Five consumer car loans. $1.55 million in Federal Court penalties. That ratio was deliberate, and it is the point.

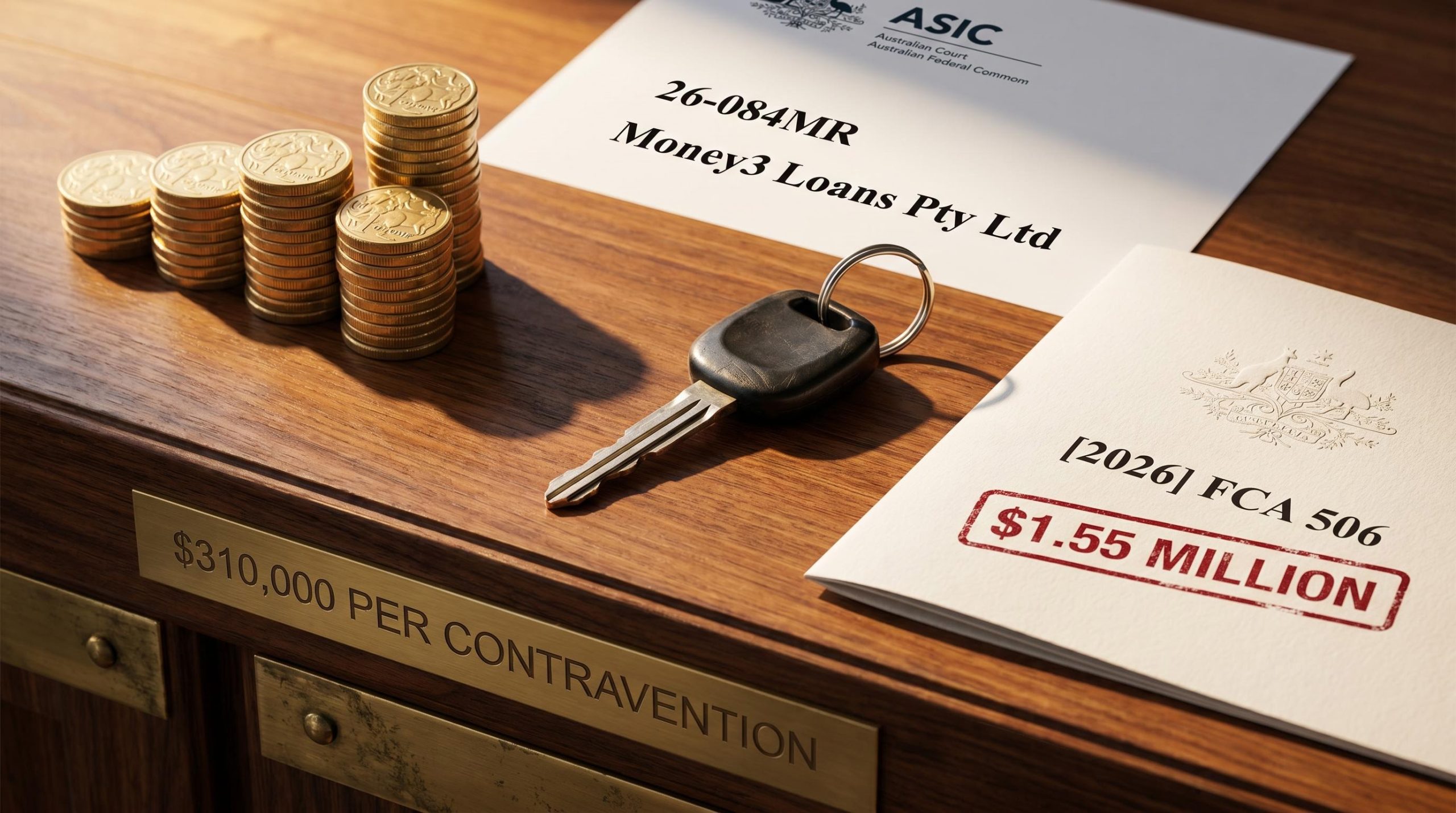

On 27 April 2026, the Federal Court ordered Money3 Loans Pty Ltd to pay $1.55 million for responsible lending breaches across five car finance products issued to financially vulnerable Australians between 2019 and 2021. The case, brought by the Australian Securities and Investments Commission (ASIC) after proceedings commenced in May 2023, now stands as a named precedent ([2026] FCA 506) with implications that stretch well beyond a single non-bank lender. What follows is a breakdown of what Money3 was found to have done wrong, what Justice McElwaine’s deterrence reasoning means for all credit licensees, and where Australia’s motor vehicle finance regulation is heading in 2026.

What a $1.55 million penalty across five car loans actually tells the market

Justice McElwaine’s penalty judgment, delivered on 27 April 2026 ([2026] FCA 506), ordered Money3 Loans Pty Ltd to pay $1.55 million across five separate contraventions of responsible lending obligations. The loans were originated between May 2019 and February 2021.

The per-contravention figure matters. At approximately $310,000 per loan, the penalty quantum was not an accident of arithmetic; it was a calibrated judicial choice.

$310,000 per contravention. Justice McElwaine’s penalty structure was designed to deliver both specific deterrence against Money3 and general deterrence across all credit licensees, signalling that the absolute number of affected loans does not diminish the seriousness of the conduct.

The procedural timeline underscores how long enforcement of this kind takes to conclude:

- 17 May 2023: ASIC commences Federal Court proceedings (23-126MR)

- September 2025: Liability judgment delivered

- 27 April 2026: Penalty judgment delivered ([2026] FCA 506)

A lender need not have issued thousands of unsuitable loans to face substantial penalties. Five was enough.

When big ASX news breaks, our subscribers know first

What Money3 actually did wrong: the court’s specific findings

The Federal Court identified two distinct categories of failure in Money3’s loan origination process:

