Two covered call ETFs can advertise the same 12% headline yield, yet one investor pays tax on the full distribution every year while the other pays nothing until they sell. The difference has nothing to do with the fund’s performance and everything to do with how the distribution is classified on a Canadian T3 slip. Covered call ETF distributions in Canada can be split into up to five distinct tax categories, and the mix between them determines the real after-tax return, not the number on the fund’s marketing page. This guide explains exactly how each T3 category is taxed, how return of capital erodes an investor’s adjusted cost base and creates a deferred obligation, how tax efficiency shifts depending on income level, and what to look for when comparing real fund examples. The capital gains inclusion rate remains at 50% as of mid-2026 following cancellation of previously proposed changes.

Prime Minister Carney’s cancellation of the proposed inclusion rate increase, announced in March 2025, confirmed that the 50% capital gains inclusion rate remains in effect, preserving the tax advantage that capital gains distributions hold over fully taxable foreign income for covered call ETF investors.

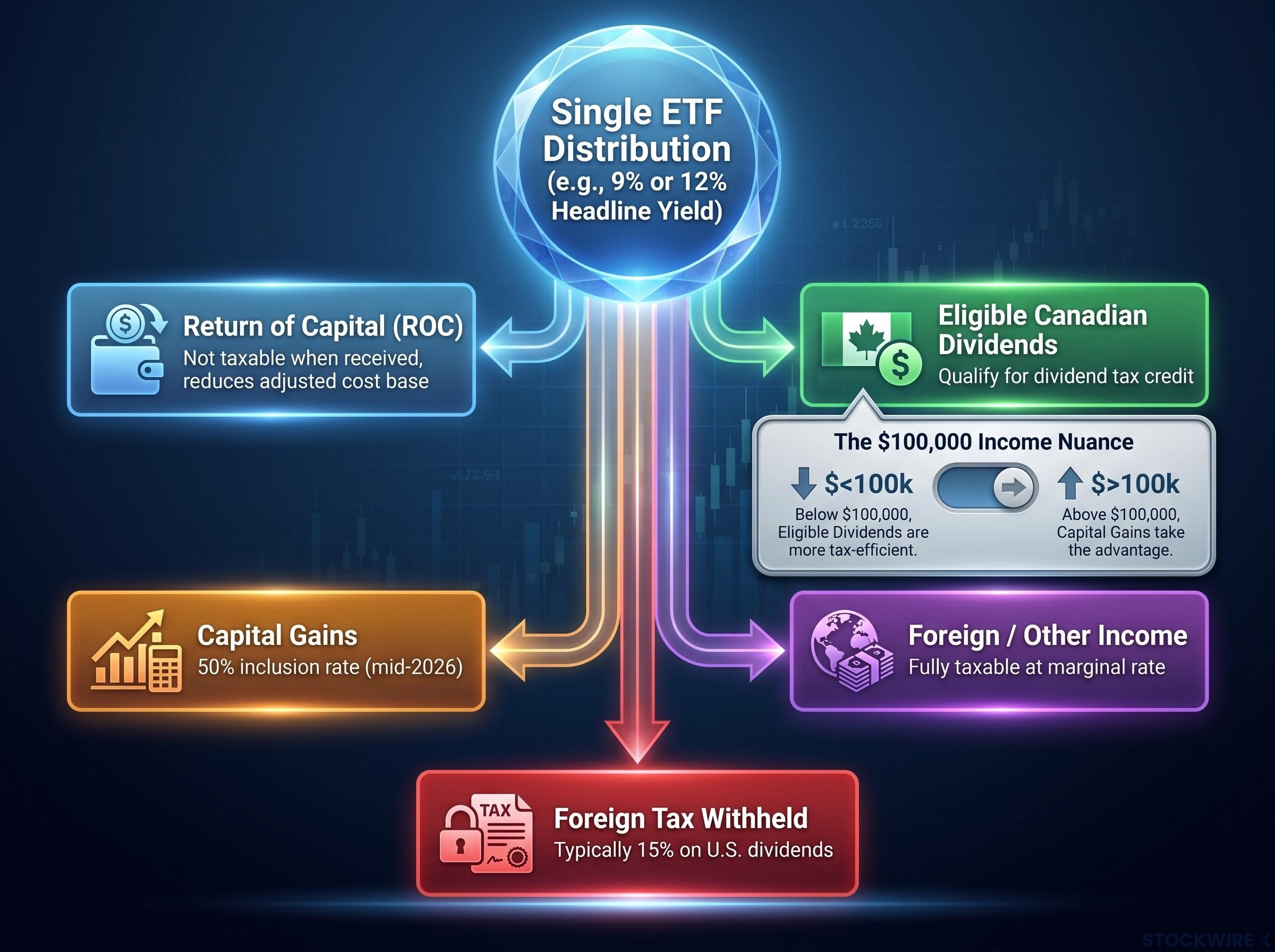

The five ways a covered call ETF distribution can be taxed in Canada

The word “distribution” implies a single cash flow. In practice, a Canadian T3 slip for a covered call ETF breaks that cash flow into up to five separate tax events, each with a different consequence:

- Return of capital (ROC): Not taxable when received. Reduces the investor’s adjusted cost base, deferring tax until units are sold.

- Eligible Canadian dividends: Qualify for the federal and provincial dividend tax credit, producing a lower effective tax rate than ordinary income.

- Capital gains distributions: Only 50% of the gain is included in taxable income under the current inclusion rate.

- Foreign income / other income: Fully taxable at the investor’s marginal rate, the same as employment income or GIC interest.

- Foreign tax withheld: Tax deducted at source by a foreign government (typically 15% on U.S. dividends under the Canada-U.S. tax treaty) before the fund receives the income. A foreign tax credit may partially recover this in a taxable account, but inside registered accounts the drag is generally permanent.

