Hormuz Shipping Collapses 52% as US-Iran Clash Sends Oil Surging

5 hrs ago

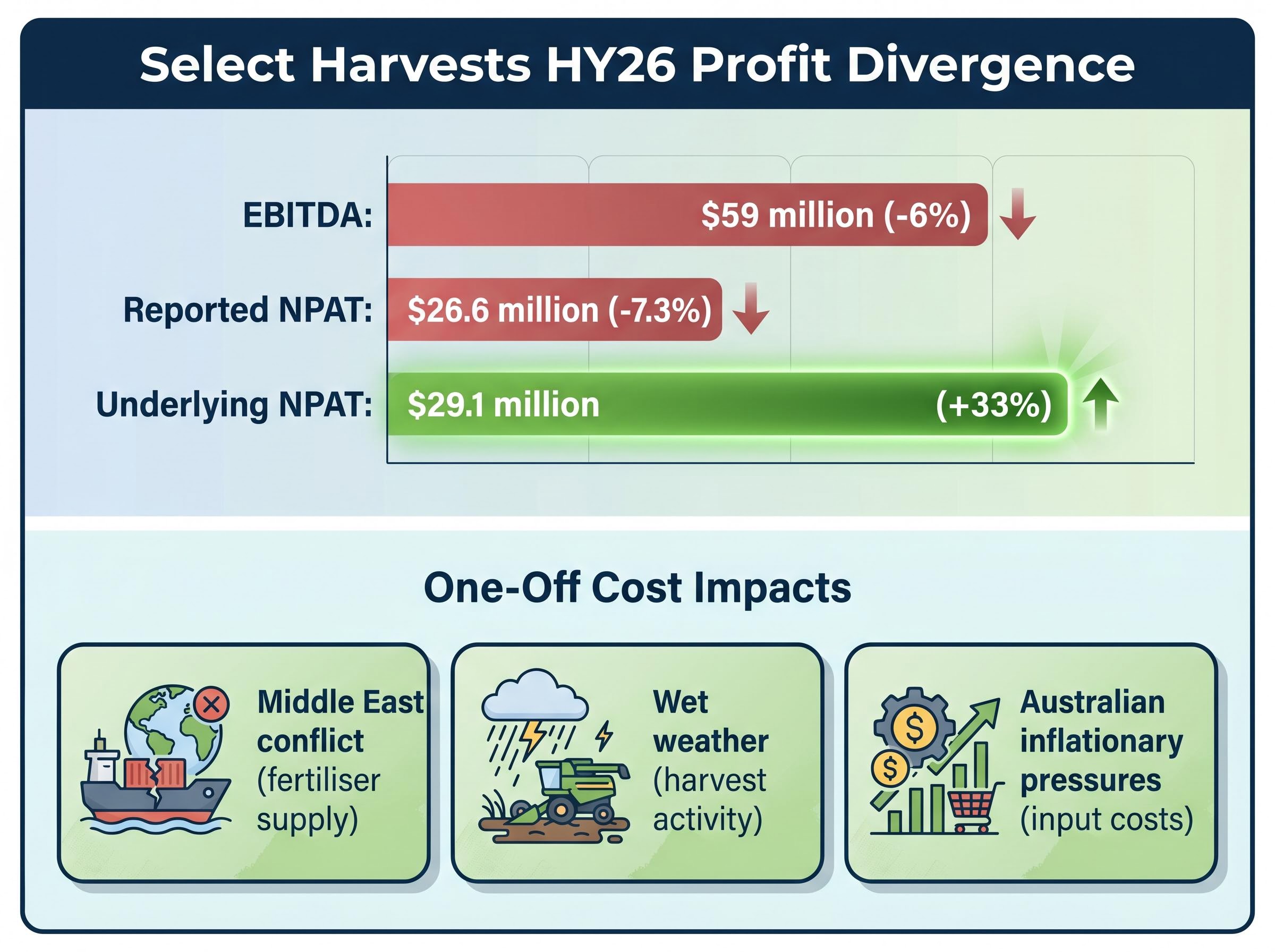

Select Harvests shares jumped approximately 14% on 28 May 2026 after the almond grower delivered a half-year result that, on the surface, sends conflicting signals. Reported net profit fell 7.3%, yet the board launched an on-market buyback and declared the company undervalued. The underlying earnings tell a different story: strip out one-off costs tied to the Middle East conflict, wet weather, and inflationary pressures, and profit rose 33%. A revived interim dividend, a record crop on the horizon, and long-term targets of $700 million in revenue and 65,000 metric tonnes of almond production by 2030 add layers that the headline number alone does not capture. What follows unpacks the earnings split, the buyback signal, and what the ASX SHV results mean for investors assessing the trajectory from here.

