SOL vs NWL: Matching the Right Metrics to Each Business

11 hrs ago

Bendigo and Adelaide Bank shares closed at $10.46 on 22 May 2026, trading at roughly 12x trailing earnings while the broader Australian banking sector averages approximately 18x. A six-multiple gap of that size is either a buying opportunity or a warning sign, and the answer depends on which valuation framework an investor trusts. With FY24 cash earnings per share (EPS) of $0.87 and a fully franked dividend of $0.63, BEN sits squarely in the crosshairs of yield-focused Australian investors hunting for income in a sector where the major four are widely described as fully valued. Two fundamental methodologies, the price-to-earnings (PE) ratio comparison and the dividend discount model (DDM), produce estimated fair values materially above the current market price. What follows works through both in detail, stress-tests their assumptions, and identifies where each can break down.

The starting point for any valuation exercise is the raw data. Four figures frame the BEN investment question:

That six-multiple discount to the sector average is large enough to demand explanation. In equity markets, a PE discount of this magnitude typically signals one of three things: the market expects earnings to deteriorate, it assigns a structurally lower quality premium to the business, or it has simply mispriced the stock relative to peers.

For BEN, the answer is unlikely to be a single explanation. Regional banks have traded at a structural discount to the majors for years, driven by lower returns on equity and higher cost-to-income ratios. Whether the current discount is larger than that structural gap justifies is the question both methodologies that follow attempt to answer.

The PE ratio measures what the market is paying per dollar of a company’s earnings. Divide the share price by EPS, and the result is the multiple investors are currently assigning to that earnings stream. A PE of 12x means investors pay $12 for every $1 of annual earnings. A PE of 18x means they pay $18.

Sector-comparative PE analysis extends this principle. If companies within the same industry share similar risk profiles, growth trajectories, and capital structures, their PE multiples should cluster within a comparable range. When one company trades at a material discount to its peers, multiplying its EPS by the sector average PE produces an estimate of what the stock would be worth if the market re-rated it to peer-group norms. The theoretical basis is mean reversion: the expectation that unjustified discounts tend to close over time.

Estimated fair value = EPS × sector average PE ratio

PE analysis has known limitations. It is backward-looking, relies on a single period’s earnings, and assumes the sector average itself is correctly priced. For bank stocks specifically, it works best as one input among several, not as a standalone verdict.

ASX bank stock valuation methods beyond PE and DDM include price-to-book ratios and discounted cash flow frameworks, each of which handles credit cycle volatility and regulatory capital requirements differently and can produce materially different conclusions when earnings are distorted by remediation charges or provisioning movements.

Applying the formula to BEN’s numbers is straightforward. FY24 cash EPS of $0.87 multiplied by the sector average PE of 18x produces an estimated fair value of $15.84 per share.

| Input | Value | Source |

|---|---|---|

| BEN FY24 cash EPS | $0.87 | FY24 full-year results (26 August 2024) |

| Sector average PE | 18x | Australian banking sector benchmark |

| Estimated fair value | $15.84 | EPS × sector PE |

Implied upside: approximately $5.38 per share, or roughly 51%, from the current price of $10.46.

The figure is striking. A 51% implied discount to sector-average valuation is not a rounding error. It is a gap wide enough to attract capital if the assumptions hold.

The critical qualifier: this estimate assumes the market would re-rate BEN fully to the 18x sector average. Regional banks have historically traded below the majors for structural reasons, including lower ROE, higher cost ratios, and more concentrated geographic exposures. A full re-rating to 18x may represent a theoretical ceiling rather than a realistic expectation; the question is how much of the gap is structural and how much is opportunity.

The DDM offers a second, independent lens. Where PE analysis asks what the market is paying for earnings, the DDM asks what a stream of future dividends is worth in today’s dollars.

Share value = annual dividend ÷ (discount rate − dividend growth rate)

This framework is considered well-suited to bank stocks given their mature, dividend-led return profiles. Banks that distribute a high proportion of earnings as dividends, as BEN does, lend themselves to a model that values precisely that cash flow stream.

The dividend discount model for ASX income stocks is structurally best suited to sectors where regulatory constraints and established payout histories produce predictable dividend streams, which is precisely why banks, REITs, utilities, and infrastructure companies dominate DDM application in Australian equity analysis.

BEN’s dividends are 100% franked, which means the $0.63 cash dividend per share converts into a $0.93 gross dividend for eligible Australian tax-resident shareholders with unused franking credits. This materially shifts the DDM output toward the upper end of the valuation range, though this benefit is specific to eligible Australian investors and is not universal.