The mix between these categories can shift from year to year for the same fund. Tax breakdowns across 2023, 2024, and 2025 have shown meaningful variation for several popular covered call ETFs. ETFs investing exclusively in Canadian equities will never carry foreign income or foreign tax withheld line items, while U.S.-focused funds almost always will.

Which category is the most tax-efficient?

The general ranking from most to least tax-efficient for a Canadian investor holding units in a taxable account is: ROC first, then capital gains, then eligible dividends, then foreign or other income, with foreign tax withheld as the largest drag.

One income-level nuance shifts that order. Below approximately $100,000 in annual income, eligible dividends typically rank above capital gains because the dividend tax credit produces a lower effective rate at those brackets. Above approximately $100,000, capital gains become comparably or more tax-efficient than eligible dividends, as the fixed 50% inclusion rate holds its advantage while the dividend gross-up can push income into higher brackets.

When big ASX news breaks, our subscribers know first

Beyond Yield: Overlooked Factors Affecting Real Returns

Three distinct drags erode the real return from a covered call ETF. They differ in one way that matters: visibility.

- Fee drag (visible): The management expense ratio (MER) and trading costs reduce total return every year. This drag appears in the fund’s reported performance; investors see it reflected in NAV.

- Strategy drag (visible): The covered call overlay caps upside when markets rise strongly, and distribution targets that exceed portfolio income can erode NAV over time. This drag also appears in reported total return figures.

- Tax drag (invisible): The after-tax return sits below the headline yield because of the character of the distributions. Annual tax payments on foreign income or other income reduce capital available for reinvestment. This drag occurs privately in the investor’s own account and never appears in any reported performance figure.

Fee drag and strategy drag are priced into the returns an investor reads on a fact sheet. Tax drag is not. It compounds silently: every dollar paid in annual tax on distributions is a dollar that cannot be reinvested to purchase more units and generate additional income.

The confusion between yield versus total return is the foundational error that makes headline distribution figures misleading: a fund can sustain a high yield for years while its NAV silently declines, leaving investors with less capital than they started with despite receiving regular cash payments.

