CSL Has Lost 43%: What the Numbers Say at A$99.76

3 hrs ago

Ten-year Australian government bond yields have climbed to nearly 4.9%, the highest level of the 2025-26 period, arriving at almost the same moment as a Federal Budget that leaves the fundamental tax rules for share investing largely untouched but quietly reshapes the economics for anyone holding large equity portfolios inside superannuation. Published on 25 May 2026, this analysis connects the dots across three developments that matter simultaneously to Australian retail investors: what the Budget actually changed (and what it did not), what rising long yields mean for equity valuations and income competition, and how the ASX’s structural concentration in banks and miners amplifies every macro shift. The result is a clear, evidence-based picture of how these three forces interact, which investor cohorts face the most material changes, and what portfolio moves strategists are recommending in response.

The bond yield and budget developments outlined in the sections that follow do not land evenly across a diversified portfolio. They land disproportionately on a market that is unusually narrow.

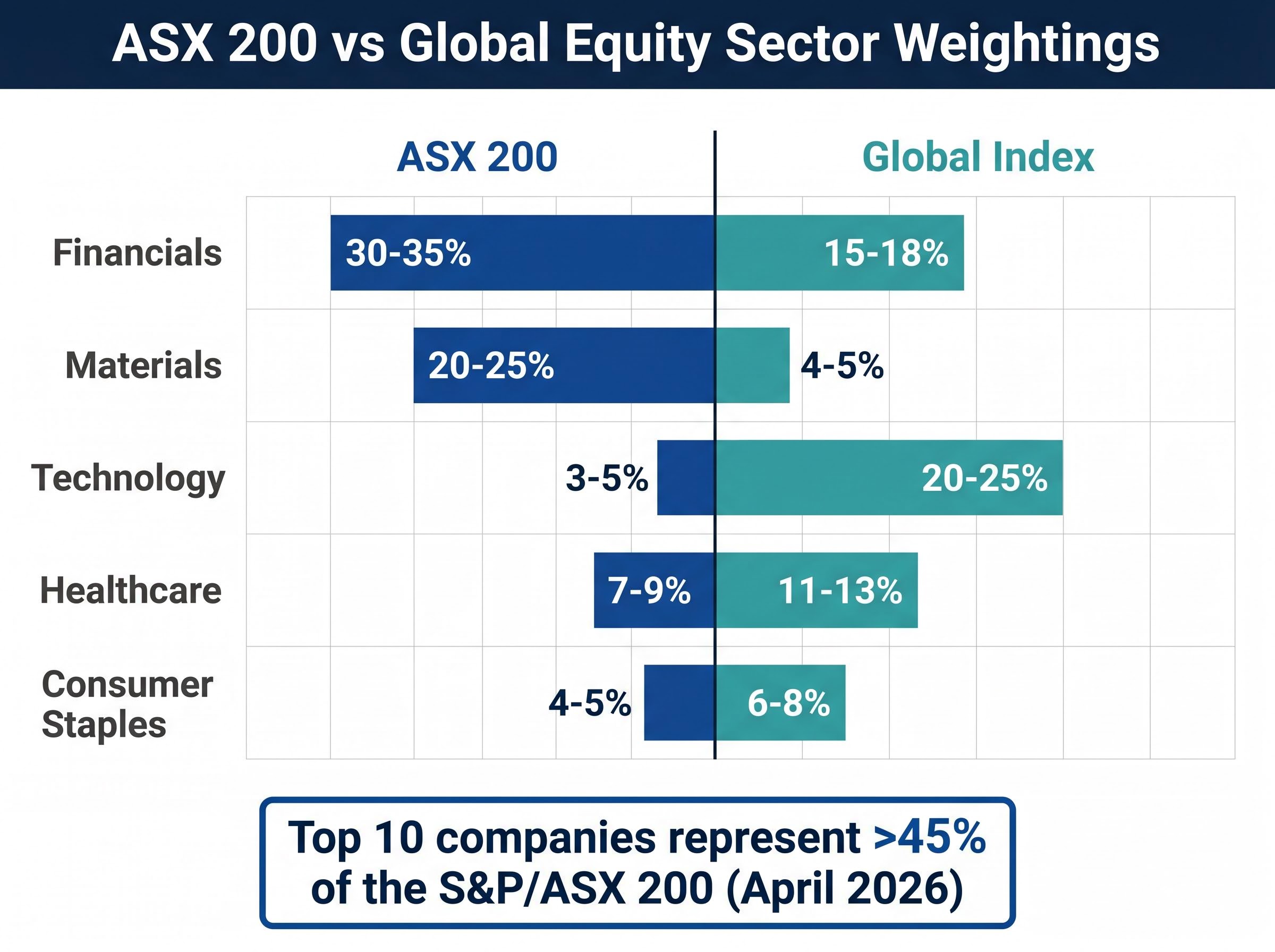

Financials (excluding REITs) and materials together account for an estimated 55-60% of the S&P/ASX 200 by market capitalisation, according to S&P Dow Jones Indices data from March 2026. The big four banks, BHP, Rio Tinto, and Fortescue dominate the upper end of the index.

