S&P 500’s Earnings Shield Is Gone; Now the Macro Must Deliver

7 mins ago

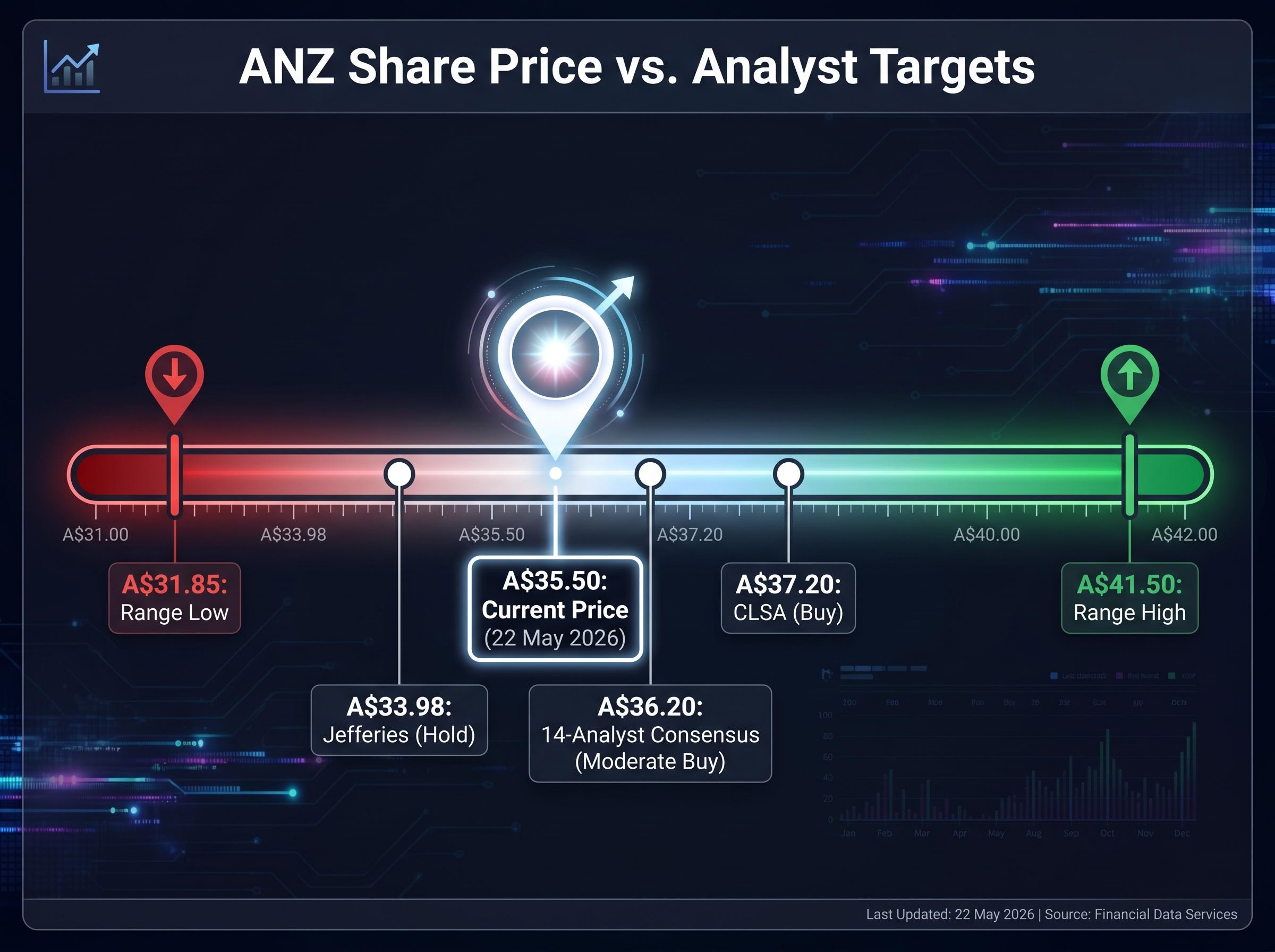

ANZ’s underlying cash profit jumped 14% in the first half of FY26, yet the bank grew its loan book by just 1%. The 1 May 2026 results revealed a bank shrinking its cost base rather than expanding its revenue engine. With operating expenses down 9% and total income essentially flat, the profit growth story rests on a foundation that cannot compound indefinitely. Against a share price sitting near A$35.50 as of 22 May 2026, the 14-analyst consensus target of A$36.20 implies the market has already priced most of the efficiency gain in. What follows unpacks the mechanics behind the profit jump, stress-tests the cost-cut narrative, examines where the ANZ share price sits relative to analyst targets, and delivers a grounded framework for retail investors assessing whether the stock warrants a position at current levels.

The arithmetic is straightforward, and that is precisely the point. Total operating income came in flat for the half. Operating expenses fell 9%. The result: profit before provisions rose 12% on an underlying basis, and underlying cash profit climbed 14%.

| Metric | H1 FY26 Movement |

|---|---|

| Total operating income | Flat |

| Operating expenses | Down 9% |

| Profit before provisions (underlying) | Up 12% |

| Underlying cash profit | Up 14% |

| Net loans and advances | Up 1% |

Every dollar of that double-digit profit growth came from the cost line. The revenue line contributed nothing. Net loans and advances rose just 1% over the six months from September 2025 to March 2026, offering no organic top-line tailwind.

The ANZ half-year results released on 1 May 2026 confirmed that non-interest operating income surged 28%, partially offsetting a 2% decline in net interest income and illustrating how the bank’s institutional and markets divisions are carrying revenue weight that retail lending is not.

