A business development team that cold-calls roughly 70,000 to 100,000 private software companies twice a year, every year. That is not a sales operation. It is an acquisition intelligence network with no real equivalent in global markets. Constellation Software has completed more than 1,100 acquisitions across nine operating groups and now deploys more than $1.5 billion annually in acquisition consideration, yet most investors still struggle to articulate precisely why the Constellation Software business model is so difficult to imitate. That difficulty has intensified through 2025 and into 2026 as AI disruption narratives have raised questions about whether entrenched software incumbents face a period of structural vulnerability. What follows is a deconstruction of the specific mechanisms that make Constellation’s acquisition engine compound over time, an explanation of why competitors who understand the model still cannot execute it, and a case that AI is more likely to expand the economic moats of Constellation’s portfolio companies than erode them.

The machine behind the numbers: how Constellation actually acquires companies

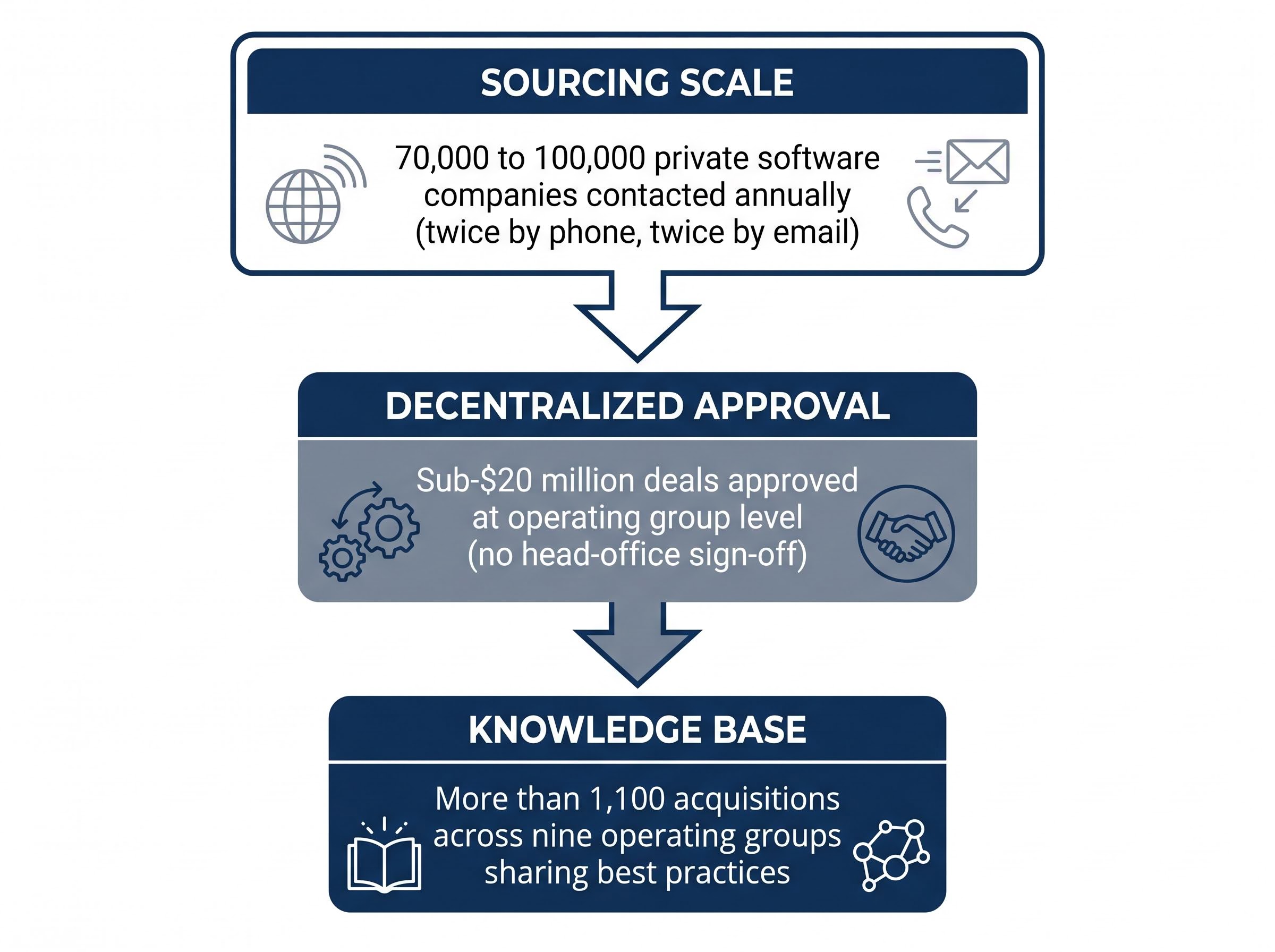

The sourcing funnel operates at industrial scale. Constellation’s business development teams contact between 70,000 and 100,000 private vertical market software companies per year, reaching each target twice by phone and twice by email. The cadence is fixed. The pipeline never stops.

Sourcing scale: Constellation contacts between 70,000 and 100,000 private vertical market software companies annually, a volume no competitor has matched.

What makes this velocity possible is the approval architecture underneath it. Transactions below approximately $20 million require no head-office sign-off. Operating groups identify, negotiate, close, and onboard acquisitions independently, which removes the bottleneck that slows every centralised acquirer in the market. Larger deals go through headquarters review, but the small-deal engine runs in parallel, continuously.

The four components of this system form a self-reinforcing loop:

- Outreach volume: 70,000-100,000 companies contacted per year, generating a proprietary pipeline of relationship intelligence

- Fixed cadence: Twice by phone, twice by email, every year, ensuring no target falls out of the funnel permanently

- Decentralised approval: Sub-$20 million deals approved and executed at the operating group level without headquarters involvement

- Best-practices repository: A continuously growing knowledge base derived from more than 1,100 prior acquisitions, available to every acquired company but imposed on none

