Most investors understand that markets move in cycles, but far fewer understand that not all stocks move with them in the same way, or even in the same direction. With the current macro environment characterised by gradually declining interest rates, mixed labour data, and persistent uncertainty about the pace of policy easing, the question of how to allocate between growth-sensitive and stability-oriented equities is front of mind for investors globally. The distinction between cyclical and defensive stocks is one of the most useful frameworks for navigating this kind of regime uncertainty.

This guide explains what cyclical and defensive stocks are, how they behave differently across the economic cycle, which sectors fall into each camp, and how investors can blend both types to build a portfolio designed to perform across varying conditions, not just in a bull market.

What separates cyclical from defensive stocks

The distinction comes down to one question: what happens to a company’s revenue when consumers tighten their spending?

Cyclical stocks are companies whose revenues and share prices closely track the broader economic cycle. They rise during expansions and fall during contractions because the products and services they provide, cars, luxury goods, holidays, are discretionary rather than essential. When household budgets come under pressure, these purchases are deferred or cancelled first.

Defensive stocks, also called non-cyclical stocks, sit on the opposite side. These companies provide goods and services that consumers continue buying regardless of economic conditions: electricity, groceries, healthcare. That persistent demand produces lower price volatility and more stable earnings, though it typically comes at the cost of slower growth during boom periods. National Grid and Enel in utilities, and Nestlé and Unilever in consumer staples, are representative examples.

The core principle: Consumer spending on non-essential goods and services contracts first in an economic downturn. Spending on utilities, food, and healthcare persists. This behavioural pattern is what separates cyclical from defensive equities at the most fundamental level.

The table below summarises the key differences across five dimensions.

| Dimension | Cyclical stocks | Defensive stocks |

|---|---|---|

| Demand driver | Discretionary spending; rises with consumer confidence | Essential needs; stable regardless of conditions |

| Volatility profile | Higher; amplifies market swings | Lower; dampens portfolio drawdowns |

| Typical sectors | Automotive, travel, luxury, construction | Utilities, consumer staples, healthcare |

| Dividend reliability | Variable; dividends may be cut in downturns | More consistent; supported by stable cash flows |

| Growth potential | Higher during expansions | Moderate but steadier across conditions |

Understanding this distinction is the foundation for every allocation decision discussed in the sections that follow. Investors who can instinctively categorise a company as cyclical or defensive are better equipped to assess how their portfolio might behave in a slowdown or recovery.

