Starlink’s financial profile, which generated $8.2 billion in revenue and more than $7 billion in adjusted EBITDA in 2025, making the satellite internet segment the core engine underwriting the $1.75 trillion floor figure rather than the launch business itself.

The SEC S-1 registration process requires companies to disclose financial statements, risk factors, and business descriptions that institutional allocators use to assess demand before a roadshow begins, making the quality and completeness of SpaceX’s public filing a critical input for the capital allocation decisions ahead.

Anthropic follows. Reports indicate the company confidentially filed on or around 1 June 2026, with an October 2026 listing target. Valuation discussions reference a figure of $900 billion in connection with a planned $30 billion capital raise.

OpenAI is working with Goldman Sachs and Morgan Stanley on a draft prospectus, targeting readiness for a September or Q4 2026 listing. The most recently referenced valuation stands at approximately $852 billion.

| Company | Filing Status | Target Listing | Implied Valuation | Exchange / Ticker |

|---|---|---|---|---|

| SpaceX | S-1 public (20 May 2026) | Mid-June 2026 | $1.75T+ | Nasdaq / SPCX |

| Anthropic | Confidential filing (~1 June 2026) | October 2026 | ~$900B | TBC |

| OpenAI | Draft prospectus in preparation | September / Q4 2026 | ~$852B | TBC |

Combined implied valuation across the three companies: approximately $3.5 trillion. Each would individually rank among the largest IPOs in market history. Their proximity within a single calendar year is without precedent.

All timelines and valuations remain subject to change based on market conditions and regulatory review.

When big ASX news breaks, our subscribers know first

What market absorption capacity actually means, and why it matters here

Market absorption capacity refers to the market’s practical ability to allocate capital to new large-scale issuances without materially displacing existing holdings or suppressing broader equity prices. When a single large IPO prices, institutional and retail investors redirect capital from existing positions or deploy new cash to participate. When multiple large listings arrive in sequence, that reallocation pressure compounds.

The mechanics operate through three distinct channels:

- Capital reallocation: Institutional allocators sell or trim existing positions to fund new allocations, creating selling pressure in secondary markets.

- Liquidity displacement: Market-making capacity shifts toward newly listed securities, temporarily thinning order books in established names.

- Sentiment compression: Investor attention concentrates on incoming listings, reducing buying momentum in the broader market during the absorption window.

Liquidity displacement mechanics at the order-book level help explain why large-scale listings compress price discovery in nearby securities: as market-makers redirect capital and attention toward a newly listed name, the passive limit orders that normally underpin price stability in adjacent holdings thin out, widening bid-ask spreads and amplifying intraday volatility across the secondary market.

Steve Brice, speaking on CNBC’s Access Middle East on 2 June 2026, warned that the near-simultaneous absorption of high-profile AI listings is expected to create market digestion difficulties. He characterised his overall stance as not strongly optimistic at the current juncture, with summer 2026 flagged as a period of potential weakness.