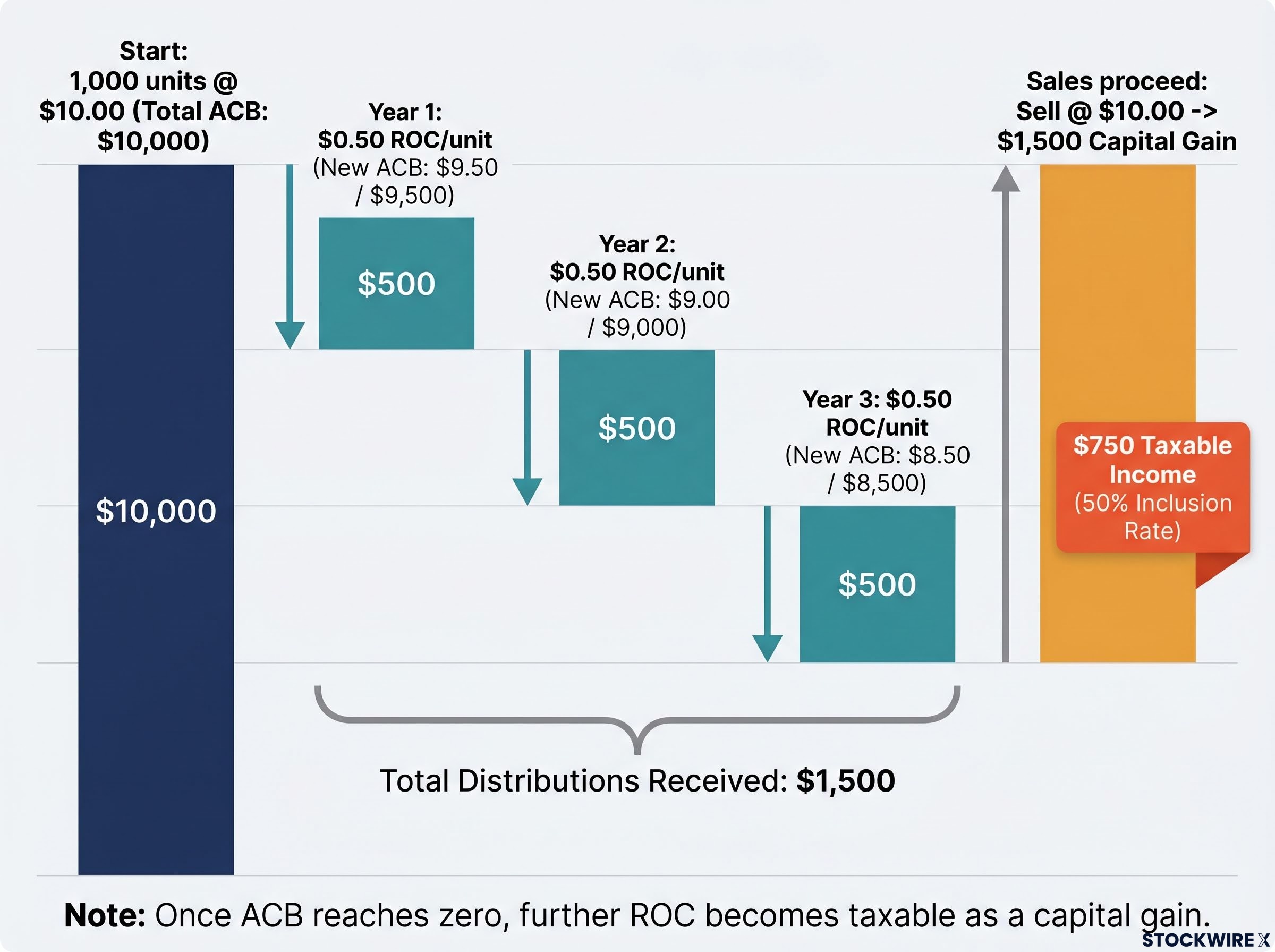

How Return of Capital Impacts Your Cost Base

Return of capital is the portion of a distribution that exceeds a fund’s taxable income for the period. When an investor receives ROC, no tax is owed in that year. The distribution does not appear as income on a tax return.

