US Strikes 60 Iran Targets as Brent Crude Breaks $80

9 hrs ago

U.S. regulators have cleared roughly 10 Chinese companies to purchase Nvidia’s H200 artificial intelligence chips. Beijing has not. The result is a commercial standoff in which both permissions are required and only one has been granted, leaving one of the world’s most valuable technology companies locked out of a market that contributed approximately 17% of its total revenue as recently as fiscal year 2024. The deadlock emerged after a January 2026 Bureau of Industry and Security (BIS) rule shifted H200 exports to China from a presumption of denial to case-by-case review. Despite that partial liberalisation, no H200 units have reached China as of late May 2026. A U.S.-China leadership summit in Beijing this month, attended by Nvidia CEO Jensen Huang, produced no semiconductor-specific resolution.

What follows is an explanation of how the two-sided approval structure works, what the stalemate costs Nvidia in near-term revenue, why Beijing is in no hurry to grant its side of the permission, and which signals would indicate the deadlock is breaking.

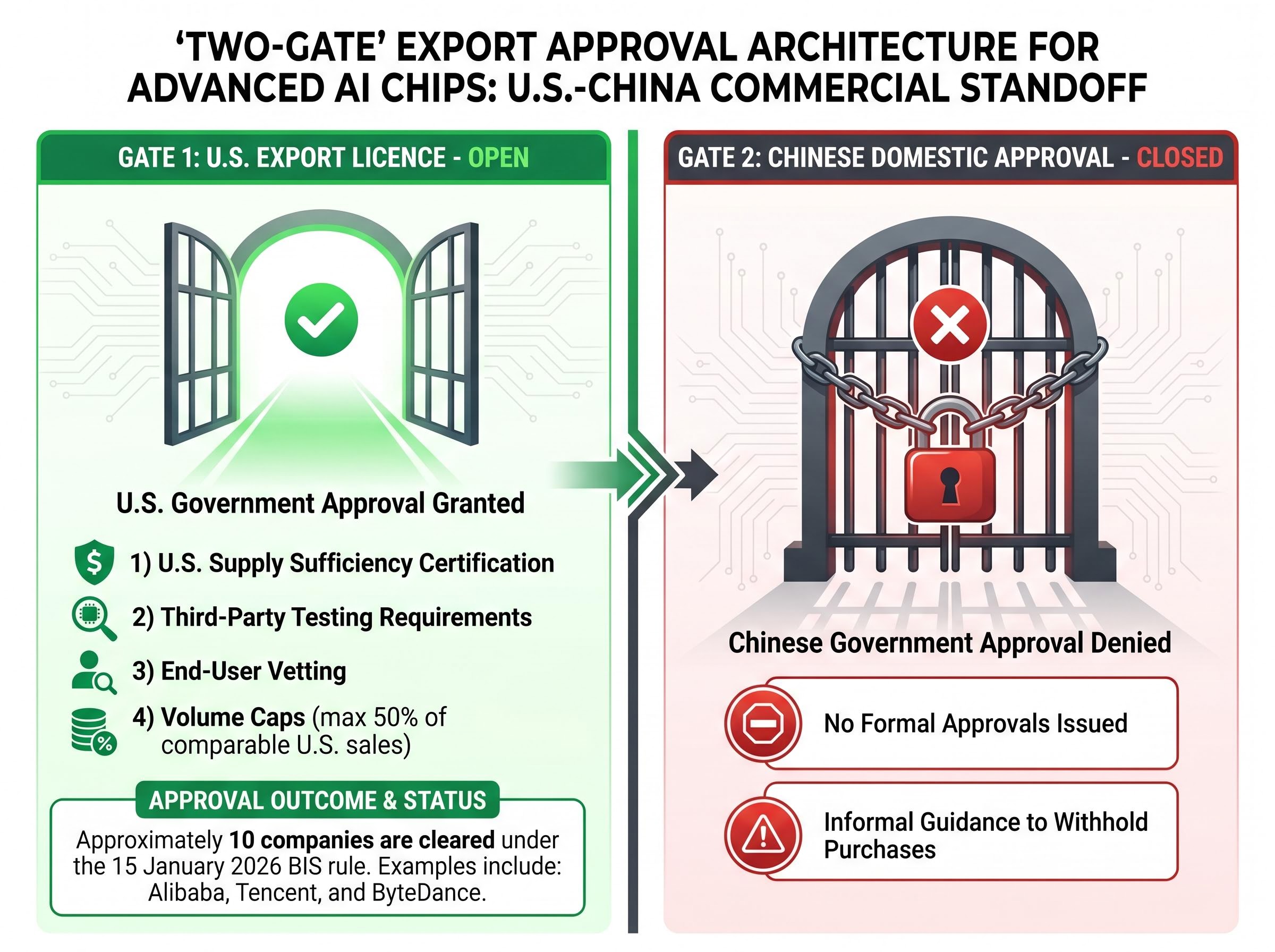

Exporting advanced AI chips to China requires valid authorisation on both sides of the Pacific: a U.S. export licence (or equivalent clearance) and a Chinese domestic import or purchase approval. The H200 stalemate exists because only the first gate has opened.

On 15 January 2026, a BIS final rule took effect that moved the H200 and equivalent processors (including AMD’s MI325X) from a presumption of denial to case-by-case licensing review. Approvals under that framework carry four conditions:

Under this framework, approximately 10 named Chinese firms, including Alibaba, Tencent, and ByteDance, received U.S. clearance. Yet Chinese regulators have not issued formal approvals, and guidance from Beijing caused those firms to pull back from completing purchases.

Approximately 10 Chinese companies have U.S. clearance to purchase H200 chips, yet no units have been delivered as of late May 2026.

The distinction matters for anyone reading licence-grant headlines as revenue signals. A U.S. export licence is a necessary condition for the sale; it is not a sufficient one. The Chinese regulatory gate operates independently, and it remains closed.

