CURE and CLNE: the ASX ETFs Returning 25% in 2026

7 hrs ago

Goodman Group’s core property metrics read like a landlord operating at the top of its game: occupancy near 97%, rental income growing at 6.1%, a $14.5 billion development pipeline weighted heavily toward data centres, and earnings guidance reaffirmed at a minimum 9% EPS growth for FY26. Yet the Goodman Group share price has shed roughly 20% from its August 2025 peak and fell a further 3% on its latest quarterly update.

For ASX investors tracking GMG, that gap between operational performance and share price movement raises an immediate question: what is the market pricing in that the fundamentals are not showing? This analysis examines that question using data from Goodman’s FY26 Q3 update and the macro conditions shaping how the market values premium-multiple property stocks. By the end, readers will understand the specific forces pulling GMG’s valuation lower, what the development pipeline and earnings trajectory suggest about the company’s medium-term position, and how to think about the current price level as either an opportunity or a justified reset.

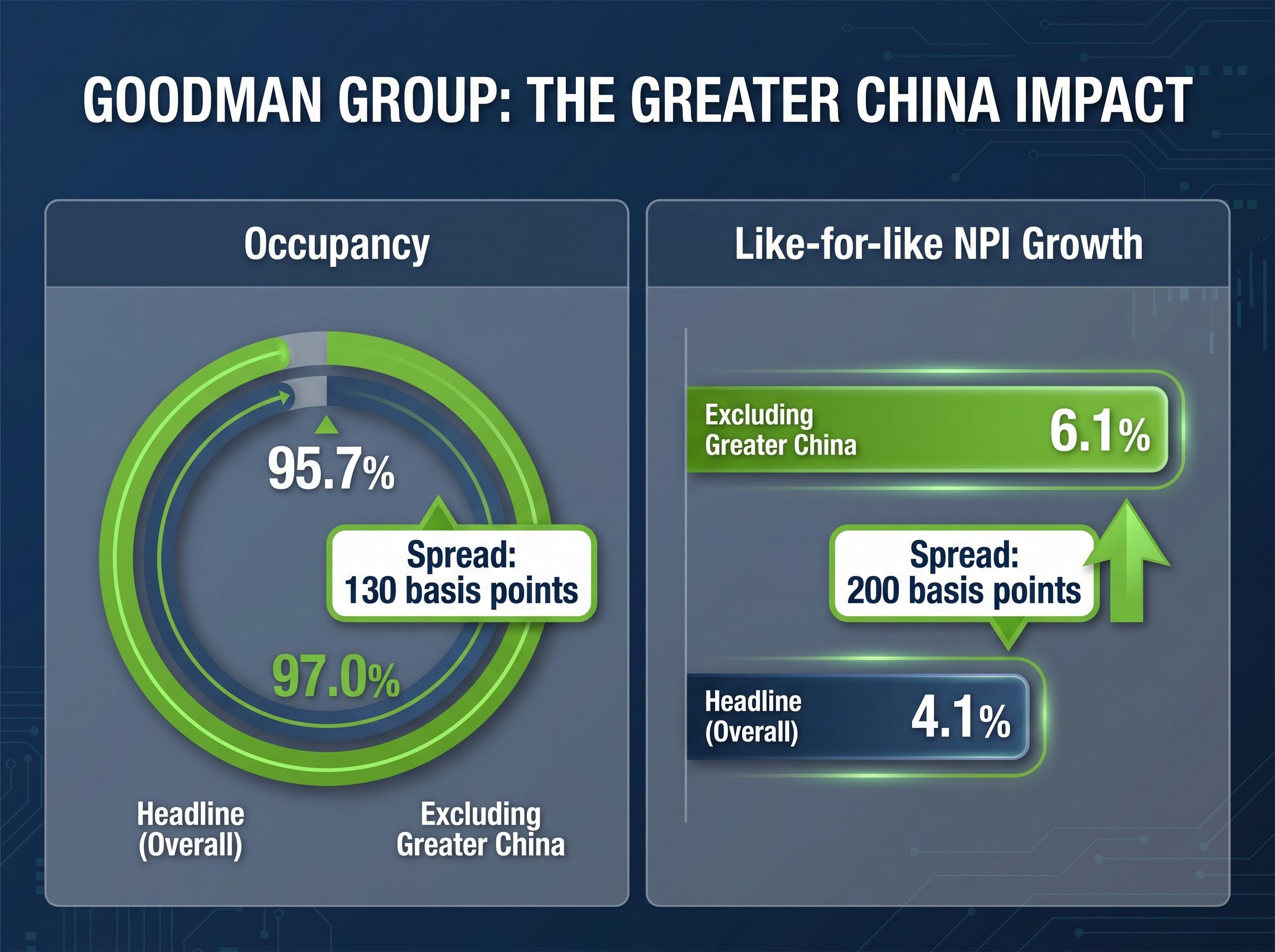

The Q3 FY26 update delivered portfolio metrics that, in isolation, would leave little room for complaint. Occupancy across the $87.1 billion global portfolio stood at 95.7%, and excluding Greater China, the figure tightened to 97.0%. Like-for-like net property income (NPI) growth followed a similar pattern: 4.1% at the headline level, rising to 6.1% once the Greater China drag was stripped out.