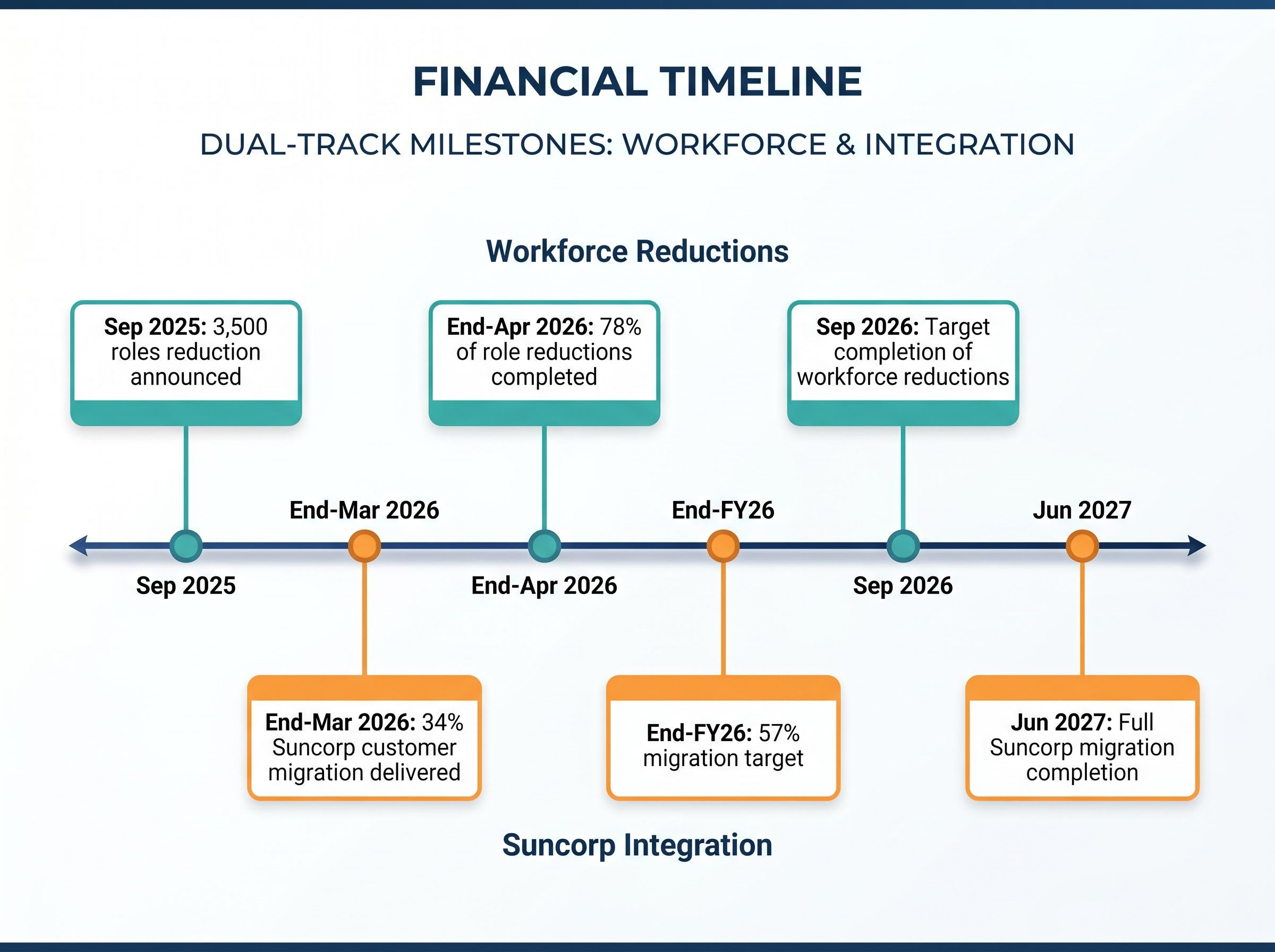

The cost reduction was programme-driven, not the product of gradual operational improvement. ANZ announced approximately 3,500 role reductions in September 2025, targeting completion by September 2026. By end-April 2026, approximately 78% of those reductions had reportedly been completed. The remaining 22% will continue to flow through the cost line into the second half, meaning the expense tailwind has not fully run its course.

A workforce reduction programme is a finite resource. Once the 3,500 roles are removed by September 2026, that lever cannot be pulled again at the same scale without launching a new restructuring cycle. The 9% fall in expenses delivered this half was the product of a specific programme with a specific end date.

Three structural constraints define the ceiling:

CEO Nuno Matos, speaking at the 1 May 2026 results release, confirmed that “reset actions are working” and reaffirmed the bank’s ANZ 2030 strategy.

That statement is accurate for now. The cost reset is delivering. The harder question is what happens once it is done. Investors extrapolating the 14% profit growth rate into future halves need to recognise that the next phase of the earnings story depends on lending volume, pricing, and revenue, areas where the first-half results offered little encouragement.

A bank earns money by borrowing cheaply and lending at a higher rate. For ANZ, the core revenue model rests on three pillars: net interest income on loans and deposits, fee income from transaction and institutional banking, and trading revenue from its markets division.

Loan book growth matters to revenue because the process works in sequence:

The core mechanics of net interest margin explain why loan book growth matters so directly to a bank’s revenue trajectory: each percentage point of volume expansion at a given margin multiplies through the interest income line in a way that fee income and trading revenue cannot replicate at scale.

When loan growth stalls at 1%, that compounding slows. The revenue engine idles rather than accelerates.

The Suncorp Bank acquisition is the strategic bet designed to address this. By end-March 2026, 34% of the customer migration programme had been delivered, with a target of 57% by end-FY26 and full migration completion by June 2027. Integration of this scale absorbs management attention and operational capacity, which partially explains the subdued lending growth in the near term. Whether the integration converts into meaningful market share gains by mid-2027 remains the central question for the revenue line.

At approximately A$35.50 as of 22 May 2026, the stock is sitting in a narrow corridor with limited consensus upside. Recent daily closes of A$35.63 on 20 May and A$35.39 on 21 May confirm the mid-A$35 range that has held since the early May trading band of A$34.45 to A$37.11.

