10 Approved Rivals, Yet S&P Global’s Moat Keeps Compounding

54 mins ago

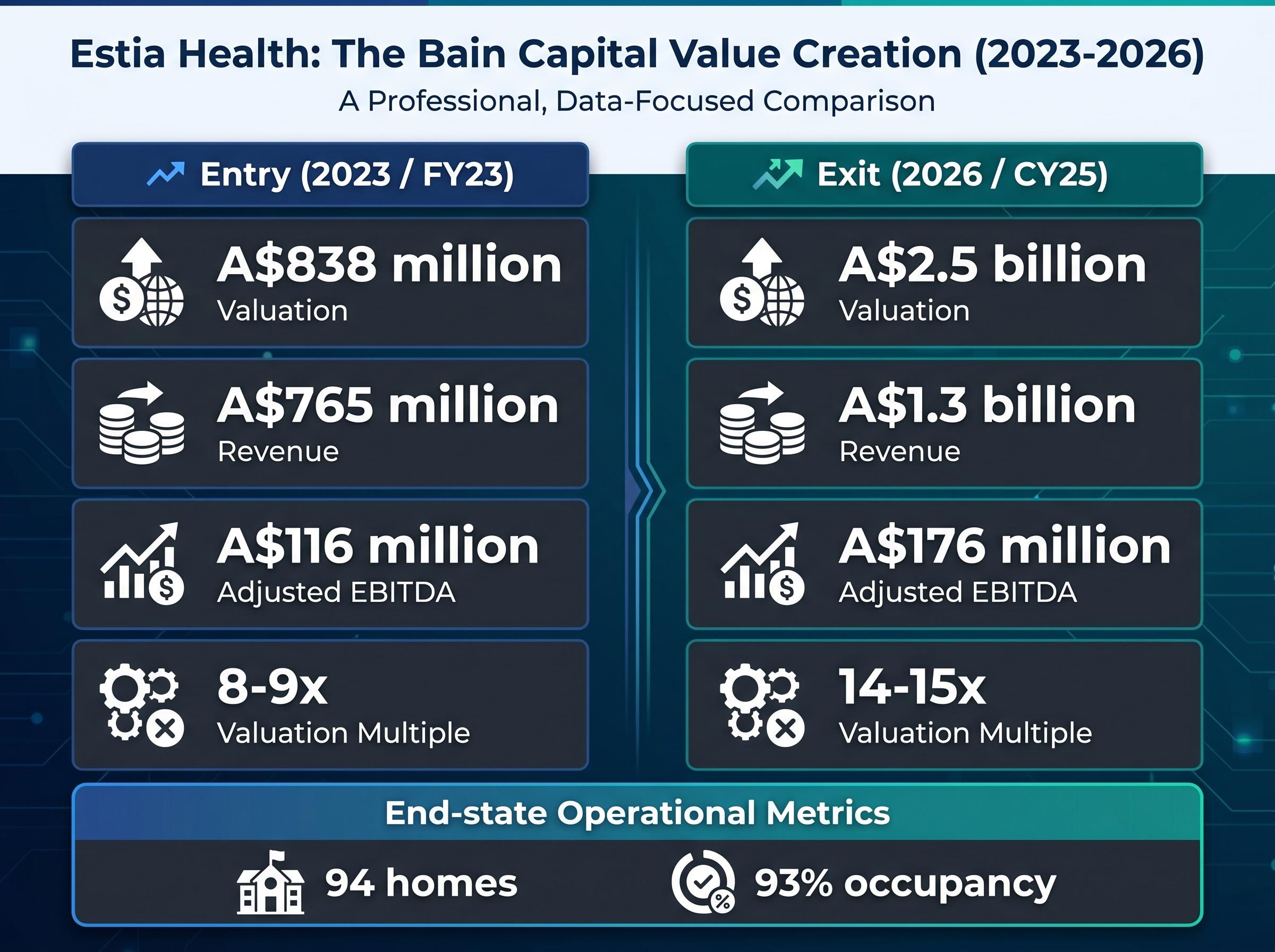

Bain Capital acquired Estia Health for A$838 million in 2023 and is selling it to Stonepeak for A$2.5 billion in 2026. That is roughly three times the entry price in under three years, a return that places the transaction among the most profitable private equity exits in Australian healthcare. The deal is more than a single fund’s windfall. It arrives at a moment when Australian aged care investment has been recast entirely: from a politically troubled, margin-compressed sector into one that global capital is prepared to pay infrastructure-grade multiples to own. What follows is an analysis of how Bain created that return, what it reveals about the capital dynamics reshaping the sector, and what competitive consequences flow from Stonepeak’s entry as a long-hold infrastructure owner.