How the 2026 AI cluster amplifies the pressure

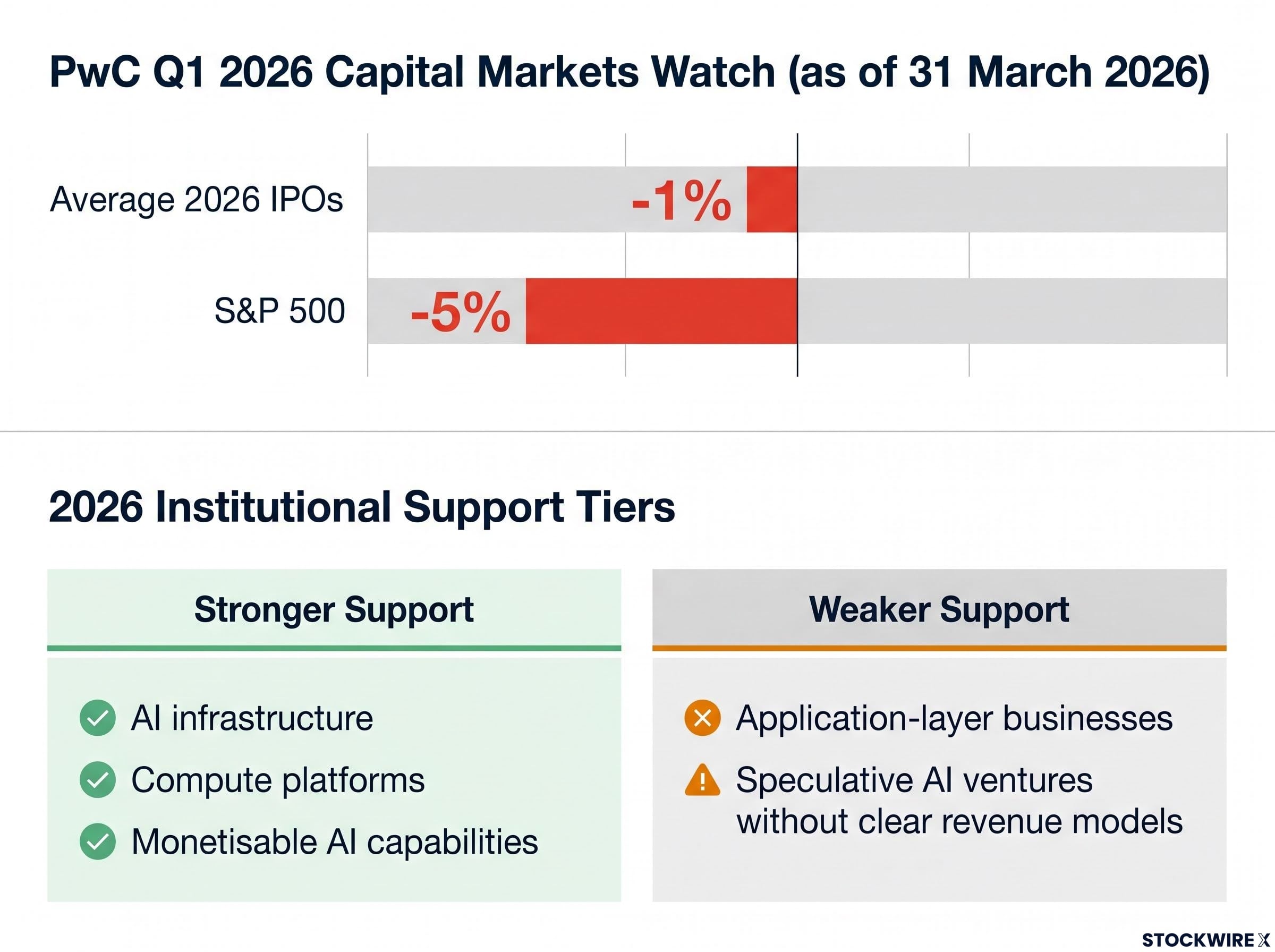

The temporal gap between SpaceX (June) and the Anthropic and OpenAI targets (autumn 2026) compresses the reallocation timeline for institutional allocators. In a typical year, a single mega-IPO might absorb market attention for weeks before capital flows normalise. Here, allocators who participate in SpaceX’s listing in June face a second and third decision point within months. PwC Q1 2026 data shows average 2026 IPO performance down approximately 1% versus the S&P 500 down roughly 5% as of 31 March 2026, meaning IPOs have outperformed the broader index. That relative strength signals demand, but demand under compression behaves differently than demand at leisure.

The 2026 IPO market: strong enough to handle a wave, but not unconditionally

The 2026 IPO market has demonstrated genuine strength. Technology and AI-related offerings have attracted meaningful institutional support, and the relative outperformance of new listings versus the broader index suggests a constructive environment for issuers.

PwC US Capital Markets Watch, Q1 2026: Average 2026 IPO performance down approximately 1% versus S&P 500 down roughly 5% as of 31 March 2026, representing meaningful relative outperformance for new listings.

That strength, however, is selective rather than indiscriminate. Coverage of the 2026 IPO cycle consistently describes investor appetite as discriminating, with a clear two-tier preference structure:

- Stronger institutional support: AI infrastructure, compute platforms, and companies with monetisable AI capabilities.

- Weaker institutional support: Application-layer businesses, speculative AI ventures without clear revenue models.

The preference divide between AI infrastructure versus application-layer companies is not simply a narrative preference; in the first five months of 2026, five infrastructure-layer names at least doubled while application-layer and hyperscaler holdings posted markedly lower returns, a divergence driven by binding constraints in power supply and high-speed interconnect that favour physical-stack companies over software-defined ones.

Technology enthusiasm driven by AI has returned following signs of recovery in 2025, setting a constructive backdrop. The question is not whether the market can absorb large AI listings. It clearly can. The question is whether it can absorb three of this scale in this timeframe without broader market consequences.