The post-results 14-analyst consensus (mid-May 2026) carries an average 12-month target of A$36.20 with a Moderate Buy / Outperform rating, implying less than 2% upside from current levels.

| Analyst / Consensus | Rating | 12-Month Target | Implied Move from A$35.50 |

|---|---|---|---|

| 14-analyst consensus | Moderate Buy | A$36.20 | +2.0% |

| CLSA (14 May 2026) | Buy | A$37.20 | +4.8% |

| Jefferies (5 May 2026) | Hold | A$33.98 | -4.3% |

| Consensus range (low) | — | A$31.85 | -10.3% |

| Consensus range (high) | — | A$41.50 | +16.9% |

The spread between Jefferies at A$33.98 (implying downside) and CLSA at A$37.20 (implying modest upside) captures the uncertainty. At the consensus level, investors are not being offered a wide margin of safety. The stock is priced for the cost story that has already been delivered.

A 1% increase in net loans and advances over a six-month period, in a lending environment where mortgage and business credit are actively contested among the four majors, raises a question that the half-year results did not fully answer.

Three interpretations are possible:

No post-results peer comparison data on net interest margin or lending market share shifts was available in sourced material, which means investors cannot yet distinguish between these explanations with confidence. The 1% figure should be treated as a caution flag rather than a confirmed structural problem, but it warrants monitoring through to the full-year result.

Net interest margin underperformance was the defining earnings miss across the Big Four in May 2026 reporting season, driven by deposit competition and mortgage refinancing pressure compressing margins from both sides, and that context matters for interpreting whether ANZ’s 1% loan growth reflects deliberate margin discipline or competitive share loss.

The investment case sits in genuine tension. The cost programme is delivering, the Suncorp integration is tracking to schedule, and management has reaffirmed its strategic direction. Set against that, the consensus target implies minimal near-term upside, and loan growth remains the unresolved variable.

The catalyst that changes the thesis in either direction is identifiable: a material acceleration in lending volumes would validate the revenue line; a second-half revenue miss would confirm that cost-cutting was masking a deeper growth challenge.

How that maps to different investor profiles:

ANZ’s interim dividend of 83 cents per share, franked at 75%, carries a trailing yield of approximately 4.58%, the highest among Australia’s Big Four banks as of May 2026, and for income-oriented investors that yield floor may represent the most compelling part of the current investment case.

At A$35.50, consensus sits at A$36.20, upside requires loan growth to materialise, and downside risk centres on revenue deterioration once the cost lever expires.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The 14% underlying cash profit result is real and credible. ANZ’s management identified a cost problem, designed a programme to address it, and delivered. That discipline deserves recognition.

It also has a defined expiry date. By September 2026, the workforce reduction programme will be complete. The year-on-year cost benefit will begin to anniversary. From that point, the earnings trajectory depends almost entirely on whether ANZ can convert the Suncorp integration into lending market share and return the revenue line to growth.

The full-year FY26 result, expected later this year, is when investors will see whether that conversion is under way. Until then, the cost story has been told. The revenue story has not.

ANZ's 14% underlying cash profit growth was driven entirely by a 9% reduction in operating expenses, not revenue growth. Total operating income was flat for the half, meaning every dollar of profit improvement came from the cost line.

As of mid-May 2026, a 14-analyst consensus carries an average 12-month price target of A$36.20, implying less than 2% upside from the A$35.50 share price level. Individual targets range from A$31.85 at the low end to A$41.50 at the high end.

ANZ acquired Suncorp Bank and is migrating customers to its platform, with 34% of the migration completed by end-March 2026 and full completion targeted by June 2027. The integration is seen as the key medium-term catalyst for lending market share gains, though it is also consuming operational capacity that may be suppressing near-term loan growth.

Loan growth directly drives net interest income, which is ANZ's primary earnings engine. With net loans and advances growing only 1% in H1 FY26 and the cost-cutting programme set to expire by September 2026, future profit growth depends on whether the bank can accelerate lending volumes.

ANZ's interim dividend of 83 cents per share, franked at 75%, carries a trailing yield of approximately 4.58%, which is the highest among Australia's Big Four banks as of May 2026, making it a notable consideration for income-oriented investors.