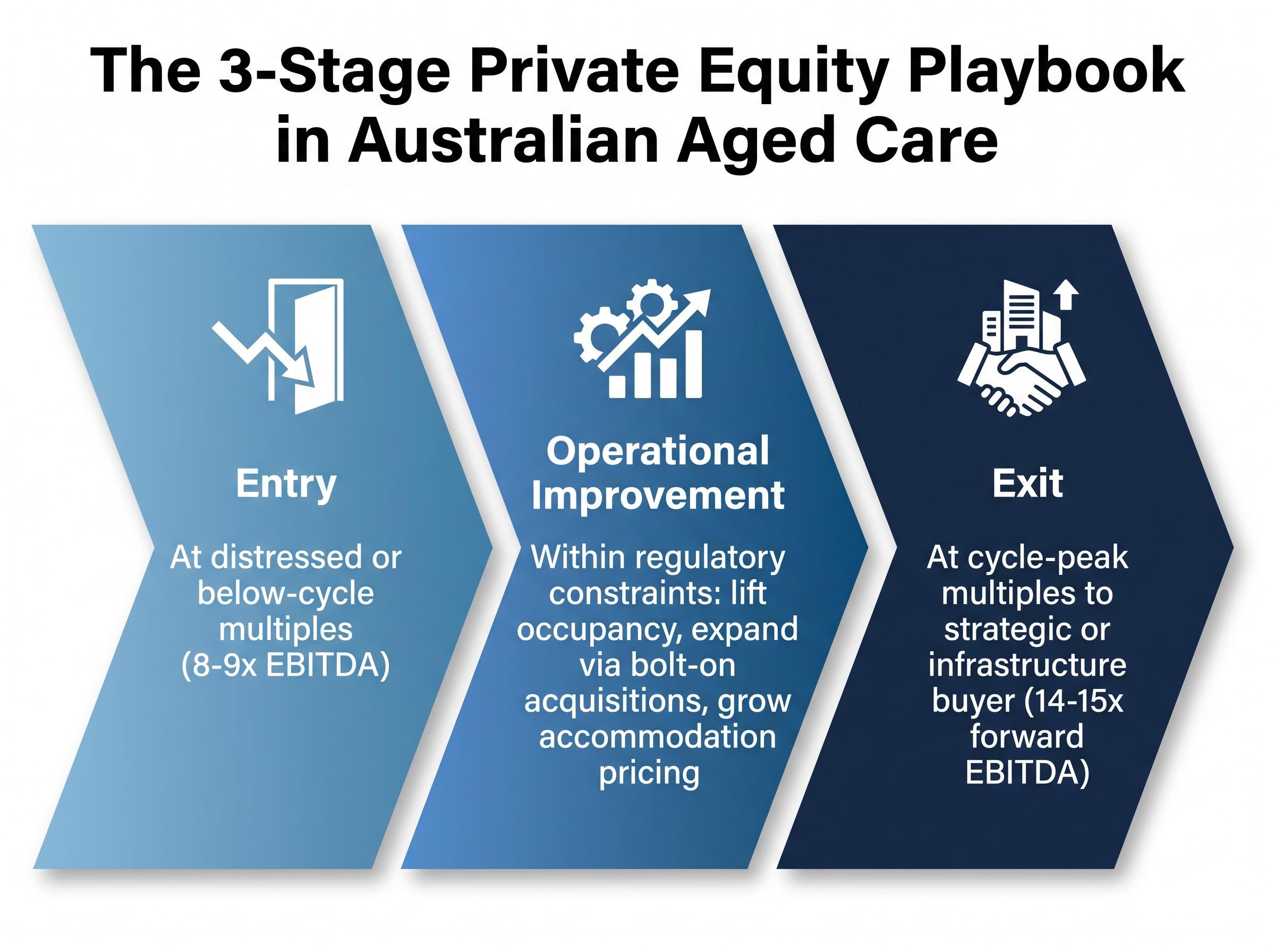

Bain’s 2023 take-private of Estia came during the post-royal-commission overhang, when listed aged care valuations were depressed and sector sentiment was cautious. The entry multiple was approximately 8-9x EBITDA, according to Australian Financial Review estimates, reflecting a market that had largely written off aged care as investable.

The value creation that followed was deliberate and sequential. Bain completed seven bolt-on acquisitions, expanding Estia’s footprint to 94 homes and 9,250 resident places. Occupancy lifted to 93%, comfortably above a sector average of approximately 89%. Accommodation pricing growth averaged 12% from January 2025, a lever that required both physical asset improvement and demand management to pull effectively.

Bain Capital commentary: Bain “executed a buy-and-build strategy, completing seven bolt-on acquisitions and expanding Estia’s footprint to 94 homes.”