The top 10 companies by market capitalisation represent more than 45% of the S&P/ASX 200, according to ASX statistical data from April 2026.

That concentration creates a specific vulnerability. When bond yields rise, banks face net interest margin pressure and equity valuation headwinds simultaneously. When commodity prices fall, the materials heavyweights drag the entire index.

ASX 200 concentration risk is more severe than its 200-stock label implies: VanEck research shows two stocks alone have historically represented approximately 22% of a typical cap-weighted Australian equity portfolio, meaning a single large-cap event can produce a 2% or greater drag on the entire index.

| Sector | ASX 200 (approx.) | Global equity index (approx.) |

|---|---|---|

| Financials | 30-35% | 15-18% |

| Materials | 20-25% | 4-5% |

| Healthcare | 7-9% | 11-13% |

| Technology | 3-5% | 20-25% |

| Consumer Staples | 4-5% | 6-8% |

The ASX 200 delivered an estimated 11% total return over the 12 months to March 2026. A concentrated index delivering strong recent returns can give investors a false sense of diversification. Understanding that this performance was substantially driven by a narrow band of banks and miners is the starting point for evaluating whether it is repeatable under a different macro regime.

The headline fear, a capital gains tax overhaul or an assault on franking credits, did not materialise. Budget Papers No.1 and No.2 (Treasury, 12 May 2026) contain no changes to CGT discount rates, and dividend imputation entitlements for individuals and self-managed super funds remain intact.

The change that did happen is targeted but consequential.