When big ASX news breaks, our subscribers know first

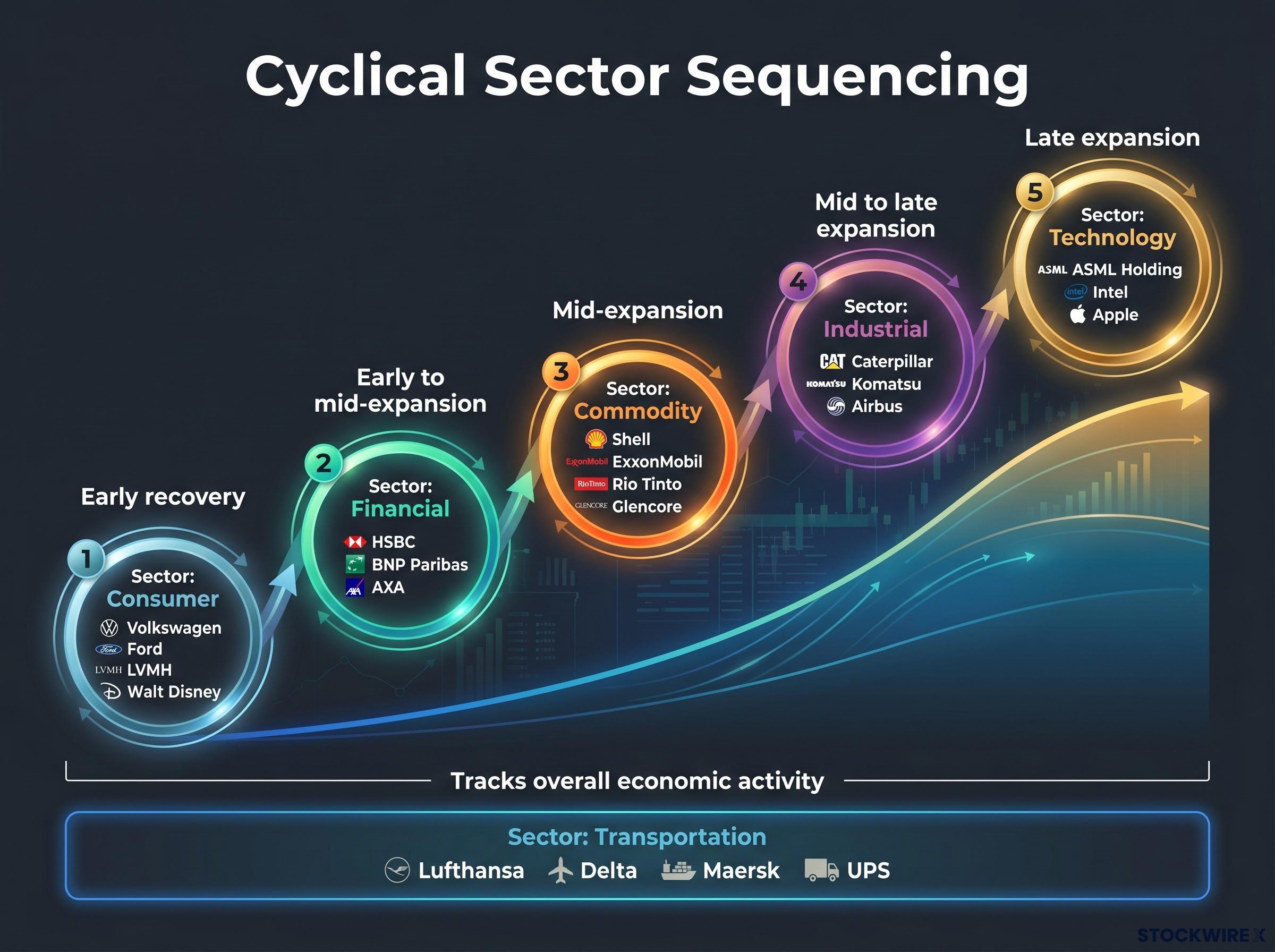

How cyclical sectors behave across the economic cycle

Treating cyclicals as a single category misses the fact that different cyclical sectors respond to different economic signals, at different times. What follows is a walk through the six main groupings, each with its own economic story.

Financial, commodity, and consumer cyclicals

Financial cyclicals stand apart from the rest because their sensitivity runs through interest rates and credit demand rather than direct consumer spending. Banks like HSBC and BNP Paribas, and insurers such as AXA, see profitability expand when rates rise and loan demand is healthy. They respond to central bank policy shifts as much as to GDP-level growth, which means they can move ahead of or behind other cyclical sectors depending on the rate cycle.

Commodity cyclicals, including Shell, ExxonMobil, Rio Tinto, and Glencore, are driven by global demand for raw materials. When industrial output and construction activity accelerate worldwide, commodity prices tend to rise and these companies benefit directly.

Consumer cyclicals are the most intuitive: companies such as Volkswagen, Ford, LVMH, and Walt Disney sell products and experiences that consumers buy more of when disposable income is rising, and cut back on first when it falls.

Industrial, transportation, and technology cyclicals

Industrial firms like Caterpillar, Komatsu, and Airbus tend to benefit later in an expansion, once confidence is high enough for governments and corporations to commit to infrastructure and capital projects. Their order books are a lagging indicator of economic strength.

Transportation cyclicals, including Lufthansa, Delta, Maersk, and UPS, track the volume of goods and people moving through the economy. When trade and travel activity rises, these companies see revenue growth; when activity contracts, they are among the first to feel it.

Technology cyclicals such as ASML Holding, Intel, and Apple are sensitive to both consumer electronics demand and corporate capital expenditure cycles. Businesses tend to expand technology spending once an expansion is well established, making this sector one of the later beneficiaries of a recovery.

| Sector | Representative companies | Primary demand driver | Typical cycle phase |

|---|---|---|---|

| Financial | HSBC, BNP Paribas, AXA | Interest rates and credit demand | Early to mid-expansion |

| Commodity | Shell, ExxonMobil, Rio Tinto, Glencore | Global industrial demand and raw material prices | Mid-expansion |

| Consumer | Volkswagen, Ford, LVMH, Walt Disney | Discretionary consumer spending | Early recovery |

| Industrial | Caterpillar, Komatsu, Airbus | Infrastructure and capital investment | Mid to late expansion |

| Transportation | Lufthansa, Delta, Maersk, UPS | Trade and travel volume | Tracks overall economic activity |

| Technology | ASML Holding, Intel, Apple | Consumer electronics and corporate capex | Late expansion |

The sequencing matters. Consumer-facing companies may benefit earliest in a recovery. Industrial firms gain later as infrastructure investment accelerates. Technology companies tend to see a boost as businesses expand capital spending in the later stages of growth. Investors who treat cyclicals as a monolithic category often make poorly timed sector moves.