The financial results compound the operational story. Revenue grew from A$765 million in FY23 to A$1.3 billion in CY25. Adjusted EBITDA rose from A$116 million to A$176 million over the same period. That EBITDA base, paired with a market willing to pay approximately 14-15x forward EBITDA, supported the A$2.5 billion exit.

| Metric | Entry (FY23) | Exit (CY25) |

|---|---|---|

| Revenue | A$765 million | A$1.3 billion |

| Adjusted EBITDA | A$116 million | A$176 million |

| Occupancy rate | Below sector average | 93% |

| Number of homes | Pre-acquisition base | 94 |

The magnitude of the return is notable, but it is explainable. EBITDA grew roughly 52%, and the exit multiple expanded from 8-9x to 14-15x. Both levers worked in parallel.

The 14-15x multiple Stonepeak paid is not an outlier. It sits at the top end of a range that has shifted structurally since 2020. Understanding why requires a reframing of what aged care represents as an asset class.

Four characteristics now place it in the same category as toll roads, data centres, and regulated utilities:

UBS sector analysis tracks the re-rating in private transaction multiples from 7-9x during the 2020-2021 royal commission overhang to 11-14x in the post-reform period. Jarden equity research notes that recent private deals have been struck at 12-15x forward EBITDA for high-occupancy portfolios with strong accommodation income.

The AN-ACC (Australian National Aged Care Classification) funding model and new care minute requirements raised short-term compliance and wage costs. For under-capitalised operators, this pressure proved terminal. For scaled operators with capital access, it created the opposite effect: greater funding predictability and a wave of acquisition targets as smaller providers exited.

The Aged Care Financing Authority (ACFA) noted in its FY23-24 report that “greater policy clarity and funding stability is contributing to renewed private investment interest.” The reform cycle concentrated market share among larger platforms and improved competitive dynamics for those that remained.

The Financial Report on the Australian Aged Care Sector 2023-24, published by the Department of Health, Disability and Ageing, documents how post-reform funding flows and capital investment patterns shifted following AN-ACC implementation, providing the clearest official baseline for measuring the sector’s financial recovery from the royal commission period.

Bain ran a dual-track exit, exploring both an ASX relisting and a trade sale. Regis Healthcare (ASX: REG) and PEP-backed Opal HealthCare both participated in earlier stages. Neither made the final cut. The reasons are analytically instructive.

Regis, which operates 64 facilities with 7,215 operational places, explored a largely scrip-funded merger that would have created a larger listed operator. According to Australian Financial Review reporting, Regis “could not match Stonepeak on price while preserving its balance sheet.” The Regis CEO has subsequently described the company as “an active participant in sector consolidation” while remaining “disciplined on capital allocation.”

Regis occupancy metrics tell a story of competitive operational strength: mature home occupancy reached 95.9% in Q3 FY26, above Estia’s 93%, with underlying EBITDA of approximately $135 million tracking at the top end of FY26 guidance and net RAD inflows of $223 million year-to-date providing balance sheet headroom for future bolt-on activity.

Opal, with approximately 90 homes and more than 9,000 beds, reportedly examined both acquisition and merger-of-equals structures before concerns about regulatory concentration and the final valuation expectations led it to withdraw. The Australian reports Opal is now pivoting to bolt-on acquisitions of sub-scale operators and regional not-for-profit conversions.

| Operator | Homes | Resident places | Ownership | Post-deal posture |

|---|---|---|---|---|

| Estia Health | 94 | 9,250 | Stonepeak (infrastructure fund) | Brownfield expansion, bolt-on acquisitions |

| Regis Healthcare | 64 | 7,215 | ASX-listed | Disciplined bolt-on growth |

| Opal HealthCare | ~90 | 9,000+ | PEP (private equity) | Sub-scale acquisitions, potential future IPO |

The failed bids reveal something specific. Stonepeak’s all-cash infrastructure fund structure, with a longer hold horizon and lower return hurdles, gave it an execution advantage that neither a listed acquirer nor a PE-backed competitor could match. A well-capitalised, long-hold owner committed to further consolidation changes the competitive calculus for every operator in markets where Estia competes.

The Estia transaction illustrates a three-stage value creation model that is becoming the standard PE playbook in Australian aged care:

The Aged & Community Care Providers Association (ACCPA) has observed that post-royal-commission compliance and wage costs triggered exits by smaller providers, creating acquisition opportunities for scaled investors. PE and infrastructure capital is accelerating consolidation among sub-scale providers.

What distinguishes this playbook from traditional PE operational turnarounds is the regulatory envelope. Bain’s bolt-on and occupancy strategy had to deliver returns within tighter operational boundaries than a typical services business. Jarden characterises recent deals as reflecting infrastructure and real-asset funds viewing aged care as “social infrastructure with quasi-regulated returns,” a framing that only works when the operator can demonstrate care quality alongside financial performance.

