Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

6 mins ago

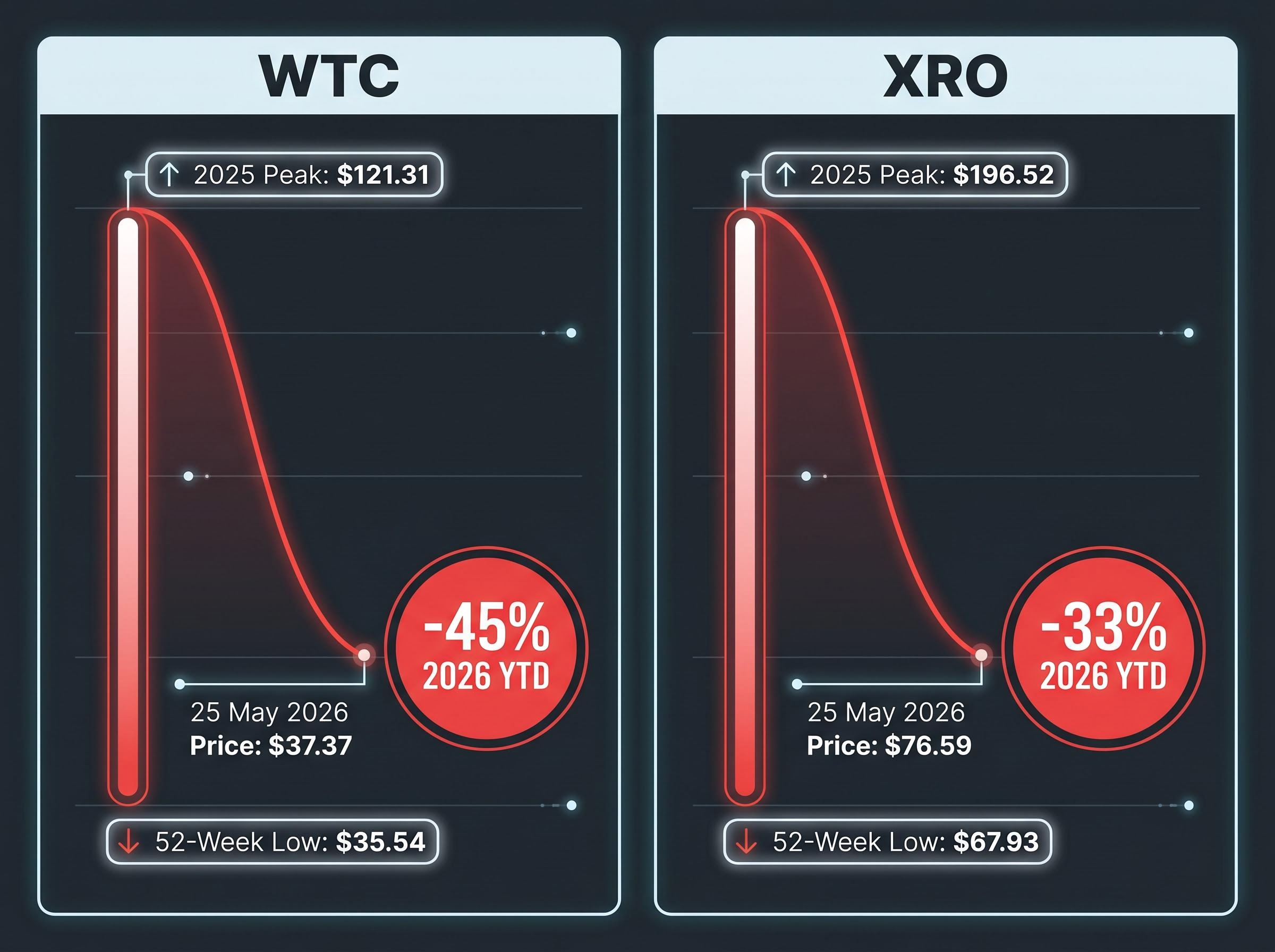

In April 2025, Morgan Stanley cut price targets across ASX technology stocks by roughly 20%, warning that valuations remained “anchored to outdated assumptions.” Thirteen months later, WiseTech Global trades at approximately $37, down 45% year-to-date, and Xero sits near $76, down 33%. The broker’s concern turned out to be understated.

Morgan Stanley’s April 2025 call was not a routine target trim. It was a sector-wide reassessment of whether premium growth multiples could survive a prolonged higher interest rate environment. That question now has an answer visible in the share price data, and it carries lessons for any Australian investor trying to interpret broker price target cuts as they happen in real time. What follows examines what Morgan Stanley actually said, traces what happened to both stocks over the 13 months since, compares how other major brokers positioned themselves, and provides a framework for reading target cuts without overreacting or dismissing them.