The 14% single-session gain on 28 May 2026 was not a straightforward response to a strong result. Reported NPAT of $26.6 million represented a 7.3% decline on the prior corresponding period. That is not the kind of number that typically triggers a double-digit repricing for an ASX-listed agricultural stock.

The market looked past it. Three signals, arriving together, shifted sentiment:

The 14% single-session gain is a textbook illustration of the expectations gap in earnings season: the market was not pricing the reported NPAT figure in isolation but weighing the buyback signal, reinstated dividend, and record crop guidance against what had already been embedded in the share price.

The board stated that the prevailing market valuation did not adequately reflect the underlying worth of the business, a direct signal that directors view the current share price as disconnected from intrinsic value.

Underlying NPAT, which strips out one-off cost items, rose 33% to $29.1 million. The market’s response suggests investors weighed the underlying figure, the capital return commitment, and the forward crop outlook more heavily than the reported headline.

The gap between a 7.3% decline in reported NPAT and a 33% increase in underlying NPAT is large enough to change the entire interpretation of this result. Understanding what sits between the two numbers matters.

| Metric | HY26 | HY25 | Change |

|---|---|---|---|

| EBITDA | $59 million | $62.8 million | -6% |

| Underlying NPAT | $29.1 million | $21.9 million | +33% |

| Reported NPAT | $26.6 million | $28.7 million | -7.3% |

The $59 million EBITDA figure, down 6%, is consistent with a period weighed down by non-recurring cost pressures rather than deteriorating operations. The underlying NPAT figure removes those pressures to show the operating trajectory beneath.

Three specific one-off categories depressed reported earnings: disruption from the Middle East conflict (which affected fertiliser supply chains), wet weather impacts on harvest activity, and broader Australian inflationary pressures on input costs.

Agricultural companies are structurally more exposed to these types of non-recurring cost events than most industrial sectors. Weather disruption is seasonal and unpredictable. Geopolitical supply chain effects on fertiliser represent an external risk, not a management failure. The analyst convention is to assess underlying operational health by stripping out these items, though repeated one-off adjustments over multiple periods would warrant closer scrutiny of whether they are genuinely non-recurring.

A buyback of up to 10% of total issued share capital is not a routine capital management exercise. Paired with the board’s explicit statement that the market was undervaluing the business, it represents one of the more direct forms of management communication available to retail investors.

Established corporate finance interpretation treats on-market buybacks as a confidence signal when three conditions are present:

Select Harvests meets all three conditions as stated. The record crop outlook provides revenue visibility. Fertiliser for the 2027 season has already been secured. Water allocations remain at favourable levels. The buyback is not being funded at the expense of operational readiness.

That said, a buyback authorisation is not an obligation. The board has approved up to 10% but is not committed to purchasing the full amount. Execution will depend on prevailing market conditions and share price levels.

Buyback capital allocation decisions are rarely binary, and the Macquarie case from earlier in 2026 illustrates why: a programme launched near a 52-week low and closed when the price had risen 25% demonstrates how management teams calibrate repurchase activity against the moving estimate of intrinsic value rather than running a programme to completion regardless of price.

The half-year result reflects a period of disruption. The forward operational picture looks materially different.

Select Harvests expects its 2026 crop to be among the largest in company history, supported by a contracted increase in externally sourced almond volumes. Yield improvement initiatives across the company’s orchards are contributing to the production uplift.

According to the USDA Foreign Agricultural Service (July 2025), Australian almond production is forecast to reach a record 175,000 metric tonnes (kernel equivalent) in marketing year 2025/26, up 21% from a revised 145,000 metric tonnes in MY 2024/25.

That macro backdrop positions Select Harvests within an expanding, export-oriented industry. Approximately 80% of Australian almond production is exported, with Asia and the Middle East as primary destinations.

The USDA Foreign Agricultural Service almond production forecasts for Australia’s 2025/26 marketing year project output at a record 175,000 metric tonnes (kernel equivalent), with exports reaching an all-time high of 143,000 metric tonnes, placing Australia firmly as the world’s second-largest almond producer and exporter behind California.

Preparation for the 2027 crop season is already underway. Three steps have been completed:

The implication for investors is that the cost pressures that depressed reported earnings in HY26 may not recur with the same intensity in the second half, allowing underlying and reported earnings to converge.

