Brent Falls 3.3% as Trump Signals Imminent Iran Peace Deal

11 hrs ago

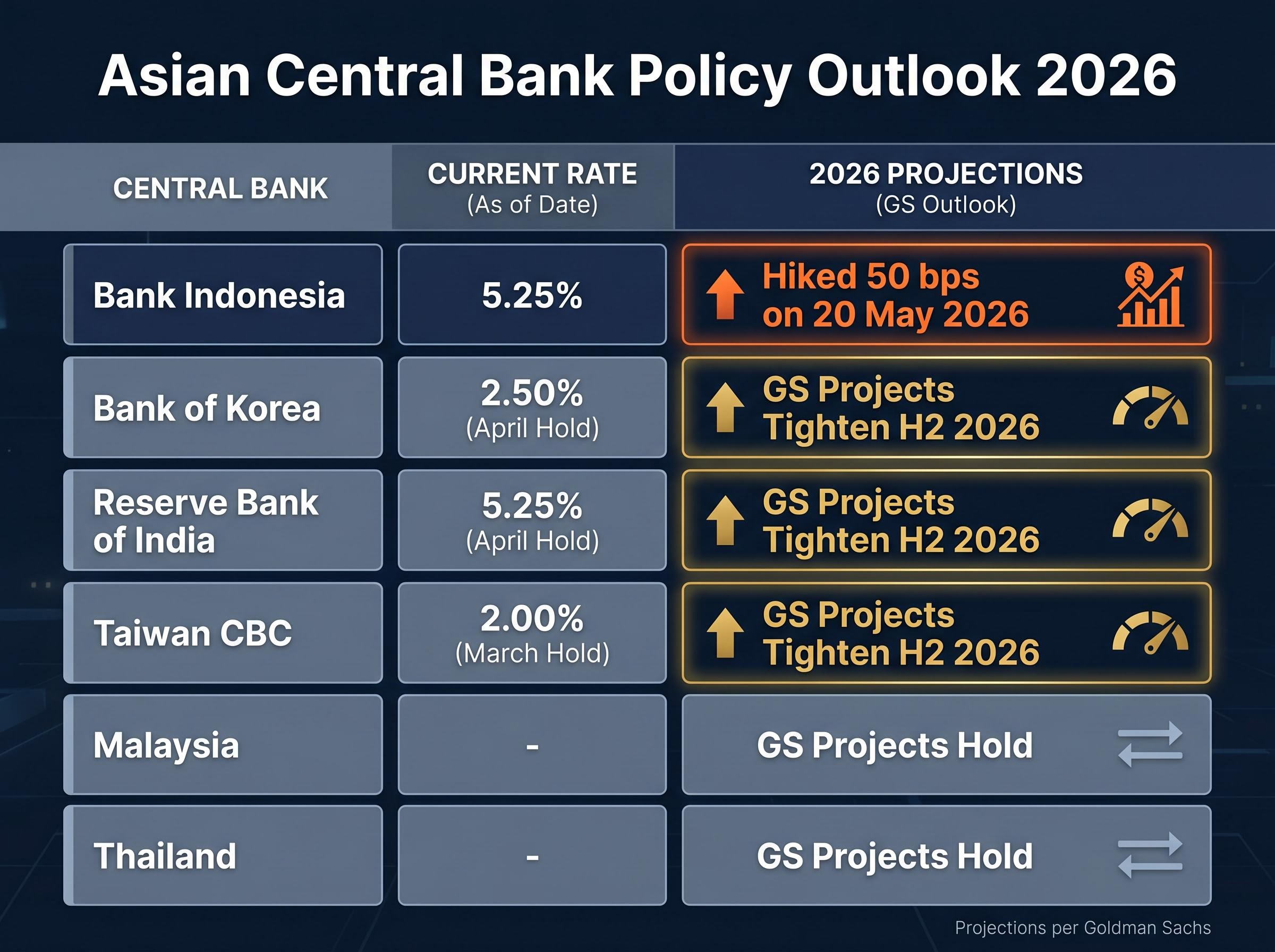

Bank Indonesia shocked markets this week with a 50-basis-point rate hike, the largest single move from any major Asian central bank in years. Jakarta may only be the first domino.

