In May 2026, a company called Global Pacific Solutions Group Pty Ltd lost its Australian financial services licence. The ground was not fraud, not client harm, not a breach of conduct standards. It was something far more mundane: the business had stopped operating. That distinction, between cancellation for misconduct and cancellation for cessation, matters more than most people realise.

AFS licence cancellations happen more often than the general public appreciates. In the 2024-25 financial year alone, ASIC cancelled or suspended 215 AFS licences, according to ASIC REP 825 (published November 2025). Understanding why and how ASIC can revoke a licence is relevant knowledge for investors relying on licensed intermediaries, business owners holding licences, and anyone working within the Australian financial services ecosystem.

What follows uses the Global Pacific Solutions Group cancellation as a real-world anchor to explain the legal framework governing AFS licence revocation, what the “ceased to carry on a business” trigger actually means in practice, what happens to affected entities, and what review rights remain available.

What just happened: the Global Pacific Solutions Group cancellation

Global Pacific Solutions Group Pty Ltd held AFS licence number 514164, granted on 24 February 2019. On 20 May 2026, ASIC cancelled that licence, ending approximately seven years of holding.

The core facts at a glance:

- Entity: Global Pacific Solutions Group Pty Ltd

- AFS licence number: 514164

- Cancellation effective: 20 May 2026

The ground ASIC cited was not misconduct. It was cessation of business, specifically under s 915B(3)(a) of the Corporations Act 2001 (Cth). ASIC’s media release confirmed the action was taken because the licensee had ceased to carry on a financial services business.

ASIC may cancel an AFS licence if the licensee has ceased to carry on a financial services business (s 915B(3)(a), Corporations Act 2001).

That statutory ground is worth understanding in detail, because it operates differently from the enforcement actions that tend to attract public attention. No investigation into wrongdoing was required. No penalty was imposed. The licence was cancelled because the business behind it was no longer operating, and the law required ASIC to act once that fact was established.

When big ASX news breaks, our subscribers know first

What an AFS licence is and why its cancellation matters

An AFS licence is the legal authorisation required to carry on a financial services business in Australia. Issued by ASIC under Part 7.6 of the Corporations Act 2001 (Cth), it covers activities ranging from providing financial product advice to dealing in financial products. Without one, an entity cannot lawfully offer these services.

What the public register is for

The ASIC register of licensed entities serves a transparency function. Consumers, counterparties, and professional advisers use it to verify that they are dealing with an authorised provider. When a licence is cancelled, even on non-misconduct grounds, it means the entity can no longer lawfully provide financial services. The register’s accuracy depends on inactive licences being removed.

The same register-accuracy principle operates across Australian financial services regulation more broadly; the ADI licence cancellation affecting in1Bank by APRA followed a similarly structured process, with all depositor funds returned before the formal revocation took effect.

The scale of ASIC’s register-management activity is considerable. Data from ASIC REP 825 shows the breakdown for FY 2024-25:

ASIC REP 825, published in November 2025, provides the full dataset on licensing and professional registration activity for FY 2024-25, including the breakdown of cancellations initiated by ASIC versus those requested by licensees, and the number of suspensions recorded across the period.

| Category | Count |

|---|---|

| Cancelled by ASIC | 51 |

| Cancelled on request | 144 |

| Suspended | 20 |

| Total | 215 |

The majority of cancellations were initiated by the licensees themselves. But the 51 cancelled by ASIC reflect cases where the regulator acted, whether because the licensee had ceased operating, failed to meet obligations, or both.

The legal trigger: how s 915B(3)(a) works

The provision that ended Global Pacific Solutions Group’s licence is not a discretionary power. It is a mandatory obligation. Once ASIC is satisfied that a licensee has ceased to carry on a financial services business, s 915B(3)(a) of the Corporations Act 2001 requires ASIC to cancel the licence. The word is “must,” not “may.”

That mandatory character is what distinguishes this ground from most other regulatory actions. ASIC does not need to weigh proportionality, conduct an investigation into wrongdoing, or engage in a prolonged show-cause process. The trigger is factual: has the business stopped operating?

The types of evidence ASIC considers when assessing whether cessation has occurred include:

- Cessation of services to clients

- Absence of revenue from financial services activities

- Departure of responsible managers and staff

- Closure of offices

- Removal of authorised representatives

- Any notification from the licensee that it has ceased business

Once the factual precondition of cessation is established to ASIC’s satisfaction, the mandatory cancellation obligation arises. ASIC is required to cancel, not merely empowered to do so.