What happens instead is mechanical. Each dollar of ROC reduces the investor’s adjusted cost base (ACB) by exactly one dollar. The tax obligation does not disappear; it moves forward in time, accumulating quietly until the investor sells.

Consider an investor who purchases 1,000 units at $10.00 per unit, for an initial ACB of $10,000. The ETF pays $0.50 per unit per year, all classified as ROC.

| Year | ROC per unit | Cumulative ROC per unit | ACB per unit | Total ACB |

|---|---|---|---|---|

| Start | — | — | $10.00 | $10,000 |

| 1 | $0.50 | $0.50 | $9.50 | $9,500 |

| 2 | $0.50 | $1.00 | $9.00 | $9,000 |

| 3 | $0.50 | $1.50 | $8.50 | $8,500 |

Three years pass. The investor has received $1,500 in distributions and paid zero tax on them. If they sell in Year 3 at $10.00 per unit, their capital gain is $1.50 per unit (sale price of $10.00 minus ACB of $8.50). On 1,000 units, that produces a $1,500 capital gain. At the 50% inclusion rate, $750 is added to taxable income.

The deferral benefit is real: the investor controlled more capital during the holding period, which could compound if reinvested. But the tax bill has not vanished. It has been converted from fully taxable income (if the distributions had been classified as foreign income) into a capital gain taxed at a preferential rate.

ROC is a tax deferral mechanism, not tax elimination. The obligation accumulates as ACB declines and is realised when units are sold, at capital gains rates rather than as fully taxable income.

One additional rule matters: once ACB reaches zero, any further ROC distributions become taxable as a capital gain in the year received, because the cost base cannot go negative.

How covered call ETFs generate income and why so much of it is classified as return of capital

A covered call ETF produces cash flow from two sources:

- Dividends from the underlying stocks (Canadian or foreign), which flow through to unitholders as eligible dividends or foreign income depending on the stock’s domicile.

- Option premiums from writing call options on those stocks, which generate immediate cash but cap the upside if the underlying shares are called away above the strike price.

At the fund level, option premiums are generally treated as capital in nature. When the fund sets a regular monthly distribution target that exceeds its current taxable income for the period, the excess is mechanically classified as return of capital. Fund managers may also incorporate tax-loss harvesting within the portfolio, further contributing to the ROC classification.

Academic research on option premium tax treatment in Canada has established that premiums received from writing exchange-traded covered call options are treated as capital in nature by Canadian tax authorities, which is the structural reason why high ROC percentages are a recurring feature of covered call ETF distributions rather than a year-specific anomaly.

This is why high ROC percentages in covered call ETFs are often structural and deliberate rather than a one-year anomaly. The combination of capital-natured option income, managed distribution targets, and internal tax planning produces a distribution profile designed for tax deferral.

The covered call ETF structure that determines whether option income is classified as return of capital or ordinary income traces back to the fund’s underlying mechanism: funds using FLEX options can generally achieve capital treatment, while funds using equity-linked notes tend to generate ordinary income that is taxed immediately at the investor’s marginal rate.

Why this matters more in a taxable account than in a registered account

Inside a Tax-Free Savings Account (TFSA), all distribution types are irrelevant for personal tax purposes. However, foreign withholding tax on U.S. dividends held within a TFSA is generally unrecoverable, creating a permanent drag on U.S.-focused funds.

Inside a Registered Retirement Savings Plan (RRSP), distributions are not taxed when received, but all withdrawals are fully taxable as ordinary income. U.S. withholding on ETF distributions inside an RRSP is also typically unrecoverable for Canadian-listed ETF structures.

The full five-category tax distinction matters most when holding covered call ETFs in a non-registered account, where each T3 line item directly affects the investor’s annual tax liability.