Acquired businesses are not operationally directed from above. They receive access to this repository, which is itself a compounding asset: each new acquisition adds operational data, pricing intelligence, and integration learnings that improve the next deal’s onboarding. In FY 2025, Constellation deployed approximately $1.579 billion in acquisition consideration. Q1 2026 alone accounted for approximately $809 million, with a further $786 million completed or committed shortly thereafter.

When big ASX news breaks, our subscribers know first

Why vertical market software is the right hunting ground

Constellation does not acquire software companies generically. It targets vertical market software, meaning applications built for a single industry or a narrow operational niche within an industry. A billing system for municipal water utilities. A scheduling platform for veterinary clinics. A compliance tool for European insurance brokers.

These businesses share a set of structural characteristics that make them unattractive to most acquirers and deeply attractive to Constellation. Their addressable markets are small, often too small to justify a private equity fund’s minimum return expectations. Switching costs are high because the software is embedded in daily workflows, regulatory processes, and reporting obligations that cannot be replicated overnight. Regulatory complexity adds a further layer of entrenchment: a new competitor must understand not only the technology but the specific compliance environment the software serves.

Software switching costs in vertical markets are structurally different from those in horizontal SaaS platforms because the embedded workflows span regulatory obligations, compliance reporting, and daily operational processes that cannot be lifted and shifted to a new vendor without significant disruption to the customer’s core business.

The result is that private equity firms, which need to engineer exits within defined holding periods, find these businesses structurally incompatible with their model. The deals are too small for meaningful fund-level returns, and the businesses do not benefit from the leveraged restructuring playbook that PE deploys in larger transactions.

| Attribute | Constellation Software | Private equity | Large strategic acquirers |

|---|---|---|---|

| Typical deal size | Sub-$20M (majority) | $50M-$500M+ | $100M-$1B+ |

| Holding period | Permanent | 3-7 years | Indefinite but integration-dependent |

| Operational integration | Autonomous; best-practices shared | Active restructuring | Full integration into parent |

| Capital return requirement | Reinvested into next acquisition | Exit-driven IRR target | Synergy-driven ROI |