| Metric | Overall | Excluding Greater China |

|---|---|---|

| Occupancy | 95.7% | 97.0% |

| Like-for-like NPI growth | 4.1% | 6.1% |

| Portfolio value | $87.1 billion (stable) | |

The weighted average lease expiry (WALE) held at 4.9 years, providing income visibility well into the next cycle. Management reaffirmed operating EPS guidance of at least 9% growth for FY26, a floor rather than a midpoint.

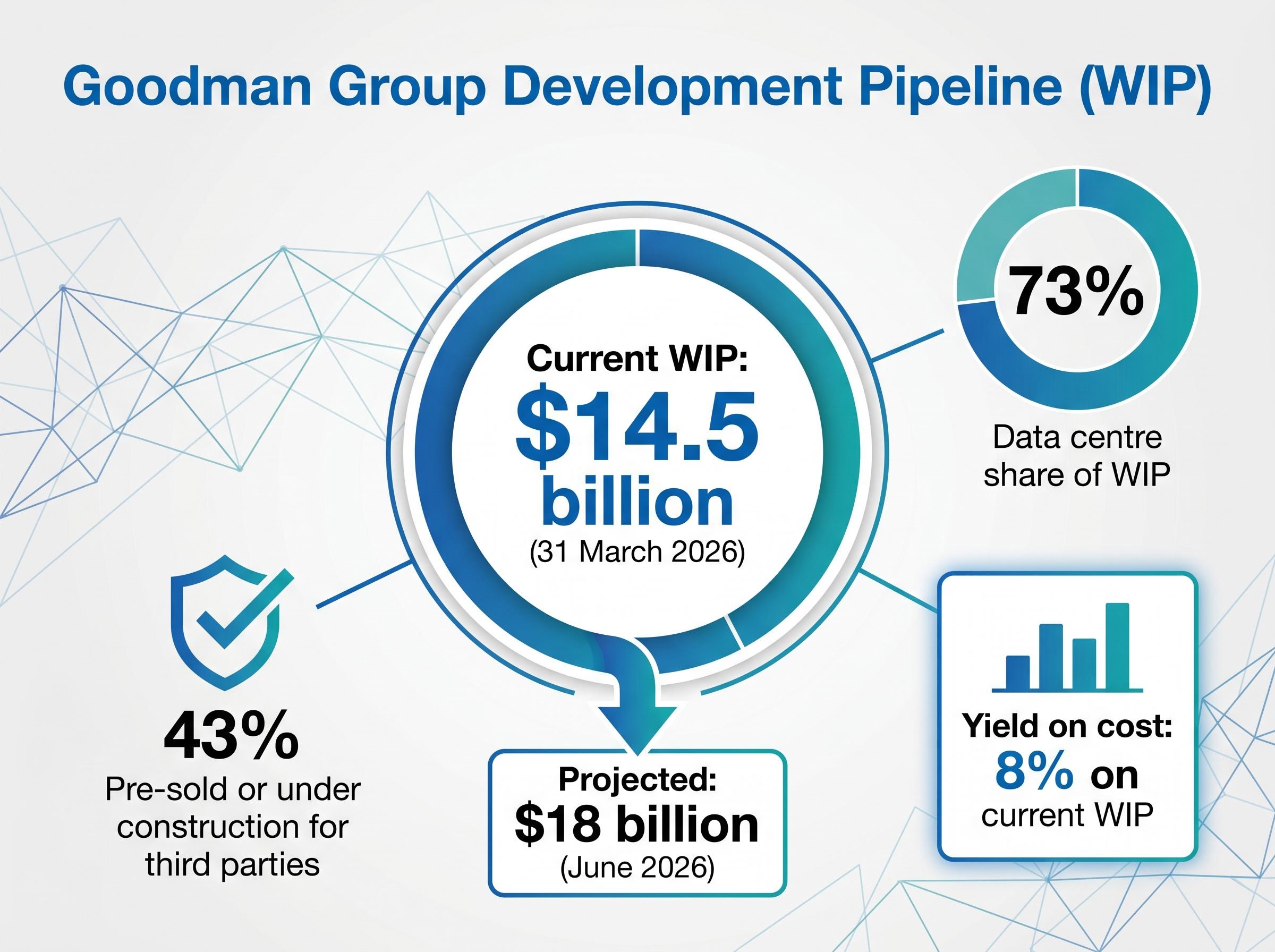

The development pipeline underpins the forward earnings case:

These are not the metrics of a business under stress. They are the metrics of a business whose share price is responding to something other than what the operations are reporting.