The long-term targets are specific: 65,000 metric tonnes of almond production and $700 million in total revenue by 2030. Two pillars underpin the strategy.

| Metric | Current | 2030 Target |

|---|---|---|

| Almond production | Record crop expected in 2026 (exact tonnage not disclosed) | 65,000 metric tonnes |

| Total revenue | Not separately disclosed for HY26 | $700 million |

The first pillar is production scale through third-party grower relationships. Select Harvests offers external growers a value proposition that includes:

The second pillar is market diversification. The company is building direct customer relationships in China and India, reducing reliance on intermediaries and improving the sales mix. Australia’s position as the world’s second-largest almond producer and exporter after the United States, as confirmed by the USDA FAS (July 2025), provides a structural tailwind for export-led growth into Asian markets.

Long-dated quantitative targets with explicit production and revenue figures give investors a measurable framework for assessing management accountability over time, a feature that appears uncommon among ASX-listed agricultural peers based on available research.

ASX agricultural capital recycling has become a recurring theme in 2026, with Duxton Farms divesting 7,061 hectares of NSW cropping land and 8.6 gigalitres of water entitlements to redirect capital toward higher-margin horticulture and specialty crop segments, a structural contrast to Select Harvests’ volume-led expansion model.

Three forward indicators will confirm or challenge the thesis embedded in this result:

No post-result broker commentary was available at the time of writing. The market’s 14% repricing has not yet been validated or challenged by institutional analysis, which means retail investors are forming views without that external reference point.

Record crops are not an unqualified positive. Both Australia and California are producing at or near record levels simultaneously. California’s 2025 crop is expected at approximately 3.6-3.7 billion pounds, according to industry sources (though this figure has not been independently verified). California carry-out stocks have fallen below 0.5 billion pounds for the first time in several years, suggesting improved demand-supply balance.

The structural tension, as flagged by Agri-Pulse (2025), is that rising Australian volumes may pressure global almond prices. California growers have expressed concern that Australian export competition could alter trade flows, particularly into Asia. If global pricing weakens, Select Harvests would need revenue growth to be driven by mix improvement and direct customer margins rather than volume alone.

AUD/USD exchange rate headwinds add a layer of complexity to the revenue growth story: with approximately 80% of Australian almond production exported and Asia as the primary destination, a sustained depreciation in the Australian dollar improves the local-currency value of export receipts, while a strengthening Aussie compresses margins on contracted volumes priced in USD.

The Agri-Pulse analysis of California-Australia almond competition identifies Asian markets, particularly China and India, as the primary battleground where rising Australian export volumes are reshaping trade flows and creating downward pricing pressure for California growers accustomed to dominant market share.

The 33% underlying profit growth and the buyback announcement together build a stronger case than the 7.3% reported decline suggests on its own. The board’s willingness to commit capital to a buyback, declare undervaluation, and reinstate the dividend indicates confidence in the forward trajectory.

That trajectory, however, rests on specific assumptions: that one-off costs normalise, that the record 2026 crop delivers, and that direct customer expansion in China and India gains traction. Each assumption is testable, and the 2030 targets of $700 million in revenue and 65,000 metric tonnes of production provide a measurable horizon against which to track progress.

The next confirmation point is the full-year FY26 result and 2026 crop volume data.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Select Harvests reported a 7.3% decline in reported NPAT to $26.6 million, but underlying NPAT rose 33% to $29.1 million once one-off costs related to the Middle East conflict, wet weather, and inflationary pressures were stripped out. The board also reinstated an interim dividend of $0.035 per share and announced an on-market buyback of up to 10% of issued share capital.

The 14% single-session gain reflected investor focus on three signals arriving together: a board-endorsed share buyback with an explicit statement that the stock was undervalued, the reinstatement of an interim dividend after zero payout in HY25, and management guidance that the 2026 crop is expected to be among the largest in company history.

An on-market buyback is when a company purchases its own shares through the stock exchange, reducing the total number of shares outstanding. When paired with an explicit statement that the board believes the market is undervaluing the business, as Select Harvests did, it is widely interpreted as a direct signal of management confidence in the company's intrinsic value.

Select Harvests has set targets of 65,000 metric tonnes of almond production and $700 million in total revenue by 2030, underpinned by third-party grower expansion and direct customer relationship building in China and India.

The main risk is global almond price pressure, as both Australia and California are producing at or near record levels simultaneously, which could weigh on export pricing. AUD/USD exchange rate movements also affect the local-currency value of export receipts, given that approximately 80% of Australian almond production is exported.