The economics of buying small and holding forever

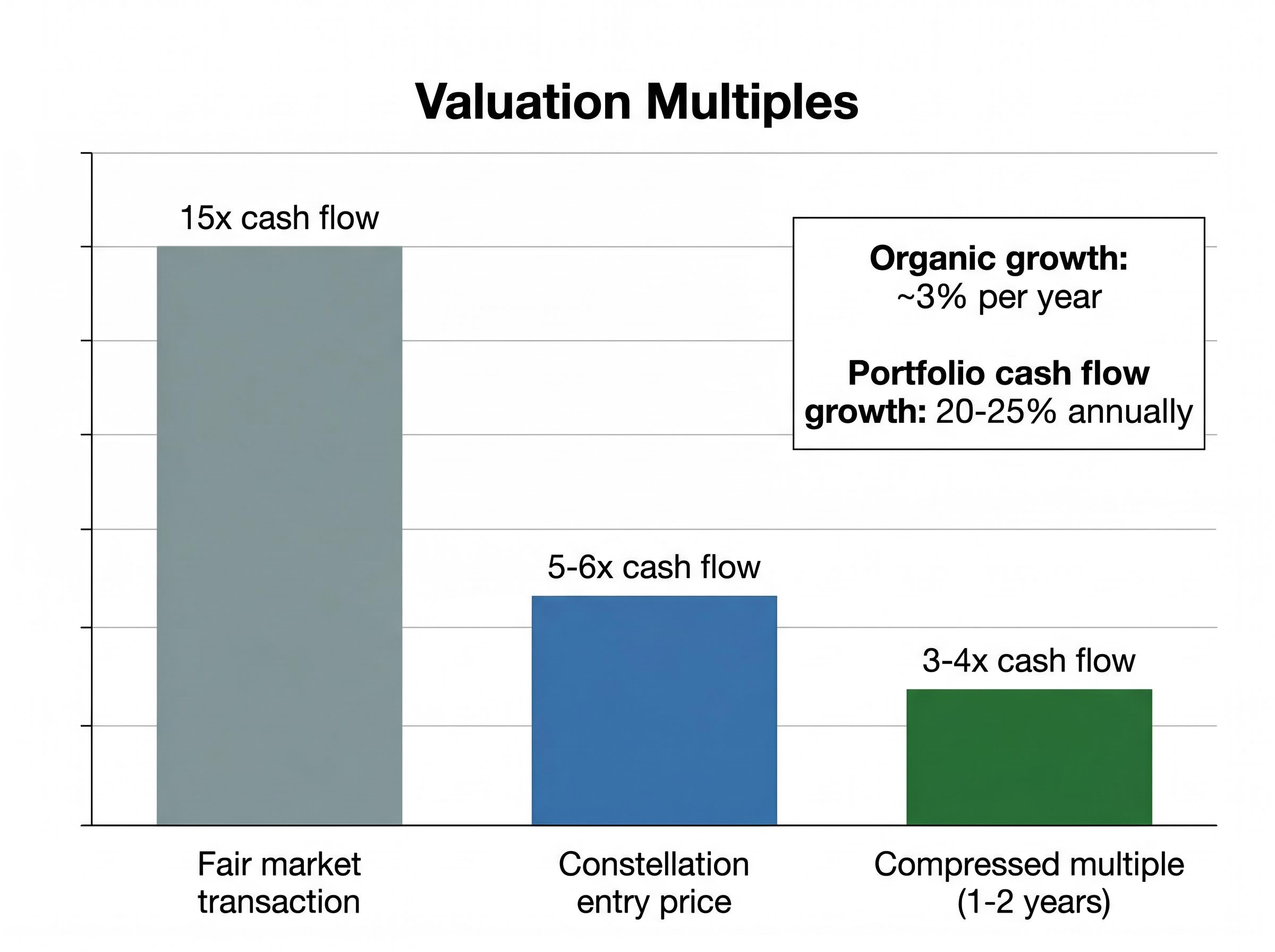

The financial mechanics compound in Constellation’s favour. Acquired businesses typically grow organically at approximately 3% per year, a modest rate that reflects the stable, low-churn nature of vertical market software. Yet at the portfolio level, combined cash flow growth reaches approximately 20-25% annually when acquisition activity and operational improvements are layered on top.