Bain’s outcome is not isolated: MA Financial’s aged care fund exits have delivered comparable conviction, with its Infinite Care sale to Anglicare Sydney generating approximately $20 million in realised gains and a 2.8x return for fund investors, reinforcing that the PE value creation thesis in Australian aged care extends well beyond a single transaction.

The same regulatory environment that created Bain’s opportunity could shift against Stonepeak. Paying 14-15x forward EBITDA requires specific conditions to hold, and several remain genuinely uncertain.

The categories of regulatory risk are identifiable:

ACCPA has stated explicitly that “stable, predictable funding and accommodation pricing settings are prerequisites for sustaining investor appetite.” A Sydney Morning Herald summary of infrastructure conference commentary noted that investors remain sensitive to future changes across all four of these dimensions.

ASX healthcare structural risks are not uniform across sub-sectors: while listed pharma and biotech face FDA staffing losses and regulatory politicisation in the US, residential aged care’s government-underwritten domestic revenue model insulates it from most of the forces that have pushed the S&P/ASX 200 Health Care Index to a six-year low.

Post-royal-commission reforms are now largely implemented. The political appetite for further structural disruption to a sector receiving significant global capital inflows may be limited. Stonepeak’s framing of aged care as sitting “at the intersection of healthcare and infrastructure” reflects a view that the asset class has crossed into regulated-returns territory.

Sector analysts also note that recent transactions, including Estia, occur in portfolios with above-average quality ratings and above-average occupancy, suggesting that the capital flowing in is selecting for operational quality rather than acquiring indiscriminately.

Australian aged care sits partway through a consolidation arc with no clear endpoint. Large PE-backed and infrastructure-backed platforms, Estia under Stonepeak and Opal under PEP, are absorbing sub-scale operators. Listed operators like Regis pursue disciplined bolt-on growth. No single ownership model has yet proved dominant.

The next likely catalysts are identifiable:

Stonepeak’s broader ambition: The Australian reports that Stonepeak sees “room for a multi-asset social infrastructure platform” in Australia spanning aged care, disability accommodation (SDA), and healthcare-adjacent property, with Estia as a cornerstone holding.

Jarden describes a “consolidation wave building” in Australian aged care, while UBS notes growing participation by global infrastructure funds and PE across residential aged care, home care, and retirement living. The Estia transaction, struck at 14-15x EBITDA for a high-occupancy portfolio, sets a valuation benchmark that will shape how all future sector M&A is priced.

The consolidation trend is clear. The capital conviction is real. The endgame ownership structure of Australian aged care remains genuinely open.

Investors exploring the technology layer shaping future operator economics will find our deep-dive into AI-driven care platforms in aged care, which examines how deployments like InteliCare’s $8.8 million agreement with mecwacare are delivering measurable outcomes including 100% fall detection accuracy and significantly reduced overnight welfare checks across residential facilities.

The Bain-to-Stonepeak transaction is simultaneously a case study in disciplined PE value creation, a signal of structural repricing in the aged care asset class, and the opening move in a longer consolidation story. At its centre sits a tension the article has tracked throughout: aged care’s appeal to institutional capital rests on regulatory stability that is politically contingent, and the sector’s transformation into infrastructure is still being negotiated between capital, government, and community expectations.

Whether Stonepeak’s infrastructure framing of Estia, with its emphasis on essential services, inflation-linked revenues, and barriers to entry, ultimately proves to be prescient or premature depends on decisions that will be made in Canberra as much as in boardrooms.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Infrastructure-grade pricing means investors value aged care assets similarly to toll roads or regulated utilities, applying multiples of 12-15x forward EBITDA based on needs-driven demand, government-underwritten revenue, and constrained new supply rather than discretionary consumer spending.

Bain acquired Estia at approximately 8-9x EBITDA during the post-royal-commission downturn, then grew revenue from A$765 million to A$1.3 billion through seven bolt-on acquisitions, lifted occupancy to 93%, and exited at 14-15x EBITDA as sector sentiment and multiples re-rated upward.

AN-ACC (Australian National Aged Care Classification) is the Commonwealth funding model that provides government subsidies to residential aged care operators, creating a quasi-regulated income stream that underpins revenue predictability and has contributed to renewed private investment interest since its implementation.

Regis explored a largely scrip-funded merger but could not match Stonepeak on price while preserving its balance sheet; Stonepeak's all-cash infrastructure fund structure, with a longer hold horizon and lower return hurdles, gave it a decisive execution advantage over listed and PE-backed bidders.

Key risks include potential means-testing reform reducing accommodation revenue, government-imposed accommodation pricing caps, further increases to mandated care minute staffing requirements, and the pending ACCC and FIRB regulatory approvals required to complete the Stonepeak transaction by Q4 CY2026.