With the U.S. dollar gaining structural support from the AI-driven domestic boom and Strait of Hormuz disruptions inflating energy import bills across the region, Asian central banks face a narrowing set of options. Goldman Sachs now projects the Bank of Korea, the Reserve Bank of India (RBI), and Taiwan’s Central Bank to join a regional tightening cycle later in 2026. The combination of persistent dollar strength, rising crude logistics costs, and fragile domestic growth has created a policy environment where rate hikes are necessary but may not be sufficient.

What follows is a breakdown of what Bank Indonesia’s decision signals, which central banks are next, why the conventional rate-hike playbook is being tested by a dollar-oil combination, and what the implications are for investors with emerging market exposure.

Markets expected a hold, or at most a 25-basis-point move. Bank Indonesia (BI) delivered 50 basis points, raising the BI-Rate to 5.25% at its 20 May 2026 Board of Governors meeting. The gap between consensus and outcome was the clearest signal Jakarta could send: currency defence has overtaken growth as the dominant policy priority.

BI framed the decision as “pro-stability,” positioning the hike not as a response to inflation already running hot, but as a pre-emptive move to anchor expectations before they could deteriorate further.

Bank Indonesia’s May 2026 rate decision confirms the Board of Governors cited Rupiah exchange rate stabilisation and Middle East conflict spillovers as the primary justifications for the move, giving the hike an explicitly external rather than domestic inflation mandate.

Bank Indonesia stated the hike aimed to “strengthen rupiah stability” and “mitigate the impact of global financial market uncertainty on the rupiah exchange rate and inflation outlook.”

The language was deliberate. BI described its monetary stance as “pro-stability” while keeping macroprudential and payment-system policies “pro-growth,” a formulation designed to signal that the central bank is not abandoning the economy, but that the exchange rate now comes first.