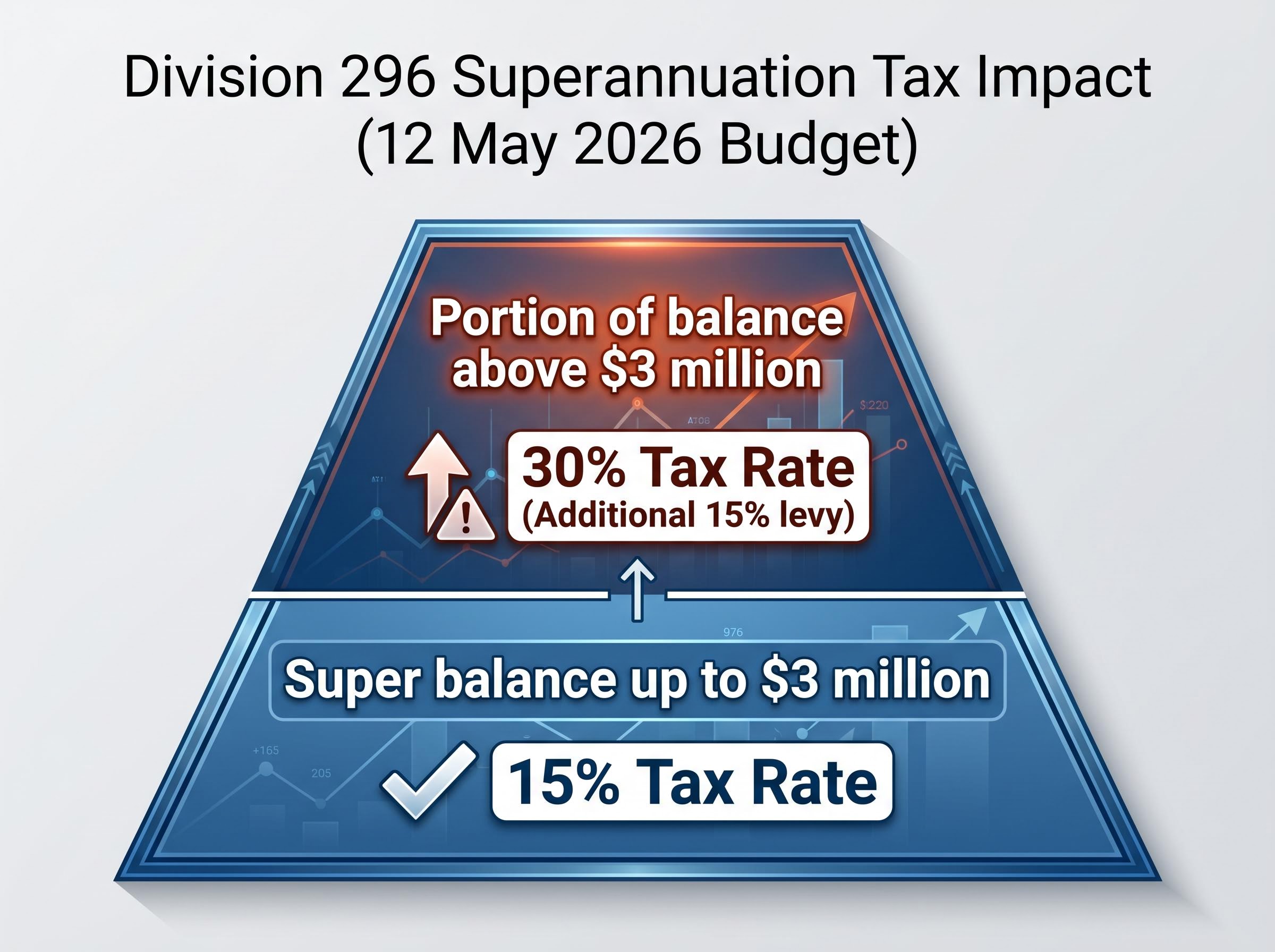

Division 296 effectively lifts the tax rate on earnings from 15% to 30% for the portion of a super balance above $3 million, including dividends and realised capital gains. Source: Treasury Laws Amendment (Better Targeted Superannuation Concessions) Act 2025, confirmed in Budget Paper No.1, 12 May 2026.

The ATO guidance on Division 296 confirms that individuals whose Total Super Balance exceeds the Large Super Balance Threshold of $3 million will face an additional 15% tax on relevant earnings from 1 July 2026, making the after-tax case for holding large equity portfolios inside super materially different from prior settings.

For the majority of retail investors with super balances below that threshold, the Budget preserves one of Australia’s most investor-friendly tax structures. Fully franked dividends remain intact, and the CGT discount is unchanged. The Division 296 measure is targeted, but for high-balance investors who hold significant ASX equity exposure inside super, the after-tax arithmetic has shifted materially.

The 10-year Australian government bond yield has risen from approximately 3.9% in January 2026 to near 4.9% in late May 2026. That 100-basis-point move reprices the competitive dynamics between equities and fixed income across two distinct channels.

The move in Australian 10-year yields does not reflect a domestic story alone; the synchronised global yield repricing of May 2026, which saw the US, UK, Japan, and Australia hit multi-decade highs simultaneously, signals a single coordinated reassessment of the risk-free rate across developed markets rather than four separate local events.

The first is the discount rate mechanism. Higher long-term yields raise the rate used to value future earnings streams, compressing the valuation multiples the market is willing to pay. This pressure falls hardest on long-duration growth stocks, those whose value depends heavily on earnings years into the future.

The second is the competing-asset argument. With the RBA cash rate at 4.35% (decision of 6 May 2026) and 10-year government bonds yielding near 4.9%, risk-free and low-risk income is meaningfully competitive with equity yields for the first time in the post-GFC era. Term deposits and government bonds now offer nominal returns that would have seemed generous just 18 months ago.

The RBA May 2026 cash rate decision lifted the benchmark to 4.35%, a level the Board characterised as restrictive, and the accompanying Statement on Monetary Policy outlined a soft-landing base case in which inflation eases gradually while unemployment remains near 4.2%.

Income-focused investors, retirees and SMSF members in particular, are now weighing term deposits and bonds against fully franked dividend yields in a way that has not been relevant since before the ultra-low-rate era.

Headline CPI came in at 4.6% year-on-year to March 2026 (ABS, released 29 April 2026). Against a bond yield of approximately 4.9%, the real return on government bonds is narrow, roughly 0.3% before tax.

That narrow real return gap complicates the picture. Nominal bond yields look attractive at first glance, but after adjusting for inflation, the income advantage over equities shrinks considerably. Dividend-paying equities, particularly those with a history of growing distributions above the rate of inflation, retain a structural case as an inflation-linked income source.

The after-tax value of franking credits remains fully intact under Budget 2026-27, which tilts the income comparison toward equities for investors who can utilise those credits. The current environment rewards deliberate allocation between bonds and equities, not a wholesale shift in either direction.