The note was a sector-wide reassessment, not a company-specific reaction to an earnings miss or a guidance revision. Morgan Stanley’s analysts looked across the ASX technology universe and concluded that growth multiples had been priced for conditions that no longer existed: lower interest rates, faster revenue acceleration, and a macro environment more forgiving of premium valuations.

“Anchored to outdated assumptions.” — Morgan Stanley, April 2025 ASX technology sector note

That phrase carried a specific valuation argument. Forward price-to-sales and forward price-to-earnings multiples for both WiseTech Global and Xero had been running well above sector averages. Morgan Stanley’s view was that the market had not yet adjusted these multiples to reflect the sustained higher rate environment, and the gap between where these stocks traded and where their models placed fair value had widened to a point requiring a broad recalibration.

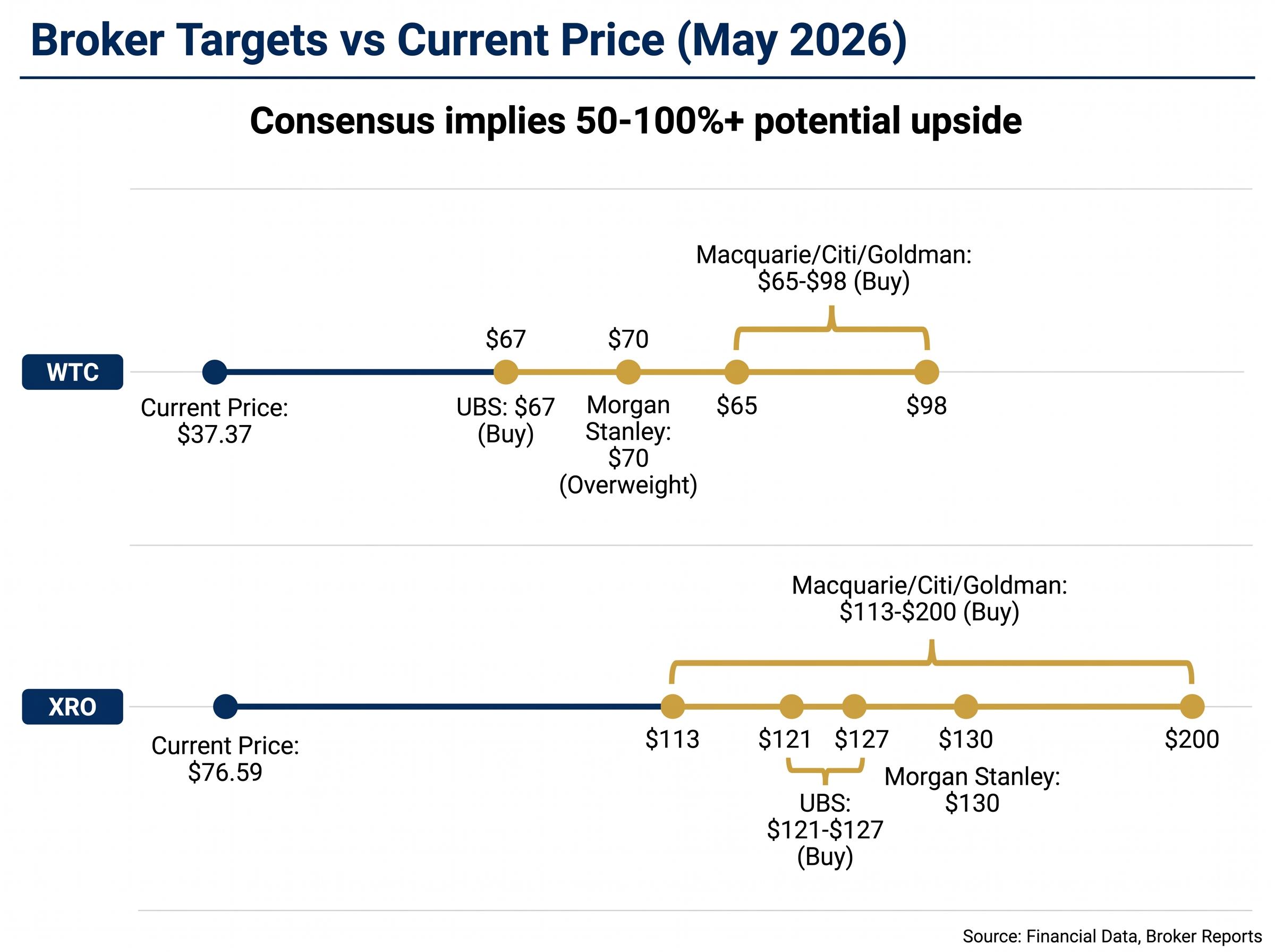

The cuts themselves were substantial. Morgan Stanley reduced its WTC price target to $70 and its XRO target to $130, representing approximately 20% reductions across the sector. Yet the broker maintained its Overweight rating on WTC and continued coverage on XRO. For investors reading the note in real time, this created a mixed signal: the valuation concern was loud, but the rating said the broker still liked the stocks on a longer time horizon.