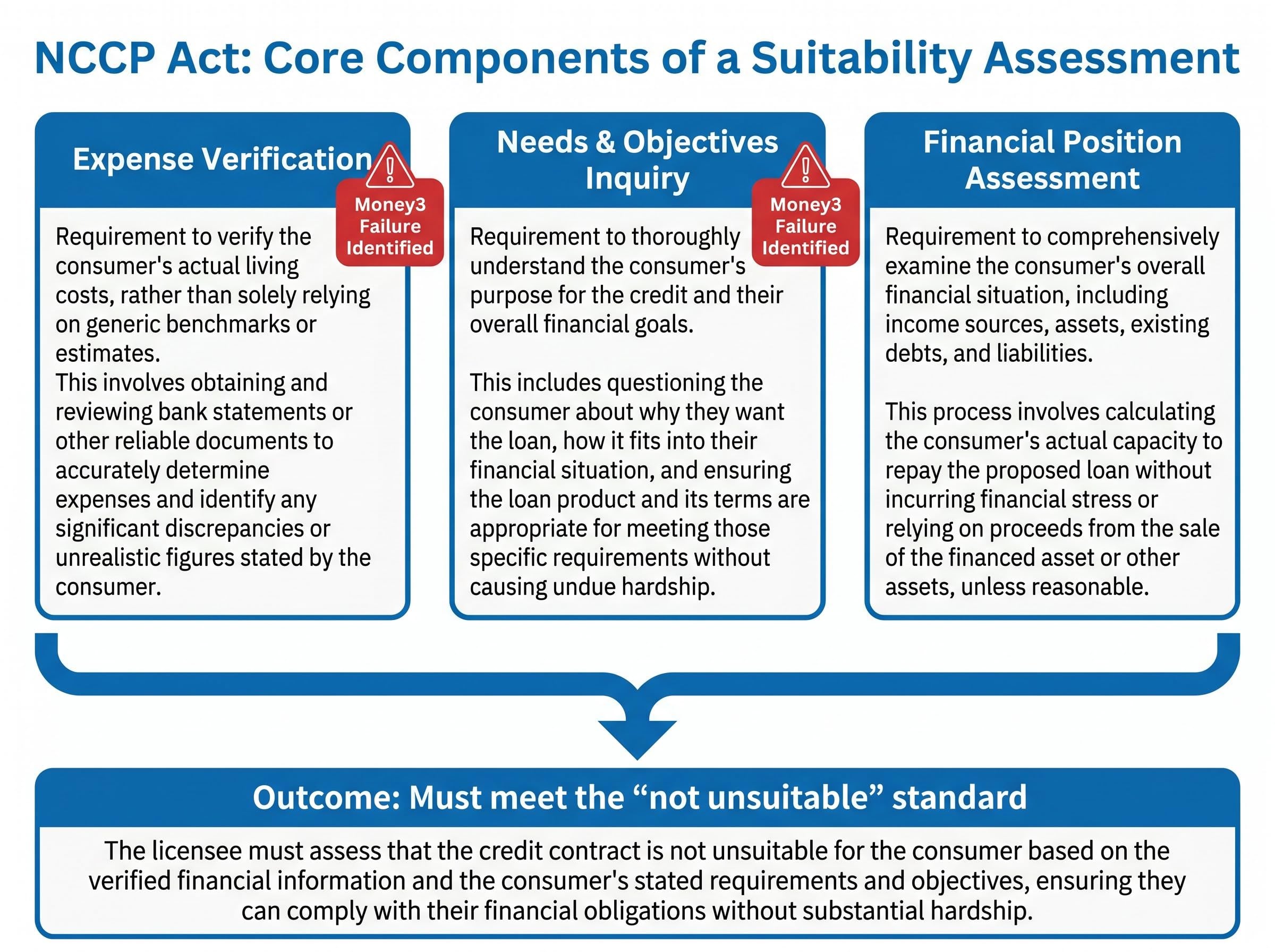

- Expense verification failure: Money3 held borrowers’ bank statement data but failed to adequately analyse that data to verify living expenses. Collecting the documents was not sufficient; the court found the company did not interrogate the information those documents contained.

- Needs and objectives inquiry failure: In at least one case, Money3 failed to make sufficient inquiries into the borrower’s financial needs and objectives before issuing the loan.

The distinction between these two failures is significant. The first concerns what a lender does with data it already possesses. The second concerns whether a lender asked the right questions in the first place. Money3 fell short on both counts across the five loans issued between May 2019 and February 2021.

How the court characterised the seriousness of the breaches

Justice McElwaine characterised the failures as undermining the fundamental purpose of responsible lending obligations under Australian credit law. The borrowers in question were financially vulnerable consumers who could not access mainstream bank lending, a factor the court treated as shaping the seriousness of the conduct rather than excusing it.

Both specific deterrence against Money3 and general deterrence across all credit licensees were active considerations in the penalty quantum. Cost determinations were deferred to a subsequent hearing.

Understanding responsible lending obligations under Australian credit law

The Money3 penalty rested on obligations established under the National Consumer Credit Protection Act (NCCP Act), the legislative framework governing consumer lending in Australia. The Act requires credit licensees to assess whether a loan is “not unsuitable” for the borrower before issuing the product. That assessment is not a procedural checkbox. It demands a genuine evaluation of the borrower’s actual financial position.

The three core components of a suitability assessment are:

- Expense verification: Making reasonable inquiries into, and taking reasonable steps to verify, the borrower’s financial situation, including living expenses

- Needs and objectives inquiry: Establishing the borrower’s requirements and objectives for the credit product

- Financial position assessment: Forming a view on whether the loan meets the “not unsuitable” standard given the borrower’s verified circumstances

These obligations apply to all credit licensees regardless of market position, covering direct lenders, broker channels, and dealer-originated finance alike. The Money3 case confirms the court will hold non-bank lenders to the same standard as major banks.

Why car finance presents particular responsible lending risks

Money3’s customer base consists substantially of borrowers excluded from mainstream bank lending. That concentration of financially vulnerable consumers in a single loan book raises the stakes of any process failure at the point of origination.