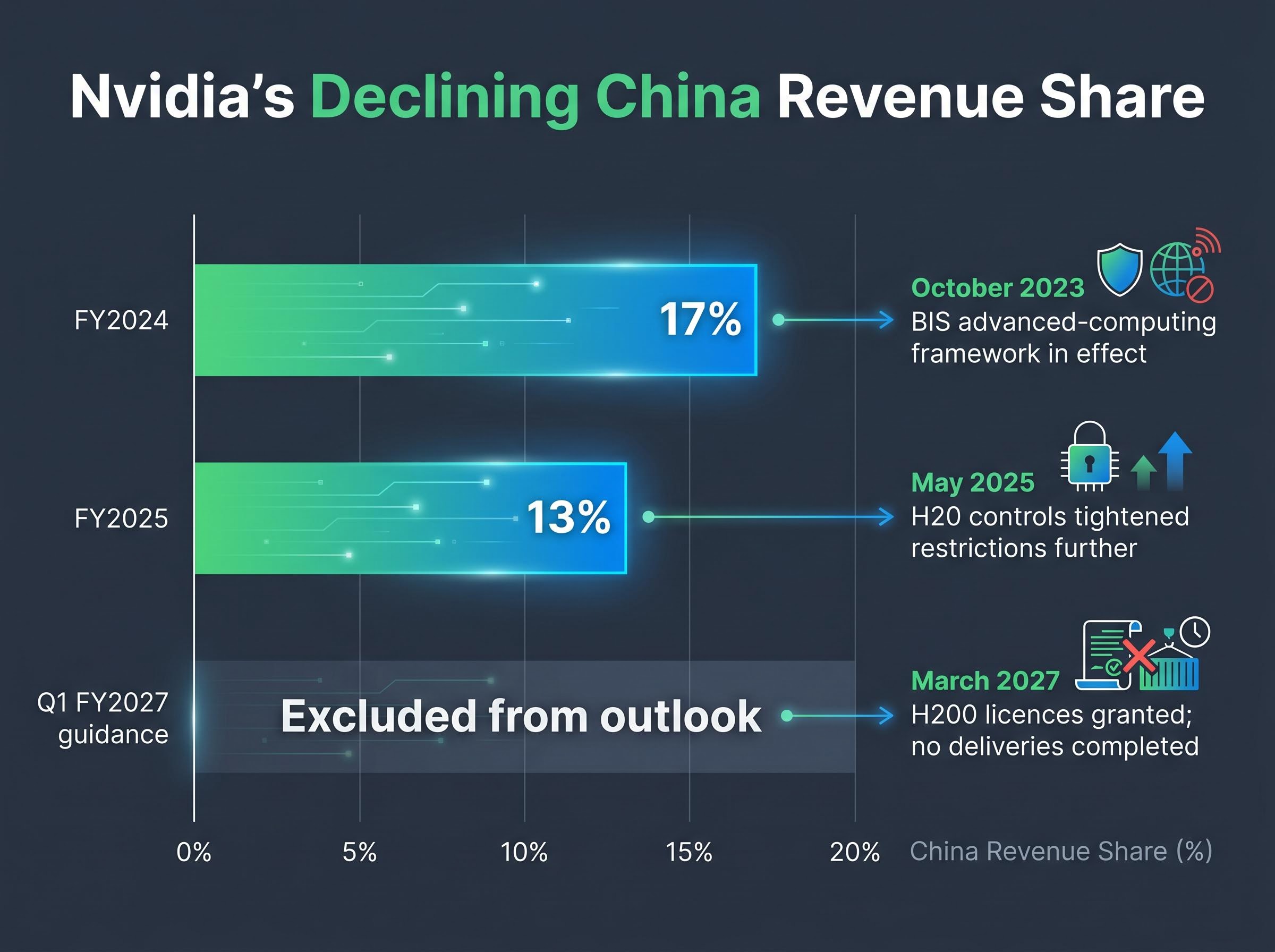

The most direct financial signal of the stalemate’s impact comes from Nvidia itself. The company’s Q1 FY2027 guidance explicitly excludes Data Centre compute revenue from China, confirming that management is not counting on near-term resolution.

China’s share of Nvidia revenue has been declining under successive rounds of export controls. The trajectory is visible across recent fiscal years.

| Period | China revenue share | Policy context |

|---|---|---|

| FY2024 | Approximately 17% | October 2023 BIS advanced-computing framework in effect |

| FY2025 | Approximately 13% | May 2025 H20 controls tightened restrictions further |

| Q1 FY2027 guidance | Excluded from outlook | H200 licences granted; no deliveries completed |

The gap between confirmed company disclosure and third-party projections is wide. Nvidia’s Q1 FY2027 guidance reflects zero China Data Centre compute revenue.

Analyst estimates, by contrast, suggest that if H200 licences translate into actual shipments, China could contribute an additional $15-26 billion in annual revenue. These figures represent upside potential contingent on full licence utilisation, not a baseline expectation, and should be treated as unverified analyst commentary rather than company guidance.

The H200 deadlock is not an anomaly. It is a predictable feature of the regulatory architecture governing advanced semiconductor exports between the United States and China.

The foundational framework was established in October 2023, when BIS expanded export controls on advanced AI chips sold to China. That rule captured Nvidia’s A100 and H100 processors and restricted the China-specific A800 and H800 variants. Every subsequent policy change has operated within this architecture, either tightening or loosening specific provisions without replacing the underlying structure.

The chronological sequence illustrates how the framework has moved in both directions:

The January 2026 rule is a modification, not a replacement. The Entity List continues to operate as an independent constraint layer, restricting sales to specific buyers regardless of product-level licensing changes.