Recent cases confirm this is not a one-off pattern. LRA Corporate was cancelled in February 2025 after it ceased to operate. Superfast AM Pty Ltd and Red Panda Future Wealth Pty Ltd were both cancelled in February 2026 on the same basis. Oscar Oliver Capital was suspended under s 915B(3)(a) after ASIC found it had ceased carrying on the business.

How this differs from misconduct-based cancellation

Other grounds within s 915B, such as non-compliance with licence obligations, insolvency, or public interest concerns, are discretionary. They typically involve investigation, a show-cause process, and regulatory engagement before action is taken. The licensee usually has an opportunity to respond, remediate, or contest the proposed action before it becomes final.

Section 915B(3)(a) does not work that way. Its trigger is purely factual. If the business has stopped, the cancellation follows. That is why cessation-based cases can move more quickly and with less procedural forewarning than misconduct-based enforcement.

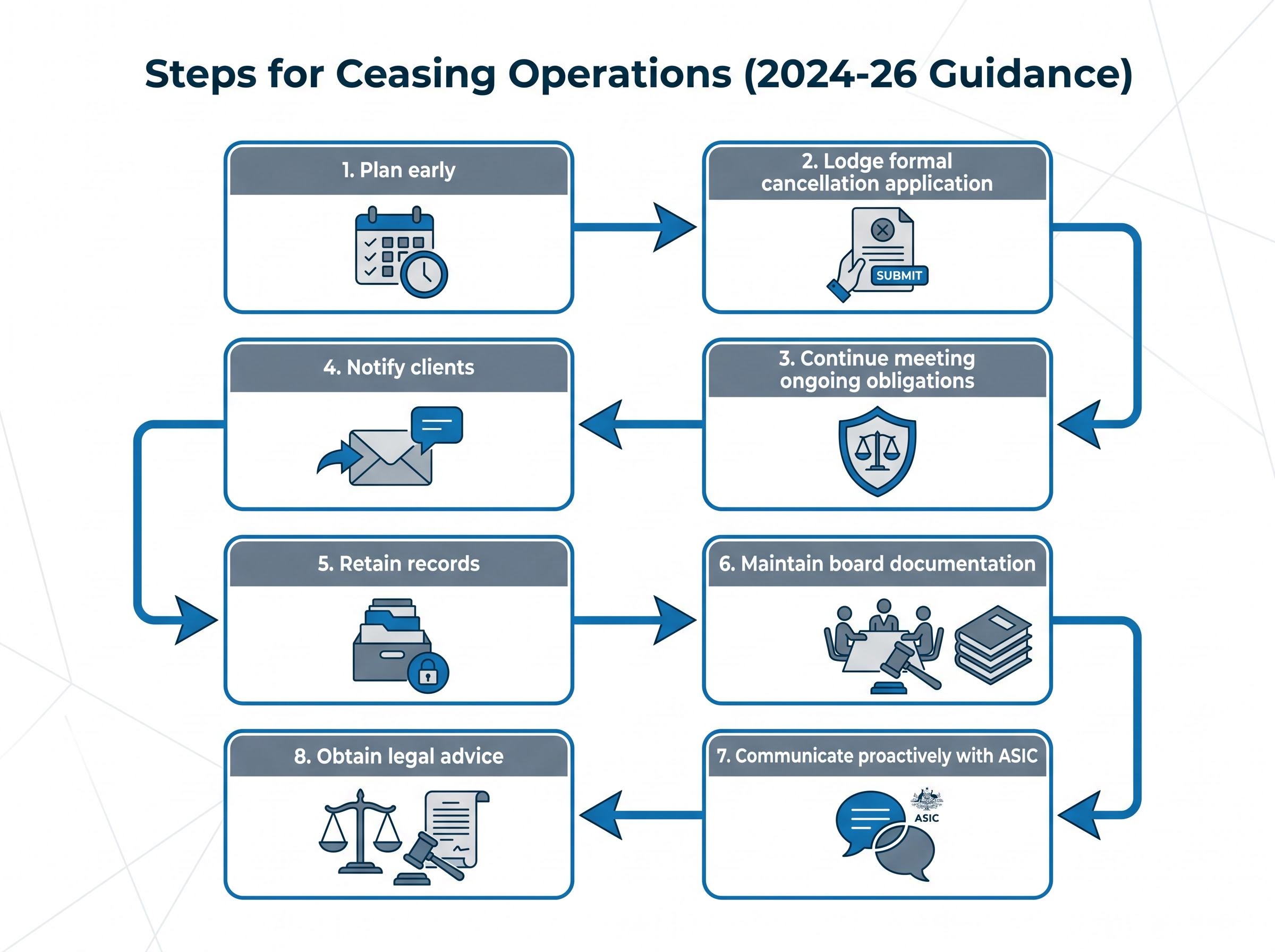

What licensees must do when they stop operating

The practical expectation is straightforward: licensees that have decided to cease providing financial services should proactively apply for cancellation or variation of their licence rather than leaving it dormant. Current compliance guidance from 2024-26 outlines the following recommended sequence:

- Plan early: Initiate the cancellation or variation process as soon as it is clear the business will cease providing financial services.