The broker and dealer distribution model common in car finance adds a further layer of risk. When a loan is originated through a third-party intermediary rather than directly, process gaps in inquiry and verification can emerge between the point of sale and the credit assessment. The court’s findings suggest Money3’s processes did not adequately bridge those gaps.

ASIC’s enforcement posture and what the ruling signals for all lenders

The Money3 penalty is not an isolated enforcement event. ASIC’s media release (26-084MR, 27 April 2026) positioned the outcome as part of a broader and active regulatory programme targeting non-bank lending conduct.

ASIC Chair Joe Longo acknowledged the case’s broader foundations:

“This outcome was assisted by the evidence and cooperation of consumer representatives and affected borrowers,” ASIC Chair Joe Longo stated, framing consumer advocate involvement as a model for future enforcement in this space.

ASIC’s confirmed 2026 enforcement priorities relevant to motor vehicle finance include:

- Misconduct exploiting consumers facing financial difficulty, including predatory lending practices

- Conduct targeting financially vulnerable consumers and First Nations communities

- Lender oversight of car finance distribution channels, including broker and dealer networks

Separately, ASIC announced a motor vehicle finance sector review in November 2025 (25-269MR). Preliminary findings highlighted gaps in lenders’ oversight of car finance distributors, with particular focus on outcomes for regional and First Nations consumers. Full findings from that review are expected by mid-2026.

For compliance teams and credit licensees, the timeline is clear. The Money3 penalty lands while the sector-wide review remains active, and ASIC has signalled that further enforcement actions may follow once the review’s findings are finalised.

Money3’s response and what it means for Solvar’s compliance trajectory

Solvar, the ASX-listed parent of Money3 Loans Pty Ltd, responded through CEO Scott Baldwin.

Solvar CEO Scott Baldwin characterised the penalty as a “legacy issue” relating to the 2019 to 2021 period, emphasising Money3’s role in providing consumer vehicle finance to borrowers excluded from traditional bank lending (The Adviser, 28 April 2026).

The “legacy issue” framing positions the conduct as historical rather than reflective of current practice. That distinction may prove relevant to Solvar’s forward compliance narrative, but it sits against a backdrop of active regulatory scrutiny. ASIC’s motor vehicle finance sector review remains underway with findings expected by mid-2026, and the regulator’s stated priorities continue to focus on the precise market segment in which Money3 operates.

Court cost determinations were deferred to a subsequent hearing, meaning the full financial impact of the proceedings on Solvar’s subsidiary has not yet been finalised.

The next major ASX story will hit our subscribers first

Where to go if you received a Money3 loan or believe a lender was unsuitable

Consumers who believe they received an unsuitable consumer loan have several avenues for assistance and redress:

- Australian Financial Complaints Authority (AFCA): The primary external dispute resolution pathway for unresolved complaints against financial services providers (www.afca.org.au)

- National Debt Helpline: Free and confidential financial counselling available by calling 1800 007 007

- Mob Strong Debt Helpline: A dedicated service providing free financial counselling for First Nations communities

- Moneysmart: ASIC’s consumer information resource covering loan products, alternatives, and debt management (moneysmart.gov.au)

These services are free. Consumers do not need to wait for a regulatory outcome to seek assistance with an existing loan that may not have been suitable for their financial circumstances.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

A $310,000-per-loan warning to every Australian credit licensee

The per-contravention penalty was calibrated to send a message beyond Money3, and Justice McElwaine’s reasoning made that explicit. General deterrence across all credit licensees was an active consideration in setting the quantum, not a secondary afterthought.

With ASIC’s motor vehicle finance sector review findings due by mid-2026, the period ahead represents one of heightened regulatory scrutiny for the entire non-bank car lending market. ASIC has confirmed that protecting financially vulnerable consumers and First Nations communities from predatory lending is an enforcement priority, and the Money3 case demonstrates it will pursue those priorities through Federal Court action.