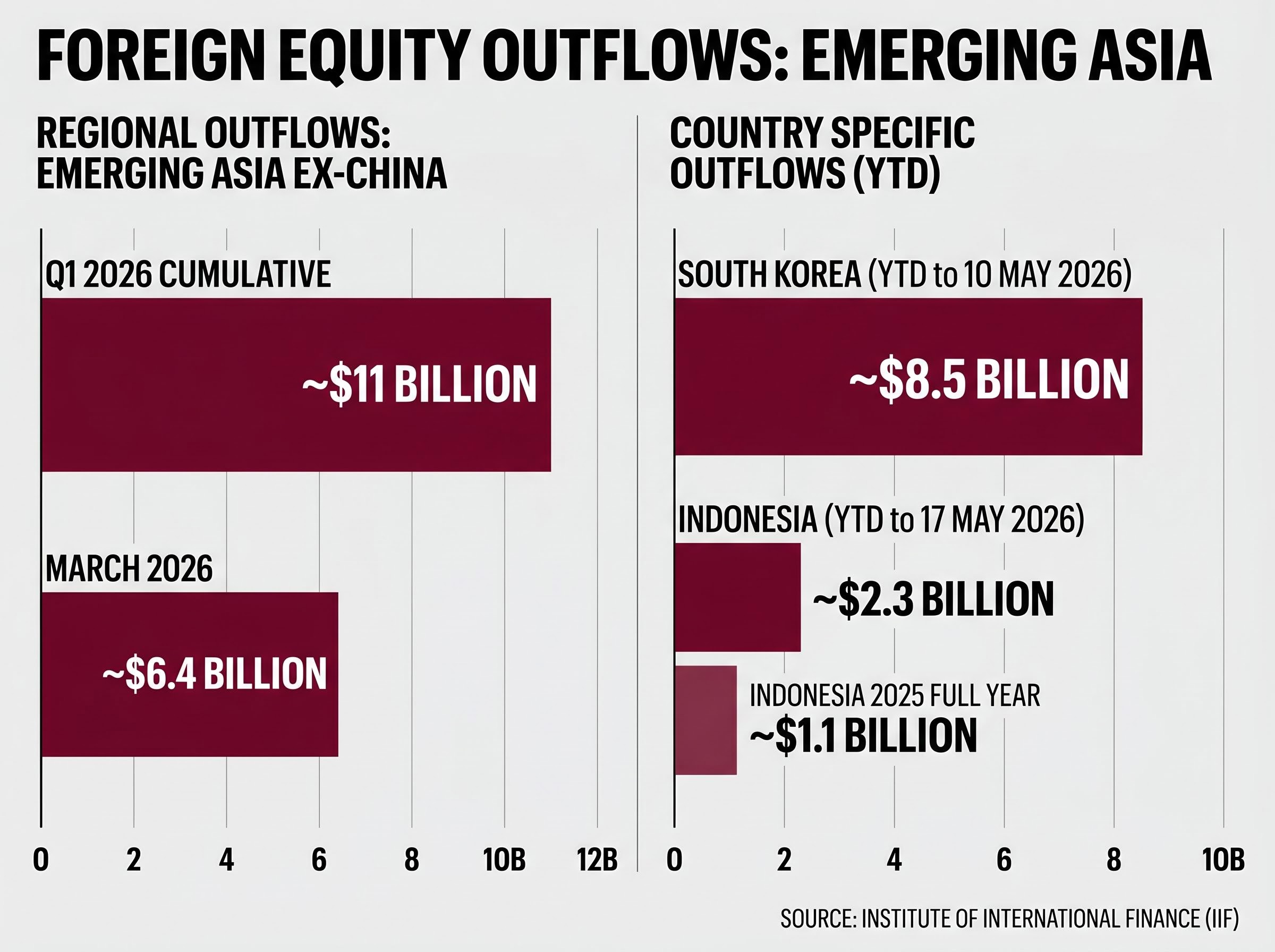

The rupiah’s weakness traces directly to the U.S. dollar. Elevated American interest rates have reduced the carry appeal of rupiah-denominated assets, driving capital reallocation toward U.S. markets. Foreign investors have been net sellers of approximately $2.3 billion in Indonesian equities year-to-date through 17 May 2026, accelerating from full-year 2025 net outflows of roughly $1.1 billion, according to IIF estimates.

Indonesia’s status as a net energy importer compounds the problem. Hormuz-linked crude price increases add a secondary inflation pressure that widens the current account deficit, weakening the rupiah from both the capital account and trade balance sides simultaneously.

The Strait of Hormuz handles a significant share of global seaborne oil. When tanker flows through that chokepoint are disrupted, the cost shock does not stay in the Middle East. It lands directly in the inflation calculations of Asia’s net energy importers: India, Indonesia, South Korea, and Japan.

The arithmetic is specific. War-risk insurance premia for Hormuz voyages have risen to approximately 1.5-2.0% of cargo value, up from 0.3-0.5% before the latest escalation. Freight rates for very large crude carriers (VLCCs) on Middle East-Asia routes are up roughly 30-40% compared with early 2025 levels. Refiners in Japan and South Korea are paying an additional $2-3 per barrel above earlier term-contract levels for spot cargoes, according to Nikkei Asia.

Higher delivered crude costs feed into domestic fuel prices and, through second-round effects, into broader consumer price inflation. This is precisely the channel that central banks are trying to close, and it operates independently of anything rate hikes can directly control.

Goldman Sachs has framed each additional period of constrained global commodity flows as offering “incremental support” to the U.S. dollar, compounding the currency pressure Asian central banks already face.