Goodman’s balance sheet structure, specifically the placement of significant leverage inside off-balance-sheet co-investment vehicles rather than on the parent entity, produces a debt-to-equity ratio that understates the true capital intensity of the business and a statutory ROE figure that obscures economic profitability; investors relying on these headline ratios without adjustment risk drawing the wrong conclusions about financial risk.

The answer sits in the mechanics of how the market values future earnings. When bond yields rise, the discount rate applied to future cash flows rises with them. For a stock trading on a trailing price-to-earnings (P/E) ratio of approximately 36x, where a large portion of the earnings growth is embedded in development completions two to three years away, the effect is amplified. The higher the multiple and the longer the earnings duration, the more a shift in discount rates compresses the present value of those future profits.

A stock’s trailing P/E tells investors what they are paying for current earnings. But when a large share of the investment case rests on earnings that have not yet been delivered, the sensitivity to discount rate changes increases. This is the core tension for premium-growth property stocks in a rising-rate environment.

This is not a verdict on Goodman’s quality. It is a function of how the market prices long-duration growth assets when the risk-free rate moves against them.

The four rate transmission channels that connect bond yield movements to property stock valuations, the economic outlook signal, the discount rate effect on future cash flows, debt financing costs, and yield competition with government bonds, each compound one another when yields rise sharply, which is why a sector-wide de-rating can feel disproportionate to the headline macro shift.

The S&P/ASX 200 A-REIT Index delivered year-to-date total returns of approximately negative 15% at one point in early 2026, reflecting the sector-wide impact of Australian 10-year government bond yields reaching above 4.5-5.0% during 2025-2026. Reserve Bank of Australia (RBA) rate uncertainty compounded the pressure.

The RBA monetary policy decision issued in May 2026 confirmed a cash rate target of 4.35%, with the Board noting that money market interest rates and government bond yields had risen, providing the official policy backdrop against which Australian property valuations are being recalibrated.

GMG’s earnings profile, driven by development completions and data centre exposure rather than passive rental yield, distinguishes it from traditional A-REITs. That distinction cuts both ways. It justifies the premium multiple in a falling-rate environment; it also means the cushion is thinner when growth expectations soften even marginally. The stock’s 52-week range of A$24.56 to A$37.31 captures that volatility. At approximately A$30.05-A$30.28, GMG sits well below its highs, having absorbed the same macro headwinds as the sector while carrying the additional weight of a higher starting multiple.

The forward P/E of approximately 22x reflects the market’s expectation that earnings will grow into the current price. Whether that growth materialises at the projected pace is the question the pipeline data must answer.

The 73% data centre weighting of Goodman’s WIP is both the strongest part of the investment thesis and the element most exposed to thematic sentiment shifts. Understanding the pipeline mechanics matters.

Goodman’s integrated development capability moves through five sequential stages:

That integration matters because 43% of WIP is either pre-sold or under construction for third parties and partnerships, reducing completion risk materially. The yield on cost of 8% on current WIP provides a concrete return benchmark against which investors can measure the pipeline’s contribution to earnings.

The supply-side constraints in data centre development, including grid capacity, water availability, site complexity, and capital requirements, function as barriers to new entrants. Established operators with secured power, land, and construction capabilities hold a structural advantage that is difficult to replicate quickly.

The pipeline is the primary earnings growth engine for the next two to three years. Investors assessing GMG’s forward P/E of approximately 22x need to understand that this multiple is pricing in pipeline conversion at projected yields, not just the current earnings run rate.

Data centre capacity demand across Australasia is being validated by operators beyond Goodman, with Infratil’s CDC platform upgrading FY27 EBITDAF guidance to A$680-720 million after adding nearly 200 megawatts of operating capacity in a single quarter and securing around 140 megawatts of new contract wins, a trajectory that supports the structural demand thesis underpinning Goodman’s 73% data centre weighting in its development pipeline.