WTC peaked above $120 in mid-2025. From there, the decline was sustained and severe. The stock reached a 52-week low of $35.54 before closing at approximately $37.37 on 25 May 2026, a year-to-date loss of roughly 45%.

XRO traced a similar path. After reaching $196.52 during 2025, the stock fell to a 52-week low of $67.93 before settling at $76.59 on the same date, a 33% decline for 2026.

The scale of these moves warrants attention not just for what they confirm but for what they complicate. Morgan Stanley’s revised WTC target of $70 now sits roughly 88% above the current price of $37.37. The broker called direction correctly, but both stocks fell well past the revised targets, which raises a separate question about the limits of even a well-reasoned broker forecast.

| Stock | 2025 Peak | Price (25 May 2026) | 52-Week Low | 2026 YTD Return |

|---|---|---|---|---|

| WTC | $121.31 | $37.37 | $35.54 | -45% |

| XRO | $196.52 | $76.59 | $67.93 | -33% |

Retail investors who sold on the Morgan Stanley cut may have avoided further losses. Those who bought on the maintained Overweight rating faced significant drawdowns. Neither interpretation of the mixed signal delivered a clean outcome.

A broker price target is a 12-month valuation estimate derived from a specific methodology, whether discounted cash flow analysis, price-to-earnings multiples, or price-to-sales ratios. It represents where an analyst’s model places fair value given a set of inputs. It is not a prediction of where the stock will trade.

A broker price target is a 12-month valuation estimate derived from a specific methodology, whether discounted cash flow analysis, price-to-earnings multiples, or price-to-sales ratios, and the valuation metrics underpinning each approach carry different sensitivities to interest rate assumptions, making the choice of methodology itself a source of divergence when macro conditions shift.

This distinction matters because the inputs driving the model, not the business itself, are often what change when a target is revised. When Morgan Stanley wrote that valuations were “anchored to outdated assumptions,” the analyst was signalling that the model’s inputs had shifted: interest rate assumptions, growth rate forecasts, or the discount rate applied to future cash flows. The business may have been performing in line with expectations while the valuation framework around it moved.

The ASIC RG 175 conduct obligations that apply to financial product advisers require clear disclosure of the basis on which recommendations are made, a standard that underscores why retail investors should pay close attention to whether a broker note constitutes general or personal advice before acting on a price target revision.

A rating change, such as a downgrade from Buy to Hold or Sell, is a strong directional signal. It tells the market the analyst’s overall view of the stock has shifted. A price target reduction, by contrast, is a recalibration. It may reflect changing macro conditions rather than deteriorating business performance.

In the case of WTC and XRO, major brokers maintained Buy or Overweight ratings throughout the target reduction period. That specific pattern carries a specific interpretation: the analysts still believed in the long-term thesis but recalibrated what they were willing to pay for it in the current environment.

When any broker cuts a price target on an ASX stock, three questions separate a useful reading from a reactive one:

Morgan Stanley was not alone in maintaining a constructive view. As of May 2026, Buy or Overweight ratings on both stocks were broadly maintained across the major institutional brokers covering the ASX technology sector, even as targets varied widely.

| Broker | WTC Target | WTC Rating | XRO Target | XRO Rating |

|---|---|---|---|---|

| Morgan Stanley | $70 | Overweight | $130 | — |

| UBS | $67 | Buy | $121-$127 | Buy |

| Macquarie / Citi / Goldman Sachs | $65-$98 | Buy | $113-$200 | Buy |

The gap between these targets and prevailing share prices is striking.

Consensus price targets across major brokers imply potential upside of 50-100%+ relative to market prices as of May 2026 on multiple individual broker notes.

That gap presents Australian investors with a binary question: either the consensus is right and the market is mispricing both stocks, or the consensus has not yet fully adjusted to a deteriorating outlook. AI integration, the medium-term theme underpinning most constructive broker ratings, has not yet driven a near-term re-rating. The bullish narrative is intact in research notes; it has not yet arrived in the share price.