U.S. inflation dynamics, with April CPI rising to 3.8% driven largely by Hormuz-linked energy costs, have effectively removed near-term rate cut expectations from the Federal Reserve’s calendar, locking in the wide interest rate differential that is pulling capital away from Asian emerging markets and toward dollar-denominated assets.

| Economy | Net Energy Importer | Crude Cost Channel | CPI Sensitivity | Central Bank Response |

|---|---|---|---|---|

| India | Yes (major) | Higher freight and insurance on ME imports | Fuel and food price pass-through | RBI holding at 5.25%; monitoring second-round effects |

| Indonesia | Yes | Rising delivered crude costs widen trade deficit | Fuel subsidy pressure, imported inflation | BI hiked 50 bps to 5.25% on 20 May 2026 |

| South Korea | Yes | Spot cargo premia of $2-3/bbl above term levels | Energy input costs for manufacturing sector | BOK holding at 2.50%; discussing H2 tightening triggers |

The intuition behind a rate hike as currency defence is straightforward: higher rates increase the yield on local-currency assets, which attracts foreign capital inflows and puts upward pressure on the currency. When a central bank raises rates, it makes its bonds more competitive relative to alternatives elsewhere.

The complication is that this transmission weakens when the U.S. policy rate is materially higher. Even after Asian hikes, the interest rate differential still favours dollar assets, meaning the capital pull toward the U.S. does not reverse. According to the Asian Development Bank, monetary tightening can mitigate but not neutralise depreciation if the dollar remains structurally strong and energy prices are elevated.

Japan’s currency defence, which involved an estimated 8-9 trillion yen deployed during the Golden Week 2026 window and the likely liquidation of $40-50 billion in U.S. Treasury holdings to fund it, illustrates how the same dollar-energy configuration is forcing even the world’s third-largest economy into costly and structurally limited defensive manoeuvres.

For net energy importers, there is an additional problem: higher oil import bills widen current account deficits, a structural source of currency depreciation that rate hikes alone cannot address.

The conditions under which rate hikes effectively support currencies versus the conditions present in Asia now differ sharply:

As Capital Economics senior Asia economist Gareth Leather has argued, “additional tightening in Korea, India and Indonesia may stabilise FX in the near term but cannot fundamentally change the growth-dollar-oil configuration.”

Goldman Sachs projects the Bank of Korea (BOK), the Reserve Bank of India, and the Central Bank of the Republic of China (Taiwan) to enter tightening cycles later in 2026. Jakarta’s 50-basis-point move was the opening salvo; the next three are conditional.

BOK Governor Rhee Chang-yong has indicated the Board is “discussing the conditions under which additional tightening in the second half of 2026 could be warranted,” tying any move to sustained won weakness and upside inflation risk from energy. The BOK Base Rate sits at 2.50% after an April hold, with the next meeting expected around 28 May 2026.

RBI Governor Shaktikanta Das said it is “premature to talk about rate cuts,” with the policy repo rate held at 5.25% at the April MPC meeting. The RBI will act if second-round energy effects threaten the 4% CPI inflation target on a durable basis.

Taiwan’s CBC Governor Yang Chin-long said the bank “would not rule out further tightening later in 2026 if the Taiwan dollar weakens sharply.” The discount rate stands at 2.00% after a March hold.

The tightening is selective, not universal. Goldman Sachs projects Malaysia and Thailand to hold rates unchanged, creating a differentiated policy map within the region.

| Central Bank | Current Rate | GS 2026 Projection | Key Trigger Cited | Most Recent Decision |

|---|---|---|---|---|

| Bank Indonesia | 5.25% | Tightened (50 bps) | Rupiah defence, capital outflows | 20 May 2026 |

| Bank of Korea | 2.50% | Yes (H2 2026) | Won weakness, energy inflation | April 2026 (hold) |

| Reserve Bank of India | 5.25% | Yes (H2 2026) | Second-round energy effects on CPI | April 2026 (hold) |

| Taiwan CBC | 2.00% | Yes (H2 2026) | Sharp Taiwan dollar weakening | March 2026 (hold) |

| Bank Negara Malaysia | Hold | Hold | N/A | Hold |

South Korea has recorded approximately $8.5 billion in net foreign equity selling year-to-date through 10 May 2026. Across emerging Asia ex-China, Q1 2026 cumulative foreign equity outflows reached approximately $11 billion, according to the Institute of International Finance (IIF).

The structural tension facing Asian central banks is a three-way constraint with no clean exit:

Each rate hike carries a growth cost that is higher than it would be in a conventional tightening cycle. The central banks raising rates know this.