Investors wanting a deeper analytical framework for acting on these sequencing patterns will find our dedicated guide to sector rotation strategy covers the business cycle phase model in full, including how Relative Rotation Graphs and institutional fund flow data reveal where capital is moving before official economic data confirms it.

Timing the cycle and managing the risks that come with it

The rewards of cyclical investing come with a discipline requirement. Mistimed entry is the central risk, and it cuts both ways.

Reading the economic cycle

Buying too far into an expansion exposes the investor to the next contraction, often with limited upside remaining. Entering too early means absorbing losses or dead time before gains materialise. Both failure modes are common, and both are avoidable with disciplined monitoring.

The indicators worth watching fall into a natural sequence:

- Leading indicators first: Manufacturing Purchasing Managers’ Indices (PMIs), which measure factory activity, tend to signal turning points before they appear in GDP data. Credit spreads, the gap between corporate bond yields and government bond yields, widen when the market senses rising default risk and narrow when confidence improves.

- Consumer confidence data: Surveys tracking household spending intentions provide a read on discretionary demand, which is the primary revenue driver for most cyclical sectors.

- Central bank signalling: Rate decisions and forward guidance from major central banks shape the cost of borrowing and, by extension, the trajectory of business investment and consumer credit.

- Confirming signals: Employment data, corporate earnings revisions, and retail sales figures confirm whether the cycle shift flagged by leading indicators is translating into real economic activity.

PMI readings are one of the most widely cited leading indicators for cyclical positioning, but markets typically pre-price PMI trends 3–30 months before official survey releases, meaning the actionable signal lies in the surprise relative to consensus rather than the absolute level of any given print.

Federal Reserve research on credit spreads as economic predictors confirms that the gap between corporate and government bond yields provides statistically significant advance warning of turning points in cyclically sensitive economic activity, making it one of the more reliable inputs for investors assessing where the cycle currently stands.

Tools for managing cyclical exposure

Even with accurate cycle reading, company-specific risk can undermine a cyclical position. A firm carrying excessive debt or operating with weak fundamentals may underperform even when the broader economic environment is favourable. Balance sheet quality and debt load should serve as a screening filter before any cyclical stock enters a portfolio.

Stop-loss orders, which automatically trigger a sale when a share price falls below a specified level, limit downside on individual positions. Diversifying across multiple cyclical sectors, rather than concentrating in one, reduces the risk that a single sector-specific shock derails returns.

Cyclicals reward disciplined investors and penalise those who rely on instinct rather than evidence. The analytical habits outlined above are not optional extras; they are the cost of admission.

Performance Drivers in Cyclical Equities

The case for cyclical stocks is not speculation. It is a considered strategic choice grounded in how economic expansions distribute returns.

During growth phases, cyclical stocks tend to outperform as rising consumer spending and business investment lift company revenues. The share price appreciation during these periods can be substantial, particularly for investors who position themselves early.

The most frequently cited timing advantage centres on the post-trough entry point. The period immediately following an economic trough, when sentiment is still poor but the data has stopped deteriorating, is often among the most rewarding entry windows for cyclical equities. These stocks frequently begin to recover ahead of the broader economy, rewarding investors willing to act on early signals.

A practical rule of thumb: The best cyclical entry points tend to come when economic data has stopped getting worse but has not yet started getting better. Waiting for confirmation of a recovery often means missing a meaningful portion of the move.

Beyond timing, cyclicals contribute to portfolio construction in several ways:

- Growth potential: Substantial share price appreciation during economic expansions

- Diversification effect: Cyclical and defensive equities behave differently across conditions, and combining both may reduce overall portfolio volatility

- Inflation hedge: Commodity and energy cyclicals can serve as a buffer against rising prices, since higher goods prices often translate into improved revenues

- Post-trough entry opportunity: Early positioning in recoveries can capture outsized returns

- Long-term growth contribution: Given the general upward economic trajectory over extended periods, investors with longer time horizons can benefit from cyclical exposure provided they tolerate interim drawdowns

Understanding why cyclicals belong in a portfolio, not just when they perform well, helps investors hold positions through volatility rather than selling at the worst moment in the cycle.