The BIS final rule on advanced computing exports, published at 91 Fed. Reg. 1684 and effective 15 January 2026, established the case-by-case licensing framework under which the four conditions applied to H200 shipments, including volume caps and third-party testing requirements, now govern any approved transaction.

Beijing can effectively block U.S.-approved sales without issuing a formal denial, simply by providing informal guidance to domestic buyers to withhold purchases.

Chinese domestic approval requirements exist independently of U.S. export controls. This means investors evaluating future policy announcements should treat any single-side approval as half of the equation, not the whole of it.

U.S. AI chip export controls derive their structural durability from bipartisan Congressional backing and national-security legal authority that sits outside the jurisdiction of trade negotiators, meaning no diplomatic summit outcome can unilaterally lift the U.S. side of the dual-approval requirement without separate legislative or regulatory action.

The regulatory delay is not passive. Beijing has used the period of restricted Nvidia access to accelerate adoption of domestic alternatives, turning the H200 stalemate into an industrial policy instrument.

Huawei’s Ascend 910 series (910B, 910C, and the planned 910D) sits at the centre of this effort. Chinese cloud providers and government-backed projects have been actively directed toward Huawei hardware over foreign alternatives. Bloomberg reported in September 2025 that Huawei planned to double output of its top AI chip as Nvidia’s China position wavered. Production targets for the Ascend 910C reportedly reach approximately 600,000 dies for 2026, though this figure remains unverified.

The broader domestic chip ecosystem extends beyond Huawei:

The Trump-Xi summit in Beijing this month produced no communiqué and no semiconductor-specific concession. Jensen Huang attended as a member of the U.S. delegation but made no public announcement of a breakthrough on H200 approvals.