Illustrative Examples: How Funds Show Different Tax Mixes

Hamilton ETFs offers two products that illustrate how dramatically tax outcomes can diverge, even under the same manager. Hamilton Enhanced U.S. Covered Call ETF (HYLD) is an equity-based covered call ETF. HBELL is a T-bill focused maximiser fund. Both target high yields, but the underlying asset classes produce entirely different T3 profiles.

| Metric | HYLD | HBELL |

|---|---|---|

| Return of capital | ~100% | ~30% |

| Foreign tax withheld | 0% | ~7% |

| Foreign income | 0% | ~55% |

| YTD total return | ~13.53% | ~1.27% |

The gap between HYLD’s approximate 13.53% total return and HBELL’s approximate 1.27% total return underscores a broader pattern: tax efficiency and total return often move in the same direction. A cleaner distribution profile frequently accompanies stronger underlying fund economics.

HYLD’s approximately 100% ROC classification means no immediate tax liability was triggered from distributions in the 2025 tax year. HBELL, by contrast, allocated roughly 55% of its distributions as foreign income (fully taxable at the marginal rate) and approximately 7% as foreign tax withheld.

A Canadian-equity-focused example adds further context. HMAX (Hamilton Canadian Financials Yield Maximizer ETF) distributes only ROC and eligible dividends, with no foreign income components, because its holdings are exclusively Canadian equities. Multiple covered call ETFs from Global X and Hamilton ETFs showed 100% ROC classification in 2025 tax year data.

The implication is direct: a lower headline yield with a cleaner tax profile can produce a better after-tax outcome than a higher yield dominated by foreign income.

A practical checklist for selecting tax-efficient covered call ETFs in a taxable account

The following steps form a repeatable evaluation process for any covered call ETF under consideration:

- Check the last two to three years of distribution tax breakdowns on the provider’s website or from past T3 slips. Specifically, look for:

- The percentage classified as return of capital

- The split between capital gains and eligible dividends

- The allocation to foreign income or other income

- Any foreign tax withheld

- Review the underlying holdings geography. Mostly Canadian dividend stocks typically means eligible dividends and ROC with no U.S. withholding. Mostly U.S. or global stocks typically means foreign income and withholding tax will appear on the T3.

- Compare after-tax yield, not headline yield. A fund advertising 9% with 80% ROC and 20% capital gains can deliver more after tax than a fund advertising 12% where most distributions are foreign income.

- Review total return (price plus distributions) over time, not just the current yield. A high yield means little if NAV is declining faster than the income being paid.

NAV erosion in covered call ETFs is most acute in concentrated single-stock strategies, where distribution yields of 18-25% can mask annual capital base declines of 5-10%, making the comparison between headline yield and total return particularly stark for investors who rely on screener data rather than full fund performance records.

- Confirm that the tax profile is reasonably consistent across years. Funds that flip unpredictably between high ROC one year and high foreign income the next make tax planning difficult and signal an unstable distribution structure.

The after-tax comparison principle: A 9% yield that is 80% ROC and 20% capital gains can be more attractive after tax than a 12% yield that is mostly foreign income. Headline yield is not after-tax yield.

Red flags for taxable investors include large recurring allocations to foreign income, significant foreign tax withheld (particularly if the fund is held in a registered account where that credit is unrecoverable), and highly volatile tax characterisation from year to year.

The after-tax return is the only return that matters

Headline yield is a marketing number. After-tax return, adjusted for fee drag, strategy drag, and the invisible tax drag created by distribution character, is the number that determines long-term wealth accumulation. Two funds with identical reported yields can produce materially different after-tax outcomes depending on how their distributions are classified on a T3 slip.

Investors holding or considering covered call ETFs in non-registered accounts should apply two disciplines consistently: track the adjusted cost base as ROC distributions accumulate, and review the distribution tax breakdown across multiple years before selecting or retaining a fund.

Leveraged covered call ETFs extend the same tax deferral logic further by combining 1.25x equity exposure with a call-writing overlay, producing distribution yields that have exceeded 13% in live trading while maintaining a portfolio delta of approximately 0.92, though the leverage component introduces borrowing costs that interact with the tax treatment in ways a standard covered call structure does not.

Tax outcomes depend on province, income level, account type, and personal circumstances. A qualified tax professional or financial planner should be consulted before making investment decisions based on tax treatment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.