Joey Chew, Head of Asia FX Research at HSBC, has argued that FX-supportive rate hikes in Asia “can buy time but are unlikely to fully reverse depreciation against the dollar while U.S. yields are high and energy import bills are rising.”

One BOK board member put it plainly in the minutes of the 11 April 2026 meeting: “raising the Base Rate solely to counter exchange-rate depreciation has limited effectiveness when the depreciation is driven by a stronger dollar and higher global energy prices.”

The rate hikes are a holding action. They are not a resolution.

The equity outflow data tells a story that rate hikes have not yet reversed. Emerging Asia ex-China recorded approximately $6.4 billion in net equity outflows in March 2026 alone, described by the IIF as the largest monthly outflow since October 2023. Indonesia has lost roughly $2.3 billion year-to-date. South Korea has lost approximately $8.5 billion.

Emerging market equity outflows from Asia have been part of a broader defensive rotation: in the week ending 8 May 2026, approximately $136 billion moved into cash funds globally at the fastest pace since January 2026, with China-focused equity funds alone shedding roughly $47.5 billion over six consecutive weeks, a backdrop that contextualises why rate hikes have not yet slowed the selling.

Rate hikes raise local-currency bond yields, which increases funding costs for sovereigns and corporates but also improves the carry appeal of local-currency debt for investors willing to manage currency risk. The bond market calculus is not uniformly negative.

The policy divergence between tightening economies and holding economies creates risk profiles within Asian emerging markets that should not be treated as homogeneous. Three implications stand out:

The Asian Development Bank has recommended that fiscal measures and structural reforms accompany monetary tightening, a signal that rate hikes alone are not expected to stabilise the macro picture.

Bank Indonesia’s 50-basis-point hike is the opening move of a broader regional tightening cycle. Goldman Sachs projects three more central banks to follow in H2 2026. The direction is clear; the sufficiency is not.

The rate hike cycle is a necessary but incomplete response to the combined dollar-oil pressure. It buys time without resolving the underlying terms-of-trade and interest-rate-differential problems that continue to drive capital out of the region.

Three variables will determine how this cycle unfolds: the path of U.S. policy rates, the duration and severity of Hormuz shipping disruptions, and the pace of equity outflows from emerging Asia. None of those variables is under Asian central banks’ control. The policy tools are deployed; the structural forces remain unresolved.

For investors looking to translate the structural forces described here into portfolio positioning, our deep-dive into regime-aware portfolio construction examines how Bridgewater Co-CIO Bob Prince frames mercantilism and AI as twin forces reshaping global macro investing, including why the traditional 60/40 framework struggles under tariff-driven sticky inflation and why Asia requires country-level precision rather than a single regional allocation.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking projections, including Goldman Sachs forecasts and central bank guidance, are subject to change based on market developments and evolving macroeconomic conditions.

Asian central bank policy tightening refers to central banks raising interest rates to defend currencies and control inflation. For investors, it affects equity valuations, bond yields, and capital flows across emerging markets in the region.

Bank Indonesia raised its BI-Rate by 50 basis points to 5.25% on 20 May 2026 primarily to stabilise the rupiah against a strengthening U.S. dollar and to mitigate inflation risks linked to Strait of Hormuz shipping disruptions raising crude import costs.

Goldman Sachs projects the Bank of Korea, the Reserve Bank of India, and Taiwan's Central Bank to enter tightening cycles in the second half of 2026, driven by currency weakness, energy inflation, and persistent U.S. dollar strength.

Hormuz disruptions raise war-risk insurance premia and freight rates on crude shipments to Asia, pushing up delivered oil costs for net energy importers like India, South Korea, and Indonesia, which feeds into broader consumer price inflation and forces central banks to consider tightening.

Rate hikes raise local-currency bond yields and can improve carry appeal for debt investors, but they also slow domestic growth and have not yet reversed large equity outflows, with emerging Asia ex-China recording roughly $11 billion in cumulative foreign equity outflows in Q1 2026 alone.