- Lodge a formal cancellation application with ASIC using its online portals or prescribed forms.

- Continue meeting all ongoing obligations until the effective cancellation date, including financial statements, client money reconciliations, and dispute resolution membership.

- Notify clients and transfer or wind down client positions appropriately.

- Retain records for the required retention period.

- Maintain board documentation of decisions taken and steps followed to cease business and protect clients.

- Communicate proactively with ASIC where complexity exists, such as run-off obligations or legacy products.

- Obtain legal advice on whether full cancellation or a narrower variation of authorisations is more appropriate if any residual activities continue.

A dormant AFS licence is not a neutral administrative state. It is a live source of ongoing regulatory obligations and potential breach exposure.

The risks of inaction are real. Under s 912A, obligations relating to adequate competence, resources, financial reporting, and breach reporting continue to apply regardless of whether the business is actively operating. ABL Funds Management Pty Ltd was cancelled in April 2026 specifically for failure to lodge financial reports and auditor opinions, an illustration of what can happen when ongoing obligations lapse after a business effectively ceases operating.

The risks attached to ongoing s 912A obligations do not disappear because a business has wound down its client-facing operations; the $1.55 million Federal Court penalty against Money3 Loans for responsible lending breaches across just five historical loans demonstrates that courts and regulators will pursue compliance failures from prior operating periods regardless of subsequent business changes.

How affected entities can challenge the decision: merits review rights

Cancellation is not necessarily final. An entity whose AFS licence is cancelled retains the right to seek merits review of ASIC’s decision, including decisions made under s 915B. The ASIC media release for Global Pacific Solutions Group explicitly noted this retained right.

Merits review means the tribunal considers the matter afresh, standing in ASIC’s position (a de novo standard of review). It is not limited to the materials or reasoning that ASIC relied on when making its original decision. The tribunal may reach one of four outcomes:

- Affirm ASIC’s decision

- Vary the decision

- Set aside the decision

- Substitute its own decision

Interim stays or orders preserving the licence pending a final determination remain available where appropriate circumstances exist. The standard window for lodging a review application is 28 days, or as specified in the decision notice.

AAT or ART: which applies to your review?

A structural change took effect on 14 October 2024. The Administrative Review Tribunal (ART) replaced the Administrative Appeals Tribunal (AAT) as the body conducting merits review of Commonwealth government decisions, pursuant to the Administrative Review Tribunal Act 2024 (Cth).

The Attorney-General’s Department guidance on the ART confirms the commencement date of 14 October 2024 and the legislative basis for the transition, providing the official record of how the new tribunal was established and which legacy AAT matters were carried across under the transitional arrangements.

Applications lodged before 14 October 2024 continue through AAT processes. New applications from that date onward go to the ART. The transition arrangements preserve all existing statutory merits-review rights under the Corporations Act 2001, so the change is procedural rather than substantive. The right to challenge an AFS licence cancellation remains intact.

What the Global Pacific case signals about how ASIC manages the licensing register

The Global Pacific Solutions Group cancellation is consistent with a clear ASIC position: the AFS register should be a live, accurate public record, not an administrative archive of former licensees. When a business stops operating, the licence should go with it.

The pattern of recent cessation-based cancellations reinforces this. Beacon Wealth, Ballast Financial Management, LRA Corporate, Superfast AM, Red Panda Future Wealth, and Oscar Oliver Capital were all subject to ASIC action under s 915B(3)(a) across 2025 and 2026. Combined with the 215 total cancellations and suspensions recorded in FY 2024-25, the data points to sustained register-management activity rather than isolated enforcement.

ASIC’s licensing enforcement posture has hardened considerably across multiple sectors in 2025-2026, extending well beyond AFS licence cancellations for ceased businesses into active Federal Court proceedings against crypto platforms operating without adequate compliance infrastructure, a shift that signals the regulator’s intention to treat licensing requirements as substantive obligations rather than administrative formalities.

The public register is designed to reflect only entities that are genuinely carrying on a financial services business. ASIC has both the obligation and the tools to enforce that standard.

For investors, this is reassuring: a licence appearing on the register reflects a genuinely operating entity. For business operators, the signal is equally clear. If a financial services business is winding down, proactive engagement with ASIC on licence cancellation is the lowest-risk path. Dormancy is not a neutral option; it is a choice with regulatory consequences.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.