Why selectivity matters more when scale is this large

In a normal IPO market, selectivity filters out weaker performers but does not meaningfully constrain total capital absorption. When individual offerings are each potentially hundreds of billions in implied market capitalisation, selectivity can concentrate demand unevenly. The strongest name may attract oversubscription while the others face thinner institutional books at the margin, a dynamic that grows more pronounced as the aggregate capital demand across all three listings rises.

How investors might think about positioning ahead of the wave

Brice’s framing on 2 June 2026 offered a dual register: cautious on the near-term summer window, constructive on any pullback as a potential entry point for longer-horizon investors. He noted that broader market participation typically expands during major IPO periods, but the transition is not expected to proceed without volatility.

That framing translates into a practical decision architecture:

- Assess time horizon before evaluating participation. The summer absorption window carries distinct near-term risk. Investors with a multi-year horizon may view volatility differently from those managing quarterly performance.

- Distinguish infrastructure from application-layer exposure. The infrastructure and compute tier of AI companies is attracting stronger institutional demand than speculative application-layer names. That distinction applies both to the three IPO candidates and to existing portfolio holdings in the AI sector.

- Treat near-term volatility as a potential entry signal rather than an exit trigger. If absorption pressure does materialise as Brice anticipates, the resulting pullback could create more attractive entry conditions than a frictionless listing environment would.

The participation question versus the portfolio management question

Direct IPO participation, whether through allocated shares or day-one market purchases, carries a different risk profile from managing existing portfolio exposure around broader market volatility triggered by the listings. Institutional access to IPO allocation differs materially from retail access, shaping the practical relevance of each approach by investor type. For most retail investors, the more actionable question is how existing equity portfolios might respond to the liquidity pressure, not whether to seek allocation in the offerings themselves.

Investors exploring how to translate the infrastructure-versus-application-layer distinction into concrete portfolio weights will find our comprehensive walkthrough of AI infrastructure stock allocation, which covers the three-layer hardware, cloud, and software framework with specific position sizing guidance and the valuation metrics that institutional advisors are using to screen holdings across each tier.

What to watch as the listing window opens

The SpaceX roadshow, targeted around 4 June 2026 with a mid-June listing potential, provides the first observable data point. From there, the signals to monitor include:

- SpaceX day-one trading performance: Whether the stock holds its offering price or trades materially above or below will set the tone for the subsequent listings.

- Oversubscription data from roadshow reporting: The level of institutional oversubscription signals how much excess demand exists, or whether the offering is absorbing most of the available appetite.

- Secondary market rotation in existing tech holdings: Selling pressure in established AI and technology names during the listing window would indicate capital reallocation is in progress.

- Anthropic and OpenAI filing updates: Any acceleration or delay in their respective timelines will alter the absorption dynamic materially.

- Sequence changes that compress or extend the gap between listings: If Anthropic or OpenAI moves its timeline forward into summer, the clustering risk Brice flagged intensifies. If either pushes into late Q4 or beyond, the digestion pressure eases substantially.

The gap between SpaceX’s listing and the Anthropic and OpenAI filings will be the single most telling temporal indicator for whether the clustering risk is real or overstated. A staggered wave spread across six months poses a qualitatively different challenge from three mega-listings pricing within weeks of each other.

All timelines remain subject to change based on market conditions, regulatory review, and company decisions.

A $3.5 trillion test for the market’s capacity to absorb the future

The 2026 AI IPO wave represents a genuine structural test of market absorption capacity, not merely a cluster of exciting listings. Three companies that would each rank among the largest debuts in history are approaching public markets in a timeframe that compresses the capital reallocation cycle for institutional allocators worldwide.

Near-term caution is analytically warranted. The summer window carries real absorption risk, and Brice’s characterisation of his stance as not strongly optimistic at the current juncture reflects the weight of the structural challenge. For longer-horizon investors, the calculus is different.

Steve Brice, Standard Chartered, 2 June 2026: Any potential market pullback during the summer absorption window was characterised as a possible entry opportunity for longer-horizon investors.

The SpaceX listing will be the opening chapter. How the market absorbs it, and how the Anthropic and OpenAI timelines respond, will determine whether the summer of 2026 is remembered as a liquidity stress event or as the moment public markets proved they could absorb the scale of the AI era.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. All IPO timelines, valuations, and filing statuses referenced are subject to change based on market conditions and regulatory review. Forward-looking statements regarding market performance, listing dates, and investor positioning are speculative and subject to change based on market developments.