Speaking at Taipei airport on 23 May 2026, Huang stated that he expects the Chinese market to open “over time” but confirmed no direct H200 chip discussions occurred during the meetings. China continued to emphasise domestic alternatives in parallel with the diplomatic engagement, consistent with the broader pattern in which summit-level talks have not translated into regulatory resolution on either side.

For investors who want to separate verified commitments from unverified claims across all sectors touched by the summit, our full explainer on what the Beijing summit actually confirmed walks through each sectoral outcome, identifies which official statements came from Chinese authorities versus U.S. claims without Beijing corroboration, and details why chip controls and Taiwan were structurally outside the scope of what trade negotiators could resolve.

Rather than speculating on timing, investors can monitor a concrete hierarchy of indicators that would signal a genuine shift in the H200 deadlock.

Jensen Huang, speaking on 23 May 2026, stated that he expects the Chinese market to open “over time,” framing eventual access as a long-range expectation rather than a near-term catalyst.

Nvidia’s own strategic planning reflects continued conviction that China matters. The company’s $200 billion addressable CPU market projection for its Vera platform, outlined during the 21 May 2026 earnings call, explicitly includes China. A prior $1 trillion cumulative revenue projection from the flagship AI chip lineup similarly accounts for eventual Chinese market access.

Hyperscaler capex commitments of $600-725 billion across 2026, already board-approved by Amazon, Meta, Microsoft, and Alphabet, provide the demand foundation that keeps Nvidia’s revenue trajectory intact even as China remains excluded from Q1 FY2027 guidance, underscoring why analysts maintain approximately 80-86% market share estimates for Nvidia’s AI accelerator position outside China.

The next Nvidia earnings call represents the nearest formal checkpoint at which management could update China guidance. Until then, the three-tier signal hierarchy above offers the clearest framework for tracking progress.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements, including analyst revenue projections and management expectations regarding China market access, are speculative and subject to change based on regulatory developments, diplomatic outcomes, and market conditions.

The H200 stalemate reduces to a structural fact: U.S. export authorisation is a necessary but not sufficient condition for Nvidia to complete sales in China. Both gates must open before revenue materialises. As of late May 2026, the January 2026 BIS rule change has produced zero incremental China revenue for Nvidia in the Data Centre segment.

Beijing’s simultaneous acceleration of domestic chip suppliers means any eventual resolution will arrive into a more competitive Chinese AI hardware market than existed when the stalemate began. Huawei’s Ascend production ramp, the directed adoption of domestic alternatives by Chinese cloud providers, and the absence of any semiconductor-specific diplomatic outcome all point in the same direction.

Institutional investors at BlackRock, Goldman Sachs, and Vanguard have formalised this framing by treating China upside as a call option on geopolitical resolution rather than a base-case revenue driver, with analyst consensus price targets built entirely on U.S. and allied market demand and China contributing zero to the base model.

For investors, the framework is durable beyond this single story. In an era of dual-sided technology regulation, no single approval from either government constitutes a commercial green light. Both gates matter. Only one is open.

Exporting H200 chips to China requires approval from both U.S. and Chinese regulators. While roughly 10 Chinese companies received U.S. clearance under the January 2026 BIS rule, Beijing has not issued its own formal approval and has informally guided domestic buyers to withhold purchases, leaving the second regulatory gate closed.

The dual-approval architecture means that a U.S. export licence and a Chinese domestic import or purchase approval are both required before a sale can be completed. Either government can effectively block a transaction, meaning U.S. clearance alone is a necessary but not sufficient condition for Nvidia to recognise revenue from Chinese buyers.

Analyst estimates suggest China could contribute an additional $15-26 billion in annual revenue if H200 licences are fully utilised, though this represents unverified upside potential and not a figure reflected in Nvidia's own guidance, which excludes China Data Centre compute revenue from its Q1 FY2027 outlook.

The three key indicators are: a formal Chinese regulatory approval of H200 imports, confirmed delivery of H200 units to any of the 10 licensed buyers, and an update from Nvidia management reversing the exclusion of China Data Centre compute revenue from its financial guidance.

Beijing has used the period of restricted Nvidia access to accelerate adoption of domestic alternatives, directing Chinese cloud providers and government-backed projects toward Huawei's Ascend 910 series, with production targets for the Ascend 910C reportedly reaching approximately 600,000 dies for 2026.