The ATO franking credit rules for individuals set out the eligibility conditions under which resident shareholders can convert imputation credits into refundable tax offsets, a distinction that directly determines whether the $0.93 gross dividend figure applies to a given investor’s position.

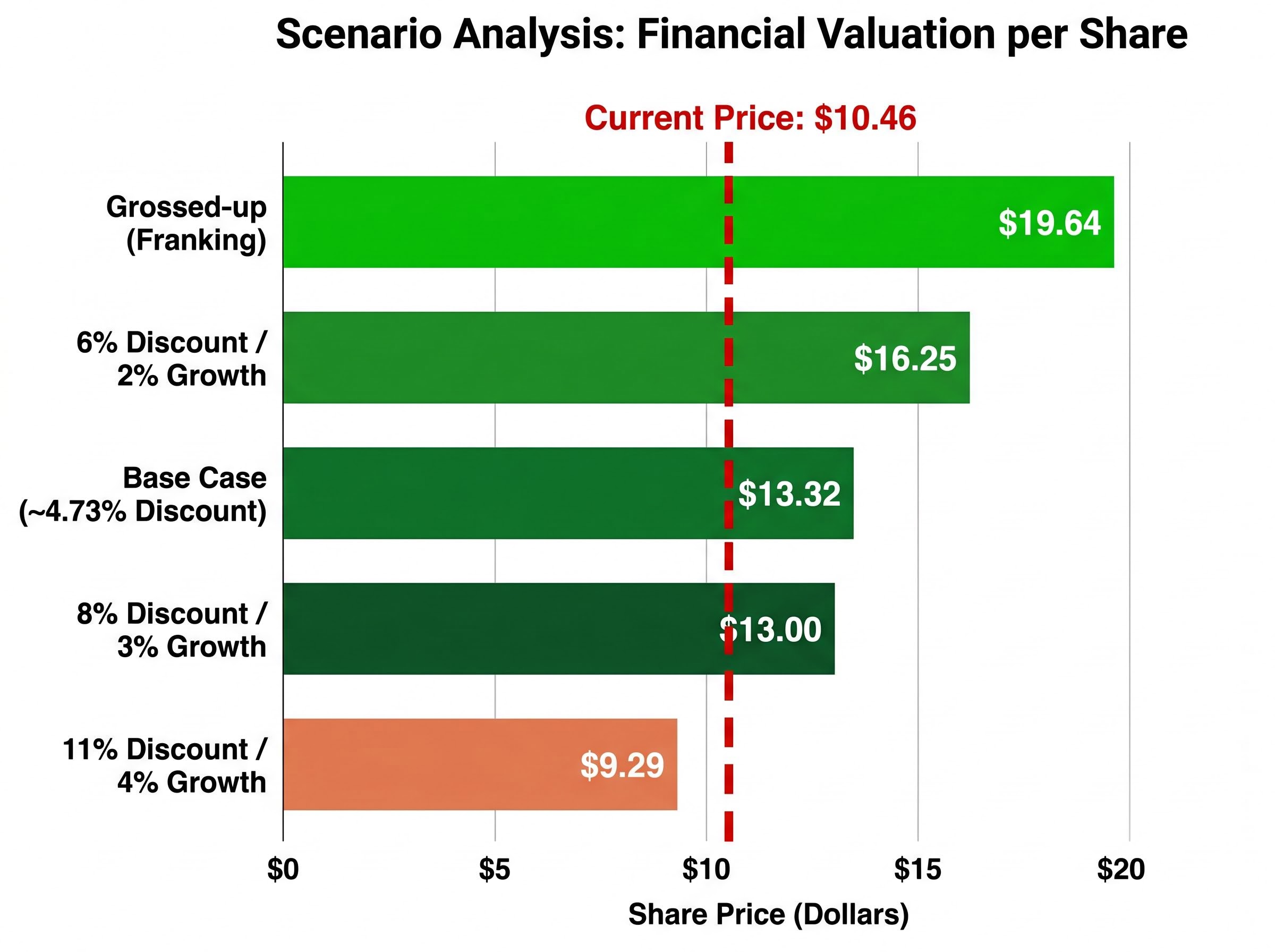

Three core DDM scenarios emerge from the analysis, supplemented by sensitivity testing across a range of discount rate and growth rate assumptions:

| Discount Rate | Growth Rate | Estimated Value | vs Current Price ($10.46) |

|---|---|---|---|

| ~4.73% (base case) | Implied | $13.32 | +27% |

| Adjusted forecast | Implied ($0.65 dividend) | $13.75 | +31% |

| Grossed-up (franking) | Implied ($0.93 gross) | $19.64 | +88% |

| 6% | 2% | $16.25 | +55% |

| 8% | 3% | $13.00 | +24% |

| 11% | 4% | $9.29 | −11% |

The sensitivity range tells the story. At a 6% discount rate and 2% growth, the model produces $16.25, comfortably above the current price. At 8% and 3%, the estimate falls to $13.00 but still implies meaningful upside. At 11% and 4%, the output drops to $9.29, below the current price.