The macro picture from preceding sections translates into concrete sector-level consequences for the stocks that dominate the ASX 200. Three sensitivity channels are worth understanding:

Materials and financials were among the stronger sectors through 2025, according to S&P Dow Jones Indices data published in February 2026. Whether that leadership persists under a different yield regime is the question retail investors holding standard ASX 200 ETFs or heavy bank and miner weightings should be evaluating.

The sector-level damage from the May sell-off illustrates these dynamics in real time: gold miners fell 5-6% in a single session on 20 May 2026 as higher US real yields suppressed gold prices and raised energy input costs simultaneously, while Consumer Staples was the only ASX sector to advance, confirming the defensive rotation pattern that income-focused investors should understand.

The diagnosis is clear: concentration, rising yields, and targeted super tax changes create a case for rebalancing. The prescription needs to respect the reason Australian investors own domestic equities in the first place: the franking credit system remains one of the most favourable equity tax structures in the developed world.

Investors approaching or above the $3 million Division 296 threshold should review whether concentrating large equity holdings inside super remains optimal, given the effective 30% earnings tax on that tranche. Non-super structures, including family trusts and investment companies, may complement super holdings for some investors. This is an area requiring personal financial advice tailored to individual circumstances.

Investors exploring the practical contribution levers available before and after the threshold changes will find our dedicated guide to superannuation strategy for 2026, which covers the carry-forward rule mechanics, the expiry of unused FY2020-21 cap amounts on 30 June 2026, and the potential $340,000 long-term difference from switching investment options inside an existing fund.

These strategies are drawn from publicly available strategist commentary and should not be considered personal financial advice. Past performance does not guarantee future results.

The ASX 200 delivered an estimated 11% total return in the 12 months to March 2026, a period during which yields rose materially. High yields and positive equity returns are not mutually exclusive; the recent evidence reinforces that point directly.

The RBA’s May 2026 Statement on Monetary Policy characterises the broader economic outlook as consistent with a soft-landing scenario: GDP growth modestly below trend but not recessionary, unemployment at approximately 4.2%, and inflation elevated but forecast to ease.

The macro environment is not comfortable, but neither is it crisis-grade. The Budget preserved the fundamental equity tax advantages that make Australian shares distinctive in a global context. Bond yields are high, but real returns on bonds are narrow. ASX concentration is the most structurally persistent risk, and also the most actionable one.

Investors who distinguish between structural risks worth acting on (concentration, super tax settings above $3 million) and cyclical conditions worth monitoring but not over-reacting to (current yield levels, the inflation path) are better positioned to compound returns through this environment rather than be whipsawed by it.

The Budget’s limited but targeted changes, the yield environment’s dual implications for valuation and income competition, and ASX concentration as the most structurally persistent risk converge on a single portfolio question. It is not whether to own Australian equities; the franking advantage remains compelling for most retail investors. It is whether the current weighting toward banks and miners is still appropriate given the macro environment and budget settings.

The strategist consensus from JBWere, Morningstar, and BetaShares points toward a leaner domestic core with broader global and mid-cap exposure layered around it. Investors should review their sector exposure, consider their super balance relative to the Division 296 threshold, and assess whether their global equity allocation reflects genuine diversification or is an afterthought.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Division 296 is an additional 15% tax on superannuation earnings attributable to the portion of a total super balance above $3 million, effectively lifting the tax rate on that tranche from 15% to 30%. It applies to dividends and realised capital gains from 1 July 2026, making large equity portfolios held inside super materially more expensive to run for high-balance members.

No. Budget Papers No.1 and No.2 (Treasury, 12 May 2026) confirmed no changes to CGT discount rates for individuals or trusts, and franking credit entitlements for individuals and SMSFs remain fully intact, preserving one of Australia's most investor-friendly tax structures for the majority of retail investors.

Higher long-term yields raise the discount rate applied to future earnings streams, compressing the valuation multiples the market is willing to pay for equities, particularly long-duration growth stocks. Rising yields also make risk-free income from term deposits and government bonds more competitive with equity dividend yields for the first time since the pre-GFC era.

Financials and materials together account for an estimated 55-60% of the ASX 200 by market capitalisation, and the top 10 companies represent more than 45% of the index, meaning a single macro shock to banks or miners can produce outsized damage across a seemingly diversified Australian equity portfolio.

JBWere, Morningstar Australia, and BetaShares all recommend reducing over-reliance on banks and large miners by raising global equity allocations, adding quality mid-caps in healthcare and infrastructure, and blending sector and factor ETFs around a core ASX 200 holding to broaden exposure and support long-term total return.