The entry price tells the story. Constellation typically acquires at approximately 5-6 times cash flow. Within one to two years, pricing adjustments and operational improvements compress that effective multiple to approximately 3-4 times cash flow, without requiring integration, restructuring, or management replacement. Permanent ownership removes the need to engineer an exit, which is itself a source of value that no time-limited holding model can replicate structurally.

The imitation problem: why competitors understand the model but cannot run it

Constellation’s model is not proprietary. It is not secret. Mark Leonard’s annual shareholder letters describe the philosophy in detail. Analysts study the acquisition cadence, the return thresholds, and the governance architecture. Competitors can read everything. The paradox is that none have replicated it at comparable scale.

The barriers are not informational. They are institutional, and they compound with time.

- Sourcing funnel depth: Building a network that contacts 70,000-100,000 companies annually requires years of relationship development, staffing, and cultural investment. No new entrant can shortcut this with capital alone.

- Decentralised cultural norms: Operating group autonomy at Constellation is not a policy. It is a deeply internalised set of behaviours that evolved across more than 1,100 acquisitions. A policy document cannot produce it.

- Best-practices repository scale: The knowledge base only becomes competitively valuable after hundreds of acquisitions have populated it with sector-specific operational data. A competitor with 20 acquisitions has a filing cabinet. Constellation has an institutional memory.

The broader market could, in theory, support three or four Constellation-style entities. None currently exist.

Topicus and Lumine Group extend the model into specific geographies and verticals, but both remain sub-scale relative to the parent. According to a 2024 Veritas Investment Research note, no acquirer has matched Constellation’s combination of sourcing density, underwriting discipline, and post-acquisition autonomy at scale. Roper Technologies pursues a different deal profile: larger, fewer, more integrated transactions that do not replicate Constellation’s granular engine. The imitation gap does not narrow with time. It widens, because each year Constellation completes adds to the institutional capability stack that competitors would need to build from scratch.

AI and the software moat: why disruption narratives misread the incumbency advantage

The investor anxiety is specific and worth naming directly. If AI allows new entrants to build competitive software faster and cheaper, does that compress the switching cost moat underpinning Constellation’s entire portfolio? If a generative AI tool can produce in weeks what took an incumbent years to develop, does the installed base become a depreciating asset rather than a compounding one?

The mechanism-level answer runs against the anxiety. Four specific dynamics explain why AI reinforces rather than erodes vertical market software moats:

Software moat differentiation has become the central analytical task of 2026, with the spread between the top and bottom deciles of US technology stocks reaching a record 133 percentage points, a level of dispersion that rewards investors who can identify which incumbents possess structural advantages durable enough to survive AI-driven competitive pressure.

- Domain data advantage: AI features perform better when trained on rich, domain-specific data. Incumbents already possess this data through years of customer workflows, transaction histories, and regulatory filings. New entrants must achieve comparable domain coverage and data scale before their AI features become competitive.

- Rising switching costs from AI workflow accumulation: According to the Software Equity Group 2026 Annual SaaS Report, switching costs are rising in many verticals because customers must rebuild AI-enhanced workflows and automations, not just replace core systems.

- Margin expansion through development productivity: AI reduces development costs and accelerates feature delivery, improving operating margins over time. Mark Leonard’s 2023 shareholder letter framed AI in precisely these terms: as an incremental margin-accretive tool, not an existential threat.

- New entrant disadvantage on data scale: Newcomers must not only build core functionality but also achieve comparable domain coverage and data scale to deliver competitive AI features in specialised verticals.