The spread from $9.29 to $19.64 is not a flaw in the model. It is the model doing its job: showing how dramatically the conclusion shifts depending on the discount rate an investor applies and whether franking credits are incorporated.

Both methodologies point to upside. Neither should be taken at face value without understanding where the assumptions can fail.

At an 11% discount rate and 4% growth rate, the DDM produces an estimated value of $9.29, below the current BEN share price of $10.46. The models do not universally support upside.

The source analysis recommends supplementing quantitative models with qualitative research: reviewing at least three years of annual reports, assessing management communication quality, and actively seeking analyst views that challenge the investment thesis.

A qualitative checklist for bank investors covering management quality, capital adequacy, loan book concentration, macroeconomic sensitivity, revenue mix, and operational resilience is what transforms a DDM output from a number into a defensible investment thesis, because those six dimensions determine whether the assumptions driving the model are likely to hold.

Both methodologies converge on the same directional signal. PE analysis points to approximately $15.84. The central DDM scenarios cluster between $13.32 and $13.75 in cash terms, rising to $19.64 on a grossed-up basis for eligible Australian investors. All sit meaningfully above the current $10.46 price.

| Methodology | Estimated Fair Value |

|---|---|

| PE ratio (sector comparative) | $15.84 |

| DDM base case ($0.63 dividend) | $13.32 |

| DDM adjusted ($0.65 dividend) | $13.75 |

| DDM grossed-up (franking credits) | $19.64 |

Two distinct investor profiles emerge. The income-focused investor prioritises BEN’s approximately 6.0% fully franked yield at the current price, a figure that grosses up materially for those with unused franking credits. The capital-appreciation investor focuses on the PE re-rating thesis, betting that some portion of the six-multiple discount to the sector will close over time. Both cases depend on different assumptions holding true.

The convergence of two independent methodologies around a fair value range above the current price is the strongest quantitative signal this analysis produces. Convergence alone, however, is not a buy signal. It is an invitation to dig deeper: into management quality, annual reports, and bear-case analyst perspectives.

Both the PE ratio and the DDM, across a range of reasonable assumptions, produce estimated fair values above $13 and as high as $19.64. All sit above the current $10.46 price. The signal is consistent; the assumptions are not guaranteed.

The regional bank discount, the sensitivity of DDM outputs to discount rate assumptions, and a 72% payout ratio are factors that could prevent or delay a re-rating. These quantitative models provide a structured starting framework, not a conclusion. Layering in qualitative research on management quality, annual report review, and stress-testing assumptions against bear-case perspectives remains the necessary next step before any capital allocation decision.

For investors ready to move beyond the single-stage DDM and into the balance sheet metrics that drive whether BEN’s earnings assumptions hold up quarter to quarter, our deep-dive into NIM, provisioning, and funding risk for ASX banks walks through loan impairment expense trends, deposit-to-wholesale funding ratios, and the five-priority due diligence checklist that practitioners apply before acting on any bank valuation number.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

BEN share price closed at $10.46 on 22 May 2026, implying a PE ratio of approximately 12x against an Australian banking sector average of around 18x, a six-multiple discount to peers.

By multiplying BEN's FY24 cash EPS of $0.87 by the sector average PE of 18x, the estimated fair value comes to $15.84 per share, approximately 51% above the current market price.

BEN's fully franked $0.63 dividend grosses up to $0.93 for eligible Australian tax-resident investors, lifting the DDM estimated fair value to $19.64 compared to $13.32 using the cash dividend alone.

At an 11% discount rate and 4% growth rate, the dividend discount model produces an estimated value of $9.29, which is below the current BEN share price of $10.46, illustrating how sensitive the model is to rate assumptions.

The key risks include a structural discount that regional banks have historically carried relative to the majors due to lower ROE and higher cost-to-income ratios, a high payout ratio of around 72% that may constrain dividend growth, and a higher-for-longer interest rate environment that compresses DDM estimates.