The one genuine operational wrinkle in an otherwise strong quarter sits in the regional decomposition. The gap between headline portfolio metrics and ex-Greater China figures is not negligible.

| Metric | Headline (Overall) | Excluding Greater China | Spread |

|---|---|---|---|

| Occupancy | 95.7% | 97.0% | 130 basis points |

| Like-for-like NPI growth | 4.1% | 6.1% | 200 basis points |

A 200 basis point spread in NPI growth is material. It means the core portfolio outside Greater China is performing meaningfully stronger than the headline figures suggest. Goodman has disclosed this breakdown transparently, and the strategic direction of the portfolio, concentrated in major urban global assets that are difficult to replicate, points toward continued emphasis on these higher-performing markets.

For ASX investors conducting their own analysis, the practical takeaway is straightforward: headline figures alone understate the strength of the ex-China portfolio. Any assessment of GMG’s operational quality that relies solely on aggregate numbers without this regional decomposition risks misreading the underlying health of the business.

The 13-broker consensus places a price target of approximately A$34.46-A$34.92 on Goodman Group, implying roughly 15% upside from the current trading range of A$30.05-A$30.28.

At current levels, the gap between the consensus price target and the trading price implies that the majority of covering analysts view the de-rating as having overshot the fundamental picture.

The range of professional opinion clusters around three scenarios:

The market capitalisation of approximately A$61.9-A$63.1 billion positions GMG as one of the largest A-REIT-adjacent names on the ASX. The breadth of the analyst range, A$29 to A$40, captures the genuine uncertainty around the two variables that matter most: the rate trajectory and the pipeline conversion rate.

The analytical threads pull in opposing directions. On one side: occupancy near 97% ex-China, NPI growth of 6.1%, a $14.5 billion pipeline with 73% data centre exposure, reaffirmed 9% EPS growth guidance, and a consensus target implying 15% upside. On the other: a trailing P/E of approximately 36x, Australian bond yields that have reached above 4.5-5.0%, a Greater China drag that softens headline metrics, and a forward P/E of approximately 22x that still requires pipeline delivery to justify.

The investor’s decision rests on a view of two variables:

At approximately A$30, the stock sits in the lower third of its 52-week range of A$24.56 to A$37.31. The 20% de-rating from the August 2025 peak has already absorbed a significant portion of the macro headwind.

That said, the forward P/E of approximately 22x is not yet at a level that traditional value-oriented investors would characterise as inexpensive for a property-linked name. The price reflects a business that the market still expects to grow, just not at the pace previously embedded in the multiple.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Goodman Group’s operational fundamentals are holding up. The share price decline is primarily a valuation-multiple story driven by macro rate dynamics rather than a deterioration in the underlying business.

The uncertainty is two-sided. Investors who believe Australian rates are near their peak may find the current price an attractive entry into a structurally positioned business with visible earnings growth. Investors who expect rates to stay higher for longer, or who question whether data centre pipeline conversion will meet projected timelines, may prefer to wait for either lower prices or clearer macro signals.

GMG is not cheap by traditional property standards. But it is materially cheaper than it was three quarters ago, and the pipeline data suggests the earnings story remains intact. The market has repriced the multiple; it has not yet repriced the fundamentals.

Investors exploring the competitive landscape for Australian data centre infrastructure will find our deep-dive into NEXTDC’s contracted order book useful context, covering the 297MW forward pipeline providing earnings visibility through FY29, the 173% contracted-to-built-capacity ratio that signals demand outpacing supply, and the breakdown showing cloud and AI deployments at 59% of contracted megawatts across the portfolio.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Like-for-like net property income (NPI) growth measures rental income growth across a consistent set of properties, excluding acquisitions and disposals. For Goodman Group, the ex-Greater China NPI growth of 6.1% in Q3 FY26 signals that the core portfolio is performing materially stronger than the 4.1% headline figure suggests.

The Goodman Group share price decline is primarily driven by valuation multiple compression caused by rising Australian bond yields, which increase the discount rate applied to future earnings. Because GMG trades on a high trailing P/E of approximately 36x with significant earnings embedded in future development completions, it is more sensitive to rate movements than lower-multiple property stocks.

Goodman Group's work in progress stood at $14.5 billion as at 31 March 2026, projected to reach $18 billion by June 2026, with 73% weighted toward data centres and a yield on cost of 8%. With 43% of WIP either pre-sold or under construction for third parties, the pipeline provides material earnings visibility and reduces completion risk.

A 13-broker consensus places the price target for Goodman Group at approximately A$34.46 to A$34.92, implying around 15% upside from the current trading range of A$30.05 to A$30.28. Analyst scenarios range from a bear case of A$29.00 to a bull case of A$40.00.

Greater China drags both headline occupancy and NPI growth lower, creating a 130 basis point gap in occupancy (95.7% overall versus 97.0% ex-China) and a 200 basis point gap in like-for-like NPI growth (4.1% overall versus 6.1% ex-China). Investors relying solely on aggregate figures risk underestimating the strength of Goodman's core portfolio.