The WTC and XRO declines were not isolated. Pro Medicus experienced similar dynamics over the same period, and the ASX technology sector was among the weakest performers across multiple reporting periods through 2025 and into early 2026. This was a sector-wide repricing, driven by a mechanism that applies to any high-multiple growth stock.

The mechanism operates in three steps:

High-growth software companies like WTC and XRO derive most of their theoretical value from earnings several years into the future. When discount rates shift, these stocks absorb a disproportionate share of the valuation impact compared to businesses with nearer-term cash flow profiles.

The mechanism behind both declines is the discount rate channel: as yields rise, the present value of cash flows projected several years out falls, compressing the multiples investors are willing to pay even when the underlying business delivers on its revenue targets.

Most broker commentary characterised the post-correction multiple reset as a valuation normalisation rather than a deterioration in underlying business quality. Both companies retained their structural growth drivers: logistics software for WiseTech, cloud accounting for Xero. What changed was the price the market assigned to those drivers.

Historical patterns in high-multiple ASX growth names suggest that significant drawdowns and broker target resets have, in prior cycles, sometimes been followed by material recoveries when macro conditions shifted. That is a pattern, not a guarantee, and it depends on whether the business fundamentals hold through the compression period.

With consensus targets sitting 50-100%+ above current prices and ratings broadly maintained at Buy or Overweight, the central question is whether the Morgan Stanley thesis represents a completed correction or the beginning of a more prolonged de-rating.

Two competing interpretations sit side by side. The constructive case holds that underlying business quality in WTC and XRO is intact, multiples have normalised to levels closer to sector peers, and a macro rotation back toward growth remains the missing catalyst. The cautious case argues that consensus has not yet fully repriced for sustained lower growth, and that broker targets will continue to fall as analysts absorb further data.

Late-cycle macro positioning from Morgan Stanley and Bank of America, which flagged a potential 10-20% drawdown in 2026 and recommended a defensive tilt toward quality balance sheets and cash-flow-rich businesses, provides the broader market backdrop against which the WTC and XRO correction unfolded.

Neither reading is obviously correct. Australian retail investors tracking these stocks in the months ahead should focus on three specific signals rather than anchoring to any single broker note:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Morgan Stanley’s April 2025 thesis was correct that valuations were stretched. Both WTC and XRO declined materially from the levels at which the note was published. But neither the broker nor the broader market anticipated the depth of the correction that followed. WTC at $37.37 sits roughly 47% below Morgan Stanley’s own revised target of $70. XRO at $76.59 sits 41% below its revised target of $130.

The takeaway for Australian retail investors is specific: broker price target cuts are meaningful signals about valuation model inputs. They are not necessarily signals about business quality. The rating, whether it shifts from Buy to Hold or remains unchanged, is the stronger directional indicator.

Both stocks sit at significant discounts to consensus targets as of May 2026, which makes the next set of earnings results and any further broker note revisions the data points worth watching most closely.

Earnings report interpretation at each upcoming reporting date will be the next key test for both stocks: a result that beats headline revenue estimates but cuts forward guidance carries a materially different signal than one that misses estimates while maintaining full-year outlook, and the two scenarios require different investor responses.

A maintained Buy rating alongside a price target cut is a different signal from a rating downgrade. Confusing the two is one of the most common mistakes retail investors make when reading broker notes.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

A broker price target cut is a revision to a 12-month valuation estimate derived from models such as discounted cash flow analysis or price-to-earnings multiples. It often reflects changes in model inputs like interest rate assumptions or discount rates rather than a deterioration in the underlying business.

A rating downgrade, such as moving from Buy to Hold or Sell, is a strong directional signal that the analyst's overall view of the stock has shifted, while a price target reduction is a recalibration that may only reflect changing macro conditions. Confusing the two is one of the most common mistakes retail investors make when reading broker notes.

Both stocks fell sharply because rising or persistently elevated interest rates increased the discount rate applied to future cash flows, reducing the present value of earnings projected several years out and compressing the high growth multiples both companies had been trading on. WiseTech fell roughly 45% year-to-date by May 2026 and Xero fell approximately 33% over the same period.

Investors should ask three questions when a price target is cut: whether the rating itself changed, whether the revision reflects model inputs like interest rates or actual business deterioration such as a revenue miss, and where the new target sits relative to consensus across other brokers covering the same stock.

As of May 2026, consensus broker price targets across major institutions imply potential upside of 50-100% or more relative to prevailing share prices, with WiseTech trading near $37 against targets ranging from $65 to $98 and Xero trading near $76 against targets ranging from $113 to $200.