The next major ASX story will hit our subscribers first

Strategic Allocation: Cyclical-Defensive Blends

A portfolio holding both cyclical and defensive equities is designed to perform across the full economic cycle rather than optimise for one phase. Cyclicals drive gains during expansions. Defensives absorb losses during contractions. The combination produces a portfolio that adapts to shifting conditions over time.

Four-quadrant risk balancing, the framework behind Ray Dalio’s All Weather Portfolio, is one structural expression of the same logic: allocating explicitly to assets that perform across rising growth, falling growth, rising inflation, and falling inflation environments produces a portfolio that is less dependent on any single macro outcome.

The more active version of this approach involves tilting allocation toward cyclicals or defensives based on cycle positioning, rather than holding a fixed split regardless of conditions. In early recovery, for example, a heavier cyclical weighting captures the rebound. As the cycle matures and recession risk builds, rotating toward defensives protects accumulated gains.

Current macro context: J.P. Morgan Asset Management’s January 2026 Federal Open Market Committee (FOMC) commentary characterised the backdrop as one of steady policy rates, a soft but non-deteriorating labour market, and elevated but non-threatening inflation, with the expectation that the path lower for rates remains gradual. This type of environment, where rate direction is downward but the pace is slow and uncertain, is precisely the kind of regime where the cyclical/defensive balance is actively debated among institutional allocators.

Historically, rate-cut expectations have tended to favour cyclicals and risk assets, while growth fears or policy uncertainty have favoured defensives. The current setup does not offer a clean directional call, which is why some investors adopt a barbell approach: maintaining meaningful exposure to both ends of the spectrum simultaneously, accepting that one side will underperform at any given time, in exchange for overall portfolio resilience.

Fidelity Institutional’s Q2 2026 market outlook advises investors to seek cyclical companies whose fundamentals align with accelerating economic growth while retaining defensive dividend equities to stabilise portfolio returns, a positioning framework consistent with the barbell approach that many institutional allocators are applying in the current gradual rate-easing environment.

The table below illustrates how a hypothetical allocation might shift across four economic phases.

| Economic phase | Cyclical weighting | Defensive weighting | Sector emphasis |

|---|---|---|---|

| Early recovery | 60-70% | 30-40% | Consumer cyclicals, financials |

| Expansion | 55-65% | 35-45% | Industrials, technology, commodities |

| Late cycle | 40-50% | 50-60% | Utilities, consumer staples, select energy |

| Recession | 25-35% | 65-75% | Healthcare, utilities, consumer staples |

Defensive anchors such as National Grid, Enel, Nestlé, and Unilever provide stability during the phases where cyclical exposure is reduced. The goal is not to eliminate cyclical holdings entirely during downturns, but to adjust the balance so that the portfolio’s overall risk profile matches the prevailing conditions.

Building a portfolio that works in any economic season

Neither cyclical nor defensive stocks are inherently superior. Each plays a distinct role, and the most resilient portfolios hold both with intentional allocation rather than defaulting to one posture.

The practical sequence is straightforward:

- Identify the current cycle phase using leading indicators such as PMIs, credit spreads, consumer confidence data, and central bank guidance

- Assess personal risk tolerance and time horizon. Cyclicals suit investors who can tolerate elevated volatility in pursuit of higher returns. Defensives suit those prioritising capital preservation and income. Longer time horizons allow investors to ride out cyclical drawdowns; shorter horizons justify a higher defensive weighting.

- Review the current cyclical/defensive split against cycle positioning. Does the portfolio’s exposure match where the economy appears to be headed?

- Identify rebalancing actions if the allocation is misaligned. This may mean adding cyclical exposure ahead of a recovery, or rotating toward defensives as the expansion matures.

Identifying the right rebalancing actions is only the first step; executing them tax-efficiently, using new contributions before triggering taxable sales and prioritising tax-advantaged accounts, determines how much of the rebalancing benefit investors actually retain.

The discipline of cyclical investing is not market timing in the speculative sense. It is cycle-aware allocation: adjusting exposure based on observable economic evidence rather than prediction. That distinction matters. Speculation is a guess. Cycle awareness is a process.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and portfolio allocations should reflect individual circumstances, risk tolerance, and investment objectives.

—