The Software Equity Group 2026 SaaS Report documents that switching costs are rising across many verticals as customers must rebuild AI-enhanced workflows and automations rather than simply replace core systems, a dynamic that structurally favours incumbents with deeply embedded installations over new entrants offering comparable core functionality.

Software Equity Group, 2026 Annual SaaS Report: Switching costs are rising because customers must rebuild AI-enhanced workflows and automations, not just replace core systems.

Coding represents approximately one-fifth of total software value creation, as investor Mohnish Pabrai has framed it. AI-driven productivity in development does not proportionally erode the workflow integration, regulatory familiarity, and trust relationships that define incumbency. Ben Thompson of Stratechery argued in 2025 that incumbents with sticky workflows and trusted brands are favoured when AI becomes a feature layer rather than a standalone product. The logic applies directly to Constellation’s portfolio: AI is additive to the moat, not corrosive.

Vertical software bolt-on acquisitions that add AI capability layers to an existing domain-specific platform, such as Gentrack’s NZ$24 million acquisition of Factor’s machine learning pricing engine, illustrate the practical mechanics of how incumbents with deep regulatory and workflow entrenchment are using M&A to accelerate AI feature delivery rather than building from scratch.

Capital allocation at scale: how the model evolves without losing its character

The capital deployment trajectory tells a clear story. FY 2025 total acquisition consideration reached approximately $1.579 billion. Q1 2026 alone accounted for approximately $809 million, with a further $786 million completed or committed shortly thereafter. Constellation is deploying more capital in mid-sized and larger transactions as its capital base has grown.

Q1 2026 deployment: approximately $809 million in acquisition consideration in a single quarter, reflecting both continued high-volume activity and the capacity to execute larger transactions.

The governance structure accommodates this shift without centralising. Large deals go through head-office review, while the operating group layer continues to approve and execute smaller transactions independently. The high-volume, small-deal engine has not been replaced. It runs in parallel with a growing capacity for larger platform acquisitions.

The acquisition multiples reinforce the discipline. A business growing at 3% in a normalised interest rate environment would reasonably command approximately 15 times cash flow in a fair market transaction. Constellation enters at 5-6 times. That spread is the return engine, and it has not compressed despite rising deployment volumes.

What the valuation premium tells investors

Constellation trades at structurally higher multiples than the average software or diversified industrial peer group. Canadian bank research from RBC, BMO, and National Bank attributes this premium to capital allocation discipline and acquisition runway depth rather than speculative growth expectations.

The premium reflects market recognition of the acquisition engine’s scarcity value. It is worth noting that the original investment opportunity identified in earlier research occurred when Constellation traded at a low-teens earnings multiple, illustrating that the premium is not permanent and that dislocations create entry points for patient capital.

A model built to outlast its moment

Three structural characteristics make Constellation’s model genuinely difficult to dislodge, and each compounds with time rather than depreciating:

- The sourcing network: A proprietary pipeline covering tens of thousands of private software companies, maintained through fixed-cadence outreach that no competitor has replicated at scale

- The permanent holding philosophy: No exit timeline means no forced sales, no restructuring for resale, and no value leakage to intermediaries

- The scale-dependent best-practices repository: A knowledge base that grows with every acquisition and improves the operational trajectory of every subsequent deal

These characteristics were designed for a world where switching costs and domain expertise compound over time. That is precisely the world AI is reinforcing. Incumbent data advantages grow as AI features layer onto existing workflows. Switching costs rise as customers embed AI-enhanced automations into entrenched systems. The model was not built for a particular market era. It was built for the structural reality of specialised software markets.

The forward-looking question for investors is not whether the model is durable. It is whether the capital deployment pace and return thresholds can be maintained as deal sizes grow and the addressable pool of sub-$20 million software businesses gradually depletes. From 132 acquisitions in FY 2023 to over $1.5 billion deployed in FY 2025, the trajectory reflects both higher volumes and larger individual transactions. No Constellation-equivalent has emerged despite full transparency of the model, which suggests the institutional capability gap is structural rather than temporary.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.